SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

When everybody has guaranteed access to high-quality care without financial barriers, physicians can focus solely on their patients’ needs and patients can trust that our recommendations are based on science.

The following remarks were delivered as testimony to the Congressional Progressive Caucus, Medicare for All Shadow Hearing on July 22, 2026.

Thank you for the opportunity to speak about our urgent need for Medicare for All. My name is Dr. Diljeet Singh, and as a practicing gynecologic oncologist, I do not exaggerate when I say our healthcare system is in dire straits. Every day in my clinic, I see patients struggling with the cost of healthcare: a woman on chemotherapy who cannot afford her anti-nausea prescription, or a patient forced to choose between an MRI copay and groceries for her family. If you walked through my clinic, you would know that this is no time to be tinkering with unproven reforms or complex regulations. It is long past time for Medicare for All.

I care for a part-time elementary school teacher whose health plan did not cover routine preventive care. Instead of getting regular Pap smears over the years, she arrived in my office with advanced cervical cancer. She underwent radical surgery followed by chemotherapy and radiation that fundamentally changed her body and her life—and she still has no guarantee of a cure.

Or consider another patient of mine who works two part-time jobs, with no health insurance. She ignored severe abdominal pain until it doubled her over. In the emergency room, she was told she had a potentially cancerous mass. She came to me for care, and thankfully, it turned out to be a non-cancerous ovarian cyst, cured by surgery. Yet, even in this best-case medical scenario, she still owes thousands of dollars. A treatable, curable medical problem absorbed her children’s college savings and her retirement money.

When the drive for profit outweighs patient health, professionals and patients alike are betrayed.

I am speaking to you today as president of Physicians for a National Health Program (PNHP), an organization of more than 25,000 health professionals nationwide. We are working to achieve universal single-payer healthcare—free from corporate middlemen, copays, deductibles, prior authorization, and the risk of medical debt. Similar countries around the world provide care to all while spending only half of what we spend—yet we die younger, face higher maternal mortality, and lose more newborns. We already spend enough money, but at least 35 cents of every healthcare dollar is wasted on insurance administration and corporate profit instead of patient care.

The root cause of this failure is the corporate takeover of healthcare, where financial interests take precedence over the sacred oath we swore as physicians—to prioritize our patients’ health and make evidence-based, patient-centered decisions free from third-party interference.

At PNHP, we conducted a two-year research project speaking with doctors about working in a profit-driven system where financial goals dictate clinical care. We found that doctors, like nurses, suffer from profound “moral injury”—the acute psychological harm caused by systemic barriers that prevent us from providing compassionate, evidence-based care. When the drive for profit outweighs patient health, professionals and patients alike are betrayed, driving clinicians out of medicine in increasing numbers.

Reversing this crisis requires recentering healthcare on patients and aligning with its true mission. The most commonsense solution is single-payer Medicare for All. When everybody has guaranteed access to high-quality care without financial barriers, physicians can focus solely on their patients’ needs and patients can trust that our recommendations are based on science and their healthcare needs—not corporate bottom lines.

Doctors, nurses, and patients understand that we need Medicare for All. Now we need Congress to understand the same thing—and to act with all of the urgency that this moment requires.

As politicians debate “universal healthcare,” we need those two words to be much more than a campaign slogan or an empty promise. Healthcare must be a true human right, easily exercised by every single person in America.

As a Maryland pediatrician, I serve patients and communities who struggle at the broken edges of the American healthcare “system.” My patients are from families working three or four jobs with no benefits, just barely getting by. With more grace than I could ever summon, these families diligently follow the protocols to determine their children’s “eligibility” for healthcare. The American healthcare system scrutinizes a family’s pay stubs, bank statements, and employment status—a process called means testing—to determine if they are eligible for Medicaid or a pittance of help to purchase a private insurance plan. It is not enough to be a human being. Our healthcare system must determine where you are on the spectrum of worthy to unworthy before you can get any medical care.

My pediatric patients whose parents get health insurance through their employment are not doing much better. An inhaler that helps an asthmatic breathe easier is covered by the insurance corporation one year, but not the next. Similarly, a specialist who has masterfully managed a patient’s seizures for several years is suddenly “out of network.” Never mind that the patient’s parents are paying premiums from every single paycheck to that multibillion-dollar insurance corporation. Playing by the corporate greed machine’s rules does not protect patients from arbitrary decisions that are supposedly good for business.

Over the course of my 20 years working in healthcare, I have seen more and more patients with supposedly good insurance avoid necessary medical care because the out-of-pocket costs keep increasing. In the richest country in the world, families are stuck between the false choices of paying for rent, groceries, utilities, or healthcare. Choosing healthcare can cost anywhere from feeding your family to putting a roof over their head.

All of us are trapped in this infuriating maze of puzzles and peril. Looking at this cruel mess of a system, we have politicians saying a “public option” is enough to fix things. There are think tanks describing a system of “universal healthcare” where the expensive (and yet, worthless) plans from private insurance corporations, the 50 shades of Medicaid, and a public option somehow achieve a magical harmony. To make things even more complicated, it is unclear what exactly a public option could look like. It could mean patients have the option of buying into Medicare or Medicaid. Or it could mean a separate public insurance plan at the federal level, possibly available to everyone or possibly just the ones deemed needy enough.

Medicare For All is true universal healthcare, where patients and families have peace of mind whenever and wherever they need medical help.

We need to be clear about what “universal healthcare” ought to mean. Everybody getting expensive-but-worthless plans from insurance corporations is universal financial stress, not universal healthcare. Similarly, adding any kind of “public option” fragment to a ridiculously fragmented system is universal confusion, not universal healthcare.

