SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

The new debt ceiling agreement will achieve the essential goal of avoiding a potentially catastrophic default in the days ahead. But to say that the deal is likely to lead to highly unbalanced results would be an understatement. The deal places the nation on a disturbing policy course and sets what may become important precedents that are cause for serious concern.

The agreement starts with nearly $1.1 trillion (or $840 billion, depending on the budget baseline used) in discretionary (i.e., non-entitlement) spending cuts over ten years, enforced by binding annual caps through 2021. It also calls for a Joint Select Committee on Deficit Reduction to propose, by November 23, steps to reduce the deficit by at least another $1.5 trillion over ten years, and for the House and Senate to consider the proposal under fast-track procedures that guarantee an up-or-down vote in both bodies, with a simple majority needed for passage. If policymakers achieve less than $1.2 trillion in deficit reduction through this process, an automatic across-the-board cut in non-exempt discretionary and entitlement programs will take effect to make up the difference between what they accomplished and the $1.2 trillion target.

Multi-year discretionary caps were included in the major 1990 and 1993 deficit reduction agreements -- but as part of larger deals that also included revenue increases. As we have noted repeatedly in recent years, establishing multi-year discretionary caps without an agreement on increased revenues makes it even harder to secure revenue increases for deficit reduction in the future. That's because the only way to secure a bipartisan agreement that includes increased revenues is to provide anti-tax policymakers with significant spending cuts in return, likely including substantial savings from imposing discretionary caps. With 10-year discretionary caps already in place (and with the potential for across-the-board cuts that would further cut discretionary programs), there will be little prospect to exchange substantial discretionary cuts in return for revenue increases unless policymakers who support a meaningful federal governmental role are willing to accept even deeper, more draconian cuts in discretionary programs than the $1.1 trillion in such cuts the agreement already requires.

To be sure, the joint committee will have the legal authority to produce a balanced package that includes revenue increases as well as program cuts. But House Speaker John Boehner, in an effort to secure votes for the deal, is undermining the joint committee before it's even established. Boehner has circulated documents to his caucus claiming the agreement requires the use of a "current-law revenue baseline," thus "making it impossible for Joint Committee to increase taxes." That's flatly not true, as my colleague Jim Horney has ably explained; the agreement does not require the joint committee to use any particular baseline, and the joint committee is free to adopt revenue-raising measures if it so chooses.

But the fact that one party is being led to believe that the deal does bar the joint committee from raising tax revenue is not helpful, to say the least. And coupled with Speaker Boehner's pledge not to name any members to it who will raise any tax revenue at all and to defeat any joint committee-produced package on the House floor if it raises any revenue, this seems to give the joint committee only three places to go -- severe cuts in entitlement programs, deep cuts in entitlements coupled with even deeper cuts in discretionary programs (i.e., cuts on top of the at-least $1.1 trillion in discretionary cuts that the annual caps will produce), or a failure to meet its target.

If the joint committee were only to cut entitlement programs to reach its target, how deep would those cuts be? The deal that President Obama and Speaker Boehner were negotiating several weeks ago would have raised Medicare's eligibility age, raised Medicare cost-sharing charges, shifted significant Medicaid costs to states, modified cost-of-living adjustments in Social Security and other benefit programs (and in the tax code), and instituted other entitlement savings. Those steps would have saved $650 billion to $700 billion over ten years. The joint committee would have to produce cuts twice as deep -- and roughly twice as deep as those in the Gang of Six plan.

Democrats on the joint committee would not conceivably agree to entitlement cuts, or a mixture of entitlement and deeper discretionary cuts, that deep. Hence, if Speaker Boehner honors his pledge to keep revenue increases off the table, the committee will surely fail -- and gridlock and policy warfare will continue.

The joint committee could agree on a much smaller amount of savings without revenues, but nothing close to $1.2 trillion to $1.5 trillion. Thus, unless Republicans back off their refusal to consider any increase in revenues, the joint committee will fail to produce savings anywhere close to $1.2 trillion -- triggering across-the-board cuts that are of unprecedented depth and will remain in place for nine years.

In key respects, then, this deal postpones the biggest battle over deficit reduction, creating an even more cataclysmic clash that would occur most likely in a lame-duck congressional session after the 2012 election. At that point, three huge events will loom: 1) across-the-board cuts in January 2013, with half of them coming from defense (amidst likely charges that they will jeopardize national security); 2) the scheduled expiration of President Bush's tax cuts at the end of 2012; and 3) the renewed specter of default if policymakers do not raise the debt ceiling quickly again by early 2013. Where all of that will lead policy debates and outcomes is impossible to predict at this point.

Anticipating the policy battles to come, we should not lose sight of an alarming development. Those who have engaged in hostage-taking -- threatening the economy and the full faith and credit of the U.S. Treasury to get their way -- will conclude that their strategy worked. They will feel emboldened to pursue it again every time that we have to raise the debt limit in the future.

They also will likely continue insisting, in future hostage-taking efforts, that for every dollar we raise the debt ceiling, we must cut spending by a dollar, with no revenue allowed. When one considers that even the harsh budget plan of House Budget Committee Chairman Paul Ryan would require policymakers to raise the debt limit by nearly $9 trillion over the coming decade, one begins to understand the extraordinary results such a policy path would produce over time. Substantial parts of the federal government, including important parts of the Great Society and even the New Deal, would be cut sharply or eliminated. That would put us on a path toward achieving anti-tax activist Grover Norquist's vision of shrinking government to the point where "we can drown it in the bathtub."

Having said all this, the agreement has some partially -- but important -- redeeming features. For one thing, the Administration ensured that half of the automatic cuts that could be triggered will come from defense programs, and that basic entitlement assistance programs for low-income Americans, as well as Social Security, will be exempt from such cuts. This could provide helpful leverage for a more balanced solution in the showdown likely in the 2012 lame-duck session. For another, the deal raises the debt ceiling until about early 2013, so the nation's credit will not be threatened in coming months by election-year politics. (On a smaller front, the Administration secured beneficial provisions related to Pell grants.)

