SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

When a major hurricane kills hundreds or thousands of people made vulnerable by the Trump administration’s unprecedented assault on weather forecasting and disaster planning, Democrats shouldn’t hesitate to blame those casualties on Trump.

The United States dodged a bullet when Hurricane Erin veered away from its coastline. Put differently, we were lucky enough to survive another round in the game of Russian roulette that President Donald Trump is playing with our lives. But the next hurricane could be the loaded chamber. Or the one after that, and so on. On August 25, more than 180 Federal Emergency Management Agency (FEMA) workers sounded the alarm, writing in an open letter that the Trump administration’s actions are putting us at risk of a Katrina-scale disaster. On August 26, dozens of those FEMA whistleblowers were placed on administrative leave.

When a major hurricane kills hundreds or thousands of people made vulnerable by the Trump administration’s unprecedented assault on weather forecasting and disaster planning, Democrats shouldn’t hesitate to blame those casualties on Trump, Elon Musk, and other Republican figures who are making preventable deaths inevitable. If they fail to hold Trump and his MAGA regime accountable, the president’s 2016 quip that he could “shoot somebody” and not “lose any voters” will sound even more prophetic than it already does. It sounded absurd when Trump first uttered it, and yet he keeps getting away with murder, in part due to Democrats’ self-defeating reluctance to punch fast, hard, and often.

Erin’s arrival served as a potent reminder, following a quiet June and July, that we’ve entered the peak of the Atlantic hurricane season. Meteorologists still expect a “slightly above-average probability” for major storms making landfall along the U.S. coastline and in the Caribbean for the remainder of the season, which lasts until the end of November. Just before Erin became this year’s first Atlantic hurricane, forecasters predicted 12 more named storms—including eight hurricanes, three of which were projected to be “major,” i.e., category 3 or higher—over the next few months. Historically, hurricane activity in the Atlantic basin picks up from August through mid-October. That’s the time frame when Hurricanes Katrina, Sandy, Harvey, Irma, Maria, Ida, Ian, Helene, and Milton—and many more besides—struck.

Thankfully, Erin didn’t hit the U.S. mainland, though its passage through the Caribbean knocked out electricity for nearly 150,000 people in Puerto Rico. Even as Erin remained offshore, the powerful and remarkably wide hurricane generated life-threatening surf and rip currents along the entire Eastern Seaboard, prompting storm alerts of various kinds in 15 states, from Florida to Maine. Coastal flooding was particularly severe in North Carolina and New Jersey.

Erin transformed from a tropical storm into a Category 5 hurricane in roughly 24 hours—making it one of the most rapidly intensifying cyclones ever—before eventually weakening as it moved north and east. Erin exemplifies an increasingly common kind of storm—one turbocharged by two centuries of unmitigated planet-heating pollution driven primarily by the burning of fossil fuels. The hurricane’s rapid intensification was propelled by unusually warm ocean waters, which are a consequence of rising global greenhouse gas emissions. Through their ongoing war on climate research and clean energy, Trump and congressional Republicans—bankrolled by the fossil fuel industry—have ensured that more heat-trapping gasses will be pushed into the atmosphere while fewer scientists and regulators will be around to monitor, let alone mitigate, the impacts.

We’re due for seven more hurricanes, including two big ones, over the next dozen weeks or so. That means Trump’s FEMA, which admitted internally in May that it was unprepared for hurricane season, is beefing up its disaster response capacities, right? No. Instead, the Department of Homeland Security (DHS) has been forcibly reassigning FEMA employees to Immigration and Customs Enforcement (ICE) in a bid to bolster Trump’s cruel push to terrorize, detain, and deport as many migrants as possible.

A federal judge recently ordered the closure of Trump’s sadistic immigration jail in the Everglades within 60 days (two cheers for environmental review!), but if a hurricane hits Florida before then, it would likely be a mass casualty event; one suspects that this is what Trump, DHS Secretary Kristi Noem, White House adviser Stephen Miller, and other fascists want. Noem’s efforts to prevent disaster aid from reaching undocumented immigrants underscores why disaster experts have long advocated for reestablishing FEMA as an independent, Cabinet-level agency free from DHS interference.

Meanwhile, the National Weather Service (NWS) has been scrambling to hire back hundreds of workers pushed out months ago by Musk’s so-called Department of Government Efficiency (DOGE). These developments—really just the tip of the iceberg—epitomize the Trump administration’s utter disregard for the lives of people who will be harmed by severe weather, which is destined to grow in frequency and intensity thanks to the GOP megabill signed into law by Trump, and other reactionary White House moves.

It’s incredibly fortunate that no hurricanes have made landfall in the U.S. so far this year. That’s because the Trump administration’s wide-ranging attacks on federal and state officials’ capacity to understand, prepare for, withstand, and recover from extreme weather events have dramatically increased the likelihood of mass harm. But this serendipity is all but guaranteed to end soon, and when it does, many people will die needlessly. When that happens, will Democrats have the guts to blame Trump and his Republican accomplices?

Congressional Progressive Chair Greg Casar (D-TX) probably will. Last month, he secured an independent investigation into how Trump’s gutting of the National Oceanic and Atmospheric Administration (NOAA) may have undermined the response to deadly floods in central Texas that began on July 4. Last week, Casar and Rep. Joe Neguse (D-CO) introduced bills to reverse Trump’s gutting of FEMA and NOAA, respectively. Given that Republicans control both chambers of Congress and the White House, this legislation has a near-zero chance of being enacted. However, it does offer good messaging opportunities if a critical mass of Democrats consistently raise hell about Trump’s myopic cuts—before, during, and after potential calamities.

Casar is an exception. The Democratic Party’s generalized timidity in the wake of the Trump administration’s abysmal response to the Texas flooding disaster does not inspire confidence. Democratic leaders’ hesitancy to politicize disasters—that is, to hold relevant decision-makers accountable for creating the conditions for catastrophe—was also evident last fall in Kamala Harris and Tim Walz’s refusal to connect the dots between right-wing policymaking and the devastation of Helene and Milton. This is a dynamic that has to change; for the sake of our collective future, Trump’s critics must make Republicans loyal to Trump pay a political price for routinely putting Americans in harm’s way—and prematurely ending some of our lives.

It’s impossible to overstate how much damage Trump has done in just seven months. For an in-depth exploration of the lethal consequences of the administration’s war on NOAA and FEMA, see our new report, Trump’s Homicidal Hurricane Policy.

As hurricane season kicks into full gear, the adverse impacts of the Trump administration’s mutilation of NOAA are still coming into view, but we know they will be cumulative and devastating. Last month, in its first big test, Trump’s hollowed-out FEMA failed miserably. I’m referring, of course, to the administration’s inept response to the early July floods in Central Texas, which killed more than 130 people and provided tragic confirmation that dismantling the agency is a grave mistake.

During his July 23 testimony before a House committee, Acting FEMA Director David Richardson, who waited nine days to visit Texas, called the Trump administration’s response a “model of how disasters should be handled.” Richardson’s outlandishly positive interpretation of events is diametrically opposed to the candid assessment of an on-the-ground FEMA worker, who warned that “if this is how they are going to do a major hurricane response, people are fucked.”

Today, August 29 marks the 20th anniversary of Hurricane Katrina’s landfall. Experts warned weeks ago that Trump and Musk’s war on NOAA and FEMA has left the United States ill-prepared for another storm of that magnitude. Scores of FEMA workers raised the alarm again on August 25 and were summarily disciplined.

Let’s imagine that, sometime in the next few months, the Gulf Coast or the Atlantic Coast is hit by one massive category 5 hurricane, or perhaps the country endures two big storms back-to-back. This isn’t hard to envision; last October, Milton hammered Florida just days after Helene rocked North Carolina. Last time Trump was in the White House, in 2017, Harvey, Irma, and Maria devastated Texas, Florida, and Puerto Rico, respectively, in the span of a few weeks.

