5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

The policy brief, published Monday by the American Economic Liberties Project (AELP), an anti-monopoly think tank, argues that the system is a massive drag on the US healthcare system, draining doctors of their time, fueling hiring shortages, and—most importantly—worsening treatable health problems for millions of Americans.

"This practice has massive financial and human costs, as I know personally from my family’s own tragic experience,” said the report's author, Hannah Garden-Monheit—a senior fellow at the AELP, whose late father was denied rehab by UnitedHealthcare after cancer forced his leg to be amputated.

"Prior authorization may have started as a narrow cost-control tool," she explained. "But it’s mushroomed into private insurers’ strategy for diverting resources from care toward their own profits. It’s time to ban prior authorization as we know it.”

The report examines how prior authorization went from a tool used sparingly to prevent payment for unnecessary treatments to what Garden-Monheit and co-author, AELP senior healthcare fellow Emma Freer, described as a "corporate care veto."

Around 1 in 5 adults with private insurance report that they or a family member had experienced a coverage denial in the past year, with 28% reporting that it worsened their health problem, according to a June survey from the Commonwealth Fund.

While insurers claim that their decisions to deny care are "evidence-based," the authors say that "in reality, the practice empowers distant corporate entities with a financial conflict of interest to override the professional judgment of physicians with firsthand knowledge of patients’ medical needs."

"There is generally little to no transparency or accountability for these decisions," the authors wrote.

While insurers claim that denials are reviewed by qualified clinicians, one survey from the American Medical Association (AMA) found that only 16% of physicians participating in peer-to-peer reviews reported that the “peer” was often or always qualified.

Garden-Monheit said United denied her father's claim multiple times, first citing his cancer diagnosis—the reason his leg was amputated in the first place—then by claiming that he had made significant enough "progress" that paying for rehab was unnecessary. The "progress" was that he "had figured out how to hop on one leg from his hospital bed to a chair."

Garden-Monheit describes how she, her father, and their care team were forced to navigate a "bureaucratic maze" by United, which ultimately led them to give up.

"At least twice, I learned of a denial only after calling United to check on the status of their request. They hadn’t even bothered with a letter," she said. "While the lines of communication felt frustratingly unpredictable, the answers always led to the same place: 'no.'"

As she explained in a recent op-ed for MS NOW: "My family’s experience wasn’t a one-off glitch. For United, the system was working as designed."

Former United chief medical officer Dr.Archelle Georgiou estimated that across just two Medicare Advantage plans from United and Humana, the companies save an estimated $100 million per year by denying claims that never get appealed. She said that's a "conservative estimate." Across the two plans, 1.75 million people were denied care, even after appeal.

While insurers pad their profits, patients suffer, the researchers found. Among people reporting a prior authorization denial, 41% said it delayed their care and 28% said their health problem worsened, according to the Commonwealth survey.

"My family’s experience wasn’t a one-off glitch. For United, the system was working as designed."

Meanwhile, the AMA survey found that 95% of physicians said that prior authorization delays care, 79% said it causes patients to abandon recommended treatments, and more than 1 in 4 doctors said it has caused a serious adverse event, including hospitalization, permanent impairment, or death.

Denied timely treatments, many patients end up paying for costly and ineffective alternatives that only make their situations worse and cause the costs to increase down the line.

"It was extremely difficult to obtain authorizations for substance abuse treatment when I covered the emergency department as a practicing psychologist," one healthcare professional, identified in the report as Nancy, said. "Other times, in my private practice, I would get authorizations and later experience ‘clawbacks’ where Blue Cross, for example, would decide the treatment was not medically necessary and take back the money already paid."

"It is impossible at times to provide sound ethical treatment and extremely hard to make a living," she said, "when reimbursement rates kept going down, and the insurance companies could take back the money they had already paid for no obvious reason.”

