SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

Fossil fuel companies risk wasting up to $2.2 trillion in the next decade, threatening substantially lower investor returns, by pursuing projects that could be uneconomic in the face of a perfect storm of factors including international action to limit climate change to 2@C and rapid advances in clean technologies, think tank the Carbon Tracker Initiative warns today.

No new coal mines will be needed, oil demand will peak around 2020, and growth in gas will disappoint industry expectations, it finds in a new report highlighting the danger zone between industry business-as-usual strategies and action that would be needed to meet the UN commitment to limit climate change to 2@C.

The $2 trillion stranded assets danger zone: How fossil fuel firms risk destroying investor returns, maps out coal, oil and gas supply that makes neither financial nor climate sense in a 2@C world and how this affects both listed and public companies. The report warns: "If the industry misreads future demand by underestimating technology and policy advances, this can lead to an excess of supply and create stranded assets. This is where shareholders should be concerned - if companies are committing to future production which may never generate the returns expected."

James Leaton, head of research and co-author of the report, said: "Too few energy companies recognise that they will need to reduce supply of their carbon-intensive products to avoid pushing us beyond the internationally recognised carbon budget. Clean technology and climate policy are already reducing fossil fuel demand - misreading these trends will destroy shareholder value. Companies need to apply 2@C stress tests to their business models now."

The US has the greatest financial exposure with $412 billion of unneeded fossil fuel projects to 2025 at risk of becoming stranded assets, followed by Canada ($220bln), China ($179bln), Russia ($147bln) and Australia ($103bln).

The companies that represent the biggest risk in a demand misread to the climate and shareholders alike in the next decade are a mix of state and listed companies, including oil majors Royal Dutch Shell, Pemex, Exxon Mobil, and coal miners Peabody, Coal India, and Glencore. Around 20-25% of oil and gas majors' potential investment is on projects that will not be needed in a 2@C scenario, and cancelling them would mean going ex-growth.

The report looks at production to 2035 and capital investment to 2025. It warns that energy companies must avoid projects that would generate 156 billion tons of carbon dioxide (156Gt CO2), in order to be consistent with the carbon budget in the International Energy Agency's 450 demand scenario, which sets out an energy pathway with a 50% chance of meeting the UN 20C climate change target.

Mark Fulton, advisor to Carbon Tracker, former head of research at Deutsche Bank Climate Change Advisors, and co-author of the report, said: "Our work shows thermal coal has the most significant overhang of unneeded supply in terms of carbon of all fossil fuels on any scenario. No new mines are needed globally in a 2@C world."

Carbon Tracker warned last month that big energy companies are ignoring rapid advances in clean technologies which threaten to undermine their business models, such as renewables, battery storage and electric cars, in a report[1] challenging nine business as usual assumptions made by the industry to argue that coal, oil and gas will all continue to grow in the next decades.

Anthony Hobley, CEO of Carbon Tracker, said: "Business history is littered with examples of incumbents[2] who fail to see the transition coming. Fossil fuel incumbents seem intent on wasting capital trying to hold onto growth by doing what they have always done rather than embracing the energy transition and preserving value by adopting an ex-growth strategy. Our report offers these companies both a warning and a strategy for avoiding significant value destruction."

COAL - In a 2@C world, demand can be met from existing mines and no new mines will be needed. "It is the end of the road for expansion of the coal sector," the new report states. Over the next decade, capital expenditure of $177 billion on new projects and $42 billion on existing ones is unneeded.

China, the US, Australia, India and Indonesia have the greatest exposure, accounting for over 90% of unneeded investment. Export markets are in structural decline as China seeks to peak its coal demand and India aims to become more self-sufficient in energy, threatening big exporters like Australia and Indonesia. In the US half of all potential projects from Peabody, Murray and Foresight will be unneeded.

OIL - "In the 450 scenario oil demand peaks around 2020. This means the oil sector does not need to continue to grow, which is inconsistent with the narrative of many companies," the report states. Spending of $1.3 trillion on new projects and $124 billion on existing projects is unneeded. Overall 43% of investment in new projects and 33% of new supply should be avoided to align with a 2@C scenario, avoiding 28Gt of CO2.

The countries with the greatest financial exposure are the US, Canada, Russia, Mexico and Kazakhstan. The biggest risk is from shale oil in the US, oil sands in Canada and conventional oil in Russia. All three, with Norway, are exposed to Arctic oil. Deep water projects in the US and Mexico and Venezuela's heavy oil are also in the danger zone. However, OPEC conventional production faces little risk due to its low cost.

GAS - In a 2C world gas growth will be "at a lower level than expected under a business as usual scenario", the report finds. Capital expenditure of $459 billion on new projects and $73 billion on existing projects is surplus to requirements. Overall 41% of investment in new projects and 25% of new supply, accounting for 9 Gt of CO2, is unneeded.

The US, Australia, Indonesia, Canada and Malaysia have the greatest exposure, accounting for three-quarters of investment risk. Within the markets we analyse (North America, Europe, and the LNG export market), two-thirds of new coal bed methane and Arctic projects are in the danger zone; half of the supply in new LNG projects is unneeded and very little new capacity will be needed in the US and Canada in a 2@C scenario.

CARBON CAPTURE AND STORAGE - Carbon Tracker's analysis assumes 24Gt of CO2 will be captured by CCS by 2035 in line with the IEA 450 scenario, but it warns that this would require CCS to grow to a level 150 times where it is today. Delays in CCS could significantly increase the reductions in coal that will be needed and the IEA has estimated that a 10-year delay in large-scale CCS deployment from 2020 to 2030 could cost fossil fuel producers $1.35 trillion in lost revenues.

From Wednesday 25th November the report will be available for download at https://www.carbontracker.org/report/stranded-assets-danger-zone/

The Carbon Tracker Initiative is a not-for-profit financial think tank that seeks to promote a climate-secure global energy market by aligning capital markets with climate reality. Our research to date on unburnable carbon and stranded assets has begun a new debate on how to align the financial system with the energy transition to a low carbon future. www.carbontracker.org

"People are trying to divide our society and set some people against others," said a spokesperson for the Christopher Street Day festival. "At the CSD in Berlin, we will not allow this."