Now imagine if, as numerous communities are inundated in the wake of a hurricane, several new wildfires break out across the drought-stricken West, and another deadly heat wave envelops tens of millions of people around the country. Then the mortal consequences of ripping our already-threadbare disaster preparedness and response infrastructure to shreds will become even more painfully evident. As risks compound and failures cascade (e.g., hospitals flood and flames engulf toxic superfund sites), Trump’s madness will become even clearer. But this will only matter politically if people make a big deal of everything the Trump administration and Musk’s DOGE vandals are doing to increase the odds of preventable suffering and death.

The question is whether Democrats will capitalize on Trumpified disasters, in a way that echoes how FDR and his allies made Herbert Hoover infamous for his woefully inadequate response to the Great Depression. Sharp political rhetoric (e.g., Hoovervilles) and, more importantly, popular New Deal policies that improved people’s lives in sharp contrast to Republicans’ destructive market fundamentalist model, discredited the GOP and led to two generations of Keynesian hegemony. The task at hand requires going beyond one-off denunciations; it would entail months- or years-long campaigns to villainize specific officials and policies responsible for causing preventable suffering while offering just alternatives.

It’s worth noting that the worst-case scenario might not materialize this year. While the attacks I summarized in Trump’s Homicidal Hurricane Policy have already unleashed significant damage, the long-term consequences of his actions will become clearer over time; unfortunately, things are poised to get even worse moving forward.

Recall that Trump said he plans to “phase out” FEMA after this year’s hurricane season. An April 12 memo from then-Acting FEMA Administrator Charles Hamilton discussed how Trump could make it tougher for communities to qualify for federal disaster assistance. The memo suggested quadrupling the damage threshold a state would need to meet to qualify for public assistance, and it also recommended keeping the federal cost share for disaster recovery from surpassing 75 percent. An Urban Institute analysis found that if these proposed changes had been in effect, 71 percent of major disasters declared from 2008 to 2024 would not have qualified, and state and local governments would have missed out on $41 billion in aid. Hamilton’s “Abolish FEMA” memo, shared on March 25, outlined other ways to shrink the federal government’s role in disaster response.

Despite being directly responsible for delaying the response to the deadly Texas floods, Noem still had the gall to criticize FEMA for being “slow to respond at the federal level,” adding that “this entire agency needs to be eliminated as it exists today, and remade into a responsive agency.” But it appears that what the Trump administration has in mind is still a devolution of responsibility to state and local officials, even though only the federal government is capable of coordinating effective disaster mitigation and response efforts. It will be important to keep a close eye on the forthcoming recommendations from the FEMA review council, which is “doing Trump’s bidding” to dismantle the agency, according to Shana Udvardy, senior climate resilience policy analyst at the Union of Concerned Scientists.

The Texas flooding disaster doesn’t appear to have changed Trump’s mind about gutting NOAA. In May, OMB Director Russell Vought requested a roughly 25 percent cut to NOAA’s budget for fiscal year 2026, which begins on October 1. The White House’s proposal would wipe out nearly all of the agency’s earth system science and shutter world-class climate research offices around the country. A more detailed proposal released at the end of June shed additional light on the catastrophic scale of the Trump administration’s plans.

As meteorologist Michael Lowry explained, Trump’s budget would eliminate “all federally funded meteorological, oceanographic, and climate labs and non-profit cooperative research institutes across America.” The proposed cuts would shut down “Miami’s Atlantic Oceanographic and Meteorological Laboratory and its Hurricane Research Division, institutions responsible for most of the advancements in hurricane forecasting and science over the past 50 years,” Lowry lamented. “With the proposed shuttering of AOML, HRD, and their sister cooperative institutes starting in 2026, forecasters could lose all tools currently available to estimate and forecast hurricane intensity,” he added. “It’s a seismic blow to the arsenal of tools forecasters rely on to confidently deliver timely and accurate predictions of threatening hurricanes.”

Also on the chopping block is NOAA’s National Severe Storms Laboratory in Norman, Oklahoma. Jeff Masters pointed out that the closure of this lab, opened in 1964, would “significantly degrade our ability to improve flash flood forecasting,” meaning more calamities of the sort we saw recently in Texas.

To date, congressional appropriations committees have largely rejected the draconian cuts sought by Trump and Vought. The spending bill advanced by House lawmakers would still reduce NOAA’s budget by 6 percent, a detrimental and unnecessary blow, while the version advanced by the relevant Senate panel would fund NOAA at nearly the same level as 2025. Nevertheless, the Republican-led rescissions package that Trump signed into law last month included deleterious cuts. About $60 million in unspent money for atmospheric, climate, and weather research was rescinded at the request of the Senate Commerce Committee chaired by Ted Cruz (R-TX). In addition, thanks to GOP lawmakers, the Corporation for Public Broadcasting can no longer administer the $136 million Next Generation Warning System grant program, which helps public radio and TV stations improve their emergency alert systems to warn people of severe weather.

Moreover, the Trump administration is already achieving significant cuts by refusing to spend money that Congress approved for this fiscal year. As Science reported on August 25, “some $1 billion in spending for the current year may still be sitting on [Howard] Lutnick’s desk,” awaiting the Commerce Secretary’s approval. “The agency has no plans to spend all of that money by the fiscal year’s end on 30 September—if ever.” According to Science, the Trump administration is set to spend $100 million less on NOAA’s research arm this year than Congress intended, a 14 percent cut. Other divisions have seen similar cuts, especially those offices doing climate-related work. Meanwhile, the White House has begun canceling contracts for next-generation weather satellites that were supposed to launch next decade.

Frankly, any extreme weather disasters that happen in the foreseeable future will have Trump’s bloody fingerprints on them, so thorough and devastating has his dismantling of our disaster policy apparatus—from climate research to weather forecasting to emergency planning—been.

We live in an era of climate breakdown. Even if planet-heating pollution ceases tomorrow, the atmospheric concentration of greenhouse gases is so high that increasingly frequent and severe extreme weather is, to a certain extent, already locked-in. That said, every tenth of a degree of warming that we can avoid makes a positive difference, and so too do just adaptation initiatives. But rather than minimize hazards—through rapid decarbonization and robust investments in the social safety net, including green infrastructure—Republicans are actively aggravating an already-grim situation. Democrats aren’t talking enough about this. That’s a mistake.

This is a longstanding problem. Harris and Walz, for example, missed a golden opportunity after Helene and Milton, which occurred in the weeks leading up to the 2024 election. Trump, Musk, Hamilton, and other Republicans filled the void with lies about FEMA, sowing mistrust to gain buy-in for getting rid of the agency. We urged Harris to use the hurricanes to tell “a compelling story about the escalating and deeply intertwined climate, housing, and insurance crises that might resonate with voters of all stripes.”

That would necessarily entail denouncing fossil fuel-corrupted Republicans for obstructing a clean energy transition and thwarting investments in disaster risk reduction. It would also mean sketching, and committing to pursue, a humane agenda that prioritizes public well-being over private profit. Something like directly creating living wage jobs to achieve the universal provision of zero- or low-carbon public goods—including green social housing, clean energy, mass transit, and educational, recreational, and artistic infrastructure. That’s the kind of transformative vision that might begin to turn the tide.

Disasters offer untapped opportunities for political education and organizing. Survivors are in dire need of just responses, which includes intervening to prevent future harm. Those put off by the idea of politicking in the wake of disasters should consider that when someone like Trump White House spokesperson Karoline Leavitt or Texas Gov. Abbott (R) says that assigning blame is inappropriate, they are emulating the NRA, which insists, after dozens of schoolchildren are mowed down by someone wielding an AR-15, that it’s not the “right time” to push for gun control. Now is the right time to advocate for change. If Democrats at all levels, including state and local officials, don’t connect the dots between fossil fuel expansion, attacks on weather forecasting, and avoidable deaths when a catastrophe is at the front of people’s minds, it will fade from view and the fatal insanity will continue.

We’re not dealing with strictly “natural disasters.” That phrase obscures all of the decisions that societies make—or don’t make—before, during, and after bouts of severe weather. It conveys, in an apolitical manner, that deadly storms are inevitable, or “acts of God.” To be clear, certain environmental phenomena are inescapable, though their frequency and intensity is another matter. Still, whether natural hazards generate catastrophic outcomes depends largely on political choices about how society is organized. The Trump administration makes clear the need to denaturalize disasters—to convey the political, economic, and social forces that produce them. Today’s unnatural disasters are inseparable from planet-heating pollution and the destruction of public good-oriented government. They are neoliberal climate disasters; our future hinges on our ability to politicize them.