Our grim assessment of the agreement, its very disturbing implications, and the policy and political trajectory that we now face are not arguments for defeating the agreement on Capitol Hill. There is an adage that, as bad as things get, they can always get worse. If Congress defeats the package, one or both of two very troubling developments may well occur: we may experience a default, with potentially catastrophic consequences for the economy and the nation's future; or policymakers may quickly rejigger the deal, making it still more unbalanced in order to secure more arch-conservative votes. These are risks that are simply too dangerous to take -- despite the deeply troubling problems that this deal poses.

The Center on Budget and Policy Priorities is one of the nation's premier policy organizations working at the federal and state levels on fiscal policy and public programs that affect low- and moderate-income families and individuals.

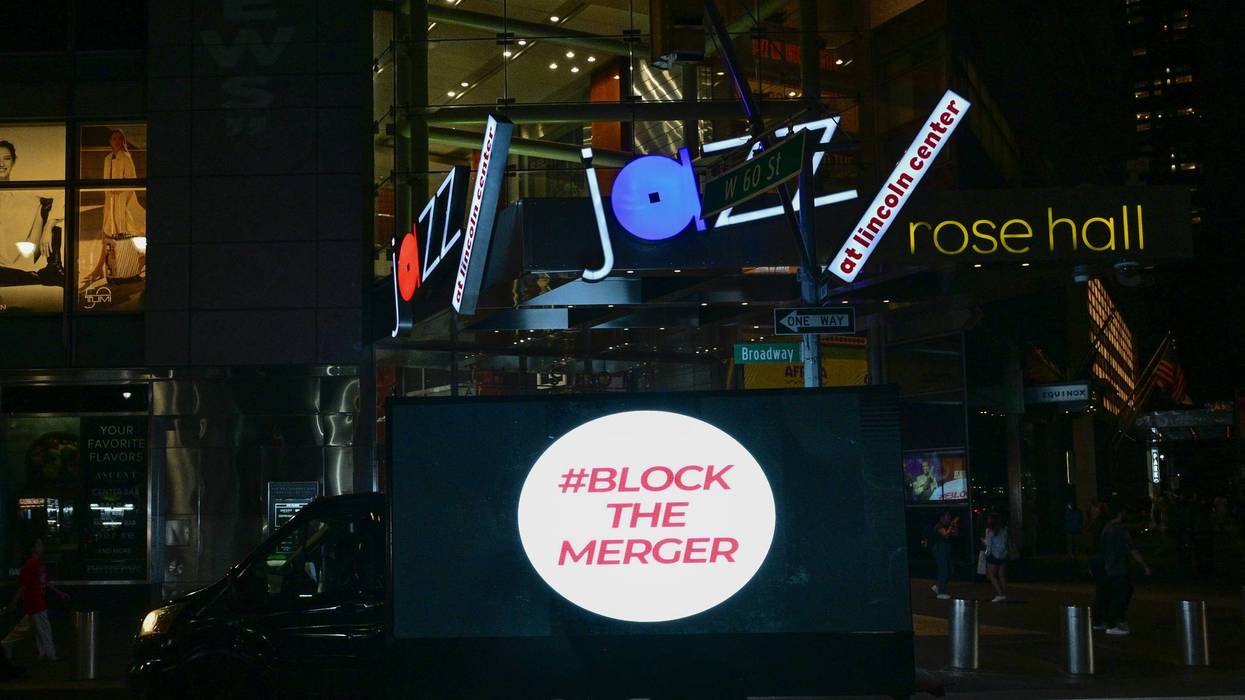

California's attorney general called the development "great news for audiences, movie theaters, and the many people who write, build, and create the art, news, and entertainment so many of us enjoy."

Paramount Skydance on Friday officially delayed its attempted acquisition of Warner Bros. Discovery after a federal judge in the Northern District of California temporarily blocked the $111 billion deal at the request of a dozen Democratic attorneys general.

US District Judge Araceli Martínez-Olguín granted the temporary restraining order on Monday after finding that the plaintiffs—led by California Attorney General Rob Bonta—provided "compelling evidence that the combined firm resulting from the transaction will possess substantial market share in the wide-release theatrical distribution market." She extended the order on Thursday.

The companies have now agreed not to close the deal—also the target of a Writers Guild of America lawsuit—until five days after a trial is held or June 1, 2027, whichever is sooner. While the attorneys general and their supporters framed the development as a victory for their side, a Paramount spokesperson similarly said that "today's agreement is a significant win because the result is exactly what we have sought from the outset: a direct path to a trial based on the evidence."

"This is the fastest and clearest way to prove that this transaction is good for competition, good for consumers, and good for creators, a conclusion dozens of competition authorities around the world have already reached," the spokesperson continued. "Plaintiffs' market definitions bear no relationship to the realities of today's marketplace and cannot withstand scrutiny. We look forward to proving our case at trial."

Meanwhile, Bonta said in a statement that "our argument against this illegal merger is straightforward: When too few corporations have too much power in markets central to American life, it makes things more expensive, and it makes things worse."

"Today's agreement is great news for audiences, movie theaters, and the many people who write, build, and create the art, news, and entertainment so many of us enjoy," he emphasized. "We are eager to continue to make our case in court and celebrate another tremendous win in our effort to ensure this unlawful merger never sees the light of day."

Joining Bonta in battle are the attorneys general of Arizona, Colorado, Connecticut, Massachusetts, Minnesota, Nevada, New Jersey, New Mexico, New York, Oregon, and Washington. They, too, celebrated on Friday.

"Stopping this merger while our case proceeds is a critical victory in our efforts to uphold the law and protect the film and television industries," New York's Letitia James stressed on social media. In a video, New Jersey's Jennifer Davenport also called the companies' decision "a huge win for consumers" and pledged to "continue to fight to block this merger for good."

Responding to one of Davenport's social media posts, actor and activist Mark Ruffalo declared: "Today's news is a repudiation of Paramount's strategy of currying favor with the Trump administration to grease the wheels on this illegal merger—from sham settlement payments to manipulating its own news coverage. Stay strong and #BlockTheMerger."

Some opposition to the deal is rooted in the fact that it would give Paramount CEO David Ellison—the son of billionaire Larry Ellison, a major donor to President Donald Trump—control of CNN, as he already faces mounting criticism for his and Bari Weiss' management of CBS News.