One person was killed and at least 29 others injured on Saturday when a van plowed into a crowd near Berlin's annual LGBTQ+ Pride festival, with the attacker—who wounded some of his victims with a machete after crashing—later shot dead by police, who said he was a suspected Islamic extremist.

The attack occurred Saturday evening during the Christopher Street Day (CSD) celebration—named after where New York's Stonewall Inn is located—following the main parade near the Tiergarten area near the Brandeburg Gate. In what German authorities have officially designated a terrorist attack, police said a 21-year-old German-Lebanese man, identified as Abdul Ballout, drove his van into a crowd before assaulting people with a machete.

One woman, whose identity has not yet been publicly disclosed, was killed.

On Sunday, police located Ballout in the Berlin suburb of Spandau. Police said Ballout was fatally shot as he ran toward officers with a sharp object.

Berlin prosecutors said Ballout traveled to Syria last year while trying to join the so-called Islamic State militant group. According to The Associated Press, Ballout was arrested in Lebanon and sentenced to three months' imprisonment for incitement. He was arrested again upon returning to Germany, where he received a suspended sentence from a juvenile court for publishing pro-Islamic State messages on Instagram and preparing an act of serious violence threatening the state.

During a Sunday press conference, a CSD spokesperson implored people not to use the attack "for political ends."

"People are trying to divide our society and set some people against others," he said. "At the CSD in Berlin, we will not allow this."

However, far-right leaders in Germany and beyond blamed "Islamism." Tino Chrupalla, co-leader of the Alternative for Germany, said on X that “we will not allow religious extremists to divide our country with violence and intolerance."

Numerous X users pushed back, with one saying, "You constantly incite against queer people and are now exploiting the attack for your disgusting incitement!"

Andre Lehmann of LSVD+, Germany's largest LGBTQ+ advocacy organization, said, “We are simply stunned by what happened," adding that the attack "hits the heart of the queer community."

Berlin Mayor Kai Wegner said on social media that the assault was "an attack on our free and open society."

"After a peaceful and colorful CSD, the assembly for a tolerant and peaceful Berlin was attacked in the most brutal way," he continued. "Berlin is the city of freedom—and our freedom has been attacked in the most horrific way today."

German Chancellor Friedrich Merz told reporters at a Saturday press conference outside the Marienkirche in central Berlin: "What a heinous act in Berlin. This attack on peaceful Christopher Street Day celebrants is an assault on our open, tolerant society. We will investigate it with utmost severity."

"Our thoughts are with the victims of this Islamist terrorist attack," Merz continued. "I wish those who sustained injuries a swift recovery."

The Christian Democratic Union chancellor thanked first responders for "intervening as quickly as possible, which could well have prevented an even worse outcome last night."

"Let us not be intimidated by these crimes," Merz added. "They want to divide our society, they want to take the most important thing that we have: namely, our open society, our liberal society."

The climate action group Fridays for Future Germany posted on X: "We are devastated. Yesterday's attack on the Berlin CSD was an attack on all of us. Our thoughts are with the victims, their loved ones, and all those who had to witness this attack. Now is the time for solidarity with the queer community."

LGBTQ+ advocates and their allies around the world condemned the attack and offered their condolences and solidarity.

In the Slovakian capital Bratislava, the gay bar Tepláreň—where a far-right extremist teen shot and killed two people in 2022—posted on Instagram: "We are thinking of you, friends in Berlin. It is with great sadness that we are watching the terrible news. We express our deepest condolences to the victims, their loved ones, and everyone who has been affected by these events."

Extremism "is growing dangerously worldwide," the bar added. "People blinded by hate and lies threaten our communities, threatening our chance to coexist in peace."

"Prides are meant to be a place where all can feel safe, welcome, and seen," the rapid response team at the US group Human Rights Campaign said on social media. "We are sending our love to the victims, their families, and the entire city of Berlin today."

People gathered for vigils across Germany and around Europe and the world Sunday to mourn and condemn the attack. In Berlin, the Brandenburg Gate was illuminated in rainbow colors, with the message "Berlin, City of Freedom" projected beneath its Quadriga sculpture, as people took part in a candlelit vigil.

“There was so much joy here yesterday,” Luise V., who attended both CSD and a vigil near the site of the attack, told Berliner Zeitung. “Today I had to face it and come here, also to process what happened."

"Don't mistake the beginning for the end," said the Cockroach Janta Party, which vowed to press for further reforms and government accountability.

India's Cockroach Janta Party ended its five-week multi-city protest on Saturday after the youth-led movement's key demand—the resignation of Education Minister Dharmendra Pradhan—was met.

“We have done it,” CJP spokesperson Saurav Das told a jubilant crowd at New Delhi's Jantar Mantar. "Pradhan has sent in his resignation, which means that our first demand has been met."

Das said that the protesters' second main demand, the withdrawal of criminal investigations targeting CJP members, was also met. However, members and supporters of the movement noted that some cockroach protesters remain in detention and vowed to continue pressing for their release.

Pradhan's resignation is the first such surrender to public pressure during the 12-year tenure of Hindu nationalist Indian Prime Minister Narendra Modi.

“Considering the situation at Jantar Mantar and elsewhere in the country, and so that anti-national forces do not take advantage of the circumstances, national unity is maintained, no student’s future gets entangled in legal complications, and our children can focus on their studies and building their careers, I have submitted my resignation," Pradhan said in a statement.

Pradhan's tenure was marred by repeated leaks of National Eligibility Entrance Test (NEET) papers in a scandal that has upended the lives of millions of students by forcing them to retake the grueling exams and delaying their university admissions. CJP organizers said more than 20 students have killed themselves over the matter.

The now-ex education minister had dismissed the protesters as “the B-team of terrorists.”

On Sunday, Modi said he would authorize the creation of an examination reform task force headed by Nandan Nilekani, co-founder of Indian tech giant Infosys.