Insurance corporations have a long track record of deploying lobbyists and misinformation to undermine provisions of the Affordable Care Act. It is foolish to think these greed machines will become good-faith partners in our healthcare, competing fair and square with any kind of public option. Corporate lobbyists will see to it that any public option uses complicated means testing to determine which members of the public are worthy or unworthy of the care. These corporations will also manipulate their own plans to shut out patients who need healthcare the most, leaving them to a public option struggling to pay doctors and hospitals. Insurance greed machines do not want competition, and will undermine a public option any way they can.

Rather than tinker with a corporate-driven healthcare system determined to put profits before patients, let’s build universal healthcare through Medicare For All. Because healthcare is a human right, Medicare For All guarantees every single person living in America is eligible. We can save billions of dollars when we stop scrutinizing who is worthy or unworthy. Medicare For All provides the kind of coverage that stays with people from cradle to grave. It is mobile coverage, staying with patients from state to state, or job to job. Hospitals and clinics will remain open and properly staffed because Medicare For All puts patients first, not profits. Because all 342 million of us are covered, Medicare For All will have powerful leverage to negotiate with Big Pharma about the cost of prescriptions. Medicare For All is true universal healthcare, where patients and families have peace of mind whenever and wherever they need medical help.

We have tolerated an intolerable healthcare system for far too long. In the coming years, as politicians debate “universal healthcare,” we need those two words to be much more than a campaign slogan or an empty promise. Healthcare must be a true human right, easily exercised by every single person in America. We can and we will make that right a reality with Medicare For All.

"Let's Give Gabe the Boot!"

On behalf of those Colorado Congressional District 8 constituents who rely on Medicaid benefits to access healthcare, your neighbors who are part of the Mountain West team for Social Security Works want to help you give Trumpublican (trum-pub-li-kin) Rep. Gabe Evans the boot. Gabe voted for your benefits to be slashed because of his deep devotion to his own well-being, not yours. Gabe thinks cutting your access to healthcare is “cost cutting,” or so he claims as his reasoning behind voting for what his boss, Donald Trump, required his Trumpublican minions to do. Gabe chose your suffering to appease people in DC, and he did not give a second (or even first) thought to what might happen if he cut healthcare access for as much as 28% of his constituents (and up to 43% of the children in CD8) who depend on Medicaid. We must give Gabe Evans the boot this fall.

Gabe is not a true representative who ought to find his glory in the US House of Representatives (aka the People’s House). “We could write shame on you, Gabe,” but we don’t think a person who sees his constituents lose healthcare access and calls it cost cutting can be easily shamed. Do you? While the people in CD8 in Colorado barely elected Gabe in 2024, now they have a much more accurate sense of his loyalties.

Let’s look at what Gabe says about himself on his campaign webpage: “Congressman Gabe Evans is a conservative leader who has spent his entire life running toward challenge. He represents Colorado's 8th Congressional District, where he is fighting to secure the border, strengthen public safety, and make life more affordable for hardworking Coloradans.”

Is he writing about the Utah border or maybe that scary Four Corners part of Colorado where folks from all sorts of other states might creep in, or is he referring to The Southern Border way south of Colorado (between Texas and Mexico) that his boss, Trump, wants him to highlight as very, very dangerous to the people of his own district? So, this, then, was one of the things that was his reasoning for cutting Medicaid benefits? To have enough funds to protect CD8 from the scary border and the scary people who might come to CD8 from the scary border, Gabe cut healthcare access.

Gabe needs to get the boot. Those of us fighting to protect the social safety net not only for future generations but for our own neighbors, friends, and families right now are a much larger group than those who would harm us. The Mountain West Team of Social Security Works invites you to learn more about CD8 in Colorado.

So, who can we vote for as a smart alternative to the cruelty and misguided loyalty Gabe offers CD8? Manny Rutinel is the Democratic candidate for the CD8 seat. Manny could use strategists who know and share the outrage of his future constituents about the healthcare mess this nation is in, and it’s way past time for him to advance a sane and clear healthcare message. During a recent primary election debate televised throughout the Front Range of Colorado, Manny stumbled a bit on his healthcare policy ideals, like many politicians do when they fear attacks from the powerful health industry. Yet even in that debate, Manny did not say cutting healthcare access would be his plan.

Manny Rutinel is a young Colorado state legislator raised by a single-immigrant mom who has all the appropriate tools for success in politics. Yet he responded inelegantly to a debate question about his previous position during his college years in support of single-payer, Medicare for All financing for healthcare. Most of us can point to our college-aged opinions and ideas as subject to modification as we aged and as we gather more information upon which to base those positions. It’s not selling out; it’s maturing. Manny believes in access to healthcare—period.

Offending or alarming any healthcare industry interests in his district could spell disaster for him, and Manny knew that. I waited for him to formulate an answer like President Barack Obama once said about single-payer. Obama said that if we were starting from scratch, there is no question that single-payer (not government control of healthcare – just one public pool for insuring everyone) would be the best system to design.

But we are well beyond that, Manny might have said. He needed to clarify and broaden his position – but instead he panicked and denied any lingering support for single-payer, and that will haunt him until he clarifies his intentions to truly represent his district. We know he will represent people in CD8, and he is not a Trumpublican. Manny intends to fight not only to restore lost Medicaid funding but also look to a better, more equitable and less volatile healthcare system going forward, and he looks forward to a rich conversation with the healthcare industry leaders, doctors, nurses, caregivers, and patients in CD8.

Might a CD8 community of healthcare interests support a form of single-payer like Medicaid or Medicare or the VA with modifications and improvements? Sure, and might it be something we haven’t even mapped out yet? Of course it could. Even in nations around the world with universal health programs for their residents, healthcare programs vary greatly—but Manny supports making sure everyone can access healthcare when they are in need, and he should say that every chance he gets. There is still time, and Manny will win on this issue by a margin at least equal to the number of people Gabe decided could be sacrificed to the Trumpublican alter—and that will be a marvelous win.