"The Ellisons believed their relationship with President Trump would help them push through a disastrous deal that threatened democracy, creative freedom, and independent journalism. We in the #BlocktheMerger campaign helped prove them wrong," said Norm Eisen, co-founder and executive chair of Democracy Defenders Fund, in a statement.

"Paramount's decision keeps two major studios competing instead of handing one company even more power over what Americans watch, what they pay, and where entertainment workers can earn a living," he continued. "The merger would have eliminated one of Hollywood's largest buyers of scripts and productions while placing Paramount+, HBO Max, CBS News, CNN, and dozens of local stations under the management of one company."

"This victory in putting the merger on hold belongs to the people who refused to treat the merger as inevitable," Eisen added. "Artists, journalists, filmmakers, and consumer advocates spoke out despite the risk of retaliation, more than 5,500 people signed our open letter, and Attorneys General Rob Bonta and Letitia James, along with 10 other attorneys general, acted. This collective resistance is turning the tide."

Craig Aaron, co-CEO of the advocacy group Free Press, said that "Paramount tried to tell us this deal was a slam-dunk, but it just shot an airball. Late in the game, Paramount's lawyers grasped what we've said all along: The states have a very solid case that this deal violates US antitrust law. For the broad and growing coalition against this corrupt and dangerous deal, this delay marks a significant victory."

"Instead of fighting against an injunction and possibly losing now, Paramount's lawyers have resigned themselves to waiting for a full antitrust trial in federal court," Aaron added. "Paramount can pretend all it wants that it looks forward to that test, but that’s just more bluster from company mouthpieces trying to spin a major setback. Now this deal will face its day in court, and we are confident the evidence will show this mega-merger should be blocked."

“The federal government cannot build secret dossiers on people because they exercise their First Amendment right to peacefully observe, document, or criticize its actions," said the head of Democracy Forward.

A coalition of privacy and civil liberties advocates filed a federal lawsuit Friday accusing the Trump administration of secretly collecting and keeping personal information about people who monitor US Immigration and Customs Enforcement operations, arguing that the practice violates federal privacy law and threatens constitutionally protected speech and association.

The lawsuit—filed in the US District Court for the District of Columbia—was brought by individuals and advocacy groups represented by Democracy Forward.

The plaintiffs—the Electronic Privacy Information Center (EPIC) and legal observers Nicole Cleland, Jacquelyn Ivey, and Anna Walker—argued that the US Department of Homeland Security (DHS), US Immigration and Customs Enforcement (ICE), and other federal agencies created and maintained databases of people who observed, documented, or protested immigration enforcement activities without providing notification or safeguards, as required under the Privacy Act of 1974.

That law was passed after the exposure of illegal government surveillance, including longtime former Federal Bureau of Investigation Director J. Edgar Hoover's infamous COINTELPRO program, under which the FBI, in addition to conducting unlawful spying, funded and armed murderous far-right militants to terrorize anti-Vietnam War protesters, anti-nuclear weapons activists, civil rights leaders including Martin Luther King, Jr., and other leftists.

“The federal government cannot build secret dossiers on people because they exercise their First Amendment right to peacefully observe, document, or criticize its actions," Democracy Forward president and CEO Skye Perryman said in a statement announcing the lawsuit. "That is exactly the kind of government surveillance Congress sought to prevent when it enacted the Privacy Act after some of the darkest chapters in our nation’s history."

The lawsuit accuses the Trump administration of collecting the names, photographs, vehicle information and license plate numbers, social media accounts, and other identifying information about legal observers, volunteers, journalists, clergy, and community members engaged in First Amendment-protected activities during the government's deadly anti-immigrant crackdown.

"When the Department of Homeland Security dramatically ratcheted up its immigration enforcement, people across the country—of all ages and backgrounds—did what anyone is supposed to do when they disagree with government action: They exercised their First Amendment rights," the suit states. "They peacefully protested. And, as matters here, they observed and recorded how law enforcement agents acted in public."

DHS is using facial recognition technology, body cameras, license plates, mobile devices, and other surveillance tools to identify, track, and punish people who legally observe immigration enforcement in public. This is a clear violation of the Privacy Act. We’ll see them in court.

[image or embed]

— Democracy Forward (@democracyforward.org) July 24, 2026 at 10:36 AM

"In response, DHS decided to record the Americans who were peacefully observing its agents, adopting a secret Protester Surveillance Policy enabling its agents to first collect records on Americans engaging in First Amendment exercise and then maintain them in DHS systems, where they can be used to retaliate against those Americans," the complaint continues.

"Beginning sometime in 2025, DHS deployed a dragnet of drones, bodycams, face-scanning apps, license plate scanners, and camera phones to, as one memo instructed, 'capture all images, license plates, identifications, and general information on hotels, agitators, protestors, etc., so we can capture it all in one consolidated form,'" the document notes.

"DHS agents have not been shy about gathering this information or its purpose," the plaintiffs contended. "In Maine, DHS agents told multiple observers that they were being added to a database of 'domestic terrorists.' In Chicago, agents routinely used facial irecognition scans on members of the public."

"In Minneapolis, observers simply watching agents on public streets have been led by those agents to their own houses, despite never having interacted with an agent—a practice so common that it has been named 'being driven home by ICE,'" the suit says. "And across the country, DHS agents have approached observers and addressed them by their full names, even though those observers never identified themselves to the agents or showed them any form of identification."

"As a result of its Protester Surveillance Policy, DHS has recorded and retaliated against each individual plaintiff," the filing alleges. "It’s bad enough that DHS publicly collected information on Americans engaged in lawful First Amendment exercise. But worse, DHS also decided to maintain the information in one or more of its systems, enabling it to later retaliate against observers and protestors—including by canceling Trusted Traveler status," which includes Transportation Security Administration Pre-Check and Global Entry.

The plaintiffs are asking the court to declare the DHS surveillance policy unlawful, end it, and ban the agency from continuing to collect and keep records of individuals’ protected First Amendment activities.

“Now more than ever, those of us who have the privilege to speak out have a responsibility to defend the rights of everyone in our communities,” Walker said in a statement. “When people are punished for exercising their First Amendment rights, we begin losing the democratic principles that protect all of us. Every American should be alarmed by retaliatory action against one’s free speech."