“The government of India is continuously taking various measures for the future of students," the Bharatiya Janata Party prime minister said in a video posted on social media. "However, we must look to the future. Our examination system needs to be reliable and transparent, and it must make maximum use of technology."

The protest movement began in May after Chief Justice of India Surya Kant reportedly compared unemployed young people to “cockroaches.” The protesters, led by political strategist Abhijeet Dipke, satirically reclaimed the slur as the symbol of a movement that has grown into a broader challenge to Modi’s increasingly authoritarian rule, which has seen mounting repression of protest and dissent, including restrictions on journalists and activists, and the use of "lawfare" to target critics.

Last week, tens of thousands of youth-led protesters marched in New Delhi, where they were met and attacked by police batons and tear gas. Indian media reported thousands of injuries.

The mood was markedly different following Pradhan's resignation.

"Cockroaches won!" many CJP members and supporters said.

Others added, "Democracy Won!"

"This is democracy," said the CJP.

"Now that the cockroaches have won their first battle, may they win many more," Tavleen Singh, a columnist for The Indian Express, wrote on X. "May they become a real political party in the near future."

Sonam Wangchuk, an environmentalist whose hunger strike was a focal point of the cockroach protests, was released Sunday from a Gurugram hospital, where he had been recovering from his 26-day fast since Thursday.

Emboldened by the CJP victory, members of the Communist Party of India (CPI)-affiliated All-India Youth Federation and All-India Students' Federation marched on the Chennai residence of Tamil Nadu Gov. Rajendra Vishwanath Arlekar demanding the abolition of the NEET. According to Indian media reports, police detained more than 200 of the demonstrators.

"The struggle will intensify," said CPI.

"Don't mistake the beginning for the end," echoed CJP.

Asked Sunday what's next for the cockroach movement, Dipke told an ANI reporter that "we will soon share the next strategy."

"This has just ended yesterday," he added, "please give us a little time."

Protesters rallied against the Trump administration's deadly anti-immigrant crackdown in the wake of the killings of Lorenzo Salgado Araujo, Johan Sebastían Guerrero, Juan Jairo Coronilla Durán, and others.

Protesters gathered in cities and towns across the United States on Saturday at vigils to remember and demand justice for people killed by US Immigration and Customs Enforcement and other federal agents during President Donald Trump's deadly crackdown on immigrants and their defenders.

The July 25 Day of Action was organized by advocacy groups and volunteers across the country, with support from the Disappeared in America project hosted by Public Citizen, the National Day Laborer Organizing Network, The Workers Circle, Detention Watch Network, and the League of United Latin American Citizens (LULAC).

The vigils brought together clergy, activists, progressive advocates, and other concerned and outraged citizens, who remembered Lorenzo Salgado Araujo, Johan Sebastían Guerrero, Juan Jairo Coronilla Durán, and the dozens of people who have died in ICE custody during Trump's second term.

“Lorenzo Salgado Araujo was a husband, a father of three, and a small business owner who built his American dream with his own hands. Johan Sebastían Guerrero was killed in front of his partner and his toddler,” LULAC CEO Juan Proaño said in a statement. “ICE has now taken the lives of immigrants and US citizens alike, and if they can kill Lorenzo and Johan, they can kill anyone."

In the Twin Cities area of Minnesota, vigils honored the immigrants killed by ICE, as well as Renee Good and Alex Pretti, two US citizens fatally shot by Department of Homeland Security agents in January.

“They weren’t doing anything wrong. They were trying to help their neighbors, simple as that," said Lisa Erbes of Indivisible Twin Cities. "They were legally observing what ICE was doing, and they were both killed for it, and that could have happened to me. It could have happened to probably every single person who is here right now. Any of us could have been Renee or Alex."

This weekend marked six months since Pretti, a 37-year-old nurse, was shot by US Customs and Border Protection agents in Minneapolis.

"No one has been held accountable, no apologies, not a single phone call from any governmental official, hospital personnel, or the police," Susan Pretti, Alex's mother, wrote Saturday on social media.

“Six months of pain, a roller-coaster of trauma over and over," she added. "I wonder how to move forward. Will I ever get over this loss and this pain? Will I ever be able to enjoy life again?”

In Chicago—where Trump deployed hundreds of federal enforcers during Operation Midway Blitz—at least hundreds of people gathered in Grant Park and marched down Michigan Avenue.

“There’s collective trauma that impacted our communities that no one can understand unless you were here and felt the helicopters and saw the unpredictability of neighbors getting snatched off the streets,” 46-year-old demonstrator Melody Rose of Rogers Park told the Chicago Tribune. “All of us, especially those who have been directly impacted and seen what that’s like, have to keep showing up and spreading the word because this isn’t over and it could be us any day."

United Church of Rogers Park pastor Rev. Hannah Kardon told Chicago rallygoers: “Remember the dead and demand the kind of world where we never would have lost them in the first place. We will not forget them, and we will live differently because of them.”

Los Angeles-area demonstrations included a march by hundreds of people in downtown LA, where protesters carried cardboard coffins representing lives lost to Trump's crackdown.

"Our communities will never be the same," protester Joseph Morales told KABC. "Even though we're strong and we hold each other together, our communities are not the same, and we grieve that loss."

STOP KILLING US!

Justice for All

Disappeared in America Coalition Vigil for ICE slain immigrant in America!

Los Angeles Coffin Protest #StopKillingUs #USDemocracy #JusticeForAll #SomosLorenzo #DondeEstan #USDemocracy pic.twitter.com/KnqeTBRTHh

— Ruben Garcia (@goRubenRuben) July 26, 2026

In Pasadena, around 50 people turned out to protest the ICE killings.

“We were originally told, ‘Oh they’re going to go after the criminals, the people who are the worst of the worst.’ That’s a lie; that is not what’s happening," 61-year-old organizer Andra Clarke—who held a sign reading "Neighbors Say ICE Out"—told the Los Angeles Times.

“They’re targeting communities, they’re targeting people of color. It’s fascism," she added. "Anybody who cares about humanity should care about what’s happening.”

