SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

As The Kansas City Star detailed last week, Amendment 5 is a "top priority for Republican Gov. Mike Kehoe," and Missouri Promise PAC, the main campaign supporting it, received "$9.6 million from six organizations or groups that do not have to disclose their donors," also known as dark money.

While some of the campaign backers remain unknown to voters, the Institute on Taxation and Economic Policy (ITEP) in Washington, DC aimed to shed light on the specifics of the amendment's anticipated impact with its new policy brief.

"Amendment 5 asks Missouri voters to approve a tax shift without telling them which purchases will be taxed or how high sales taxes will rise," said ITEP analyst and brief author Eli Byerly-Duke. "What is clear is who would benefit: the wealthiest Missourians. Working families and seniors would be asked to make up the difference."

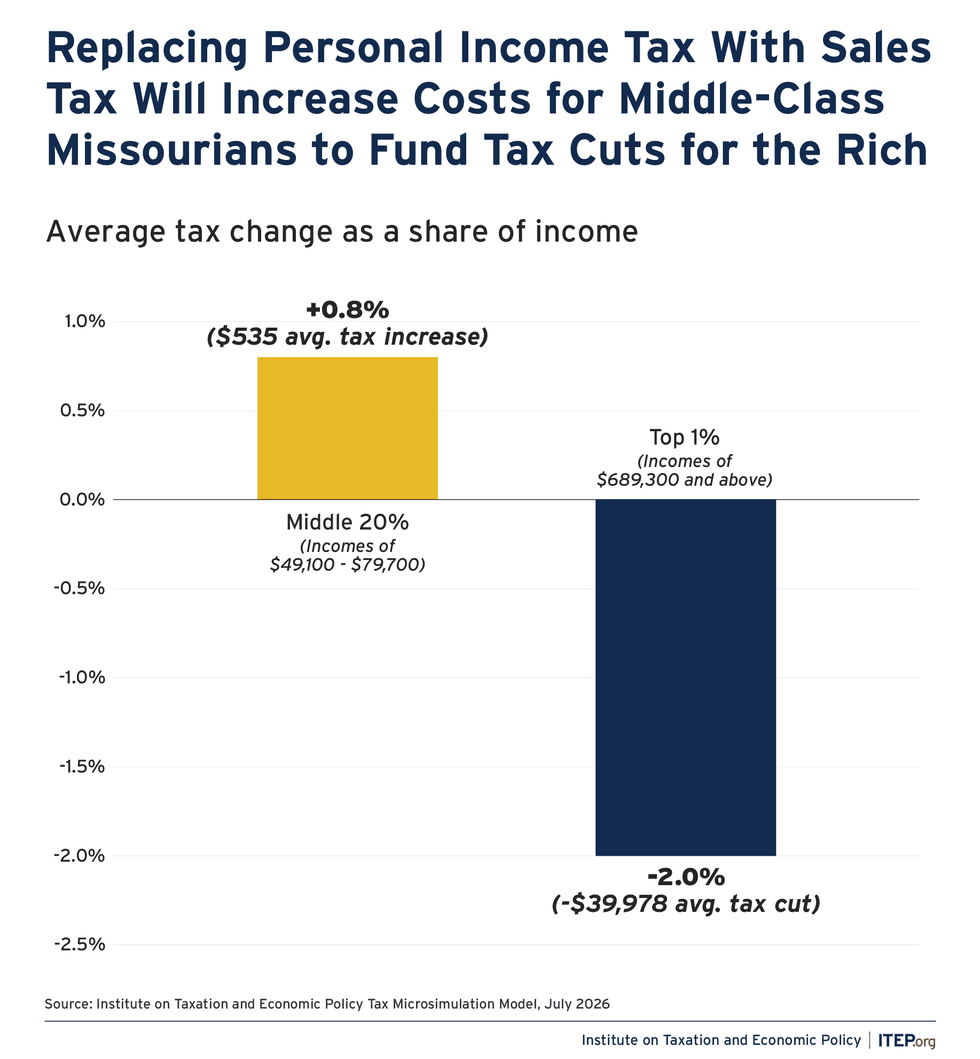

Missouri's individual income tax "makes up about 64% of the state's general fund and is the major funding source for state investments in infrastructure, schools, healthcare, public safety, and other services," the brief explains. "Low- and middle-income Missourians already pay a disproportionate share of the taxes to fund public services," and swapping income taxes for higher sales taxes "would shift even more of this responsibility from the state's highest-income individuals to teachers, farmers, truck drivers, and other middle-income Missourians."

Specifically, Byerly-Duke found that "middle-class Missourians with incomes of about $50,000 to $80,000 will pay $535 more in taxes if the personal income tax is eliminated and the sales tax expanded," all while Missouri's top 1%—or those with incomes of $689,300 and above—see an average tax break of $39,978.

The brief also highlights that "neither the Missouri Legislature nor governor has explained exactly how they will expand sales taxes if it passes. They might increase the sales tax rate, or they might expand the sales tax to include purchases of services that are not currently taxed, such as home repair and insurance, car repair and financing, personal care services such as hair or nail care, or medical services. Taxing these items will cost middle-income households a larger share of their incomes than higher-income households, but middle-income families will not get a commensurate benefit from the income tax elimination."

"For senior citizens, active-duty military families, and military retirees, the impact would be even worse," the report continues. "That's because Social Security benefits, active-duty military pay, and military pensions are already exempt from Missouri income tax, so households for whom those are the sole source of income would get no benefit from Amendment 5. For a middle-class Missourian earning between $49,100 and $79,700, this would mean an increase of $1,600 in taxes every year. Overall, seniors alone would see a net tax increase of about $335 million and each pay $365 more, on average, each year."

The brief bolsters the case for voters to say "No on 5," as Protect MO Taxpayers encourages. The "no" campaign's website warns that the amendment "hits seniors, retirees, veterans, and disabled persons hardest. Those on tight fixed incomes may not pay income tax on their limited income, but they will certainly be hurt by higher sales taxes on goods they buy every day, such as groceries, medicine, and gas, and services they use every day, from haircuts to car repairs to healthcare and housing."

"Amendment 5 hits working families hardest of all, with higher sales and use taxes estimated by the nonpartisan Missouri Budget Project to cost the average Missouri family about $500 more in taxes per year overall," Protect MO Taxpayers' site says, also pointing to concerns that it will "increase the tough economic times in rural Missouri" and "make the economic struggle even harder for small businesses."

The proposal "is a severe hit for renters who are already struggling to make ends meet," and "crushes the dreams of Missourians who want to buy or sell a home," the site adds. "Amendment 5 hits active-duty military, who do not pay state income tax but will face higher prices off the base with sales taxes that could roughly triple. This will mean less retail business and economic harm in our neighboring military host communities."