Cleland said: “I believe government accountability starts with transparency. People should be free to peacefully observe and document what their government does in public without worrying they’ll be tracked or retaliated against. This case is about protecting that right for everyone.”

EPIC deputy director John Davisson warned, “When our government compiles secret dossiers on everyday people for exercising their constitutional rights, it sends a chilling message: If you speak up, watch your back."

"If every protest, every recording, every act of dissent opens us up to surveillance and retribution, privacy and free speech are at risk of collapse," he added. "But the laws of this nation don’t permit that, and we won’t either.”

"It is despicable that the administration is taking away funding from states that did not vote for Trump," said US Sen. Dick Durbin.

President Donald Trump's administration has admitted in court that it chose to cancel certain grants for clean energy projects because they were set to benefit Democratic-voting states.

The New York Times reported on Friday that attorneys representing the US Department of Energy (DOE) acknowledged in court documents filed earlier this month that decisions about canceling grants were based "solely on the political identity of the grant recipient’s state, i.e., whether the recipient’s location and/or place of performance was in a Blue State or a non-Blue State."

The Times described this as a "stunning admission" that "offered an unvarnished glimpse into the way President Trump has weaponized the provision of federal education, energy, health, housing, and infrastructure aid in his second term."

According to the Times, the DOE last year recommended canceling more than 600 grants awarded for energy projects under former President Joe Biden's administration.

However, the White House Office of Management and Budget only made 284 of the recommended cuts while leaving the rest of the grants in place.

After a group of California researchers challenged the terminated grants in a lawsuit, the DOE acknowledged that "with one exception, the 284 terminated grants had a recipient location and/or at least one place of performance in a state that awarded its electoral votes to Kamala Harris in the 2024 election and has two Democratic-caucusing senators."

The DOE also admitted that there was no "programmatic, statutory, cost-reduction, or performance-based factor" to justify the cuts.

In a social media post, New York Times reporter Tony Romm noted that the DOE made these admissions "as part of a process meant to avoid discovery" and "perhaps spare it from sharing more damaging records" in its possession.

The Times report drew a sharp reaction from Trump administration critics.

"This is corruption," said Rep. Laura Friedman (D-Calif.). "It’s how this administration has acted since day one: punishing states, businesses, and ordinary Americans who push back on Trump. It’s a major betrayal of our nation that will lead to higher energy prices and should be condemned by people of all political parties. It’s un-American and despicable."

Sen. Andy Kim (D-NJ) accused the administration of "the weaponization of government" with its selective grant cancellations.

"This administration shows us time and time again they only care about one person," Kim added, "and that person only cares about himself."

Sen. Dick Durbin (D-Ill.) argued that the filings prove "what we have long known, that their grant cancellations were not based on 'waste' or sound policy but vindictiveness."

"It is despicable," Durbin emphasized, "that the administration is taking away funding from states that did not vote for Trump."

Jennifer Victory, political scientist at George Mason University, described the administration's scheme as "violations of the rule of law that would be sufficient for impeachment in any other American presidency but aren't in this one because pathological partisan loyalty has rotted the constitutional order."

Sam Stein, managing editor at The Bulwark, said that the DOE's admission about targeting Democratic states was "something we all knew and saw at the time and yet still breathtaking to read... in print."

"We urge the commission to withdraw this proposal, enforce the rules already on the books, and return its attention to the derivatives markets it was created to protect—and which genuinely need its attention."

A coalition of consumer advocacy groups on Friday forcefully condemned the Commodity Futures Trading Commission's move to give prediction market platforms like Kalshi and Polymarket "a green light to bypass state gambling regimes."

Users of these platforms can bet on future events, from the outcome of a sports game to the language of a political speech, by buying "shares," or "contracts." The Trump administration claims the platforms are not gambling operations, but derivatives markets because, as Chair Michael Selig has noted, "Congress has entrusted the CFTC with the sole authority to regulate" those.

Various state leaders and organizations have pushed back, arguing that "calling a sports wager an 'event contract' does not transform it into a legitimate tool for managing economic risk," as Demand Progress Education Fund communications director Eric Naing said Friday. "The CFTC should not allow federal derivatives law to become a back door for nationwide gambling."

However, the CFTC has stuck to its position, publicly backed by President Donald Trump, who has declared that the agency must have "exclusive authority" over this "major industry," which "we must protect." The Republican—who infamously bankrupted multiple casinos—notably has a company exploring how to cash in on the sector.

The CFTC announced its proposed rules for prediction markets in March, followed by an update last month. In a Friday letter to the agency chair, Demand Progress Education Fund and 10 other organizations wrote that "we oppose the proposal in its entirety. It fails as a matter of law, as a matter of policy, and as a matter of institutional competence, and we emphatically urge the commission to withdraw it."

"When Kalshi and Polymarket launched just five years ago, they were curiosities; today Kalshi alone is valued at $22 billion and processes an annualized volume of $178 billion in trades every month," the coalition detailed. "This proposal should be understood for what it is: a green light for these immense and largely unregulated financial speculation platforms to offer sports betting nationwide and aggressively market it to the public, bypassing the community and mental health protections that states and tribal authorities have spent generations building to address the risks present in this type of speculative activity."

The fact that 89% of Kalshi's total fee revenue comes from sports-related contracts "should settle the question of whether these companies are derivatives exchanges or sportsbooks," according to the coalition, which also includes Americans for Financial Reform Education Fund, Better Markets, Center for Digital Democracy, New Jersey Appleseed Public Interest Law Center, Open Markets Institute, Oregon Consumer Justice, Oregon Consumer League, Protect Borrowers, Public Good Law Center, and Revolving Door Project.

However, the organizations also challenge the CFTC's interpretation of the Commodity Exchange Act, writing that the proposal's "framing inverts the statute's logic and Congress' intent, by treating contracts as presumptively allowed unless found contrary to the public interest through a case-by-case inquiry."

If the agency charges ahead with its current plans, "ordinary people will pay the price," the groups warned. "Expanded sports betting has increased personal bankruptcies, reduced household savings, and led to higher rates of domestic violence. Prediction markets supercharge these effects: they run 24/7 in your pocket and aggressively market to young adults, who may make low bets initially but ramp up their commitment over time. Seventy percent of users lose money, and 70% of all profits go to 0.04% of traders. Those outcomes define a casino that has figured out how to escape the regulations that casinos have to follow, like responsible gaming disclosures and financial stability protections for their customers."