Around 100 protesters rallied outside ICE's downtown Atlanta field office, including Gail Maclin, who told Atlanta News First that her Senegalese husband is among the 675,000 people forcibly deported during Trump's second term.

“I lost my housing. I’ve lost my car. I’ve lost all my worldly possessions," she said. "I still have Amari, but Amari’s not here—he’s in Senegal."

Among the approximately 150 people who attended a vigil in the Silicon Valley city of Mountain View—headquarters of Google, where workers have protested the company's complicity in Trump's deadly crackdown—were members of the Raging Grannies, a longtime activist group known for their protest songs.

"People are being targeted here, and are afraid," Raging Granny Ruth Robertson told CBS News Bay Area. "They're afraid to go out of their houses, they're afraid to go to work."

A crowd of demonstrators gathered for a roadside vigil along Route 29 in Centreville, Virginia, a suburb of Washington, DC.

Rev. David Miller of the Unitarian Universalist Congregation of Fairfax told protesters: “I think that there is a moral obligation for us to speak up about our values. These values are not being represented well by this administration and certainly not by the way that ICE has been acting in our communities.”

Julio Hernandez, the director of the Congregation Action Network, told Centreville vigilgoers that “we're here to tell the story of our community being terrorized and torn apart, families being separated, children living in fear."

“We're here to ask the community to be aware of what's happening and also asking ICE to get out of our communities,” he added.

A majority of the three-judge appellate panel called part of the president's March executive order "an unprecedented federal incursion into states’ exclusive power to determine voter eligibility."

A federal appellate panel on Saturday rejected the Trump administration's request to lift a lower court's injunction blocking the US Postal Service from enforcing President Donald Trump's March executive order targeting mail-in ballots as part of Republicans' broader attack on voting rights.

A three-judge panel of the Boston-based 1st US Circuit Court of Appeals ruled 2-1 against a motion by the administration seeking a pause on US District Judge Indira Talwani's June order blocking major portions of Trump's directive, which is aimed at restricting postal voting, including by directing the USPS to ensure that mailed ballots have unique barcodes and envelope logos.

"Under the Constitution, state and local officials are responsible for administering federal elections," Judges Gustavo Gelpí and Julie Rikelman—both appointed by former President Joe Biden—wrote in a joint opinion. "In the spring of 2026, President Trump issued an executive order with nationwide effects on how state and local officials can administer federal elections, including the upcoming primary and general elections in September and November. In particular, the executive order directed substantial involvement by the United States Postal Service in deciding which ballots sent to and from voters would be delivered."

Judge Joshua Dunlap, a Trump appointee, partially dissented from the majority. The decision applies to the 23 states and District of Columbia that filed a lawsuit challenging the executive order.

The ruling also focuses on the executive order’s threats to criminally punish any state or local officials who refuse to comply. Under the order, the USPS would only send mail ballots to states that send their unredacted voter files to [the US Department of Homeland Security], which would approve voter eligibility via a national voter registration database. This is an unprecedented federal incursion into states’ exclusive power to determine voter eligibility as deemed by the US Constitution.

Saturday's ruling comes just over three weeks after Judge Emmet Sullivan of the US District Court for the District of Columbia halted the USPS' implementation of Trump's executive order. Sullivan granted a request by the NAACP to enforce a 2021 settlement agreement requiring the USPS to protect mail-in voting and prioritize delivery of mail related to elections through 2028.

That decision followed a June ruling by Chief US District Judge Denise Casper in Massachusetts that blocked portions of the president's order requiring people to show proof of citizenship when registering to vote.

Trump's March order is part of a broader attack on voting rights that includes pushing an updated version of Republicans' so-called SAVE America Act, which would mandate proof of citizenship and strict photo ID requirements to register to vote in federal elections. The legislation, which was passed by the House of Representatives in February, is stalled in the narrowly split Senate, where it lacks the support of 60 lawmakers needed to avoid a Democrat filibuster.

"This is a terror campaign with the mission of traumatizing our neighbors," one pastor said of the Trump administration's deadly anti-immigrant crackdown. "We don't need terror. We need peace."

Faith leaders are calling on US Immigration and Customs Enforcement to immediately free a pair of pastors who advocates say were wrongfully detained by ICE agents in Texas on Thursday while traveling to a religious retreat.

Pastor Nepthalí Zozaya Saucedo and his wife, pastor Cinthia Saraí Cardona Otero, were detained by federal immigration enforcers after arriving at McAllen International Airport. According to the couple and their church leaders, the longtime pastors at the Comunidad Cristiana Emanuel Assemblies of God congregation in Edinburg, Texas were on their way to a marriage retreat in North Carolina when they were detained and taken to a US Border Patrol processing center in McAllen.

At a Friday press conference hosted by leaders from the Assemblies of God and the Latino Christian National Network, LCN board member Sandy Ovalle said that the couple has valid R-1 religious worker visas.

“We are calling for their immediate release, the protection of their due process rights, and an urgent oversight into ICE’s conduct,” Ovalle said. “No one should be pressured to give up their rights under the threat of losing their children.”

A Department of Homeland Security spokesperson told Religion News Service that the pastors are "illegal aliens" who overstayed their visas.

Addressing the conference by phone from the detention center, Nepthalí said that the couple was threatened with separation from their US citizen children if they did not sign papers authorizing their "voluntary" deportation.

“They spoke with us about separation—to be separated from our children and even as married people,” he said, according to Religion News Service. “They spoke about how much time that we could end up spending here.”

Speaking during the press conference, Comunidad Cristiana Emanuel senior pastor Sarai Martinez Luna said, “I think it’s very cruel that somebody that had no status for deportation be pressured to sign a voluntary deportation based on the separation of their children."

Friday's news conference followed a Wednesday press briefing by faith leaders at the Texas Capitol in Austin to condemn the killings of Johan Sebastián Durán Guerrero in Maine, Juan Jairo Coronilla Durán in Florida, and Lorenzo Salgado Araujo in Houston.