So, in this piece, I want my Common Dreams readers to meet Manny and offer him support, courage and stamina to follow a courageous path upon which so many lives depend. In this political moment, we all understand the enemy. Now we need to surround one another with grace and courage as we lift imperfect Americans, imperfect politicians, and imperfect humans with our effort. Lives depend on it. Our democracy does too. So, let’s “Give Gabe the Boot.”

Trump and the GOP are betting that calling Democrats “communists” will matter to enough voters to overshadow their concerns about the cost of food, gasoline, housing and healthcare.

President Donald Trump is a desperate man. With the midterms on the horizon and his approval ratings under water, he doesn’t want to talk about affordability. Nor does he want to talk about his war with Iran. And he certainly doesn’t want to talk about Jeffrey Epstein.

What does he want to talk about? Communists.

Over the last two weeks, Trump has ratcheted up his overheated rhetoric in response to democratic socialists’ victories in primary elections in Colorado, New York, Washington, DC, and elsewhere.

During a speech to Christian conservatives at a Faith and Freedom Coalition convention in Washington on June 26, he called democratic socialists “animals” and said, “We have to stop this horrible threat of cancer that’s permeating our country called communism.” He went on to say that the “godless” communists in the Democratic Party pose a particular risk for Christians. “They will close your churches in this country,” he warned. “They will kill your people. And that’s what they’re about.”

It’s not as if Trump and his fellow Republicans haven’t hurled the communist epithet before, but over the past six months they have upped the ante.

Heading into the 250th birthday celebration on the National Mall, Trump continued his tirade. Speaking at Mount Rushmore on July 3, he not only besmirched Democrats, but immigrants as well. “There is now a resurgence of the communist menace in our land, including from newcomers to our country who embrace ideas totally opposed to our way of life and our great success,” he said. “...You can be a communist or you can be a patriot. You cannot be both.” He made no secret that he is trying to salvage Republican candidates’ chances in November. “America will never be a communist country,” he said. “We can only lose the midterms if we allow ourselves to lose the midterms if we are foolish, stupid, and unwise.”

Trump was only slightly more restrained on July 4 at the National Mall. After introducing a handful of World War II veterans and lauding them for their heroism, Trump ahistorically declared: “Our warriors did not fight communism on battlefields across the world, only to have that menace rear its ugly head right back here in America. We’re not going to let it happen.” (In fact, American troops, along with troops from Great Britain and communist Soviet Union, defeated fascism in World War II.)

It’s not as if Trump and his fellow Republicans haven’t hurled the communist epithet before, but over the past six months they have upped the ante. According to a recent Washington Post analysis of statements, social media posts, and podcasts, from January to June, they applied the word “communist” or “communism” to Democrats an average of 626 times per week, 43% more than during the same time frame in 2025.

Right-wing pundits have entered the fray, too. Megan McArdle, a self-described “right-leaning libertarian” columnist at The Washington Post, recently wrote that democratic socialist victories represent “a heady moment for the left, because socialism’s tainted brand has recovered from the vivid failures of the Soviet Union.”

Likewise, historian Arthur Herman, writing for Fox News, disingenuously equated democratic socialists’ policy agenda with that of the Soviet Union in a July 3 column. “In June, Marxist radicals calling themselves democratic socialists swept the New York City primaries...” he wrote. “...Communist-style socialism has brought poverty, mass starvation, and subsistence misery to tens of millions worldwide.”

Such attacks are nothing new. Republicans denounced Franklin Roosevelt’s New Deal as “socialism” and even “communism.” In 1961, then General Electric spokesman Ronald Reagan warned that government health insurance would lead to socialism. Over the following decades, however, Republicans largely abandoned that mantra in favor of attacks on “big government” and the welfare state.

Trump is a throwback to an earlier time. In his 2020 State of the Union address, Trump attacked socialism, claiming it “destroys nations.” Like Reagan before him, he specifically denounced a “Medicare for All” proposal endorsed by Sens. Bernie Sanders (I-Vt.), Elizabeth Warren (D-Mass.), and 130 other members of Congress at the time, calling it a “socialist takeover of our healthcare system.”

During the last election, Trump often called Democratic presidential candidate Kamala Harris a “Marxist,” tying her to her father’s economic perspective on markets and inequality. More recently, he labeled New York Mayor Zohran Mamdani, a democratic socialist, a “communist,” and dubbed Janeese Lewis George, a democratic socialist who won last month’s Washington, DC, Democratic mayoral primary, a “Communist adherent.”

Democratic socialists in the Democratic Party are not communists. If they are a member of any organization, it likely would be the Democratic Socialists of America, which does not function as a party. Communist organizations still exist in the United States, but they are politically marginal and have no representation in Congress or in any state legislature.

Likewise, democratic socialism is not synonymous with Soviet communism, which fell apart 35 years ago. The countries that democratic socialists in America hold up as models can be found in Western Europe. They are multiparty democracies with market economies, strong unions, and robust social safety programs that include universal healthcare. Their economic models are nothing like the one-party command economy of the Soviet Union and, as I pointed out in detail in a December 2025 essay, they do a much better job of ensuring their citizens live long, healthy, and prosperous lives than the United States does.

While only about 17% of Americans have a favorable view of democratic socialist politicians, their policies are quite popular. For example:

Perhaps what is holding democratic socialists back is how they identify themselves. The term “socialist” just may have too much baggage. After all, many Americans still associate the word with the Soviet Union, whose official name was the Union of Soviet Socialist Republics, even though it was a communist dictatorship.

New York Rep. Alexandria Ocasio-Cortez, a democratic socialist, told The Washington Post earlier this week that political labels should not be an issue. “What matters is the legislation, your proposals, the ideas before us,” she said. “How a person identifies in their economic view of the world is less important to people than if we’re making their groceries more affordable.”

Maybe. But Trump and the GOP are betting that calling Democrats “communists” will matter to enough voters to overshadow their concerns about the cost of food, gasoline, housing and healthcare. November will reveal whether that Cold War strategy still works.