As long as our society fails to confront and reverse the reckless policy choices that are increasing the likelihood, scale, and unequal impacts of every hurricane, heat wave, etc., things will only get worse. Today’s tragedies—they’re really crimes perpetuated by fossil fuel executives and magnified by those who attack public goods and elevate “personal responsibility” over social solidarity—will be repeated tomorrow.

In essence, rather than adapt to our climate-changed present and future, the Trump administration is choosing to exacerbate cataclysms. To win back the working class, Democrats could try explaining how Republican policies are endangering communities around the country while making life more expensive. Anger at elites is through the roof. If Democrats want to beat back right-wing authoritarianism, which is at odds with a livable future, they should embrace green economic populism. Green New Deal policies aimed at simultaneously lowering prices and planet-wrecking emissions (e.g., decommodifying and decarbonizing housing, transportation, and other essentials) remain popular. Trying something genuinely new—not the false promise of neo-neoliberalism being promoted by corporate-backed abundance advocates—is more than worthwhile; it’s an existential necessity.

Herein lies a big problem. Without equating the two major parties, it’s undeniable that a substantial chunk of contemporary Democrats remain wedded to an “all-of-the-above” energy strategy that ultimately privileges fossil fuels. And too many of them are committed, like their Republican counterparts, to advancing the interests of a minority of super-wealthy benefactors rather than the vast majority of working people. Thus, while even corporate Democrats may be willing to condemn attacks on clean energy and cuts to NOAA and FEMA, that doesn’t mean they’ll go to bat for the ambitious pollution- and inequality-slashing policies we actually need.

One downside to focusing so intently on the culpability of Trump and other Republicans is that it overlooks systemic sources of our unjust and precarious status quo, namely five decades of largely bipartisan neoliberalization. Neoliberals from both parties have inflicted widespread pain by attacking unions, corporate taxes, the welfare state, and myriad regulations—all of which has intensified inequality and left people vulnerable and ecosystems insufficiently protected. At the same time, Trump and DOGE represent the apotheosis of neoliberalism, understood as using state power to facilitate the upward transfer of wealth. Unlike Republicans, a growing but insufficient number of Democrats are supportive of organized labor and progressive taxation and critical of deregulation, austerity, and privatization. Our call to focus on the deadly effects of Trump’s extraordinarily aggressive assault on the federal workers who keep us safe is an invitation for Democrats to abandon the neoliberal project once and for all, and to embrace a pro-labor, pro-environment, and downwardly redistributive alternative.

Hurricane Katrina not only exposed the vulnerability of communities to extreme weather events exacerbated by climate change, but also systemic injustices and a deeply flawed US insurance system.

It’s been 20 years since Hurricane Katrina struck the Gulf Coast of the United States, wreaking havoc in Louisiana, Mississippi, and Alabama. An estimated 1,833 people died in the hurricane and the flooding that ensued. The storm destroyed or damaged more than a million housing units and more than 200,000 homes, causing one of the largest relocations of people in US history.

In the months and years that followed, entrenched inequalities, questionable policy choices, and predatory practices by private insurers decided who could return home and rebuild. For instance, countless residents impacted by the hurricane learned too late that their standard homeowners’ insurance offered no protection against flood damage, leaving them to shoulder devastating repair costs themselves. In cities such as New Orleans, these dynamics further marginalized Black residents, who were more likely to live in flood-prone neighborhoods. The result was widespread and often permanent displacement, with longtime communities effectively erased from the map.

Hurricane Katrina not only exposed the vulnerability of communities to extreme weather events exacerbated by climate change, but also systemic injustices and a deeply flawed US insurance system. Private insurers pour billions of dollars into the fossil fuel industry, which is the main contributor to climate change. Thus, insurers help fuel the very crisis that is driving more frequent and severe climate disasters like Hurricane Katrina. Meanwhile, they are passing the financial risk of the escalating impact of climate change onto policyholders and forcing them to bear the costs of the crisis the industry itself helps perpetuate.

As climate-driven storms grow more frequent and increasingly destructive, the same insurance failures, housing crises, and inequitable recovery that followed Katrina now threaten communities nationwide. Two decades later, Katrina’s hard lessons cannot be ignored. Everyone deserves to live in safety and the opportunity to stay in the place they call home. Corporate greed and government negligence cannot continue to undermine these rights.

On August 29, 2005, Hurricane Katrina made landfall with winds that reached 140 miles per hour. These high-velocity winds drove a storm surge that raised sea levels 25 to 28 feet above normal along parts of the Mississippi coast, and 10 to 20 feet along the southeastern Louisiana coast. The surge breached protective levees, causing catastrophic flooding. Two days after the hurricane struck, 80% of the city of New Orleans was underwater. Other coastal towns and cities in Louisiana, Mississippi, Alabama, and along the western Florida panhandle also experienced significant storm surges and destructive winds, which caused widespread flooding and damage to homes.

Approximately 1.5 million people aged 16 years and older had to leave their residences in Louisiana, Mississippi, and Alabama because of Hurricane Katrina. In New Orleans, where the mayor issued a mandatory evacuation order, a population of around 500,000 was reduced to a few thousand people within a week of the storm.

As water was pumped out of the flooded areas and basic services and infrastructure were restored, New Orleanians were allowed to return. But tens of thousands were not able to do so. One year after Katrina, approximately 197,000 residents had not come back to the city; many relocated to the relatively close cities of Houston and Baton Rouge, but others as far away as Alaska and Massachusetts. Still today, many of those who evacuated the city, hoping to return, remain displaced. New Orleans’s metropolitan area population remains 20% below pre-Katrina levels.

The development of New Orleans has been fraught with injustices. Racial segregation, redlining, and chronic underinvestment in Black communities pushed residents and renters into areas with crumbling infrastructure, poorer-quality homes, and greater exposure to environmental hazards and contaminants.

When Katrina hit, Black residents were concentrated in the most vulnerable parts of New Orleans, located well below sea level and poorly protected by inadequate levees. Accordingly, neighborhoods with the highest percentages of Black residents saw greater housing destruction from the storm.

Did You Know?

The disparate impact of climate disasters on property and infrastructure in US minority communities is the result of nearly a century of discriminatory home lending and insurance policies.

In the 1930s, the US federal government used a rating system in its low-cost home loan program to assess lending risk. Assessors created maps ranking the perceived risk of lending in certain neighborhoods, with race often used as the determining factor in assessing a community’s risk level. Black and immigrant neighborhoods were typically rated as “hazardous” and outlined in red, warning lenders that the area was a perilous place to lend money. Known as redlining, these and other discriminatory practices led to a lack of investment in minority communities.

This lack of financial access resulted in shoddy construction and poor infrastructure that have made minority neighborhoods less resilient to climate disasters and more prone to other financial risks. For instance, insurers are more likely to increase premiums if they determine that properties are less resilient to climate damage. This new financial practice is known as bluelining, and it occurs when insurers raise their prices or pull out of areas that they perceive to be at greater environmental risk.

For Lousina’s Black residents, Katrina’s damage was compounded by discriminatory recovery policies that deepened inequalities. After the storm, the federally funded Road Home program was launched to help residents repair or rebuild damaged homes. It offered grants of up to $150,000 per homeowner, but payments were based on whichever was lower—the home’s pre-storm value or the cost to rebuild.

Because property values in Black neighborhoods were often far lower than in white neighborhoods, this meant many Black homeowners would receive only a fraction of what they needed to rebuild. In one case, a woman had rebuilding costs of over $150,000, but because the estimated value of her home pre-storm was much lower, she would’ve received an essentially useless grant of $1,400. As a result, the program was alleged to discriminate against Black homeowners, and a federal class action suit was filed on November 12, 2008, on behalf of 20,000 homeowners. The litigation settled with Louisiana agreeing to reward approximately 1,300 homeowners with $62 million in additional compensation.