"The proposal also does almost nothing to address the insider trading problem that makes prediction markets much more easily manipulated than the structures of ordinary gambling," the coalition wrote—just over a week after the White House had to address one of Trump's teleprompter operators allegedly using his access to the president's speech plans to make money on Kalshi.

The organizations further argued that "even if the commission were the right institution to police all of this, it is not capable of doing so. The CFTC, which oversees $400 trillion in US derivatives markets, has a budget frozen at $365 million... Adding nationwide responsibility for sports betting, entertainment wagering, and political gambling on top of that is not a proper expansion of the agency's mission, and it would mean that the farmers, manufacturers, and energy companies who depend on well-functioning commodity markets will pay the price."

"We urge the commission to withdraw this proposal, enforce the rules already on the books, and return its attention to the derivatives markets it was created to protect—and which genuinely need its attention," concluded the coalition. "The regulation of gambling and gaming belongs with the states and tribal authorities that have the experience, the tools, and the democratic accountability to do the job."

Six people were killed as a Palestinian man disarmed and shot Israeli settlers raiding his village in the illegally occupied West Bank.

Israeli Prime Minister Benjamin Netanyahu on Friday announced actions to tighten and accelerate the illegal occupation and colonization of the West Bank after a Palestinian defending his village from rampaging settlers fatally shot two Israelis—whose companions killed four Palestinians in response—while other members of Netanyahu's government called for more ethnic cleansing in Palestine.

Residents of Tell—located 3 miles southwest of Nablus and less than 2 miles from the illegal Israeli settlement of Havat Gilad—said settlers attacked homes on the outskirts of the town at around 8:30 on Friday morning.

According to The Times of Israel, a group of several dozen settlers invaded the village under the pretense of going on a hike. However, as the newspaper noted, Tell is located in an area of the occupied West Bank that is off limits to Israelis unless they obtain permission from the Israel Defense Forces (IDF), which the military said they did not do.

Local Palestinian leader Essam Saifi told Reuters that settlers attacked the eastern part of Tell and tried to break into homes there. When residents emerged to confront the settlers, the intruders opened fire on them before leaving.

Backed by IDF troops, the settlers returned around half an hour later. Video recorded by one of the settlers shows an Israeli firing his gun in the air while his companions, who included minors, shout threats while other settlers stormed local residents' land. A Palestinian man snatched a long gun from a member of the Havat Gilad local security squad and shot him and an IDF major, mortally wounding both men.

Israelis returned fire, killing four Palestinians, including the shooter, and wounding four others. IDF commandos later raided a hospital in Nablus and seized two of the wounded Palestinians.

The Palestinian Foreign Ministry said in a statement that "this massacre represents a renewed image of the ongoing Nakba to which our Palestinian people are subjected," a reference to the ethnic cleansing of more than 750,000 Arabs from Palestine by Zionist forces during the establishment of the modern state of Israel in 1948.

The ministry also condemned "the misleading narratives promoted by the Israeli occupation authorities... in a systematic attempt to turn the executioner into the victim, and to cover up the crimes of murder, field executions, massacres, and grave violations committed by the occupation forces and settler militias against the Palestinian people."

IDF troops subsequently locked down Tell and Nablus while deploying five additional companies to the area and canceling soldiers' weekend furloughs in preparation for imminent "extensive counterterrorism operational activity in the sector.”

Responding to the incident as well as two separate stabbings of Israelis in the West Bank on Thursday, Netanyahu convened a security consultation, which resulted in a joint statement with Israeli Defense Minister Israel Katz announcing a tightening of the occupation and acceleration of the colonization of Palestine—both already illegal under international law.

The statement said Israel will demolish the family home of the Palestinian who shot the two Israelis, confiscate arms and revoke work permits of Palestinians in "villages acting as terrorist hubs," reinforce IDF units throughout the occupied territories, expedite the "legalization of farm outposts" and establish new ones, and increase apartheid checkpoints and road separations.

Israeli Finance Minister Bezalel Smotrich responded to the incident by calling for the destruction and "evacuation"—a term widely viewed as a euphemism for ethnic cleansing—of local Palestinians "for their own protection."

"This is our appropriate Zionist answer to terrorists and terrorism," Smotrich said.

"We will not normalize the erosion of deterrence and the brazenness of our enemies in recent weeks against the pioneers of settlement and the farms," Smotrich, who chairs the far-right Religious Zionism party, said on social media, "I demand that the IDF act with an iron fist against the village of the murderers and its surroundings and restore governance and deterrence."

Israeli National Security Minister Itamar Ben-Gvir, who leads the far-right Jewish Power party, demanded the Palestinian shooter's town be obliterated like Beit Hanoun in Gaza, where Israeli forces have been waging a war that United Nations officials, legal and academic experts, and around 20 national governments have called a genocide.

"For every Jew murdered, the enemy must suffer the loss of land and homes," Ben-Gvir said. "This is the language spoken in the Middle East, and just as we spoke it in Gaza, it is time to speak it in [the West Bank] as well."

Yair Golan, who heads the opposition Democrats, accused Netanyahu and Katz of "a clear intent to set the area ablaze."

"Every escalation in the field endangers human lives—Israelis and Palestinians alike," he added.

David Zini, the head of Shin Bet, Israel's internal security and counterintelligence agency, urged the Israeli public “not to take the law into their own hands and to place their trust in the IDF and the Shin Bet, whose mission and duty this is.”

Many settlers rejected Zini's call and instead carried out revenge attacks on West Bank towns and villages, reportedly including Madama, Urif, Burin, Far'ata, Jit, Qabalan, Sarra, and others, resulting in multiple injuries.

Meanwhile, settlers mourned the killing of the two slain Israelis, 32-year-old Havat Gilad civil defense squad member Benayahu Mellet and 27-year-old IDF Maj. Yuval Ezra.

Extremist settler Meir Ettinger eulogized Mellet on social media, saying that "he was never satisfied with recognized roads and fences, and strived continuously to conquer the region."

“Benayahu always insisted on not making a distinction between areas C and B," Ettinger added.

