SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

More than 20 million Americans are expected to see their health insurance premiums more than double next year after Republicans refused to extend a tax credit for those who purchase health insurance on the Affordable Care Act marketplace.

And as the GOP remains firm in its stance that it will not vote to extend the credits in order to end the government shutdown entering its third week and the open enrollment period for ACA insurance fast approaching, Americans in some states are already getting a glimpse into how the price of their insurance will skyrocket in 2026.

On Wednesday, ACA health insurance marketplaces in six states—California, Maine, Minnesota, Vermont, Oregon, and Kentucky—launched "window shopping" tools that allow residents to compare their current insurance premiums with the ones they can expect to pay next year.

Across each of these states, the advocacy group Protect Our Care found plans that are expected to increase dramatically, sometimes to prices several times higher than they were this year.

“There is no longer any doubt about the healthcare disaster Republicans have created,” said the group's chair, Leslie Dach. “Working families can now log onto a computer and see the Republican healthcare betrayal right before their eyes."

Middle-income Americans who are older, but not yet old enough to receive Medicare, are expected to see the steepest increases in their premiums, according to KFF. When Protect Our Care looked at plans for 60-year-old couples making $85,000 a year, the group found staggering results in each state.

In Clay County, Kentucky, the group found that a Clear Silver plan, which charges that couple a premium of $559 per month this year, will cost $2,736—nearly five times that amount—next year after subsidies expire.

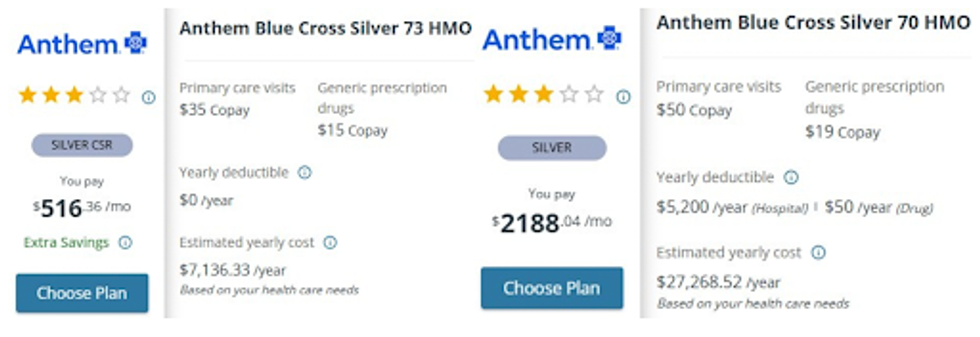

A screenshot of California's Affordable Care Act insurance marketplace website shows the price of an Anthem Blue Cross Silver plan for a couple in Mission Viejo, California, in 2025 (L) vs. 2026 (R). (Screenshot from Protect Our Care)

A screenshot of California's Affordable Care Act insurance marketplace website shows the price of an Anthem Blue Cross Silver plan for a couple in Mission Viejo, California, in 2025 (L) vs. 2026 (R). (Screenshot from Protect Our Care)

In Mission Viejo, California, premiums for the same couple's Anthem Blue Cross Silver plan would more than quadruple, from $516 per month this year to $2,188 next year.

The same is true in Medford, Oregon, where a Moda Health Silver plan would increase from $622 this year to $2,644.

In Burlington, Vermont, an MVP Silver plan that costs $602 per month this year will spike to $2,577.

While these are particularly egregious examples, KFF estimated earlier this month that the average ACA recipient will see their premiums increase by 114% next year, which the nonpartisan Congressional Budget Office expects will result in more than 4 million people becoming unable to afford health insurance.

State-level estimates from the Center on Budget and Policy Priorities (CBPP) found that across the states that have opened window shopping, costs for many families were doubling, tripling, or worse.

Residents across the country are beginning to grapple with the extraordinary rise in costs they are about to face.

In Tennessee, where more than half a million people pay lower premiums due to the ACA subsidies, a 62-year-old Chattanooga resident, Cheri Roberts, told the Chattanooga Times Free Press that if they are allowed to expire, her current $10 a month premium will explode to $1,140 next year.

"I just had no idea," Roberts said about the expiring tax credits, adding that she sees eight different specialists for varying health issues and has multiple surgeries planned. "I'm not trying to exaggerate, but I might die if I stop going to the doctor."

Julia Tilley, a resident of Harrisburg, Pennsylvania, told PennLive/The Patriot-News that she fears her premiums will soar as Pennsylvania's insurance department predicts a premium increase of 102% on average for its 530,000 ACA recipients.

Though she says she has not yet received a letter from her insurer, Tilley said one of her friends was told their family's premiums were ballooning from $100 to $1,800 a month.

“There’s really no way to prepare for it,” Tilley said. “I mean, how do you suddenly come up with $15,000 more a year? My husband can’t work more because he has a head injury."

Tilley says she already works full-time taking care of her adult daughter, who has autism. "It’s not like I can go get another job," she says. "So we’re stuck.”