Renters fared no better. Hurricane Katrina damaged or destroyed 82,000 rental units in Louisiana, 20% of which were affordable to extremely low-income households. The impact on public and federally subsidized rentals was especially severe. In New Orleans, public-housing residents were displaced at a rate of nearly 90%. And reconstruction policies only exacerbated the disparities these residents faced.

Consider this.

Before the storm hit and floodwaters rose, the Housing Authority of New Orleans evacuated all residents living in its 7,379 public housing units. After the waters receded, residents were allowed to return to approximately 1,600 units. Most other units were sealed off with steel doors and barbed wire—officially due to storm damage—before being slated for demolition. Yet, the redevelopment that followed included far fewer mixed-income apartments. By 2010, five years after the hurricane, less than half of the original 7,379 units were open in any form. The dramatic decrease in public housing contributed to the permanent displacement of many of New Orleans’ longtime residents.

After Katrina, renters faced a range of economic pressures. Many landlords delayed repairs or rebuilding, especially in low-income areas, which are seen as less profitable. Some used the disaster as an opportunity to renovate and target higher-paying tenants, further shrinking the supply of affordable rentals. Within five years of the Hurricane, the stock of mid-priced housing units in New Orleans had declined by more than two-thirds, pushing the median rent from $689 in 2004 to $876 in 2009. These rising costs hit Black residents hardest, forcing many to leave and permanently altering the city’s character.

Even those who could afford to return to New Orleans and buy a new home after Katrina faced soaring prices—up 14% in the first year alone—as demand outpaced the reduced housing supply. In addition, homeowners’ insurance premiums jumped 22% in Louisiana between 2005 and 2007, adding yet another barrier to homeownership.

Then, as now, and to the surprise of many victims of the Hurricane, standard home insurance policies in the US did not protect homeowners from floodwater damage. This means residents must buy additional flood insurance to be protected in the event of a disaster like Katrina.

New Orleans residents had among the highest participation rates in the country in the National Flood Insurance Program (NFIP), a federal government program that provides flood insurance to homeowners, renters, and businesses. However, the majority of residents in areas affected by Katrina had not purchased flood insurance. Uninsured property losses due to flooding were economically devastating, exceeding an estimated $41.1 billion (USD 100 billion in 2024 prices). In addition, the NFIP incurred some $16.1 billion in losses and a deficit exceeding $18 billion as a direct result of the flooding caused by Katrina.

Even for New Orleanians with flood insurance, coverage likely fell short. Policies typically covered about $152,000—the city’s median house price at the time. But this was rarely enough to replace the damaged household contents or to pay residents for temporary housing while their home was uninhabitable.

More and more, whether people hit by climate-driven storms get anything from their insurers depends not on the fact that their homes were damaged, but on how they were damaged.

While the standard home insurance policy does not cover water damage from a hurricane, it does cover wind damage. This gap left residents and insurers arguing about whether Katrina’s destruction to their homes was caused by its high-velocity winds or the flooding that followed, with multiple lawsuits challenging the validity of flood exclusions in insurance policies. Even before the flooding receded and residents of Louisiana and Mississippi could start to rebuild their lives, courts were inundated with litigation, with about 6,600 insurance-related lawsuits being instigated in the US District Court. Yet, Katrina’s destructive flooding was driven by a storm surge powered by the hurricane’s high winds—the very peril homeowners’ policies are supposed to cover.

On September 15, 2005, Mississippi’s Attorney General Jim Hood filed a case against five of the largest homeowners’ insurers in the state. Attorney General Hood sought a court declaration that the flood exclusion provision in standard home insurance policies was “void and unenforceable” and in violation “of the public policy of the State of Mississippi.” However, in that case and others, courts ruled that the flood exclusions were spelled out clearly in homeowners’ insurance policies and did not violate public policy.

The exclusion of water damage from insurance coverage remains a present issue for existing homeowners. According to the Federal Emergency Management Agency, since 1996, 99% of US counties have been impacted by flooding, but only 4% of homeowners have flood insurance. And, more importantly, over half (56%) of American homeowners don’t know that their home insurance policy excludes flood damage. As hurricane season intensifies, many homeowners will be shocked to learn that their insurance does not cover flood loss.

After Katrina, some insurers exploited the false dichotomy between wind and water damage, classifying losses as water damage to shift liability onto homeowners or the NFIP.

In 2013, a federal jury in Mississippi found that State Farm Fire and Casualty Co. defrauded the NFIP after avoiding covering a policyholder’s wind losses from Katrina by blaming the damage on storm surge, which is covered by federal flood insurance. Almost 10 years later, in August 2022, State Farm settled the case, agreeing to pay $100 million to the federal government.

State Farm was not the only insurer engaged in nefarious behavior, attributing Hurricane Katrina damage to flooding instead of wind. In oral argument before the Mississippi Supreme Court in 2009, insurance company USAA publicly admitted that it shifted its own costs to the NFIP and thus taxpayers.

The false dichotomy between the wind and water damage resulting from a hurricane remains nebulous. The damage caused by Hurricane Ian in Florida, North Carolina, and South Carolina in 2022, with its record-high wind speeds, generated $63 billion in private insurance claims. In contrast, 2018’s Hurricane Florence primarily caused water—not wind—damage in North and South Carolina, leaving uninsured flood losses estimated at nearly $20 billion and letting private insurers largely escape liability. More and more, whether people hit by climate-driven storms get anything from their insurers depends not on the fact that their homes were damaged, but on how they were damaged.

Hurricane Katrina exposed widespread gaps in home insurance coverage that persist today. In the 20 years since Katrina, unmitigated climate change has fueled rising temperatures and made extreme weather events such as hurricanes both more frequent and more severe. As storms grow costlier and more destructive, insurers have raised home insurance premiums and declined to renew many policies, leaving households with fewer options for protection. This escalating cycle has produced today’s insurance crisis.

Federal and state lawmakers must respond. The federal government must reform the NFIP to improve federal flood insurance and ensure it provides affordable coverage for more hazards. At the same time, the NFIP should do more to support community-based mitigation. States, meanwhile, must use their regulatory authority over insurance markets to address skyrocketing insurance costs and growing coverage gaps resulting from mounting climate change impacts.

Regulators should adopt legislation, like New York’s Insure Our Future bill, to prohibit insurers from underwriting new fossil fuel projects, require them to phase out support for existing projects, and force insurers to divest from fossil fuel companies.

The insurance industry cannot ignore its role in fueling the very crisis it now faces. Climate change-induced disasters are indisputably driven by fossil fuel emissions. And insurance companies facilitate climate change by investing in fossil fuel companies and underwriting fossil fuel projects. US insurance companies have investments of more than $500 billion in fossil fuel-related assets, including coal, oil, and gas. In 2022 alone, insurers worldwide collected $21 billion in premiums for underwriting fossil fuel projects—directly enabling their expansion.

Regulators should adopt legislation, like New York’s Insure Our Future bill, to prohibit insurers from underwriting new fossil fuel projects, require them to phase out support for existing projects, and force insurers to divest from fossil fuel companies. Without bold action, insurers will continue to profit from climate destruction while leaving families and communities to bear the costs.

With the federal government abdicating its responsibility, state and local leaders must step up. They have the power and duty to act.

A deadly storm has already claimed at least 120 lives and caused widespread devastation in Texas. Hurricane Erin has now unleashed catastrophic flooding in North Carolina before racing toward the Northeast—and hurricane season has only just begun. Storms are growing more destructive, driven by fossil fuels that warm our oceans and destabilize the climate, while the vulnerable petrochemical infrastructure in their path multiplies the danger. As the storms strengthen, US protections are unraveling, leaving millions exposed.

Every year, hurricanes grow more intense—fueled by warming oceans and a rapidly changing climate driven by fossil fuels. But it’s not just the storms becoming more dangerous. It’s the fossil fuel infrastructure in their path. It’s the toxic pollution released when storms strike. It’s the insurance companies abandoning communities in the aftermath. And it’s the US government retreating from its duty to protect.

