SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Hawai’i is the most militarized state per capita in our nation. Not only does it have a high concentration of service members, but more than 230,000 acres of land out of the 4.1 million in the island chain are currently under military control.

A dense network of military bases is conspicuously scattered across the eight islands. And almost a quarter of the state’s most populous island, O’ahu—home to Honolulu and Kailua—is currently under what local activists and groups call a military occupation, contributing to land shortages and higher land prices that make real estate development even more expensive.

To help alleviate the inflationary impacts of military rental demand on the Hawai’i’s housing market, our report recommends that all active-duty service members be housed on base.

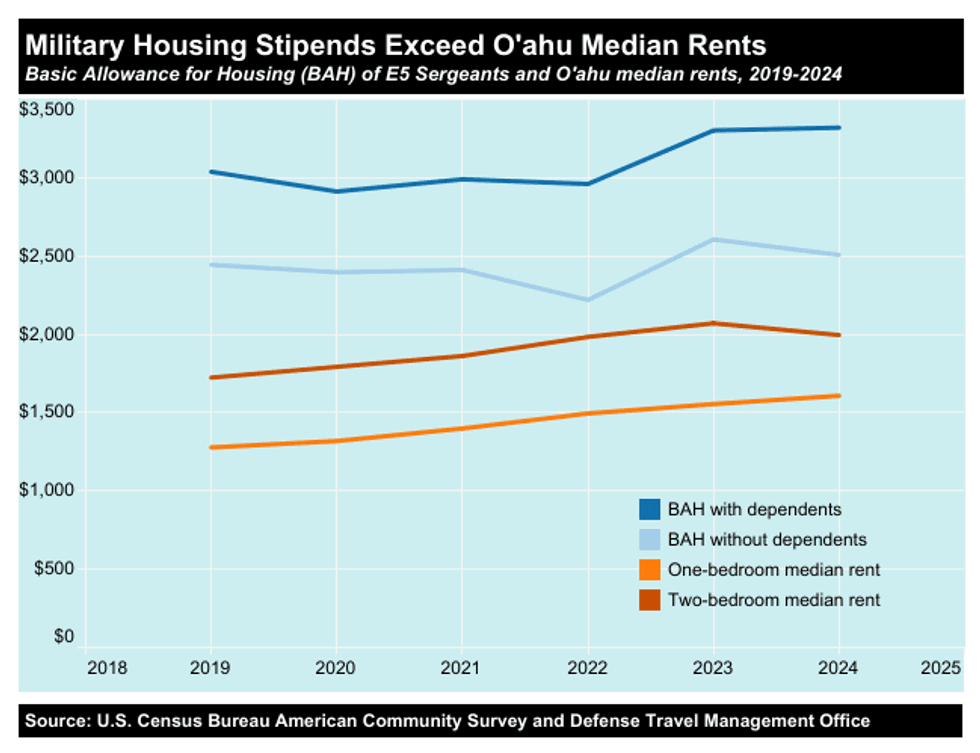

More than 98% of the 42,503 active-duty service members in Hawai’i were stationed in O’ahu in the summer of 2024. But not all of them lived on base. According to the Department of Defense, there were 14,700 active-duty service members who entered the private rental market. We estimate that they resided in 10.3% of the 142,130 renter-occupied units in Honolulu County.

Not only does the military have a significant presence in O’ahu’s rental market, but it also contributes to upward pressures on Hawai’i’s housing prices because of the tax-free stipends—known as Basic Allowance for Housing or BAH—that active-duty service members receive on a monthly basis.

Local residents have difficulty competing with compensation packages bolstered by BAH payments, making military renters more attractive to landlords.

An E5 Sergeant, a rank of enlisted personnel who have been promoted to lead a small team or section, with dependents and four years experience, had a base pay of $40,388 and a BAH of $39,852 in 2024 for a total of $80,240. This is $10,000 more than the average annual salary of an urban Honolulu worker, who earned $70,179 (a mean wage of $33.74) in the same year. This difference does not include food allowances and bonuses that military personnel also receive.