This article first appeared at the Money Trail blog and is reposted here at Common Dreams with permission.

“The swing voters who will decide the midterms are not asking Democrats to sound more like Republicans—they want Democrats to embrace progressive economic policies that will actually work to lower costs."

Democratic strategists have long clashed over whether the path to victory runs through "moderation" or bold progressive ideas, and a new analysis of 2026 swing voters boosts arguments for the latter, revealing the top policies that would sway them to vote Democrat include raising taxes on the wealthy and establishing a Medicare for All-type universal healthcare system.

On Thursday, Data for Progress published a new report identifying a relatively small but electorally crucial bloc comprising roughly 8% of likely 2026 voters who are genuinely persuadable heading into the November midterms. These swing voters, many of whom voted for President Donald Trump in 2024, identify as moderates or independents rather than conservatives, consume relatively little political news, and are primarily focused on one issue above all else: the cost of living.

"A plurality of swing voters aren’t sure which party they trust on the major issues, but Democrats hold a slight advantage on inflation and the cost of living, the top issue for swing voters," Data for Progress found. "Around 1 in 3 swing voters say their biggest issues with the Democratic Party are its 'old and out of touch' leadership and the party 'not doing enough to lower costs.'"

"The most popular proposal was simple: Raise taxes on the wealthy," the report states. "Twenty-eight percent selected it as one of their top three choices. Close behind, at 24%, was creating a Medicare for All healthcare system. Those weren't followed by tougher immigration policies or deficit reduction. Instead, voters also favored banning artificial intelligence from setting prices or wages based on personal data and preventing utility companies from passing unreasonable costs on to consumers."

NEW: Our first report on the swing voters of the 2026 midterms finds that when they are asked which policies would make them definitely vote for a Democrat, the most selected option is “raise taxes on the wealthy,” followed by “create a Medicare for All health care system.”

[image or embed]

— Data for Progress (@dataforprogress.org) July 9, 2026 at 6:30 AM

According to the report, swing voters currently favor a Democratic candidate for Congress over a Republican by a 12-point margin, with 46% undecided.

“The swing voters who will decide the midterms are not asking Democrats to sound more like Republicans—they want Democrats to embrace progressive economic policies that will actually work to lower costs and put workers first,” Data for Progress executive director Ryan O'Donnell said on Thursday. “Voters have been making clear for years that cost-of-living issues are the top priority. Taking more conservative stances is not what voters are asking for from their leaders right now.”

State Sen. Mallory McMorrow dropped out of the race on Sunday after having positioned herself as a "moderate" choice.

With state lawmaker Mallory McMorrow having suspended her US Senate campaign, progressives on Monday were looking ahead to the final weeks of a primary race in which Michigan Democrats have a clear choice to make about who should run in the general election as the party hopes to wrest control of the chamber from Republicans: a candidate backed by the pro-Israel lobby or one who has focused his campaign largely on the broadly popular Medicare for All proposal.

US Rep. Rashida Tlaib (D-Mich.) said in a video for the grassroots advocacy group Our Revolution that "the contrast could not be clearer" ahead of the August 4 primary as voters decide between Rep. Haley Stevens, who is backed by Senate Majority Leader Chuck Schumer (D-NY), and former Detroit health official Abdul El-Sayed, who's been endorsed by progressive leaders including Sen. Bernie Sanders (I-Vt.) and Rep. Alexandria Ocasio-Cortez (D-NY).

With early voting already underway in parts of Michigan, said Tlaib, voters are choosing between "a people-powered movement versus the establishment pick."

"Abdul is on the ballot right now to be our next US senator, the only candidate that is unapologetic in supporting Medicare for All," said Tlaib, urging supporters to canvass for the progressive candidate, who has also spoken out against military funding for Israel and abolishing US Immigration and Customs Enforcement.

"All of us know the importance of direct human contact. That's how we get elected, especially someone like Dr. Abdul El-Sayed, who is unbought and doesn't take corporate [political action committee] money," she said.

Our Revolution emphasized that with McMorrow out of the race, "the numbers show this is winnable."

As El-Sayed has faced Stevens and McMorrow in the three-way race in recent months, the progressive candidate has surged in several polls following his opponents' attacks on his campaigning with vocal anti-Israel critic and streamer Hasan Piker and as he has remained focused on what he says are his top three priorities: "money out of politics, money in your pocket, and Medicare for All."

The most recent polling, from Quantus Insights, showed El-Sayed with 41% support compared with Stevens' 36% and McMorrow's 8%. Other surveys, like one from Tulchin Research for the pro-El-Sayed Fighting for Michigan PAC, found the candidate up 19 points over Stevens, with McMorrow in a distant third place.

A poll by a super PAC that supports El-Sayed also asked voters ahead of McMorrow's suspension of her campaign how they would vote if El-Sayed and Stevens were the only two candidates, and found the progressive up 54-34.

El-Sayed has argued during the campaign that Stevens' support from the American Israel Public Affairs Committee (AIPAC) as well as for-profit health insurance companies is emblematic of a corrupt political system that's been worsened in recent years by the US Supreme Court Citizens United ruling.

As Common Dreams reported in May, AIPAC has appealed to its direct donors to send contributions of Stevens during the campaign, as well as spending $10 million to boost the candidate.

“I’m the only candidate today who didn’t ask AIPAC for their support," said El-Sayed at a debate in May. "I don’t think that our taxpayer dollars which we pay every April ought to be going to bomb children, to fund bombs and tanks for other countries, when we got kids who can’t afford basic things in our own.”

Before suspending her campaign, McMorrow cast herself as a candidate who could be seen as a midway point between Stevens' establishment connections and El-Sayed's demands for bold changes to the US political system and the Democratic Party's priorities.