The Gulf Coast—home to more than 84% of US plastics’ production and to nearly half of US petroleum refining capacity—is bracing for more than five major hurricanes predicted for the Atlantic Ocean this year. With each hurricane comes the risk of fires, explosions, and toxic releases—not just for these facilities, but for the surrounding communities. More than 870 highly hazardous chemical facilities are located within 50 miles of the hurricane-prone Gulf Coast, and more than 4 million residents and 1,500 schools sit within a 1.5-mile radius of a high-risk chemical facility in the region.

Nationally, 39% of the US population lives within 3 miles of a high-risk chemical facility.

And yet, as we brace for the next deadly storm, US President Donald Trump has axed critical weather forecasting jobs and announced plans to eliminate the Federal Emergency Management Agency (FEMA) altogether, leaving communities even more vulnerable in the face of escalating disaster.

But the threats don’t stop there. The US government is systematically dismantling our first line of defense. Since Trump took office in 2024, the administration has:

Fossil fuel infrastructure isn’t just at risk during storms—it supercharges the storms themselves. The industry is a major driver of global warming, accelerating the rising temperatures and warming oceans that exacerbate hurricanes. And even as storms grow more destructive, the industry is doubling down: 80% of proposed new petrochemical projects are sited within 20 miles of a hurricane or tropical storm’s path over the past decade. This means entire corridors already battered by climate disasters are being locked into even greater danger.

When disaster strikes, oil, gas, and petrochemical facilities release hazardous pollutants into the air and water, compounding the crisis for nearby communities, which are often low-income and disproportionately Black, brown, and Indigenous.

When Hurricane Katrina struck, it slammed into 466 facilities that handle hazardous chemicals and petrochemicals. More than 200 onshore releases of hazardous chemicals, petroleum, or natural gas were reported. The storm caused at least 10 oil spills, releasing more than 7.4 million gallons of oil into Gulf Coast waterways—more than two-thirds the volume spilled during the Exxon Valdez disaster, one of the worst in US history. Together, Hurricanes Katrina and Rita, just a month apart, shut down nearly a quarter of the country’s refining capacity.

And during Hurricane Harvey, Houston’s petrochemical plants and refineries released millions of pounds of pollutants. Flooding at the Arkema Petrochemical plant disabled the plant’s refrigeration system, triggering a massive explosion that sent black plumes and toxic fumes into the skies and forced evacuations across a community already on edge. An investigation by the Chemical Safety Board—recently dismantled by the Trump administration—determined that requirements of the Environmental Protection Agency’s Risk Management Program—currently being rolled back by the EPA—could have prevented this very disaster.

As extreme weather events surge, so do insurance premiums—while coverage vanishes for those living in harm’s way.

For many climate-vulnerable communities, home insurance is no longer affordable—or available. Since 2019, US home insurance rates have jumped nearly 38%. Louisiana, Texas, and Pennsylvania—all major fossil fuel corridors—rank among the top six most expensive states to insure a home. Home insurance premiums rose by 10% or more across 40 states from 2021 to 2024. Renters aren’t immune as landlords pass along skyrocketing insurance costs.

Insurance math: Communities facing hurricanes, flooding, and fires? Too risky to insure. Companies driving the disasters? Coverage and cash.

Insurers claim payouts from climate disasters are driving up costs. The truth is, insurers are investing in the very industries making those disasters worse—and raking in profits. In Louisiana, insurance companies are making $55 in profits for every $1 in underwriting losses. This profitability is not unique: NAIC data shows the property and casualty sector made an all-time high of $167 billion profits in 2024—up 91% from 2023, and 330% from 2022.

At the same time, the US insurance industry continues to bankroll fossil fuels, holding more than $500 billion in fossil fuel-related assets as of 2019 (the most recent data set available); a pattern of investing that is unlikely to have substantially changed since. While refusing to insure homeowners in climate-exposed communities, many insurers are simultaneously underwriting new fossil fuel infrastructure. At least 35 insurance companies are backing methane gas (LNG) export terminals across the Gulf South—some of the very same companies, including AIG, Chubb, and Liberty Mutual, that are raising premiums or pulling out of the housing market in vulnerable regions entirely.

Insurance math: Communities facing hurricanes, flooding, and fires? Too risky to insure. Companies driving the disasters? Coverage and cash.

Rather than confronting the crisis, insurance companies are fueling it—protecting profits and abandoning people. This isn’t just hypocrisy, it’s a business model, one built on extraction and shifting costs onto the public.

The system is rigged. Those most responsible are rewarded, while those most vulnerable are left to suffer the storms alone.

We all deserve somewhere safe to live—free from the dread of the next hurricane, the next explosion, or the next rollback of basic protections. But fossil fuel polluters—and the insurance companies profiting from their harm—are robbing us.

We will not accept this endless cycle of crisis. We deserve safety, especially from the governments whose duty it is to protect us. We deserve safety from storms and from toxic spills. We deserve a government that protects its people—and agencies that do their jobs: defending public health and the environment, not doing the bidding of polluters.

With the federal government abdicating its responsibility, state and local leaders must step up. They have the power and duty to act. It’s time for states, especially those in the eye of the storm, to lead where the federal government is failing. States must:

When Hurricane Katrina devastated Louisiana, it left behind a $170 billion bill. The federal government stepped in for $120 billion. But with FEMA on the chopping block, that kind of relief may never come again. If federal protections vanish, the financial and human cost of the next disaster will fall squarely on states—and the people who live in them.

The climate crisis isn’t waiting. The storms are here. Will our leaders meet the moment—or leave us to weather the disaster alone?

These are efforts that we can all join in and support, becoming part of the solution and adding to the abundance in our own communities.

We are now in what we used to call the “dog days of summer”—the hottest, steamiest, sultriest days of the year. As a child, I looked forward to these days of playtime outdoors, eating what we called “cool pops” aka popsicles and watermelon, and catching fireflies at dusk. Now, I wake every day to look at alarming headlines of a planet at boiling point. And the worst part is that it takes square aim at Black, Indigenous, and other communities of color.

Each year, we’ve seen climate change produce hurricane and fire seasons that are more intense and less predictable. And this year, the government infrastructure that is supposed to help us prepare and respond to those impacts—including the Federal Emergency Management Agency and National Oceanic and Atmospheric Administration—was hollowed out before the season even started.

Still, in all of this scarcity, I bring an abundance mindset to my work as the leader of The Solutions Project. We are a public foundation that works to solve the climate crisis by reallocating resources to grassroots communities. We believe that the people closest to the pain understand the problems the best. Thus, they are closer to the solutions. There is power at the front lines, and that power is abundant.

When I invoke “abundance,” I am coming from a Black, feminist, Southern perspective. My abundance eschews wealth inequality and materialism in favor of community, care, and interdependence. It rejects competition and thrives in collaboration. In this abundance, we recognize, celebrate, and tend to the bounty of the Earth just as we care for each other. In this abundance, there is no need to hoard resources and no need to “other” anyone because there is room for everyone.

None of us can survive this alone, but we can thrive together.

It’s the abundance that I learned from my grandmother in Mississippi who grew collard and mustard greens, the largest red tomatoes, juicy melons, crunchy cucumbers, and more. When it was time to harvest her crops, she shared with families in her community. I learned it from our church potlucks where everyone brought a dish—like macaroni and cheese, pound cake, or potato salad—and everyone went home with full bellies and leftovers. I learned it when I overheard Mr. Jones tell Mr. Williams, “I’ll do your taxes, if you fix my car.” Or when I saw neighbors carpooling to the grocery store or driving each other’s kids to school. Abundance was everywhere.

Even though the climate crisis creates real limits on resources, I see this abundance at work every day through The Solutions Project’s grantees. To date, we’ve supported over 350 grassroots organizations across the country, with a segment of them cultivating “resilience hubs” in their communities. These are trusted spaces that are a part of the existing local infrastructure such as churches, community centers, and libraries—and they work together to support the community before, during, and after climate disasters. These folks are pushing forward with this work even in the midst of drastic federal funding cuts and manufactured chaos.