The graph below demonstrates that E5 non-commissioned officers with and without dependents can comfortably afford a one- or two-bedroom apartment while more than half of Hawai’i’s working-class residents are cost-burdened, i.e. they spend more than 30% of their income on rent and utilities. Other households struggle to afford to rent and are forced to leave Hawai’i altogether, particularly to Nevada, which is often jokingly referred to as Ninth Island.

It is clear that the BAH contributes to rental market tightness, and thereby higher prices. However, further analysis is stymied by a lack of data transparency from the Department of Defense. We know the DOD spent $27.9 billion to endow the BAH program in 2024, but we have no information on how those resources are distributed state-by-state nor how much BAH money enters the rental market.

Our report estimates that the DOD spent $1.1 billion on BAH just in O’ahu with more than half of that money—$648.9 million—entering the private rental market. The average BAH monthly payment per service member is $3,679, and we estimate this dynamic caused rents to increase by 7.1% in 2024. As a result, non-military tenants in O’ahu spent an estimated $234.8 million more in rent that year.

To help alleviate the inflationary impacts of military rental demand on the Hawai’i’s housing market, our report recommends that all active-duty service members be housed on base.

Vacancy rates at military installations should be 0%, and the number of service members in the private market should also be zero. The US military should disclose how many on-base housing units they own, operate, and monitor. And new, dense military housing should be built if necessary.

Critical tenant protections like rent control need to be implemented in order to provide immediate relief for renters. And the development of permanently affordable social housing is necessary to deliver high-quality and inexpensive housing. Sixty-five percent of all new units need to be set at 80% of area median income, and market-based solutions have proven incapable of delivering affordability to lower-income households.

Our findings demonstrate that the military plays a significant role in Hawai’i’s affordability crisis, but there are steps that can be taken to make Hawai’i affordable to the people of Hawai’i.

They knew they had to avoid violence, and when the judicial delegation arrived, the activists did not physically engage them, but simply blocked the entrance to the house, tried to talk them out of evicting Lluís and refused to move. There was little the two police officers could do, and the eviction was postponed. Two days later, the PAH released the video of the demonstration, providing proof of what would later become one of the movement’s slogans: “Sí se puede!”

Members of PAH hold a protest. (Photo by PAH-Barcelona)

Members of PAH hold a protest. (Photo by PAH-Barcelona)

Civil disobedience as a tactic to stop evictions became part of the PAH’s regular activity. “What we have to do to stop evictions has become so normalized that when we talk about it at the assembly, we don’t speak in terms of ‘we’re engaging in civil disobedience,’ although that is what we do, and perhaps we should reflect more on that,” ponders Berni from PAHC Bages. “The PAH emerged at a time when thousands of evictions for mortgage defaults were taking place and the issue affected a lot of people who thought they were middle class; in the public discourse, everyone saw that this was something dramatic and unfair,” recalls Emma from PAHC Sabadell. “The fact that in this context, a group of people spoke out to draw attention to this injustice and engaged in nonviolent but active civil disobedience led to the success of the PAH model and its acceptance within society,” she concludes.

“The experience of protesting inside a bank with fifty people is really fulfilling, it takes away your fear and it empowers you.”

To ensure that the platform’s civil disobedience continues to be successful, it’s vitally important for it to preserve that legitimacy. That means being able to justify each and every action as legitimate. Although it will sometimes react to emergency situations, the PAH only takes action on evictions affecting people already involved in the platform. At their assemblies, PAH groups make it clear that they’re not an eviction prevention service, but that they work on the basis of mutual support and only try to block evictions when the people being evicted do not have proper alternative housing.

Beyond the general idea behind these actions—to resist peacefully at the entrance to the building to prevent the judicial delegation from entering—they must be carefully planned and roles must be assigned to make sure everything runs smoothly. If there are minors in the family’s care, a solution must be found to ensure that they aren’t in the house at the time when the eviction is scheduled. It’s very important to support the family, who might be out on the street with their compas, or prefer to resist from inside their home. It’s also very important to remember that the action revolves around their interests and they must be kept informed of what’s happening and able to make decisions when necessary.