But Lever News founder David Sirota pointed to McMorrow's dismissive comments about Medicare for All as evidence that she was far out of step with voters.

She claimed in an interview and a debate that public support for a government-run universal healthcare program "isn't there yet," despite the fact that the proposal was backed by 78% of Democratic voters and 65% of overall voters in one recent poll.

New York Times politics reporter Reid Epstein also pointed to McMorrow's decision to join in a weekslong smear campaign against El-Sayed, over his appearances with Piker, as a move that "backfired quickly."

"Her remarks helped burnish Dr. El-Sayed's claim that he was the lone progressive candidate in the race and the one most willing to criticize American funding of the Israeli military," wrote Epstein.

While Stevens supporters have suggested she's likely to appeal to more Michigan Democratic voters, recent public polling regarding AIPAC and Israel tells a different story following Israel's US-backed assault on Gaza, which has been called a genocide by top Holocaust scholars and human rights groups.

Last October, nearly half of Democrats in competitive primary districts said they "could never" vote for a candidate backed by AIPAC, and another survey in March showed a double-digit decline in support for Israel among US voters.

One campaigner for El-Sayed said Monday that interactions with voters have suggested Stevens' AIPAC ties are seen as a liability, even among people who haven't yet heard of her opponent in the primary.

Following McMorrow's announcement that she was suspending her campaign, El-Sayed thanked the state senator and said the race has been and remains a fight against "a politics that rigs the system against too many of us."

"The same party insiders she had the courage to challenge have been bullying anyone who opposes their chosen candidate," said El-Sayed. "After spending $30 million to drown Sen. McMorrow and me out, they're now spending even more to attack me. It's everything we stand against."

"I welcome her supporters to our movement to stand up against money in politics, to put money back in pockets, and pass Medicare for All," said El-Sayed. "We cannot allow the establishment to decide our nominee for us."

"As working families continue to get squeezed left and right by GOP-driven healthcare cost hikes and bureaucratic red tape, millions more Americans will lose the care they rely on to stay alive and healthy."

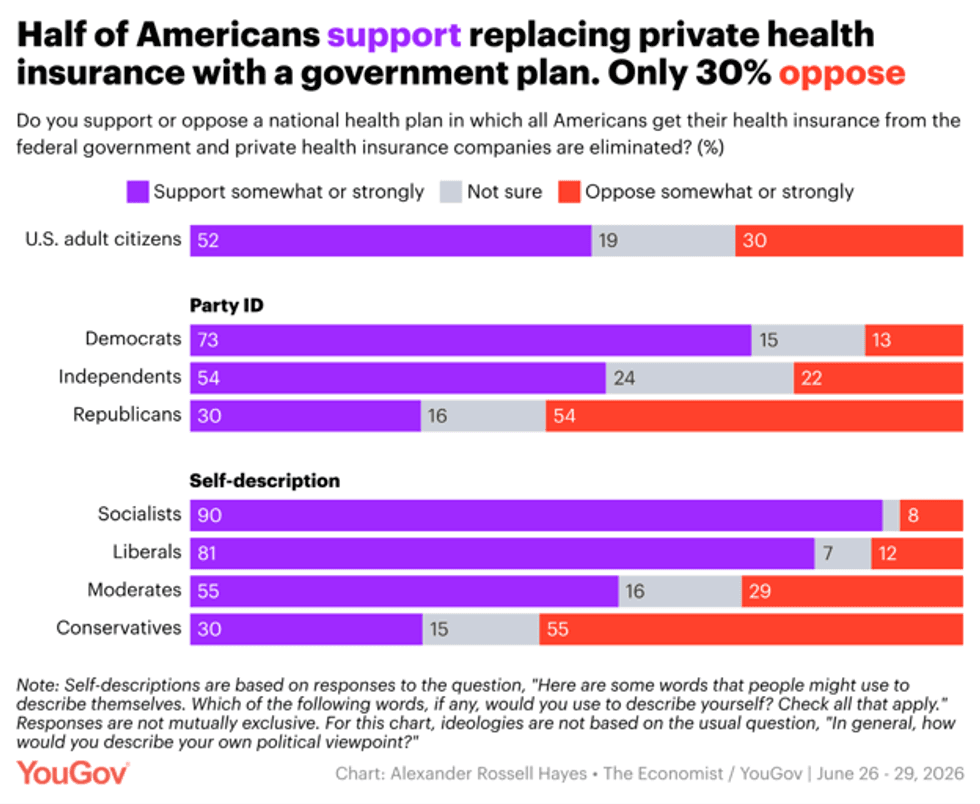

On the heels of data revealing that millions of people have lost health insurance coverage during US President Donald Trump's second term amid a series of GOP attacks on access to care, polling published Monday shows that a majority of Americans support eliminating private insurers.

The 1,606 adult US citizens surveyed by The Economist/YouGov June 26-29 were asked: "Do you support or oppose a national health plan in which all Americans get their health insurance from the federal government and private health insurance companies are eliminated?"

Fifty-two percent expressed support, and the proposal was even more popular than that among respondents under age 45 as well as registered Democrats and Independents. Just 30% of those polled were opposed, while the rest said that they were "not sure."

The polling follows the administration's quiet release of data showing that 4.2 million lost Affordable Care Act (ACA) coverage as of February. Trump and his Republican allies in Congress have come under fire for letting ACA subsidies expire at the end of last year—as well as for enacting the so-called One Big Beautiful Bill Act, which is expected to leave more working-class Americans uninsured over the next decade. Already, Protect Our Care estimates that 3.8 million people have lost coverage under Medicaid and the Children's Health Insurance Program, bringing the total for Trump's term to around 8 million.

"A mind-boggling number of Americans have found themselves joining the ranks of the uninsured," Protect Our Care president Brad Woodhouse said in a Tuesday statement. "And this is just the beginning. As working families continue to get squeezed left and right by GOP-driven healthcare cost hikes and bureaucratic red tape, millions more Americans will lose the care they rely on to stay alive and healthy."