Under the moribund Oslo Accords, the West Bank is divided into Areas A, B, and C. Area A is under full Palestinian Authority control, while Area B is under mixed control and Area C is under full Israeli control.

Israeli efforts to expand West Bank settlement activity have accelerated dramatically since the Hamas-led attack of October 7, 2023. Attacks on West Bank Palestinians, including pogroms carried out by mobs of settlers protected and sometimes joined by Israeli troops, have killed at least 1,111 Palestinians—at least 243 of them children—since October 2023, according to the latest report published by the UN Office for the Coordination of Humanitarian Affairs.

Israeli officials say 47 Israelis—including IDF troops, security personnel, and civilians—have been killed by Palestinian attacks over the same period.

According to the Israeli human rights group B’Tselem, more than 620,000 Jews currently reside in over 130 settlements in the West Bank and East Jerusalem. While Israel grants every Jew in the world the right to settle there, it has—against UN resolutions and international law—refused to allow the approximately 5 million Palestinian refugees alive today to return to their homeland.

B'Tselem is one of 20 Israeli human rights groups that on Friday issued an "urgent call to the international community to take immediate action to stop Israel's violence and prevent pogroms by settler militias and the Israeli army across the West Bank."

"How far does the 'war on drugs' go?" said a former Ecuadorian official. "Who is held accountable for the lives of Ecuadorian fishermen?"

The recently reported killing of the Ecuadorian prosecutor who had been investigating allegations that three boats from the country had been struck by the US and that dozens of survivors had been abducted and tortured by American forces, was "not a coincidence," said one congressman Friday as he called for a probe into the bombings.

"For almost a year, the US government has been illegally bombing fishing boats and killing people without evidence of wrongdoing," said Rep. Jesús "Chuy" García (D-Ill.). "And last month, Alexandra Bravo, the Ecuadorian prosecutor investigating boats that were attacked or disappeared, was murdered... There must be an independent investigation."

García's demand came a day after Drop Site News reported on Bravo's killing in the city of Manta on June 14.

Police say a hitman on a black motorcycle opened fire on Bravo and her sister at 11:00 am as they were leaving a cafe. Both women were killed and the prosecutor's driver was injured. There was "no sign of the police detail that had been assigned" to protect Bravo, leading the Police Directorate, which operates under the executive branch of President Daniel Noboa, a close ally of President Donald Trump, to investigate whether there had been an "internal security breach."

Bravo had been investigating the cases of three fishing boats—the Fiorella, the Negra Francisca, and the Don Maca—which were reportedly struck by drones in January and March.

The 36 surviving crew members of the latter two vessels reported that they were captured by US forces and subjected to torture before eventually being returned to Ecuador.

Eight fishermen went missing from the Fiorella, and their family members have reported that Ecuadorian authorities have provided little help to them as they look for answers, with the daughter of one missing fisherman saying an official had suggested the crew was involved in drug trafficking.

The three boats were hit with explosives as the Trump administration carried out "Operation Southern Spear," its campaign of boat bombings in the Caribbean and the eastern Pacific. The White House has insisted that the at least 66 strikes that have been carried out by US forces since last September were on boats that were carrying drugs, and the 221 people on board were involved in drug trafficking. Trump has claimed the US is in an armed conflict with Latin American drug cartels, but Congress has not authorized military force in the region.

Legal experts have said that even if the bombed vessels were ferrying illicit substances to the US, military attacks against civilians for their alleged involvement in drug trafficking is against international law.

According to Amnesty International, the Ecuadorian public prosecutor’s office has not submitted a formal request to the US for help with investigating the disappearance of the Fiorella and its crew.

Sources at the police department in Manta and at Human Rights Watch told Drop Site that Bravo had reported facing pressure from the attorney general's office regarding her investigation, with her superiors telling her to treat the alleged attacks on the boats only as "cases of disappearance" and to "close all lines of inquiry" after the 36 survivors of the Negra Francisca and the Don Maca returned, even though they showed signs of torture.

Meanwhile, as the US maintains it had nothing to do with bombing the three vessels, Drop Site reported that a US Coast Guard boat was detected near the Negra Francisca around the time of the bombing before the Coast Guard boat turned off its signal.

Two survivors of the Fiorella bombing, Christian Flores and Dimas Ignacio Álvarez, "corroborated seeing the Fiorella engulfed in smoke and surrounded by American assets."

"In their police statements, Flores and Álvarez described two US aircraft flying over the Fiorella on January 18; multiple grey American drones and a US-flagged patrol ship circling the vessel on January 19; and, on January 20—the day their crewmates disappeared—the large US-flagged patrol ship near the smoke," wrote Camila Lourdes Galarza at Drop Site.

Former Ecuadorian Minister of Foreign Affairs Guillaume Long said Thursday that US military presence in Ecuador as the two countries deepen their military partnership is "a clear violation of our people's sovereignty and popular will."

"Meanwhile, the families of Manta and Jaramijó wait for answers," said Long. "Eight families deserve truth and justice. How far does the 'war on drugs' go? Who is held accountable for the lives of Ecuadorian fishermen?"

"When the Trump administration declares a crisis ‘under control’, it’s time to brace for the worst yet to come," said one critic.

The United States under Trump-appointed Health and Human Services Secretary Robert F. Kennedy Jr. is currently experiencing major public health crises, including record-high measles cases, an outbreak of a parasite that causes explosive diarrhea, and potential salmonella contamination that led to a recall of nearly two million egg cartons.

Numbers released by the US Centers for Disease Control and Prevention (CDC) on Friday revealed that there have been 2,318 recorded cases of measles this year, the highest number of cases recorded since the virus was declared eliminated in the country more than two decades ago.

Some public health experts who spoke with The New York Times said that lower uptake of the measles vaccine was to blame for the outbreak.

Jennifer Nuzzo, director of the Pandemic Center at the Brown University School of Public Health, told the Times that "this is just going to keep happening" in the US unless vaccination rates improve.

"It’s going to mean living in a perpetual state of vulnerability and risk until we get vaccination levels up," Nuzzo emphasized.