"This is not of God. This is no peace that we want a part of because let's be honest, this isn't a peacekeeping initiative. This is a terror campaign with the mission of traumatizing our neighbors until they self-deport," said Dan De Leon, senior pastor at Friends Congregational Church in College Station. "We don't need terror. We need peace."

Leaders from a range of faith communities across Texas came together to send a unified anti-ICE message to Gov. Greg Abbott (R) and state lawmakers, saying ICE operations go against their core religious values. pic.twitter.com/DbPf1LPZTd

— NowThis Impact (@nowthisimpact) July 24, 2026

Elyse Rosenberg of the National Council of Jewish Women and Temple Beth Shalom in Austin said during the press conference that “throughout our history, we have repeatedly seen first-hand the consequences of governments exercising unchecked power on vulnerable populations."

Friday's event also preceded nationwide vigils in more than 300 communities across the nation on Saturday to demand justice for the dozens of people who have been killed by federal enforcers or died in ICE custody during President Donald Trump's second term.

“We refuse to grieve quietly. We refuse to accept this terror and violence as inevitable”, Crystal Cron, executive director of Presente! Maine, said ahead of the vigils. “Johan Sebastián should still be here with his wife and daughter—and instead, his name joins a growing list of people killed by an institution that treats our communities as disposable."

"This is bigger than one shooting," Cron added. "We will not stop fighting until there is justice for the Durán Guerrero family and a total dismantling of this lawless, criminal agency that took him from them.”

“We are not from the left. We are not from the right. We are from the bottom. And we are rising," the longtime labor advocate and lumberjack said.

Maine Democrats on Saturday overwhelmingly nominated Troy Jackson, a former state Senate president and logger by trade, as their party's nominee to challenge longtime Republican incumbent Susan Collins in November's high-stakes US Senate election.

"Well, thank you, Maine," Jackson, 58, said after securing the votes of 566 of 571 delegates during Saturday's special Democratic convention at Cross Insurance Center in Bangor. "Today we turn the page, today this becomes a general election campaign, and today we win the work of defeating Susan Collins in November."

“For nearly 30 years, Collins has told Maine that she is 'concerned',” Jackson said, referring to the 73-year-old incumbent's go-to word when President Donald Trump and Republicans attack rights and justice. “She was concerned while she rubber-stamped Trump’s Medicaid cuts and gutted our healthcare."

"She’s concerned when she cut taxes for corporations and the wealthy," he continued. "Concerned when she confirmed justices who overturned Roe v. Wade. And really tragically, she was concerned when she gave [US Immigration and Customs Enforcement] billions to terrorize our neighbors and murder people in the streets with no accountability.”

“But concern does not lower the costs of groceries or gas," Jackson said. "Concern does not keep our monitoring wards of rural hospitals like down in Lincoln County open. Concern does not restore all the rights that she’s taken away. Maine does not need another six years of concern. We need someone with courage. We need a fighter, and we need a senator who remembers exactly who sent them to Washington.”

"So if you've ever been ignored, underestimated, pushed around, or told that you have to wait your turn while the rich cut the line, I'm asking you to stand with us in this campaign," he continued. "If you believe in your heart that healthcare is a right, stand with us. And if you believe that workers deserve power, stand with us. And if you believe our freedoms are worth defending, stand with us."

"And if you believe that Maine deserves a senator who will fight like hell for working-class people, well, stand with us," Jackson added. "We have a party to unite, we have a movement to build, and we have a senator to defeat."

- YouTube

Jackson's improbably rapid rise followed former Democratic nominee Graham Platner's withdrawal from the race earlier this month amid allegations of sexual assault and abusive behavior. Supporters of Platner's progressive platform warned at the time that they would not back a replacement candidate who did not share the same pro-worker, anti-war agenda.

While Collins spokeswoman Blake Kernen called Jackson a "low-energy version" of Platner, Maine Democrats decided the fifth-generation lumberjack fit the bill.

“The working class has been left behind and forgotten about,” Shelly Mountain, a former Aroostook County Democratic Committee chairwoman and Jackson delegate at the convention, told NBC News. “He is definitely working class and always—has always—been a champion for the working class.”

Progressive politicians, advocacy groups, and labor organizations cheered Jackson's nomination, with Sen. Elizabeth Warren (D-Mass.) saying that "he's ready to fight for working people and flip this seat."

International Association of Machinists and Aerospace Workers (IAM) president Brian Bryant said Saturday that “Troy Jackson knows firsthand what it means to work hard for a living and fight for a better future for working families."

“Throughout his career, he has stood shoulder-to-shoulder with union members and working people, never backing down from a challenge when workers’ rights were on the line," he added. "He represents the strength of a people-powered movement focused on fairness, opportunity, and economic justice. Troy has our full support as he heads to the general election.”

California's attorney general called the development "great news for audiences, movie theaters, and the many people who write, build, and create the art, news, and entertainment so many of us enjoy."