Outside, the aim is to keep people’s spirits up while they wait for the judicial delegation to arrive, which might take the whole morning. It’s important to have people to energize the protest in creative ways and give directions. Although people can move around, someone must be responsible for making sure that the door is always protected.

It’s also important to decide in advance how to communicate the purpose and legitimacy of the action to the public, and who will be in charge of communicating with the authorities and the media, rather than leaving it to be decided on the spot.

It’s also helpful to consider preparing the affected person how to deal with the press, if necessary. The movement’s social media presence and its relationship with the media are also very important, as these are tools that can be used to amplify the PAH’s demands and reinforce its legitimacy.

Members of PAH-Barcelona stick flyers on a bank window. (Photo by PAH-Barcelona)

Members of PAH-Barcelona stick flyers on a bank window. (Photo by PAH-Barcelona)

The PAH has an extensive repertoire of actions that goes far beyond stopping evictions. In fact, stopping an eviction is not usually the final solution, but a postponement that should make it possible to find a more permanent answer to the problem. This might require action against financial institutions, public authorities or water, electricity, and gas companies. Besides taking action in support of specific cases, big demonstrations can be called to target the institutions responsible for the problems faced by many families.

“I remember the first time we occupied a bank, back in 2010 or 2011. We occupied Caixa Catalunya and the riot police came to kick us out; that was ecstasy, a real high, and then the fear disappeared,” says Delia from PAH Barcelona. “The experience of protesting inside a bank with fifty people is really fulfilling, it takes away your fear and it empowers you.” Many people emphasize the strength of collective action; sometimes the mere act of covering a bank with posters condemning its actions is very powerful. “Wallpapering is a high, an outlet for your rage; you can take out all the hatred you’ve built up inside and stick it all over the institution,” says Juan Luis from PAH Torrevieja.

That’s where the festive tone and creativity of the PAH’s actions come in. Even if you’re protesting against a very difficult issue, you have to make room for joy. If you occupy a bank, you can use the leaflets that are there for anyone to take as confetti and play music or put up balloons and banners. “It wiped away my fear of the bank when I saw how all the employees could leave and the office would be left alone, occupied by activists,” says Juan Luis. The PAH manages to paralyze the bank’s activity without confronting anyone or even directly hindering its work. The movement’s actions are simply intended to make its presence felt because the bank is unwilling to continue its activity in these conditions.

Of course, everyone experiences these actions in their own way and that’s why some groups in Madrid organize what they call “fear workshops.” “These are workshops for people to learn how to act during an action: how to avoid losing their temper or falling for police provocation, how to rely on colleagues. In short, how to overcome yourself so that you can go to the protest, even if you’re afraid, because nothing is going to happen to you in 90 percent of the cases,” explains Alejandra from PAVPS [Platform for People Affected by Public and Social Housing], Madrid.

It’s also important to think about how to look after people in these protests. This can be done, for example, by warning when there’s a possibility that the police show up and recommending that people in an irregular administrative situation stay away to avoid unnecessary risks. “Besides that, they tell you how to act or how to hold onto another person so that they don’t hurt you if they’re trying to remove you by force,” adds Francisco from PAH Barcelona.

This excerpt is adapted from Yes, It’s Possible! A Handbook for Building Power by João França and The Platform for People Affected by Mortgages, published by Common Notions. Copyright (c) 2026 Common Notions. All rights reserved. Do not republish.

Mamdani is running a very New York-focused election campaign, but one that also speaks to low-income and moderate-income voters across this nation. So many in Donald Trump’s America are now facing the possibility of either losing their healthcare or having healthcare that’s simply far too expensive and doesn’t cover what they need. All too many confront rising housing costs or their inability to purchase a home. All too many are seeing the cost of college reach a level that makes it unaffordable for their children and are now experiencing significant healthcare expenses, whether for young children or elderly sick parents, that have become suffocating.