Dr. Jonathan Temte, a former chairman of the CDC’s vaccine advisory committee, placed blame for the outbreaks on the US Department of Health and Human Services (HHS) under the leadership of Kennedy, who prior to becoming America's top public health official was best known as an anti-vaccine conspiracy theorist.

“We have seen virtually no national messaging," said Temte. "We’ve seen no ad campaigns... I think that really tells us something about their priorities."

Brad Woodhouse, president of Protect Our Care, also slammed Kennedy's leadership at NHS, accusing him and President Donald Trump of being on "a suicide mission to scare America families away from vaccines without cause or evidence."

"What they’ve accomplished is a huge dip in vaccination rates and the worst measles crisis in 35 years," Woodhouse added. "While the nation’s measles elimination status is doomed, the Trump CDC apparently has not spent a dime on public service ads promoting the one thing that will get us out of the woods: the measles vaccine."

Measles isn't the only disease spreading throughout the country, as the US Food and Drug Administration (FDA) announced on Friday that "four new states... are now considered part" of the outbreak of cyclosporiasis, a foodborne illness that causes explosive diarrhea.

The FDA has said that iceberg lettuce sourced from Taylor Farms de Mexico is likely the source of the outbreak, which so far has led to nearly 2,000 infections and almost 100 hospitalizations.

News about the continued spread of the outbreak came two days after the FDA revealed it was investigating another potential source of cyclospora, the parasitic bacteria that causes cyclosporiasis.

Sen. Jon Ossoff (D-Ga.), who earlier this week demanded answers from Kennedy about his decision to terminate the CDC's previously required surveillance of cyclospora, sent the HHS secretary a letter on Friday ripping his leadership of the department.

"Your silence amidst an ongoing outbreak of diarrheal disease," Ossoff wrote, "is indicative of the reckless arrogance with which you demolished America's public health defense."

Woodhouse, in a statement released Thursday, noted that Kennedy had declared the outbreak "under control" this week even though federal data shows it growing.

"If history is any judge, when the Trump administration declares a crisis ‘under control’, it’s time to brace for the worst yet to come," said Woodhouse.

The FDA also announced on Wednesday that Midwest Poultry Services was voluntarily recalling nearly 1.6 million cartons of eggs over potential contamination by the bacteria salmonella.

As the FDA noted, salmonella infections often result in a number of unpleasant conditions, including "fever, diarrhea (which may be bloody), nausea, vomiting, and abdominal pain."

Economist Dean Baker summed up the current situation in the US in a Friday social media post: "War, diarrhea, measles, and now salmonella, that's pretty damn MAGA!"

"We stand firmly against this report and other efforts by the Trump administration to weaponize the federal government against dissent, which is a patriotic tradition."

President Donald Trump's escalating claims that Cuba and its supporters poses a threat to US security have been denounced as "laughable" and "crazy," but progressive lawmakers are warning that the State Department's report alleging that the country of roughly 10 million people aims to "conquer" the United States and is backing "left-wing terrorism on American soil" represents a genuine attack on Trump's perceived political enemies.

"Trump appears hell-bent on taking America back 70 years to the height of Cold War McCarthyism, when hawkish foreign policy was paired with unsubstantiated accusations of communist subversion and political repression against dissidents at home," said a group of Democrats led by progressive Rep. Ilhan Omar (D-Minn.), chair of the Congressional Progressive Caucus Peace and Security Taskforce. “We condemn this report’s attack on Americans’ constitutional rights to free speech and assembly."

Omar on Thursday was joined by 10 other lawmakers, including Reps. Alexandria Ocasio-Cortez (D-NY), Jim McGovern (D-Mass.), Delia Ramirez (D-Ill.), and Rashida Tlaib (D-Mich.), in speaking out days after the State Department released its report titled “Cuba: The Capital of 21st Century Communism."

The report, said the lawmakers, was a "McCarthyite attack on Americans’ free speech rights."

The 100-page document claims that Cuba's communist government "has waged a sustained campaign of subversion against the United States" and recruited "generations" of activists in the US, listing by name people who have participated in solidarity campaigns in support of Cuban people as the Trump administration has imposed a destructive oil blockade on the island nation.

"Trump appears hell-bent on taking America back 70 years to the height of Cold War McCarthyism."

In January, Trump issued an executive order declaring that Cuba posed an "extraordinary threat" to US national security and threatened countries with tariffs should they provide oil to the Cuban government. The administration had already cut off Cuba's top source of energy by taking control of Venezuela's vast oil reserves. The blockade has left the Cuban healthcare and education systems and other daily public services struggling to operate.

US groups and citizens named in the report as having spoken out against the administration's blockade and its threats of military action against Cuba include commentator Hasan Piker, Amazon Labor Union founder Christian Smalls, the National Lawyers Guild, and campus activist Isra Hirsi—Omar's daughter.

"We denounce this administration’s irresponsible attacks against civil society organizations, activists, journalists, labor leaders, members of Congress, elected officials, and private individuals based on their advocacy for peaceful foreign policy and social justice at home," said Omar and the Democrats who joined her in the statement.

The lawmakers said they would use their "full oversight power as members of Congress and elected officials to stop the persecution of Trump’s perceived political enemies," including those who speak out publicly against the president's policies in Cuba—activity that is protected by the First Amendment.

"We stand firmly against this report and other efforts by the Trump administration to weaponize the federal government against dissent, which is a patriotic tradition," they said.

The report is the administration's latest attack on the free speech rights that are integral to the US Constitution and American history. The White House has pushed to deport foreign students who protested the US-backed Israel war on Gaza, designated anti-fascist organizers as "terrorists," and, nearly a year after issuing a presidential memo demanding a strategy to "disrupt" left-wing networks, recently convened a summit to launch a "global offensive against the transnational threat of Radical Left terrorism."

Meanwhile, said Omar on Thursday, Trump and Secretary of State Marco Rubio—the son of Cuban immigrants and a long-time proponent of regime change on the island—"are intensifying decades of economic war" against the people of Cuba and deliberately depriving "the entire island’s population of adequate food, fuel, and medicine."

Along with ending his attacks on those who oppose his policies, said Omar, "it is past time for Trump to obey the Constitution and end the dangerous, cruel, and illegal naval blockade causing collective punishment against Cuba.”