She says she has tried on multiple occasions to reach out to her Republican congressman, Rep. Scott Perry, but has not heard back.

According to KFF, 57% of ACA recipients live in congressional districts represented by Republicans, and polls by the organization have suggested that failure to extend the subsidies may hurt their electoral chances.

A poll from early October found that 78% of adults say that Congress should extend the subsidies, including the vast majority of Democrats and independents and even 57% of self-identified "MAGA" Republicans. If the subsidies are not extended, 39% who support extending them have said they'd blame US President Donald Trump, while another 37% say they'd blame Republicans in Congress. Just 22% say they'd blame Democrats.

"Virtually all marketplace enrollees—across states, ages, family sizes, and income levels—will see big premium increases," said Gideon Lukens, a senior fellow and director of health policy research for CBPP. "These are real people facing real consequences if Congress doesn’t act to extend the enhancements as soon as possible."

More than 20 million Americans are expected to see their health insurance premiums more than double next year after Republicans refused to extend a tax credit for those who purchase health insurance on the Affordable Care Act marketplace.

And as the GOP remains firm in its stance that it will not vote to extend the credits in order to end the government shutdown entering its third week and the open enrollment period for ACA insurance fast approaching, Americans in some states are already getting a glimpse into how the price of their insurance will skyrocket in 2026.

On Wednesday, ACA health insurance marketplaces in six states—California, Maine, Minnesota, Vermont, Oregon, and Kentucky—launched "window shopping" tools that allow residents to compare their current insurance premiums with the ones they can expect to pay next year.

Across each of these states, the advocacy group Protect Our Care found plans that are expected to increase dramatically, sometimes to prices several times higher than they were this year.

“There is no longer any doubt about the healthcare disaster Republicans have created,” said the group's chair, Leslie Dach. “Working families can now log onto a computer and see the Republican healthcare betrayal right before their eyes."

Middle-income Americans who are older, but not yet old enough to receive Medicare, are expected to see the steepest increases in their premiums, according to KFF. When Protect Our Care looked at plans for 60-year-old couples making $85,000 a year, the group found staggering results in each state.

In Clay County, Kentucky, the group found that a Clear Silver plan, which charges that couple a premium of $559 per month this year, will cost $2,736—nearly five times that amount—next year after subsidies expire.

A screenshot of California's Affordable Care Act insurance marketplace website shows the price of an Anthem Blue Cross Silver plan for a couple in Mission Viejo, California, in 2025 (L) vs. 2026 (R). (Screenshot from Protect Our Care)

In Mission Viejo, California, premiums for the same couple's Anthem Blue Cross Silver plan would more than quadruple, from $516 per month this year to $2,188 next year.

The same is true in Medford, Oregon, where a Moda Health Silver plan would increase from $622 this year to $2,644.

In Burlington, Vermont, an MVP Silver plan that costs $602 per month this year will spike to $2,577.

While these are particularly egregious examples, KFF estimated earlier this month that the average ACA recipient will see their premiums increase by 114% next year, which the nonpartisan Congressional Budget Office expects will result in more than 4 million people becoming unable to afford health insurance.

State-level estimates from the Center on Budget and Policy Priorities (CBPP) found that across the states that have opened window shopping, costs for many families were doubling, tripling, or worse.

Residents across the country are beginning to grapple with the extraordinary rise in costs they are about to face.

In Tennessee, where more than half a million people pay lower premiums due to the ACA subsidies, a 62-year-old Chattanooga resident, Cheri Roberts, told the Chattanooga Times Free Press that if they are allowed to expire, her current $10 a month premium will explode to $1,140 next year.

"I just had no idea," Roberts said about the expiring tax credits, adding that she sees eight different specialists for varying health issues and has multiple surgeries planned. "I'm not trying to exaggerate, but I might die if I stop going to the doctor."

Julia Tilley, a resident of Harrisburg, Pennsylvania, told PennLive/The Patriot-News that she fears her premiums will soar as Pennsylvania's insurance department predicts a premium increase of 102% on average for its 530,000 ACA recipients.

Though she says she has not yet received a letter from her insurer, Tilley said one of her friends was told their family's premiums were ballooning from $100 to $1,800 a month.

“There’s really no way to prepare for it,” Tilley said. “I mean, how do you suddenly come up with $15,000 more a year? My husband can’t work more because he has a head injury."

Tilley says she already works full-time taking care of her adult daughter, who has autism. "It’s not like I can go get another job," she says. "So we’re stuck.”

She says she has tried on multiple occasions to reach out to her Republican congressman, Rep. Scott Perry, but has not heard back.

According to KFF, 57% of ACA recipients live in congressional districts represented by Republicans, and polls by the organization have suggested that failure to extend the subsidies may hurt their electoral chances.