Here in New York City, poverty is already double the national average. One quarter of New Yorkers don’t have enough money for housing, food, or medical care. Twenty-six percent of children (that’s 420,000 of them!) live in poverty. Of the 900,000 children in the city’s public school system, 154,000 are homeless. (And sadly, each of these sentences should probably have an exclamation point after it!) In the face of such grim realities, Mamdani, among other policies, is calling for a freeze on rents in rent-stabilized apartment buildings in the city; making buses free; offering free childcare for those under the age of five; building significant amounts of new affordable housing; improving protections for tenants; providing price-controlled, city-owned grocery stores as an option; and raising the minimum wage.

At its most basic, the Mamdani campaign is about affordability and the dignity of working people.

Make no mistake: Zohran Mamdani distinctly represents the “other” in Donald Trump’s universe. In that world, he’s viewed as not White, which is in itself a crime for so many of the president’s supporters. Trump has always been a divider. As the Guardian reported in 2020 in a piece headlined, “The politics of racial division: Trump borrows Nixon’s southern strategy,” the president warned that, if Joe Biden were to replace him as president, the suburbs would be flooded with low-income housing.

He’s backed supporters who have sometimes violently clashed with Black Lives Matter (BLM) protesters across the country. He even refrained from directly condemning the actions of a teenager charged with killing two protesters in Kenosha, Wisconsin, suggesting that he might have been killed if he hadn’t done what he did. He’s also called the BLM movement a “symbol of Hate.”

With such rhetoric, the president is indeed taking a page or two out of the 1960s “southern strategy,” the playbook Republican politicians like President Richard Nixon and Senator Barry Goldwater once used to rally political support among White voters across the South by leveraging racism and White fear of “people of color.” Much of what drives Republican strategists today is figuring out what can be done to slow and mute the browning of America. It’s always important to remember that race is almost invariably a critical issue in the American election process.

The election of Mamdani in New York City would indeed send a message across the country and the world that this — my own city — is a place where immigrants can achieve political office and thrive. It would send a message that an agenda focused on low-income people — promising to provide them with opportunity, access to needed resources, and assistance — is a winning approach. In truth, Mamdani’s platform and agenda could undoubtedly be used to attract large groups of Americans who might indeed upend the political situation in many conservative districts across America. In other words, it — and Mamdani — are a threat.

The election of Mamdani in New York City would indeed send a message across the country and the world that this — my own city — is a place where immigrants can achieve political office and thrive. It would send a message that an agenda focused on low-income people — promising to provide them with opportunity, access to needed resources, and assistance — is a winning approach. In truth, Mamdani’s platform and agenda could undoubtedly be used to attract large groups of Americans who might indeed upend the political situation in many conservative districts across America. In other words, it — and Mamdani — are a threat.

As an observer of the Mamdani campaign, I can’t help reflecting on the civil rights struggle I was engaged in during the 1960s in the South. The challenges were enormous and the dangers great, but we made lasting change possible.

I hear a lot about the number and intensity of the workers in the Mamdani campaign. From my own past experience, I believe that the intensity of those involved in his campaign, the fact that many of them are workers, and their focus on affordability add up to a distinctly winning combination.

Let me now break down the future Mamdani experience as mayor of New York into four categories:

Vision

Zohran Mamdani has what it takes to be a great mayor because he has a vision that speaks to so many sectors of New York’s population, emphasizing as he does the dignity of working people and hope as an active force to put in place meaningful programs for a better future. He articulates a future for this city that is more equitable and will make it so much more livable for so many. As a politician, he’s both an optimist and unafraid to propose big solutions.

Dignity

At its most basic, the Mamdani campaign is about affordability and the dignity of working people. I’ve lived in this city for nearly 60 years and raised my family here. My wife was born here and has lived here her entire life. She was raised by a single father who worked for a fabric company. We managed to build a middle-class life, but right now such a future is anything but a given for so many in a city that has become all too difficult for working people to remain in and create a life worth living.