"These are diabetic patients rationing insulin and parents skipping cancer screenings," he continued. "These are small business owners and farmers shutting down their life's work because they can no longer afford to buy insurance on their own. These are moms, veterans, and seniors. These are the millions who will hand Trump and Republicans in Congress a withering rebuke at the ballot box in November for making healthcare unaffordable so they could make billionaires and big corporations richer."

As premiums soar and Americans begin to endure the consequences of the national Republican healthcare agenda, a sweeping coalition of groups that support a universal single-payer system declared earlier this month that "now is the time for Medicare for All."

Sen. Bernie Sanders (I-Vt.) and Reps. Pramila Jayapal (D-Wash.) and Debbie Dingell (D-Mich.) have repeatedly introduced the Medicare for All Act in Congress, and support for it has grown among elected Democrats and the US public—as suggested by the new polling.

In a statement about the healthcare findings, the pollsters explained:

While eliminating insurance companies may sound like a radical change to healthcare, the share of Americans who want to replace private insurance with a government health plan (52%) is larger than the share who want to expand the existing Obamacare (the health coverage system established by the Affordable Care Act) (38%). The share who favor repealing Obamacare (28%) is about as large as the share who oppose replacing private insurance with a government plan (30%).

Americans who support a national healthcare plan do not universally see expanding Obamacare as a step in the right direction. Only a little more than half (56%) of the Americans who support creating a national health plan also support expanding Obamacare. On the other hand, most Americans who support expanding Obamacare would also support a national health plan that replaces private insurance (77%).

Although "only 8% of Americans would describe themselves as socialists," which is "smaller than the shares who describe themselves with several other ideological adjectives offered in a poll question, including progressive (17%), liberal (23%), and conservative (34%)," the pollsters also noted, "many policy proposals championed by democratic socialists draw significant support from Americans."

For example, majorities of respondents endorsed the government covering the cost of college tuition for all students (55%) and building public housing (57%).

When asked, "Do you think Donald Trump has had the right priorities or hasn’t paid enough attention to the country's most important problems?" 60% of respondents said the president "hasn't paid attention to the most important problems."

The polling comes just over four months away from the November midterm elections, in which Democrats hope to reclaim majorities in both chambers of Congress. Some Democratic candidates, including US Senate hopefuls Graham Platner in Maine and Abdul El-Sayed in Michigan, are explicitly running on support for Medicare for All.

After multiple progressives running to represent various New York districts in the US House of Representatives won their primaries last week, Sanders called their victories proof that Americans "are sick and tired of status quo politics," while Jayapal similarly celebrated that "bold, people-powered candidates took on the Democratic establishment and won."

"They ran on Medicare for All. On a public option for housing. On a foreign policy that centers human dignity over political convenience. And they won," Jayapal said. "This is what happens when movements build power. People-powered movements win."

The party is trying to get born again. This is a fight worth having.

The Democratic Party is trying to get born again.

For forty years it didn’t want to be. Since Reagan, the Democrats stopped fighting the world he built and started managing it. Bill Clinton signed NAFTA and sent the factories south. He signed the crime bill Joe Biden wrote and helped fill the prisons. He ended welfare and called it reform. He tore down the wall between the banks and your money, and a few years later the banks lost your money and got bailed out for it. Obama bailed them out, let the houses go, deported people by the millions, and kept the drone war and the surveillance state running without missing a step. On the things that decide who holds power, money and war and the police and the spying, our party and theirs were one party. That was never where they fought.

What they fought over was the rest of it, and even there they did the least they could get away with, because anything real would have cost their donors. They told us things were getting better and better. They told us they were on our side. They put out a statement for women and Black people and immigrants and Latinos every time one was due, and then they went back to managing the decline. And every couple of years they came back and told us this was the most important election of our lifetimes, so hold your nose and vote, and we did, and the rent went up anyway.

The left is connecting now because it tells the same truth and points it the right way. America is falling apart, and it didn’t fall by accident, and the people who broke it are not the busboy or the kid at the border.

Then Trump stood up and said the whole thing was a fraud and the country was a wreck. Media talking heads were appalled. They laughed at him. But he connected, because it rang true. We’d been told for thirty years that we’d never had it so good while the ground gave out under us, and here was a man saying out loud that it was a lie. The trouble was where he pointed. Trump took the truth of our condition and aimed it straight down, at the immigrant and the poor and the weak and the despised, the people with the least power in the whole arrangement. He found the real anger and fed it to the worst part of us.

The left is connecting now because it tells the same truth and points it the right way. America is falling apart, and it didn’t fall by accident, and the people who broke it are not the busboy or the kid at the border. We’ve been unjust. We’ve been immoral, paying for a genocide in Gaza with our own tax money while we couldn’t house our own people. We are failing, and we need to be redeemed. Trump never offers that last part, because his whole act runs on it being someone else’s fault. The left says it plain. We did this, and we can undo it, and we can make this country great, the real kind, not the red hat version.

So this is a fight about which future we get. One is the future the war party keeps selling, a trillion-dollar arsenal standing guard over a pile of money while the killing goes on. The other one has to be built, and it starts by telling the truth about where we’re standing. The whole question is which one we choose.

On Tuesday we got our first real look in a while at people choosing the hard one. Zohran Mamdani is the mayor of New York, and he spent his own standing to back primary challengers against sitting Democrats. Three of the House candidates he backed won, two of them democratic socialists. They ran against the party that signed the checks for Gaza, and they won anyway. Krystal Ball put it as plain as anybody, that the real radicals are the politicians who back the killing of children. Jaime Harrison, who used to run the party machine, told people like Mamdani that if they hate the Democratic Party they should stop using its name and go build their own. We’re not going anywhere. The party was never Harrison’s to hand out, and the people who actually built it just voted for the truth.