"Abdul is the best candidate to win Michigan in November because he is the one who has the capacity to build the grassroots movement that is going to power Democrats to victory," Smith said.

With less than two weeks left before Michigan’s Democratic primary, Senate hopeful Dr. Abdul El-Sayed earned support from another US senator on Thursday, with Sen. Tina Smith praising the progressive as "a fighter."

The endorsement comes as El-Sayed's opponent, Rep. Haley Stevens, rakes in massive support from large super PACs but continues to be massively outraised by him among small donors.

Smith (D-Minn.), who is not seeking reelection in 2026, is nevertheless the fourth member of the chamber to endorse El-Sayed, following Sens. Bernie Sanders (I-Vt.), Chris Van Hollen (D-Md.) and Elizabeth Warren (D-Mass.).

"I've been a United States senator for nearly nine years. And in that time, I have seen there are basically two kinds of senators," Smith said in a video posted to social media. "There are the ones who go along to get along, that hoard their power, and do everything they can to pacify big money. And then there are the fighters—the ones that are ready to challenge the status quo and fight a system that too often seems like it's rigged for the rich and the powerful."

El-Sayed, she said, was one of the latter, crediting his support for Medicare for All, his longtime union membership, and his refusal to accept corporate PAC money.

"Abdul is the best candidate to win Michigan in November," Smith said, "because he is the one who has the capacity to build the grassroots movement that is going to power Democrats to victory."

The endorsement comes as new Federal Election Commission filings released Thursday showed El-Sayed's grassroots fundraising advantage. Between July 1-15, he raised over $2.3 million from individual donors compared to about $921,000 for Stevens during the same period.

The divide is even starker among small donors, where El-Sayed leads Stevens by nearly 9-to-1.

Stevens still has the vast funding advantage thanks to the intervention of powerful outside groups. According to OpenSecrets, the United Democracy Project, the political spending arm of the American Israel Public Affairs Committee (AIPAC), has poured nearly $20 million to push her over the line.

Another super PAC, known as A Stronger Michigan, has spent an additional $14 million on ads promoting Stevens. The dark money group that provides nearly all of its funding, Center Forward, has not disclosed its donors and won't be required to do so until after the August 4 primary.

This wave of outside money has helped Stevens remain competitive against El-Sayed. But her struggles to raise money from voters have raised concerns about her ability to perform in the general election against Republican former Rep. Mike Rogers, who would be expected to suck up the AIPAC funding currently going to Stevens.

While Smith may not have the star power of other Democrats who have backed El-Sayed, journalist Zaid Jilani argued that her endorsement “is a big one” and “a sign [Democrats] think Abdul has a good chance of winning.”

"AIPAC is bailing [Stevens] out right now," he wrote. "But I don’t see why they’d spend on her in a general when Mike Rogers is even friendlier to them."

Journalist Ryan Grim asserted that without AIPAC money for a potential Stevens general election campaign, the Democrats could be forced to pull funding from "Ohio, and Iowa, and Alaska, and so on."

"El-Sayed, meanwhile, has a built-in fundraising base, because he has regular people supporting him, not a super PAC that doesn’t care about Michigan or the Democratic Party," said Grim.

Recent polls show El-Sayed with a slightly larger polling lead over Rogers than the one enjoyed by Stevens. Recent polls for next month's Democratic primary, however, have been more challenging to parse, with some showing El-Sayed far in front and others showing leads for Stevens.

David Dulio, a political science professor at Oakland University, described the race to OpenSecrets as a “battle for the future of the Democratic Party” between powerful donors and the grassroots.

"The story right now… is that Stevens is dominating with outside funding,” Dulio said. “El-Sayed has momentum, and Stevens has money.”

"Congress should not respond to an escalating occupational hazard by permanently removing the Department of Labor’s authority to address it."

A Republican-controlled House committee passed legislation earlier this week that would prevent the US Labor Department from enacting federal standards to protect workers from extreme heat, a move that came amid sweltering heat across the country.

The Heat Workforce Standards Act, led by Rep. Mark Messmer (R-Ind.), passed the House Education and Workforce Committee on Tuesday in a 18-15 vote along party lines. If enacted, the legislation would bar the Occupational Safety and Health Administration (OSHA) from implementing nationwide heat protections for workers—including those proposed by the Biden administration in 2024.

The Biden Labor Department estimated that its proposed rules would protect around 36 million workers. Trump's Labor Department has done nothing to move forward with the Biden-era proposal.

The AFL-CIO, the largest labor federation in the US, has condemned the GOP bill, noting that "extreme heat is one of the deadliest workplace hazards in America."

"House lawmakers are considering legislation that would block OSHA from issuing or enforcing a federal heat safety standard," the labor group said earlier this week. "That's the wrong direction when workers' lives are on the line."

Ahead of Tuesday's vote, a coalition of labor unions and advocacy groups wrote in a letter to members of Congress that the Republican legislation "would permanently remove the federal government’s authority to address a workplace hazard that is already resulting in worker fatalities."

"The Bureau of Labor Statistics recorded 55 worker deaths from heat exposure in 2023, a number that safety researchers widely consider to be an undercount due to frequent misclassification or underreporting of heat-related illnesses and fatalities," the coalition wrote. "More broadly, heat-related deaths in the United States have more than doubled since 1999, and extreme heat now claims more lives each year than any other weather-related hazard."

"Workers have no control over extreme heat, and many are unable to refuse hazardous assignments without jeopardizing their livelihoods," the groups added. "Congress should not respond to an escalating occupational hazard by permanently removing the Department of Labor’s authority to address it."

The Groundwork Collaborative, Workshop, and Harvard Law School’s Center for Labor and a Just Economy estimated in a report published earlier this year that basic, federal workplace heat protections could save up to 1,500 lives annually. The report observed that major industry groups, including the US Chamber of Commerce, have mobilized against proposed national heat protections.

"Companies like Amazon and the United Parcel Service (UPS) that employ hundreds of thousands of workers subjected to extreme workplace temperatures make public statements about their commitments to worker safety while actively lobbying to weaken or block heat regulations," the report noted. "As extreme heat intensifies, the cost of inaction will be measured in lives lost. The question facing policymakers is no longer whether effective protections exist, but whether they have the political will to stand up to those unscrupulous employers lobbying hard to block them."