Make no mistake: Zohran Mamdani distinctly represents the “other” in Donald Trump’s universe.

It’s no small thing that, at this moment in the city’s history, Mamdani has made affordability the central issue of his campaign and suggested that a more affordable New York can be created based on a tax increase on those earning more than a million dollars annually. His focus on the dignity of working people and their families allows his message to have a deep resonance among the population and reach the young, the middle-aged, and the old. His focus is on how New York City can restructure its operations so that it serves us all, not just the well-off and the rich.

Hope

I suspect Zohran Mamdani recognizes that his focus on dignity is also connected to “hope,” and that such hope would be an active force in achieving change. His version of hope isn’t about mere optimism. It’s much broader than that. I was a member of the last generation born into segregation and a Jim Crow system in the American South. During my college days, the most powerful voice for dignity and hope in America was Martin Luther King Jr. He was just 26 years old when he was asked to lead the fight for civil rights and against segregation and Jim Crow in Montgomery, Alabama. Though that fight, in which I was a participant, did indeed seek to end segregation, it was equally about securing a sustainable economic life for Blacks. Indeed, Martin Luther King lost his life fighting for a decent wage for sanitation workers in Memphis, Tennessee.

Zohran Mamdani has been influenced by Dr. King when it comes to his focus on the issues of Dignity and Hope (which should indeed be capitalized in Donald Trump’s America). In a recent interview in the Nation Magazine, responding to a question about how he defines himself, and if he considers himself a democratic socialist, he said, “I think of it often in terms that Dr. King shared decades ago: ‘Call it democracy or call it democratic socialism. But there must be a better distribution of wealth within this country for all God’s Children.’” King believed that hope was not a passive but an active force. As he once said, “We must accept finite disappointment, but never lose infinite hope.”

Inclusiveness and Outreach

I spent 36 years working in the New York City and New York state government, much of that time as the leader or commissioner of agencies impacting the daily lives of citizens. I served under mayors Ed Koch, Mario Cuomo, David Dinkins, Michael Bloomberg, and Bill de Blasio. I was City Personnel Director, Commissioner of Human Rights for the State of New York, and Director of the Bureau of Labor Services. I finished my government service with a 16-year stint as Deputy Fire Commissioner for the Fire Department of New York City. And I know one thing: it’s critical to have vision and purpose if you plan to lead such a city successfully. In addition, a mayor can only put in place big ideas and see them to fruition if he’s connected to all the diverse constituencies and array of institutions that also work daily to reach citizens. In terms of outreach, Governor Mario Cuomo, the father of Andrew Cuomo, once told me that he judged a commissioner by how much time he spent in the community talking and listening to people as opposed to sitting in the office.

New York City has a population of 8.5 million people, which swells each day to more than 15 million, if you include all the commuters and visitors who must be served. With an annual budget of nearly $116 billion, it would be difficult for any mayor to manage. No one can truly be prepared for it, so it’s critical that the mayor selects a group of managers who have the experience and moxie to achieve his or her goals. I’m not concerned about Mamdani’s youth because no one becomes mayor with the singular management skills to confront such a giant budget and the diverse, powerful interest groups within the metropolis. None of those who preceded him, not Koch, Dinkins, Giuliani, Bloomberg, de Blasio, or Adams, could have led the city without the help of a cadre of able managers. Some chose well. Some chose poorly.

It’s critical, though, that if he wins on November 4th, a future Mamdani administration be composed of astute, experienced managers, from first deputy mayor to all the agency heads. And it’s not merely the agency heads who must be capable and well-focused, but all the other managers and deputies within those agencies, too. After all, in New York City, from fiscal crises to snowstorms, sanitation issues to policing, violence in the streets to ethnic tensions, education to housing, union negotiations to potential conflicts with New York State and the federal government, crises erupt on a remarkably regular basis. And don’t forget the more than 210,000 migrants who have arrived in the city since the spring of 2022 in search of an opportunity for a better life. All of that can overwhelm any mayor.