It’ll be loud and it’ll be ugly, and men like Jaime Harrison will keep telling us to leave. We’re staying, because the country is worth saving and we’re the ones who’ll do it.

We’ve been here before, and the last time we got it right. Between the 1930s and the 1960s, Democrats and socialists fought over the future and then they built one. They passed Social Security and the right to a union into law. They strung electric lines out to farms that had never seen a light bulb. They sent a generation to college on the GI Bill and gave the old and the poor a doctor with Medicare and Medicaid. They put us on the road to the moon. They built the biggest middle class the world had ever seen and pulled millions out of poverty doing it. They argued the whole way, and the country came out stronger for the fight.

But we forgot the other half of the job, which was the building. A roof you can afford. A doctor you can see. A job that holds a family together. We handed all of it to the market, and the market handed us back rent we can’t pay and care we can’t afford and kids who don’t believe they’ll ever own a home. The rights we won, for Black people and women and immigrants and gay and trans people, were real and worth every fight, but they don’t pay the rent, and the party that told us to clap never wanted to talk about the rent.

The Democratic Party needs a rebirth not a rebrand.

We’ve done it before, so we know it’s not a dream. We need a politics and an economy and a democracy and a country that works for all of us, and not for the shrinking few who bought up the last one. We can build that. And the thing they have left to stop us with is fear.

Jesse Watters went on television and said the New York socialists aren’t even socialists, they’re communists, and you can’t reason with them, you have to crush them. That’s the same move Trump makes, the powerful turning your fear on someone weaker than you. Be scared of your neighbor, and keep trusting the people who paid for a genocide and couldn’t fix a thing here at home. We’re done taking that.

So the party is trying to get born again. It’ll be loud and it’ll be ugly, and men like Jaime Harrison will keep telling us to leave. We’re staying, because the country is worth saving and we’re the ones who’ll do it. We tell the truth about how far we’ve fallen, and then we build our way back up. We make it great for real, or we don’t get it.

"He’s the strongest and safest candidate to not only hold the seat but use it to pass transformative legislation to get money out of politics, put money in pockets, and pass Medicare for All," said Abdul El-Sayed's campaign.

Opponents of progressive former Detroit public health official Abdul El-Sayed have insisted he would be a risky candidate to face Republican contender Mike Rogers, with state Sen. Mallory McMorrow, who is running against El-Sayed in the Democratic primary, suggesting his support for Medicare for All is too radical, and a centrist think tank attacking him for campaigning with an outspoken critic of Israel.

But polls released Wednesday revealed that not only is El-Sayed continuing to surge ahead of McMorrow and US Rep. Haley Stevens, but he also appears to have a better chance of beating Rogers in a statewide race.

A new poll taken by Mitchell Research and Communications between June 11-13 found El-Sayed received the support of 42% of respondents, nine points ahead of Stevens. McMorrow, who has positioned herself as a "moderate" middle ground between her two opponents, had 6% support.

The survey found that El-Sayed continued to build his support among voters under the age of 45, with the candidate 83 points ahead of his opponents in the race that has been called a "millennial showdown" by local media. All three candidates are between the ages of 39 and 42.

Last month, another survey by Mitchell Research and Communications found El-Sayed with the support of 80% of voters ages 18-44.

A separate poll released by Zenith Research on behalf of Common Defense—a grassroots organization of military veterans and their families—found El-Sayed three points ahead of Rogers, a former congressman.

Forty-five percent of respondents backed El-Sayed in a hypothetical matchup with the Republican, who had polled at 42%.

In a hypothetical McMorrow-Rogers matchup, the Democrat had 44% support compared the Republican's 42%, while Stevens was just one point ahead of Rogers.

"The difference between El-Sayed and Stevens’ vote shares—45% and 43%, respectively—appears to be due to Stevens’ relative unpopularity among voters who self-identify as 'very progressive or liberal,'" said Adam Carlson, founding partner of Zenith Polls. "Thirty-one percent of progressive/liberal voters hold a 'strongly unfavorable' view of Stevens."

Several respondents, said Carlson, cited Stevens' ties to the American Israel Public Affairs Committee "as the driving cause, which coincides with AIPAC taking a more active role in the campaign in recent weeks."

Polls have shown that since Israel began its US-backed assault on Gaza in October 2023, public support for Israel and AIPAC, the powerful pro-Israel lobby group, has plummeted, particularly among Democratic voters.

The pollster found that 51% of respondents would support a candidate who backs Medicare for All—a top focus of El-Sayed's policy platform—while 33% said they would prefer a candidate who supports maintaining the for-profit healthcare system as it is. Stevens and McMorrow have said they support a "public option" to compete with for-profit insurers. McMorrow falsely claimed in a recent interview that Medicare for All does not have significant public support.

"Abdul is the ONLY one who can turn out a broad coalition to beat Rogers in November," said El-Sayed's campaign in response to the poll. "He’s the strongest and safest candidate to not only hold the seat but use it to pass transformative legislation to get money out of politics, put money in pockets, and pass Medicare for All."

At MeidasTouch on Wednesday, correspondent Scott MacFarlane asked El-Sayed why his critics continue to claim he would not be electable in the general election.

“I think my party doesn’t really know what electability is any more," said El-Sayed. "They think electability is about being the most middle-of-the-road Democrat."

Question from @MacFarlaneNews: “You hear these concerns in your party that you’re the least electable in a general election. Why do people say that?”

Dr. @AbdulElSayed (D-MI): “I think my party doesn’t really know what electability is any more.” @MeidasTouch https://t.co/EqsPlLuyuD pic.twitter.com/3dRxenuDYv

— Luke Radel (@lukeradel) June 17, 2026

"What they don't realize," said El-Sayed, "is that the Democratic Party's brand has been destroyed by Democrats who take money from corporations to water down a message, and then wonder why our base doesn't show up for us."