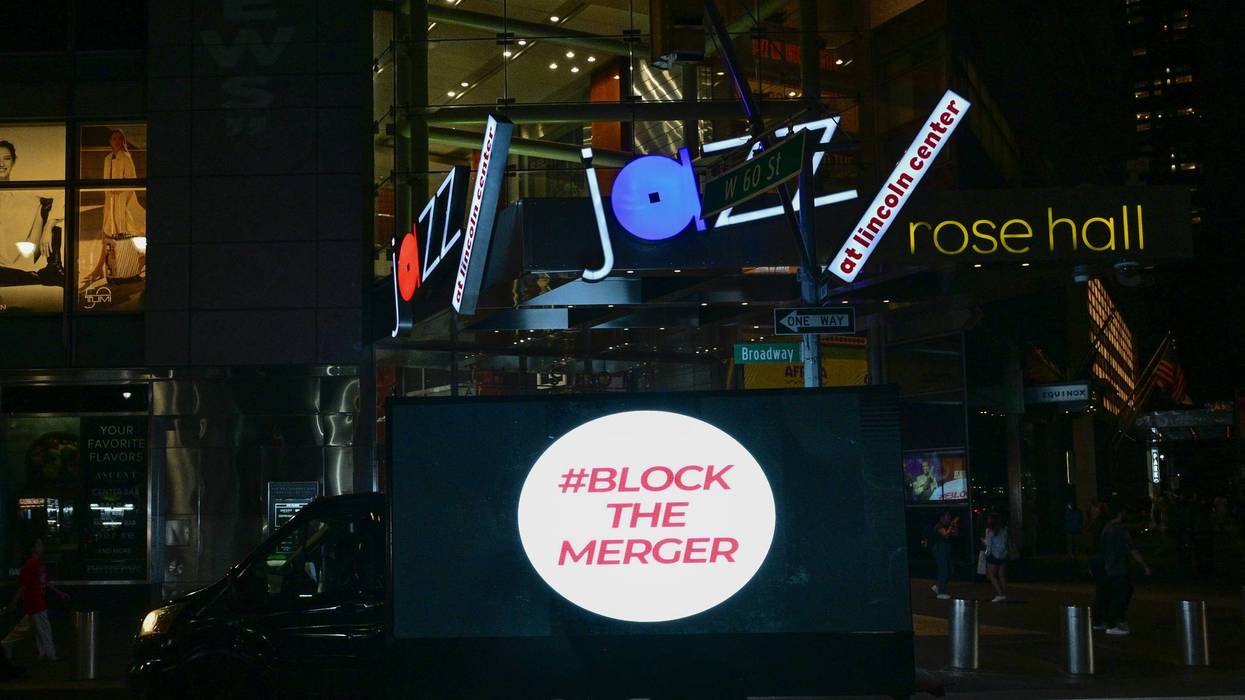

Paramount Skydance on Friday officially delayed its attempted acquisition of Warner Bros. Discovery after a federal judge in the Northern District of California temporarily blocked the $111 billion deal at the request of a dozen Democratic attorneys general.

US District Judge Araceli Martínez-Olguín granted the temporary restraining order on Monday after finding that the plaintiffs—led by California Attorney General Rob Bonta—provided "compelling evidence that the combined firm resulting from the transaction will possess substantial market share in the wide-release theatrical distribution market." She extended the order on Thursday.

The companies have now agreed not to close the deal—also the target of a Writers Guild of America lawsuit—until five days after a trial is held or June 1, 2027, whichever is sooner. While the attorneys general and their supporters framed the development as a victory for their side, a Paramount spokesperson similarly said that "today's agreement is a significant win because the result is exactly what we have sought from the outset: a direct path to a trial based on the evidence."

"This is the fastest and clearest way to prove that this transaction is good for competition, good for consumers, and good for creators, a conclusion dozens of competition authorities around the world have already reached," the spokesperson continued. "Plaintiffs' market definitions bear no relationship to the realities of today's marketplace and cannot withstand scrutiny. We look forward to proving our case at trial."

Meanwhile, Bonta said in a statement that "our argument against this illegal merger is straightforward: When too few corporations have too much power in markets central to American life, it makes things more expensive, and it makes things worse."

"Today's agreement is great news for audiences, movie theaters, and the many people who write, build, and create the art, news, and entertainment so many of us enjoy," he emphasized. "We are eager to continue to make our case in court and celebrate another tremendous win in our effort to ensure this unlawful merger never sees the light of day."

Joining Bonta in battle are the attorneys general of Arizona, Colorado, Connecticut, Massachusetts, Minnesota, Nevada, New Jersey, New Mexico, New York, Oregon, and Washington. They, too, celebrated on Friday.

"Stopping this merger while our case proceeds is a critical victory in our efforts to uphold the law and protect the film and television industries," New York's Letitia James stressed on social media. In a video, New Jersey's Jennifer Davenport also called the companies' decision "a huge win for consumers" and pledged to "continue to fight to block this merger for good."

Responding to one of Davenport's social media posts, actor and activist Mark Ruffalo declared: "Today's news is a repudiation of Paramount's strategy of currying favor with the Trump administration to grease the wheels on this illegal merger—from sham settlement payments to manipulating its own news coverage. Stay strong and #BlockTheMerger."

Some opposition to the deal is rooted in the fact that it would give Paramount CEO David Ellison—the son of billionaire Larry Ellison, a major donor to President Donald Trump—control of CNN, as he already faces mounting criticism for his and Bari Weiss' management of CBS News.

"The Ellisons believed their relationship with President Trump would help them push through a disastrous deal that threatened democracy, creative freedom, and independent journalism. We in the #BlocktheMerger campaign helped prove them wrong," said Norm Eisen, co-founder and executive chair of Democracy Defenders Fund, in a statement.

"Paramount's decision keeps two major studios competing instead of handing one company even more power over what Americans watch, what they pay, and where entertainment workers can earn a living," he continued. "The merger would have eliminated one of Hollywood's largest buyers of scripts and productions while placing Paramount+, HBO Max, CBS News, CNN, and dozens of local stations under the management of one company."

"This victory in putting the merger on hold belongs to the people who refused to treat the merger as inevitable," Eisen added. "Artists, journalists, filmmakers, and consumer advocates spoke out despite the risk of retaliation, more than 5,500 people signed our open letter, and Attorneys General Rob Bonta and Letitia James, along with 10 other attorneys general, acted. This collective resistance is turning the tide."

Craig Aaron, co-CEO of the advocacy group Free Press, said that "Paramount tried to tell us this deal was a slam-dunk, but it just shot an airball. Late in the game, Paramount's lawyers grasped what we've said all along: The states have a very solid case that this deal violates US antitrust law. For the broad and growing coalition against this corrupt and dangerous deal, this delay marks a significant victory."

"Instead of fighting against an injunction and possibly losing now, Paramount's lawyers have resigned themselves to waiting for a full antitrust trial in federal court," Aaron added. "Paramount can pretend all it wants that it looks forward to that test, but that’s just more bluster from company mouthpieces trying to spin a major setback. Now this deal will face its day in court, and we are confident the evidence will show this mega-merger should be blocked."