A poll from early October found that 78% of adults say that Congress should extend the subsidies, including the vast majority of Democrats and independents and even 57% of self-identified "MAGA" Republicans. If the subsidies are not extended, 39% who support extending them have said they'd blame US President Donald Trump, while another 37% say they'd blame Republicans in Congress. Just 22% say they'd blame Democrats.

"Virtually all marketplace enrollees—across states, ages, family sizes, and income levels—will see big premium increases," said Gideon Lukens, a senior fellow and director of health policy research for CBPP. "These are real people facing real consequences if Congress doesn’t act to extend the enhancements as soon as possible."

More than 20 million Americans are expected to see their health insurance premiums more than double next year after Republicans refused to extend a tax credit for those who purchase health insurance on the Affordable Care Act marketplace.

And as the GOP remains firm in its stance that it will not vote to extend the credits in order to end the government shutdown entering its third week and the open enrollment period for ACA insurance fast approaching, Americans in some states are already getting a glimpse into how the price of their insurance will skyrocket in 2026.

On Wednesday, ACA health insurance marketplaces in six states—California, Maine, Minnesota, Vermont, Oregon, and Kentucky—launched "window shopping" tools that allow residents to compare their current insurance premiums with the ones they can expect to pay next year.

Across each of these states, the advocacy group Protect Our Care found plans that are expected to increase dramatically, sometimes to prices several times higher than they were this year.

“There is no longer any doubt about the healthcare disaster Republicans have created,” said the group's chair, Leslie Dach. “Working families can now log onto a computer and see the Republican healthcare betrayal right before their eyes."

Middle-income Americans who are older, but not yet old enough to receive Medicare, are expected to see the steepest increases in their premiums, according to KFF. When Protect Our Care looked at plans for 60-year-old couples making $85,000 a year, the group found staggering results in each state.

In Clay County, Kentucky, the group found that a Clear Silver plan, which charges that couple a premium of $559 per month this year, will cost $2,736—nearly five times that amount—next year after subsidies expire.

A screenshot of California's Affordable Care Act insurance marketplace website shows the price of an Anthem Blue Cross Silver plan for a couple in Mission Viejo, California, in 2025 (L) vs. 2026 (R). (Screenshot from Protect Our Care)

In Mission Viejo, California, premiums for the same couple's Anthem Blue Cross Silver plan would more than quadruple, from $516 per month this year to $2,188 next year.

The same is true in Medford, Oregon, where a Moda Health Silver plan would increase from $622 this year to $2,644.

In Burlington, Vermont, an MVP Silver plan that costs $602 per month this year will spike to $2,577.

While these are particularly egregious examples, KFF estimated earlier this month that the average ACA recipient will see their premiums increase by 114% next year, which the nonpartisan Congressional Budget Office expects will result in more than 4 million people becoming unable to afford health insurance.

State-level estimates from the Center on Budget and Policy Priorities (CBPP) found that across the states that have opened window shopping, costs for many families were doubling, tripling, or worse.

Residents across the country are beginning to grapple with the extraordinary rise in costs they are about to face.

In Tennessee, where more than half a million people pay lower premiums due to the ACA subsidies, a 62-year-old Chattanooga resident, Cheri Roberts, told the Chattanooga Times Free Press that if they are allowed to expire, her current $10 a month premium will explode to $1,140 next year.

"I just had no idea," Roberts said about the expiring tax credits, adding that she sees eight different specialists for varying health issues and has multiple surgeries planned. "I'm not trying to exaggerate, but I might die if I stop going to the doctor."

Julia Tilley, a resident of Harrisburg, Pennsylvania, told PennLive/The Patriot-News that she fears her premiums will soar as Pennsylvania's insurance department predicts a premium increase of 102% on average for its 530,000 ACA recipients.

Though she says she has not yet received a letter from her insurer, Tilley said one of her friends was told their family's premiums were ballooning from $100 to $1,800 a month.

“There’s really no way to prepare for it,” Tilley said. “I mean, how do you suddenly come up with $15,000 more a year? My husband can’t work more because he has a head injury."

Tilley says she already works full-time taking care of her adult daughter, who has autism. "It’s not like I can go get another job," she says. "So we’re stuck.”

She says she has tried on multiple occasions to reach out to her Republican congressman, Rep. Scott Perry, but has not heard back.

According to KFF, 57% of ACA recipients live in congressional districts represented by Republicans, and polls by the organization have suggested that failure to extend the subsidies may hurt their electoral chances.

A poll from early October found that 78% of adults say that Congress should extend the subsidies, including the vast majority of Democrats and independents and even 57% of self-identified "MAGA" Republicans. If the subsidies are not extended, 39% who support extending them have said they'd blame US President Donald Trump, while another 37% say they'd blame Republicans in Congress. Just 22% say they'd blame Democrats.

"Virtually all marketplace enrollees—across states, ages, family sizes, and income levels—will see big premium increases," said Gideon Lukens, a senior fellow and director of health policy research for CBPP. "These are real people facing real consequences if Congress doesn’t act to extend the enhancements as soon as possible."