For example, West Street Recovery’s hub house in Houston and The SMILE Trust’s hub house in Miami have proven invaluable in the face of storms that have become more intense and unpredictable due to climate change. These homes provide food, shelter, and backup generators in the face of devastating storms or power outages and facilitate neighbors meeting and helping each other out.

Resilience hubs are a collective response, representing a groundswell of people and organizations and businesses working together. They are also hyperlocal, which allows them to adjust to the local context and needs. What works in a large city in California, for example, might not work in rural South Carolina. That collective response is what creates a vibrant, thriving, energized culture in each individual community. This is the “abundance” approach that will help us thrive and take care of each other through this crisis.

These are efforts that we can all join in and support, becoming part of the solution and adding to the abundance in our own communities. Whatever your skills and talents are—growing, cooking, fixing, creating—they are needed in your community now. It’s important that we get off our screens and into our streets because local solutions are often the most powerful. None of us can survive this alone, but we can thrive together.

This builds on the type of support systems that my ancestors created in the wake of Emancipation and into Reconstruction. They organized themselves and pooled their resources to help one another survive the horrors this country inflicted on them. Even in the teeth of such violent oppression, they believed in interdependence, interconnection, relationship, and community. Abundance, for communities of color, is a tradition.

This August, I’ll be spending time at my altar, as I often do to commemorate days of Black and Indigenous resistance and celebration. I will say a prayer and light a candle. I will pour libations and put out offerings of fruit to honor my ancestors. I will thank them for their fortitude, their sacrifices, and, of course, their vision and practice of abundance.

I invite Black, Indigenous, other communities of color, and all frontline communities to share the traditions that are important to you and your families, as part of our Stronger Together campaign. We encourage us all to go back to our elders and recover generational wisdom and rituals that may be at risk of getting lost. It can be something as simple as planting trees or maintaining a phone tree (even if you didn’t call it that.) The more that we share, the stronger we become.

"You feel like you are in the aftermath of a nuclear war," said one resident. "I saw an entire neighborhood disappear."

Undocumented migrants living in informal settlements in the French territory of Mayotte were among those whose lives and livelihoods were most devastated by Cyclone Chido, a tropical cyclone that slammed into the impoverished group of islands in the Indian Ocean over the weekend.

Authorities reported a death toll of at least 20 on Monday, but the territory's prefect, François-Xavier Bieuville, told a local news station that the widespread devastation indicated there were likely "some several hundred dead."

"Maybe we'll get close to a thousand," said Bieuville. "Even thousands... given the violence of this event."

Mayotte, which includes two densely populated main islands, Grande-Terre and Petite-Terre, as well as smaller islands with few residents, is home to about 300,000 people.

The territory is one of the European Union's poorest, with three-quarters of residents living below the poverty line, but roughly 100,000 people have come to Mayotte from the nearby African island nations of Madagascar and Comoros in recent decades, seeking better economic conditions.

Many of those people live in informal neighborhoods and shacks across the islands that were hardest hit by Chido, with aerial footage showing collections of houses "reduced to rubble," according to CNN.

"What we are experiencing is a tragedy, you feel like you are in the aftermath of a nuclear war," Mohamed Ishmael, a resident of the capital city, Mamoudzou, told Reuters. "I saw an entire neighborhood disappear."

Bruno Garcia, owner of a hotel in Mamoudzou, echoed Ishmael's comments, telling French CNN affiliate BFMTV: "It's as if an atomic bomb fell on Mayotte."

"The situation is catastrophic, apocalyptic," said Garcia. "We lost everything. The entire hotel is completely destroyed."

Residents of the migrant settlements in recent years have faced crackdowns from French police who have been tasked with rounding up people for deportation and dismantling shacks.

The aggressive response to migration reportedly led some families to stay in their homes rather than evacuate, for fear of being apprehended by police.

Now, some of those families' homes have been razed entirely or stripped of their roofs and "engulfed by mud and sheet metal," according to Estelle Youssouffa, who represents Mayotte in France's National Assembly.

People in Mayotte's most vulnerable neighborhoods are now without food or safe drinking water as hundreds of rescuers from France and the nearby French territory of Reunion struggle to reach victims amid widespread power outages.

"It's the hunger that worries me most. There are people who have had nothing to eat or drink" since Saturday, French Sen. Salama Ramia, who represents Mayotte, told the BBC.

The Washington Post reported that Cyclone Chido became increasingly powerful and intense—falling just short of becoming a Category 5 hurricane with winds over 155 miles per hour—because of unusually warm water in the Indian Ocean. The ocean temperature ranged from 81-86°F along Chido's path. Tropical cyclones typically form when ocean temperatures rise above 80°F.

"The intensity of tropical cyclones in the Southwest Indian Ocean has been increasing, [and] this is consistent with what scientists expect in a changing climate—warmer oceans fuel more powerful storms," Liz Stephens, a professor of climate risks and resilience at the University of Reading in the United Kingdom, told the Post.

People living on islands like Mayotte are especially vulnerable to climate disasters both because there's little shielding them from powerful storms and because their economic conditions leave them with few options to flee to safety as a cyclone approaches.

"Even though the path of Cyclone Chido was well forecast several days ahead, communities on small islands like Mayotte don't have the option to evacuate," Stephens said. "There's nowhere to go."

"The longer climate deniers keep up this charade, the more expensive things will get," said the JEC chair.

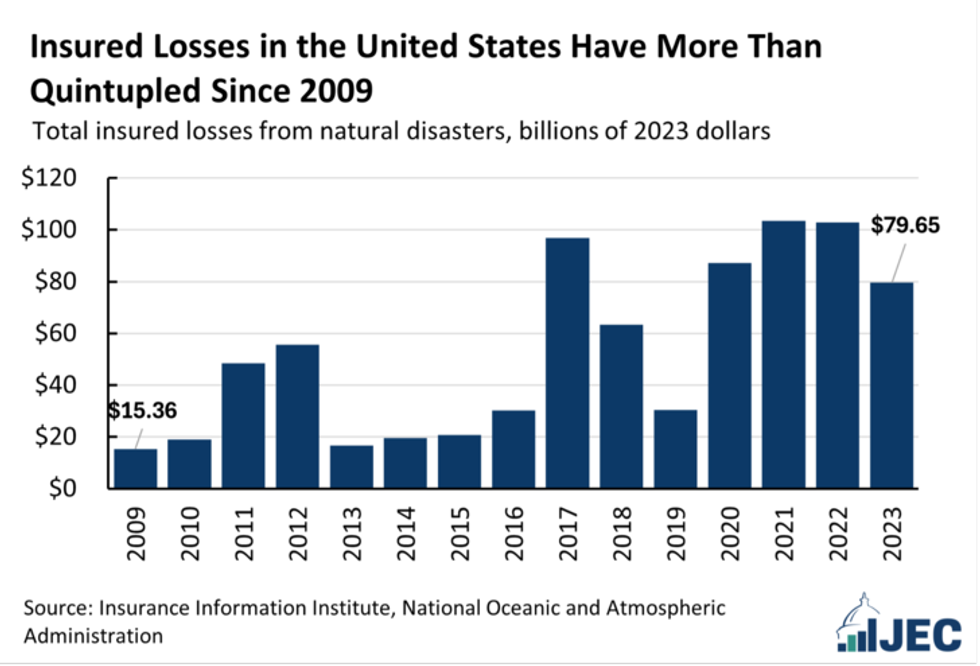

After at least two dozen U.S. disasters with losses exceeding $1 billion during a year that is on track to be the hottest on record, a congressional committee on Monday released a report detailing how the fossil fuel-driven climate emergency poses a "significant threat" to the country's housing and insurance markets.

"Climate-exacerbated disasters, such as wildfires, hurricanes, floods, drought, and excessive heat, are increasing risk and causing damage to homes across the country," states the report from Democrats on the Joint Economic Committee (JEC). "Last year, roughly 70% of Americans reported that their community experienced an extreme weather event."

"In the 1980s, the United States experienced an average of one billion-dollar disaster (adjusted for inflation) every four months; now, these significant disasters occur approximately every three weeks," the document continues. "2023 was the worst year for home insurers since 2000, with losses reaching $15.2 billion—more than twice the losses reported in 2022."