“The federal government cannot build secret dossiers on people because they exercise their First Amendment right to peacefully observe, document, or criticize its actions," said the head of Democracy Forward.

A coalition of privacy and civil liberties advocates filed a federal lawsuit Friday accusing the Trump administration of secretly collecting and keeping personal information about people who monitor US Immigration and Customs Enforcement operations, arguing that the practice violates federal privacy law and threatens constitutionally protected speech and association.

The lawsuit—filed in the US District Court for the District of Columbia—was brought by individuals and advocacy groups represented by Democracy Forward.

The plaintiffs—the Electronic Privacy Information Center (EPIC) and legal observers Nicole Cleland, Jacquelyn Ivey, and Anna Walker—argued that the US Department of Homeland Security (DHS), US Immigration and Customs Enforcement (ICE), and other federal agencies created and maintained databases of people who observed, documented, or protested immigration enforcement activities without providing notification or safeguards, as required under the Privacy Act of 1974.

That law was passed after the exposure of illegal government surveillance, including longtime former Federal Bureau of Investigation Director J. Edgar Hoover's infamous COINTELPRO program, under which the FBI, in addition to conducting unlawful spying, funded and armed murderous far-right militants to terrorize anti-Vietnam War protesters, anti-nuclear weapons activists, civil rights leaders including Martin Luther King, Jr., and other leftists.

“The federal government cannot build secret dossiers on people because they exercise their First Amendment right to peacefully observe, document, or criticize its actions," Democracy Forward president and CEO Skye Perryman said in a statement announcing the lawsuit. "That is exactly the kind of government surveillance Congress sought to prevent when it enacted the Privacy Act after some of the darkest chapters in our nation’s history."

The lawsuit accuses the Trump administration of collecting the names, photographs, vehicle information and license plate numbers, social media accounts, and other identifying information about legal observers, volunteers, journalists, clergy, and community members engaged in First Amendment-protected activities during the government's deadly anti-immigrant crackdown.

"When the Department of Homeland Security dramatically ratcheted up its immigration enforcement, people across the country—of all ages and backgrounds—did what anyone is supposed to do when they disagree with government action: They exercised their First Amendment rights," the suit states. "They peacefully protested. And, as matters here, they observed and recorded how law enforcement agents acted in public."

DHS is using facial recognition technology, body cameras, license plates, mobile devices, and other surveillance tools to identify, track, and punish people who legally observe immigration enforcement in public. This is a clear violation of the Privacy Act. We’ll see them in court.

[image or embed]

— Democracy Forward (@democracyforward.org) July 24, 2026 at 10:36 AM

"In response, DHS decided to record the Americans who were peacefully observing its agents, adopting a secret Protester Surveillance Policy enabling its agents to first collect records on Americans engaging in First Amendment exercise and then maintain them in DHS systems, where they can be used to retaliate against those Americans," the complaint continues.

"Beginning sometime in 2025, DHS deployed a dragnet of drones, bodycams, face-scanning apps, license plate scanners, and camera phones to, as one memo instructed, 'capture all images, license plates, identifications, and general information on hotels, agitators, protestors, etc., so we can capture it all in one consolidated form,'" the document notes.

"DHS agents have not been shy about gathering this information or its purpose," the plaintiffs contended. "In Maine, DHS agents told multiple observers that they were being added to a database of 'domestic terrorists.' In Chicago, agents routinely used facial irecognition scans on members of the public."

"In Minneapolis, observers simply watching agents on public streets have been led by those agents to their own houses, despite never having interacted with an agent—a practice so common that it has been named 'being driven home by ICE,'" the suit says. "And across the country, DHS agents have approached observers and addressed them by their full names, even though those observers never identified themselves to the agents or showed them any form of identification."

"As a result of its Protester Surveillance Policy, DHS has recorded and retaliated against each individual plaintiff," the filing alleges. "It’s bad enough that DHS publicly collected information on Americans engaged in lawful First Amendment exercise. But worse, DHS also decided to maintain the information in one or more of its systems, enabling it to later retaliate against observers and protestors—including by canceling Trusted Traveler status," which includes Transportation Security Administration Pre-Check and Global Entry.

The plaintiffs are asking the court to declare the DHS surveillance policy unlawful, end it, and ban the agency from continuing to collect and keep records of individuals’ protected First Amendment activities.

“Now more than ever, those of us who have the privilege to speak out have a responsibility to defend the rights of everyone in our communities,” Walker said in a statement. “When people are punished for exercising their First Amendment rights, we begin losing the democratic principles that protect all of us. Every American should be alarmed by retaliatory action against one’s free speech."

Cleland said: “I believe government accountability starts with transparency. People should be free to peacefully observe and document what their government does in public without worrying they’ll be tracked or retaliated against. This case is about protecting that right for everyone.”

EPIC deputy director John Davisson warned, “When our government compiles secret dossiers on everyday people for exercising their constitutional rights, it sends a chilling message: If you speak up, watch your back."

"If every protest, every recording, every act of dissent opens us up to surveillance and retribution, privacy and free speech are at risk of collapse," he added. "But the laws of this nation don’t permit that, and we won’t either.”

"It is despicable that the administration is taking away funding from states that did not vote for Trump," said US Sen. Dick Durbin.

President Donald Trump's administration has admitted in court that it chose to cancel certain grants for clean energy projects because they were set to benefit Democratic-voting states.

The New York Times reported on Friday that attorneys representing the US Department of Energy (DOE) acknowledged in court documents filed earlier this month that decisions about canceling grants were based "solely on the political identity of the grant recipient’s state, i.e., whether the recipient’s location and/or place of performance was in a Blue State or a non-Blue State."

The Times described this as a "stunning admission" that "offered an unvarnished glimpse into the way President Trump has weaponized the provision of federal education, energy, health, housing, and infrastructure aid in his second term."

According to the Times, the DOE last year recommended canceling more than 600 grants awarded for energy projects under former President Joe Biden's administration.