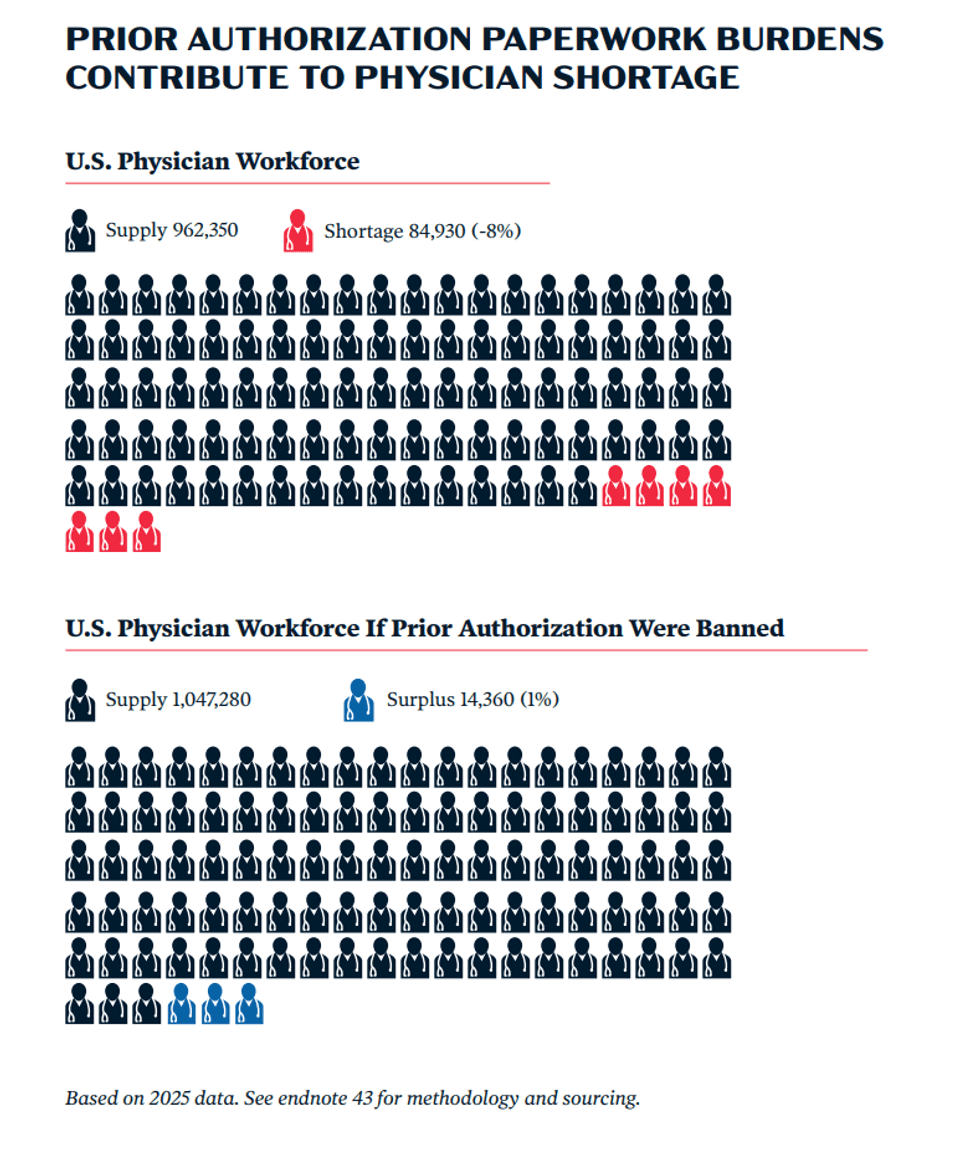

Prior authorization doesn't just deny care to patients. It also creates piles of paperwork for their doctors, taking away precious time that could be dedicated to their care.

The report found that physicians and their teams now spend so much on prior authorization paperwork that it consumes the equivalent of nearly 100,000 full-time physician and advanced practice clinician workloads, plus more than 213,000 clinic staff, costing as much as $32.7 billion each year. If prior authorization were eliminated, they found, it would free up enough capacity to turn a national physician shortage into a surplus.

(Graphic: American Economic Liberties Project)

(Graphic: American Economic Liberties Project)

A YouGov poll for AELP found that more than two-thirds of voters in both parties want legislation banning prior authorization outright. But the researchers said both the Trump and Biden administrations have enacted only minor reforms that "fail to address the structural conflict of interest that underpins the corporate care veto strategy."

Meanwhile, the industry is making the denial process even more ruthlessly efficient, increasingly deploying artificial intelligence to deny requests en masse.

According to a 2023 class action lawsuit, United's NaviHealth system used a predictive AI model to determine whether Medicare Advantage patients should receive rehabilitation care despite knowing that the model had a 90% error rate.

President Donald Trump, meanwhile, has expanded prior authorization for traditional Medicare through a pilot program that allows AI models to adjudicate claims in some states. In July, Senate Republicans blocked Democrats' attempt to end the pilot program.

As part of a national pro-AI strategy, Trump has also sought to preempt state laws banning the use of AI to deny care.

The AELP researchers called for a series of reforms to end prior authorization as it currently exists. Among other changes, they said decisions to authorize treatments should be made by independent third parties without the incentive to deny care, that denials must be evidence-based, that the use of AI tools to deny claims should be banned, and that physicians should review patients in person before denying their claims.

“For too long, prior authorization has allowed insurance companies to put profits ahead of patients by overruling doctors and delaying and denying essential care,” Freer said. “This status quo is failing patients, ratcheting up costs, and undermining the basis of effective, expert-informed care. It’s time to end this ‘corporate care veto’ and put medical decisions back where they belong: with patients and their doctors.”