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief."

The insurance industry is already responding to that stress. The publication highlights that "insurers are pulling out of some states with substantial wildfire or hurricane risk—like California, Arizona, Florida, and North Carolina—leaving some areas 'uninsurable,'" and "in many regions, even if the homeowner can get insurance, the policy covers less than the actual physical climate risks (for example, rising sea levels or more intense wildfires) that their home faces, leaving them 'underinsured.'"

JEC Democratic staff found that last year, "the average U.S. homeowners' insurance rate rose over 11%," and from 2011-21, it soared 44%. Researchers also documented state-by-state jumps for 2020-23. For increases, Florida was the highest ($1,272), followed by Louisiana ($986), the District of Columbia ($971), Colorado ($892), Massachusetts ($855), and Nebraska ($849).

The highest premiums for 2023 were in Florida ($3,547), Nebraska ($3,055), Oklahoma ($2,990), Massachusetts ($2,980), Colorado ($2,972), Hawaii ($2,958), D.C. ($2,867), Louisana ($2,793), Rhode Island ($2,792), and Mississippi ($2,787).

The report ties the rising premiums to "surging" prices for repairs, reinsurers also hiking rates, insurance litigation issues, and rate caps in some states pushing higher costs off to states that regulate the industry less. While JEC Democrats focused on the United States, as Common Dreams reported last week, the climate threat to the insurance industry is a global problem.

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief," the new report warns. "Given this rising threat, innovations in climate mitigation and adaptation, insurance options, and disaster relief are essential for protecting Americans and their finances."

The publication points out that "a previous JEC report on climate financial risks discussed other potential solutions like parametric insurance (a supplemental insurance plan that can pay homeowners faster), community-based catastrophe insurance that incentivizes community-level resilience efforts, and attempts to use risk-pooling, data, and AI to better price risk."

The new document also promotes the Wildfire Insurance Coverage Study Act, introduced by JEC Chair Sen. Martin Heinrich (D-N.M.) "to address these data needs and study wildfire risk, insurance, and mitigation to help Americans make more informed decisions about the risks to their homes," and the Shelter Act, which "would create a new tax credit, allowing taxpayers to deduct 25% of disaster mitigation expenditures."

The report further recommends improvements to several Federal Emergency Management Agency (FEMA) programs, including:

The JEC publication comes as the country prepares for President-elect Donald Trump to take office next month after running a campaign backed by billionaires and fossil fuel executives and pledging to "drill, baby, drill," which would increase planet-heating pollution as scientists warn of the need for cutting emissions. Republicans will also have control of both chambers of Congress.

Heinrich on Monday called out the GOP for its climate record, saying that "Republicans have denied that climate change is real for over 40 years, and as a result, homeowners are seeing their insurance costs rise."

"Homeowners in New Mexico have seen their premiums increase by $400 over the last three years because of Republicans' refusal to act," he added, citing the 2020-2023 data. "The longer climate deniers keep up this charade, the more expensive things will get."

Rolling back every shred of climate progress and propping up rich polluters is going to make matters much worse for Georgia, Florida, and every other state on the Gulf and Atlantic coasts.

It’s 2029. JD Vance has been president for six months following Donald Trump’s second term in office. You’re waking up in a storm shelter in Georgia. You cowered all night as Hurricane Don smashed its way across the state.

You open the door to utter devastation—buildings destroyed, whole communities washed away, hundreds of people dead or missing.

Despite its Category 5 strength, Hurricane Don hit the Atlantic coast with little warning. Several years earlier, following the Project 2025 blueprint, the National Oceanic and Atmospheric Administration was privatized. Hurricane hunter planes were scrapped because they were unprofitable. And satellite data was sold to the highest bidder.

Back here in the present day, just days before Election Day, we should be clear-eyed about the consequences of a second Trump term.

Without NOAA forecasts, countless people were caught unprepared. They chose not to evacuate and tried to protect their homes.

In the days and weeks that follow, you realize that the federal government is not coming to help.

In line with Project 2025, emergency response activities were transferred to state and local governments. Federal disaster preparation grants have been eliminated. And the National Flood Insurance Program was wound down, leaving only the rich and lucky few who have private insurance with the ability to rebuild.

This was the consequence of electing Donald Trump and the fruition of his Project 2025’s extreme anti-people, pro-polluter agenda.

But there was more. Following through on his campaign promise, Trump delivered an oil and gas development frenzy with more fracking, more pipelines, and a battle plan to “drill, drill, drill.”

And Trump made quick work following through on his promise to oil executives that he’d block or reverse any environmental law they wanted if they donated $1 billion to his campaign.

Between 2025 and 2028, President Trump appointed two more justices to the Supreme Court. With an 8-1 conservative hegemony, the Supreme Court ruled that the Environmental Protection Agency had no authority at all to address greenhouse gas emissions. In fact, the court rejected that climate change was even real.

As a result, all federal agencies were left unable to address any impact of climate change. Superstorms, extreme wildfires, category 5 hurricanes have become the new normal.

Back here in the present day, just days before Election Day, we should be clear-eyed about the consequences of a second Trump term.

We just saw Hurricane Milton intensify in the Gulf of Mexico at one of the fastest rates ever on record. It finally slammed into Florida as a powerful Category 3 storm, leaving at least 24 people dead, more than 3 million without power, spawning dozens of tornadoes and creating a once-in-a-thousand-year rain event.

Two weeks earlier, Hurricane Helene brought a 1,000-year rainfall event to North Carolina and Georgia. It was the deadliest storm to hit the U.S. mainland since Hurricane Katrina, leaving at least 230 people dead across six states and carving a path of destruction as much as 500 miles from any coastline.

Milton’s rapid intensification and Helene’s immense rainfall surprised some observers but both storms exemplify the effects of global heating driven primarily by digging up and burning fossil fuels.

For decades, scientists have predicted the increasing strength of such storms as governments fail to stop fossil fuel expansion and the planet keeps getting hotter. Continuing to burn ever more oil, gas, and coal means warmer oceans and warmer air. Warmer oceans provide immense energy that intensifies storms. Warming air holds more moisture, bringing heavier rainfall.

Rolling back every shred of climate progress and propping up rich polluters is going to make matters much worse for Georgia, Florida, and every other state on the Gulf and Atlantic coasts. Storms of the century will increasingly become storms of every few years—same goes for heatwaves, droughts, wildfires, and floods—with little relief or recovery in sight.

And Trump’s reckless plans to pull out of the Paris agreement again and throw sand in the gears of the international climate negotiations threatens world leaders’ long-overdue agreement last year to “transition away from fossil fuels.”

In a year of climate extremes, we’ve learned that nowhere is safe on a heating planet.

Hurricanes will keep happening, as they always have. But when you emerge after 2029’s Hurricane Don, do you want a government that acts on science to protect people and planet, making polluters pay for their destruction? Or one that sacrifices our lives and livelihoods to the highest bidder?

The modern state’s drive to dominate the environment and its rich history of accumulation by dispossession are the prototypes and contexts for ideas that the U.S. government can control hurricanes.

The recent natural disasters caused by the Helene and Milton tropical cyclones in the Southern U.S. have triggered unfounded and ill-informed conspiracies about the origin of the disasters and the government’s involvement in weather modification. Despite being based on ill-informed claims that defy common sense, these conspiracies have historical contexts.

In a broader sense, the modern state’s drive to dominate nature and its rich history of accumulation by dispossession are the prototypes and contexts for such conspiracies. Environmental conspiracies have long been an integral part of the larger conspiracy against nature, which treat nature as a cornucopia of resources external to human identity and society that must be dominated to maximize its utility.

Environmental conspiracies have long served the interests of power structures, enabling them to control people and societies by dominating nature. These false claims have significantly shaped modern Western techno-bureaucratic approaches to nature and the environment. Interestingly, many of the dominant misguided claims were not propagated by ordinary people but by epistemic circles within the state apparatus, including scientists, ecologists, geographers, and naturalists who were and are part of the bureaucratic and technical machinery of the colonial or neocolonial states.