The former public health official has centered the government-run healthcare proposal in his campaign.

In his first TV ad of the US Senate primary race in Michigan on Tuesday, former Detroit health official Abdul El-Sayed emphasized his top three priorities as he vies to represent working people across the state.

"This campaign will take on the powerful with three simple ideas," he said in the ad. "Money out of politics, money in your pocket, and Medicare for All."

The ad, featuring longtime Medicare for All advocate and early El-Sayed supporter Sen. Bernie Sanders (I-Vt.), marked only the latest time the candidate placed front and center the proposal to improve and expand the existing Medicare program to the entire US population, providing a government-run healthcare system that resembles those in other wealthy countries.

Today, we're going up on TV with our new ad, "Chorus."

This movement is powered by Michiganders and pro-worker champions. And our momentum is undeniable.

Michigan, we're going to get money out of politics, put money in pockets, and pass Medicare for All.

WATCH: pic.twitter.com/SM9eGH3Pm1

— Dr. Abdul El-Sayed (@AbdulElSayed) June 16, 2026

El-Sayed made the case for the program—supported by more than 100 members of the Democratic caucus in Congress as well as 78% of Democratic voters—in a video he posted on social media Monday, asking Michigan voters to imagine being diagnosed with cancer—only to realize they'll have to drive three hours to get the nearest cancer center, like many residents who don't live near one of Michigan's two nationally designated, comprehensive cancer treatment facilities.

"That's the reality for too many people who live in rural communities across our state," said El-Sayed, who wrote a book called Medicare for All: A Citizen's Guide in 2021. "Distance becomes an access issue, above and beyond all of the challenges with health insurance... And to make matters worse, with Medicaid cuts and [Affordable Care Act] cuts, all the reimbursements that should go into keeping those hospitals and clinics open, well, they're dwindling away."

Medicare for All, he said, would be "a lifeline" for people who are "traveling way too long to get the care they need."

A single-payer healthcare system that expanded the existing program, he said, would mean that everyone "reimburses at the same level, meaning it doesn't matter who you are, when you walk into a healthcare center, you're going to bring the full freight of Medicare payments to that hospital. It means that those hospitals that otherwise would have shut down get to stay open."

Imagine you’re diagnosed with cancer. And then you find out the cancer center is 3 hours away. And it’s the middle of winter.

Distance quickly becomes an access issue.

The solution? Medicare for All. pic.twitter.com/9MiJz5aKXh

— Dr. Abdul El-Sayed (@AbdulElSayed) June 15, 2026

El-Sayed also shared an exchange he had at a campaign event with a woman who said she had lost her daughter to cancer and had lost her income due to her need to become her child's full-time caregiver because in Michigan's Upper Peninsula, she had limited access to cancer care.

"Part of the reason that communities like this don't have healthcare is because you guys have two twin challenges," said El-Sayed. "One is the brokenness of our multiclass healthcare system. And one of them is distance."

"A lot of people ask me, 'Why are you so passionate about Medicare for All?'" he said. "Well part of it is, I want people to have healthcare when they need it. But part of is also for you, healthcare access isn't just health insurance. It's having a place to get the healthcare when you need it."

This is one of hundreds of stories I’ve heard from Michiganders about what can happen when someone simply gets sick in a country where healthcare is not guaranteed.

Pass Medicare for All. pic.twitter.com/g63BiKRVHT

— Dr. Abdul El-Sayed (@AbdulElSayed) June 12, 2026

El-Sayed is one of several progressive candidates pushing to bring Medicare for All to the center of US politics, six years after Sanders debated Democrats including former Vice President Kamala Harris and former President Joe Biden on the proposal on debate stages during the 2020 election.

At the time, Biden, who ultimately won the nomination and the presidency, dismissed Medicare for All as "unrealistic" and too expensive—despite studies that have shown it would save an estimated $650 billion per year. One organizer told Common Dreams in 2024 that during the Biden administration, the movement for Medicare for All became "quiet."

As Common Dreams reported last week, more than 325 organizations signed an open letter arguing that—as working families across the US struggle to keep up with rising costs of housing, groceries, gas, and other essentials while also facing the Republican Party's cuts to Affordable Care Act (ACA) subsidies and Medicaid—right now "is the time to organize" for Medicare for All.

The ACA was passed more than 16 years ago, and many Democratic candidates continue to run on promises to "protect" the program from Republican attacks.

But the GOP's efforts to gut the program have contributed to an ongoing healthcare crisis, with premiums, the uninsured rate, and the number of people relying on high-deductible "catastrophic" insurance rising this year.

In Michigan last week, the director of the United Auto Workers Region 1A in southeast Michigan told The Detroit News that El-Sayed's stance on healthcare helped him emerge as "the clear winner" as the influential union was weighing whom it would endorse in the three-way Democratic primary race.

El-Sayed is facing state Sen. Mallory McMorrow (D-8)—who recently claimed that public support "isn't there yet" for a government-run healthcare program—and US Rep. Haley Stevens (D-Mich.), who has expressed support for a "public option" but has not introduced legislation for such a system. El-Sayed noted at a recent debate that both of his opponents have taken donations from the for-profit health insurance industry.

At town halls, on his "We Can Do Better" listening tour, and on his social media accounts, El-Sayed has centered the demand for Medicare for All, denouncing opponents of the proposal who have claimed it would be unaffordable for the US—despite the fact that Republicans in Congress last week advanced a proposed Pentagon budget that exceeds $1 trillion.

"It's a funny thing, nobody ever asks the general who's drawing up war plans in Iran, 'General, how are you gonna pay for that?'" said El-Sayed at a recent event. "I happen to believe that rather than sending our money over there, or fighting foreign wars over there... I would rather end this dumb-ass war in Iran, abolish [Immigration and Customs Enforcement], and spend our money on healthcare here at home."