However, the White House Office of Management and Budget only made 284 of the recommended cuts while leaving the rest of the grants in place.

After a group of California researchers challenged the terminated grants in a lawsuit, the DOE acknowledged that "with one exception, the 284 terminated grants had a recipient location and/or at least one place of performance in a state that awarded its electoral votes to Kamala Harris in the 2024 election and has two Democratic-caucusing senators."

The DOE also admitted that there was no "programmatic, statutory, cost-reduction, or performance-based factor" to justify the cuts.

In a social media post, New York Times reporter Tony Romm noted that the DOE made these admissions "as part of a process meant to avoid discovery" and "perhaps spare it from sharing more damaging records" in its possession.

The Times report drew a sharp reaction from Trump administration critics.

"This is corruption," said Rep. Laura Friedman (D-Calif.). "It’s how this administration has acted since day one: punishing states, businesses, and ordinary Americans who push back on Trump. It’s a major betrayal of our nation that will lead to higher energy prices and should be condemned by people of all political parties. It’s un-American and despicable."

Sen. Andy Kim (D-NJ) accused the administration of "the weaponization of government" with its selective grant cancellations.

"This administration shows us time and time again they only care about one person," Kim added, "and that person only cares about himself."

Sen. Dick Durbin (D-Ill.) argued that the filings prove "what we have long known, that their grant cancellations were not based on 'waste' or sound policy but vindictiveness."

"It is despicable," Durbin emphasized, "that the administration is taking away funding from states that did not vote for Trump."

Jennifer Victory, political scientist at George Mason University, described the administration's scheme as "violations of the rule of law that would be sufficient for impeachment in any other American presidency but aren't in this one because pathological partisan loyalty has rotted the constitutional order."

Sam Stein, managing editor at The Bulwark, said that the DOE's admission about targeting Democratic states was "something we all knew and saw at the time and yet still breathtaking to read... in print."

"We urge the commission to withdraw this proposal, enforce the rules already on the books, and return its attention to the derivatives markets it was created to protect—and which genuinely need its attention."

A coalition of consumer advocacy groups on Friday forcefully condemned the Commodity Futures Trading Commission's move to give prediction market platforms like Kalshi and Polymarket "a green light to bypass state gambling regimes."

Users of these platforms can bet on future events, from the outcome of a sports game to the language of a political speech, by buying "shares," or "contracts." The Trump administration claims the platforms are not gambling operations, but derivatives markets because, as Chair Michael Selig has noted, "Congress has entrusted the CFTC with the sole authority to regulate" those.

Various state leaders and organizations have pushed back, arguing that "calling a sports wager an 'event contract' does not transform it into a legitimate tool for managing economic risk," as Demand Progress Education Fund communications director Eric Naing said Friday. "The CFTC should not allow federal derivatives law to become a back door for nationwide gambling."

However, the CFTC has stuck to its position, publicly backed by President Donald Trump, who has declared that the agency must have "exclusive authority" over this "major industry," which "we must protect." The Republican—who infamously bankrupted multiple casinos—notably has a company exploring how to cash in on the sector.

The CFTC announced its proposed rules for prediction markets in March, followed by an update last month. In a Friday letter to the agency chair, Demand Progress Education Fund and 10 other organizations wrote that "we oppose the proposal in its entirety. It fails as a matter of law, as a matter of policy, and as a matter of institutional competence, and we emphatically urge the commission to withdraw it."

"When Kalshi and Polymarket launched just five years ago, they were curiosities; today Kalshi alone is valued at $22 billion and processes an annualized volume of $178 billion in trades every month," the coalition detailed. "This proposal should be understood for what it is: a green light for these immense and largely unregulated financial speculation platforms to offer sports betting nationwide and aggressively market it to the public, bypassing the community and mental health protections that states and tribal authorities have spent generations building to address the risks present in this type of speculative activity."

The fact that 89% of Kalshi's total fee revenue comes from sports-related contracts "should settle the question of whether these companies are derivatives exchanges or sportsbooks," according to the coalition, which also includes Americans for Financial Reform Education Fund, Better Markets, Center for Digital Democracy, New Jersey Appleseed Public Interest Law Center, Open Markets Institute, Oregon Consumer Justice, Oregon Consumer League, Protect Borrowers, Public Good Law Center, and Revolving Door Project.

However, the organizations also challenge the CFTC's interpretation of the Commodity Exchange Act, writing that the proposal's "framing inverts the statute's logic and Congress' intent, by treating contracts as presumptively allowed unless found contrary to the public interest through a case-by-case inquiry."

If the agency charges ahead with its current plans, "ordinary people will pay the price," the groups warned. "Expanded sports betting has increased personal bankruptcies, reduced household savings, and led to higher rates of domestic violence. Prediction markets supercharge these effects: they run 24/7 in your pocket and aggressively market to young adults, who may make low bets initially but ramp up their commitment over time. Seventy percent of users lose money, and 70% of all profits go to 0.04% of traders. Those outcomes define a casino that has figured out how to escape the regulations that casinos have to follow, like responsible gaming disclosures and financial stability protections for their customers."

"The proposal also does almost nothing to address the insider trading problem that makes prediction markets much more easily manipulated than the structures of ordinary gambling," the coalition wrote—just over a week after the White House had to address one of Trump's teleprompter operators allegedly using his access to the president's speech plans to make money on Kalshi.

The organizations further argued that "even if the commission were the right institution to police all of this, it is not capable of doing so. The CFTC, which oversees $400 trillion in US derivatives markets, has a budget frozen at $365 million... Adding nationwide responsibility for sports betting, entertainment wagering, and political gambling on top of that is not a proper expansion of the agency's mission, and it would mean that the farmers, manufacturers, and energy companies who depend on well-functioning commodity markets will pay the price."

"We urge the commission to withdraw this proposal, enforce the rules already on the books, and return its attention to the derivatives markets it was created to protect—and which genuinely need its attention," concluded the coalition. "The regulation of gambling and gaming belongs with the states and tribal authorities that have the experience, the tools, and the democratic accountability to do the job."