As a result, assuming he wins, Mamdani’s Transition Committee must cast a wide net for the best managers the city has to offer. On the whole, they should be young, yet seasoned. They should be diverse and represent an array of sectors. What he needs are not “yes” personnel but leaders who are themselves astute, critical, and committed to government service. His outreach should be to all races, religions, business areas, and nonprofit groups. As it happens, I’m encouraged by reports in the press of the way he’s already reaching out and I hope he does so in all the years of his mayoralty.

If Mamdani merges a focus on leadership and management with his already clear commitment to expanding affordability, dignity, hope, and opportunity for ever more New Yorkers, then he’ll cement his place in the city’s history and possibly—as Donald Trump grows ever less popular in a distinctly disturbed country—in American history, too.

That’s why this September, dozens of New York City youth organizations, New York City Council members, and 150 youth leaders came together to chart a new vision for our interconnected movements, unveiling the Livable Future Package. Now, the New York City Council Progressive Caucus, a 17-member bloc of elected officials, joins our campaign centered on the four most urgent crises facing New York City youth.

The priorities include 1) the NYC Trust Act, which will strengthen enforcement of our sanctuary city laws. 2) Intro 1180 to lower utility bills and hold ultra-wealthy landlords accountable by enforcing our landmark 2019 climate and energy efficiency law. 3) The Community Opportunity Purchase Act, which will give community organizations the first chance to purchase buildings, providing youth communities a pathway to stable housing over corporate speculation. Lastly, 4) City G.I.R.D.S. and a companion bill to make sure that young trans, non-binary, intersex, and gender-nonconforming New Yorkers in the jail and prison systems have access to housing decisions aligning with their identity and to gender-affirming medication and items.

“We grew up in New York. We want to stay here, and I want to be proud of the place I am from.”

This is a model for a city government that stands up for our generation in the face of fascism and won’t back down from the fight for a city we can afford.

The Livable Future coalition spans both traditional movement divides and the five boroughs. Our coalition, from middle schoolers to young adults newly entering the workforce to sitting NYC Council members, collectively shares in the belief that a livable future is possible. Our future is not just 100 years into the future; it’s 2026, 2030, and every minute in between.

The 15+ youth organizations behind the Livable Future Package united at the September 20 Make Billionaires Pay March, holding banners for each of the bills and demanding New York’s leaders put their future over Trump-allied billionaires. (Photo by Ken Schles)

The 15+ youth organizations behind the Livable Future Package united at the September 20 Make Billionaires Pay March, holding banners for each of the bills and demanding New York’s leaders put their future over Trump-allied billionaires. (Photo by Ken Schles)

Our campaign presents a road map for our youth movements in cities across the country. From New York City to Los Angeles, Chicago to DC, and Houston to Philadelphia, we can and we must organize our cities as fortresses against encroaching oligarchical fascism.

Leaders across New York City have already taken note of our organizing, joining us at our launch event in September and for rallies outside City Hall.

As youth-leader Emma Rehac of Youth Alliance for Housing said at one of these events, “We grew up in New York. We want to stay here, and I want to be proud of the place I am from.”

“The Livable Future Package is about ensuring New York is a city that stands up for all our communities. We deserve to afford to grow old in the neighborhoods we grew up in, to live in a place that defends against detention and deportation—somewhere that takes action to fight the climate crisis and for affordability, and ensures our basic human rights are protected no matter our gender identity.”

Our work on the package is just beginning. The Council, led by Speaker Adrienne Adams, and the mayor have a choice.

Will they stand by as our city capitulates to Trump? As ICE floods our schools, and our future disappears? Or, will they join us and pass the Livable Future Package by the end of the year?

We hope they will help us build a city that stands up, that fights back, and charts a livable, affordable future for the next generation.