The rhetoric and discourse about the “brutality,” “ferocity,” or “violence,” of nature imply the pressing necessity for the state to manage, regulate, and exert control over nature and natural processes.

One of the conspiracy theories surrounding recent natural disasters involves the alleged involvement of the U.S. federal government in controlling and harnessing these disasters for political and economic ends. Although this claim that the Biden administration has manipulated Hurricane Milton is ludicrous, the desire to exert control over nature and natural processes has long been the inspiration of the modern state and its techno-bureaucratic machinery, at least since the European Enlightenment. From the colonial state manipulating and altering ecological landscapes, socio-ecological practices, and dismantling traditional knowledge sources, to current efforts to manipulate and control planetary processes through techno-bureaucratic techniques, such as geoengineering and planetary management, the domination and control of nature have remained an active pursuit within the state’s or state-supported technocratic and epistemic circles. Control over nature is part of the rationalizing and moralizing mandate of the modern state.

Embedded in the works of influential Enlightenment thinkers was establishing mastery over nature. This maxim provided a clear intellectual foundation for the systematic and cumulative progression in the understanding of nature through the means and tools of natural sciences within the epistemological fabrics of empiricism. Francis Bacon, an early Enlightenment philosopher, advocated for scientists to meticulously observe and accurately measure natural processes to gain mastery over them. He also proposed that the government should financially support these scientific pursuits to achieve such mastery. Consequently, in tandem with the progress in natural science, Western colonial and post-colonial states financed and endorsed scientific, and at times pseudo-scientific, undertakings to exert dominance over nature.

Although Bacon proposed a methodical approach to gathering evidence, involving a continuous interaction between theory and evidence, in the colonies, the European colonial states couldn’t afford to postpone their loot and plunder for the sake of a time-consuming scientific process or exert their power over nature and people. Instead, they resorted to ecological conspiracies and ill-informed theories to justify and rationalize their socio-ecological intervention and domination.

During colonial rule in al-Maghrib, French colonial ecologists expounded ecological conspiracies that gained widespread acceptance as scientific facts, even to an extent today. Drawing on biblical narratives, they claimed that the Sahara Desert had once been a fertile and lush geography that had served as the Roman Empire’s granary. They further doubled down on the conspiracy and blamed the native people’s social and ecological practices for transforming the once lush region into the arid Sahara. Scientifically, there is no evidence suggesting that the Sahara Desert was green during the Roman Empire. Contrary to the colonial ecologists’ claim, recent scientific evidence indicates that the Saharan region was just as arid and harsh at the end of the last Ice Age as it is today.

India essentially served as a testing ground for British colonial “experts” to validate and perpetuate their ecological conspiracies and schemes and violence against nature.

The environmental conspiracy provided a convenient excuse for colonial powers to justify their oppression and domination by blaming the natives for an imagined ecological catastrophe. It also justified European dominance and invasions by claiming a historical responsibility to restore the Sahara to its original fertile state, which they portrayed as a region that could once again supply Europe with agricultural goods. This justification not only upheld European colonial control but also moralized and materialized their plunders by dispossessing Indigenous people of their lands and resources.

In South Asia, the colonial administrators, experts, and operatives faced the challenge of dealing with unpredictable rivers, especially those originating from the Himalayas. They devised environmental conspiracies that long served as scientific claims. In Northern India, facing persistent failure to contain and control the flow of the Indus and other mighty rivers for centralizing irrigation practices, British colonial experts wrongly attributed the frequent destructive floods in the upper Indus Valley to the obstruction of the rivers by glaciers in their upper regions. Lacking evidence, they based their speculative scientific claims on their knowledge of European rivers.

Environmental conspiracies by the colonial British in India were mostly due to the unscientific socialization of colonial experts. Many of these experts, such as ecologists, hydro- and civil- engineers, and geographers, were not trained as scientists but rather as soldiers, military officers, or colonial operatives. Their roles as scientists in India were more out of necessity, primarily driven by the need to assert control over nature by manipulating socio-ecological practices to maximize economic plunder. As a result, these colonial agents engaged in extensive and unregulated ecological experimentation, which resulted in numerous human tragedies such as floods, famines, and diseases. India essentially served as a testing ground for British colonial “experts” to validate and perpetuate their ecological conspiracies and schemes and violence against nature.

Environmental conspiracies and conspiracies against nature for ecological and social exploitation were not confined to 19th-century European colonial powers; similar ideas flourished in the United States as well. James Espy, the first official American meteorologist, lobbied Congress for funding to burn forests of Appalachia in hopes of inducing rain. A storm enthusiast, much like today’s amateur storm chasers, Espy initially worked as a schoolteacher before he devoted himself to studying storms. He believed that burning forests could trigger rain.

Although Congress ultimately declined to back Espy’s proposal, it did allocate funds for Robert Dyrenforth’s rain theory. In the late 19th century, the Senate approved funding for Dyrenforth, a former Civil War general and an engineer by profession, who proposed that creating loud noises through explosives in the atmosphere could agitate clouds and cause them to release rain. Drawn from his experiences during the war, Dyrenforth’s idea was a bold attempt to manipulate weather patterns.

After his experiment of tossing dry ice into the cloud at the Schenectady airport in New York caused a cloud to dissipate and turn into rain, Irving announced in joy that mankind finally learned how to control the weather.

In the summer of 1891, Dyrenforth and his team of rainmaking enthusiasts, which included a meteorologist from the Smithsonian Institute and a college professor, embarked on a series of experiments by waging several attacks against the atmosphere. They launched an all-out assault on the sky detonating blasting dynamite, firing mortar shells, igniting smoke bombs, flying electrified kites, setting off oxy-hydrogen balloons, and even unleashing a spectacular array of fireworks. The intention was to manipulate the natural process of rainmaking.

Controlling the atmospheric dynamics in the United States has not been the hobby or fixation of weather enthusiasts. Scientists equally contributed to the fascination of dominating and controlling the atmosphere. During the initial years of the Cold War, the Nobel Prize-winning physicist and chemist Irving Langmuir claimed to have developed a method of harnessing and controlling hurricanes. After his experiment of tossing dry ice into the cloud at the Schenectady airport in New York caused a cloud to dissipate and turn into rain, Irving announced in joy that mankind finally learned how to control the weather. Around this time, weather manipulation became a strategic goal during the Cold War. The political and geopolitical landscape of the era compelled the two superpowers to engage scientists and harness scientific advancements to manipulate weather and nature for their strategic objectives and goals.

These examples could easily, and also rightly, be viewed as anecdotal. However, beyond these specific instances, there exists a common and overarching ontological premise that has led to various scientific and pseudo-scientific experiments. Moreover, this premise also influences popular environmental conspiracies and techno-bureaucratic/epistemic conspiracies against nature. The premise is the aspiration to dominate nature. Although Irving was indeed a bright scientist, the setting of his experiment parallels those of colonial scientists—or so-called scientists—active in regions like al-Maghrib and South Asia. They all sought to assert control over natural processes. In the 21st century, amid ongoing ecological crises, this mission has broadened its scope to include the manipulation and management of global planetary systems and processes.

The enabling context for popular environmental conspiracies, such as those that emerged following the two tropical cyclones in the southern United States, is an overarching reductionist, simplistic, and anthropocentric understanding of nature. It isn’t, however, an outlook born from the minds of everyday individuals; rather, it reflects a deeper understanding of modern civilization rooted in the logic of the modern state, influenced by Enlightenment ideals. It is further implemented through the techno-bureaucratic apparatus of the state that aims to realize the state’s legal and moral duty of monopolizing violence, whether caused by humans or nature. The rhetoric and discourse about the “brutality,” “ferocity,” or “violence,” of nature imply the pressing necessity for the state to manage, regulate, and exert control over nature and natural processes.

Nature is not an external entity out there to be controlled and dominated. On the contrary, it is a complicated self-regulating and self-perpetuating collection of processes, elements, and mechanisms, where humans are as much a part of it as non-human living and non-living elements. Although contemporary humans, through their advanced material-technological culture, can manipulate various aspects of nature, we—along with our political and social structures, including the state—often struggle to predict or design the outcomes of such interventions.