September, 17 2008, 10:46am EDT

The American Civil Liberties Union was founded in 1920 and is our nation's guardian of liberty. The ACLU works in the courts, legislatures and communities to defend and preserve the individual rights and liberties guaranteed to all people in this country by the Constitution and laws of the United States.

(212) 549-2666LATEST NEWS

As Premiums Soar and Millions Lose Coverage, Over Half of Americans Say End Private Health Insurance

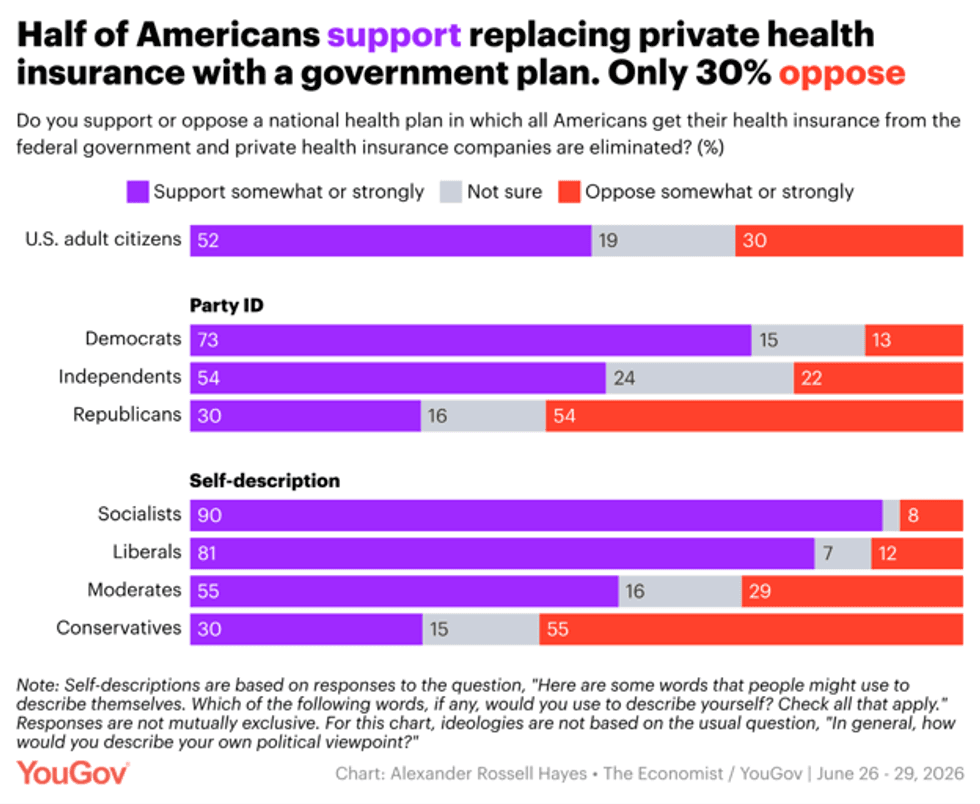

Fifty-two percent expressed support, and the proposal was even more popular than that among respondents under age 45 as well as registered Democrats and Independents. Just 30% of those polled were opposed, while the rest said that they were "not sure."

The polling follows the administration's quiet release of data showing that 4.2 million lost Affordable Care Act (ACA) coverage as of February. Trump and his Republican allies in Congress have come under fire for letting ACA subsidies expire at the end of last year—as well as for enacting the so-called One Big Beautiful Bill Act, which is expected to leave more working-class Americans uninsured over the next decade. Already, Protect Our Care estimates that 3.8 million people have lost coverage under Medicaid and the Children's Health Insurance Program, bringing the total for Trump's term to around 8 million.

"A mind-boggling number of Americans have found themselves joining the ranks of the uninsured," Protect Our Care president Brad Woodhouse said in a Tuesday statement. "And this is just the beginning. As working families continue to get squeezed left and right by GOP-driven healthcare cost hikes and bureaucratic red tape, millions more Americans will lose the care they rely on to stay alive and healthy."

"These are diabetic patients rationing insulin and parents skipping cancer screenings," he continued. "These are small business owners and farmers shutting down their life's work because they can no longer afford to buy insurance on their own. These are moms, veterans, and seniors. These are the millions who will hand Trump and Republicans in Congress a withering rebuke at the ballot box in November for making healthcare unaffordable so they could make billionaires and big corporations richer."

As premiums soar and Americans begin to endure the consequences of the national Republican healthcare agenda, a sweeping coalition of groups that support a universal single-payer system declared earlier this month that "now is the time for Medicare for All."

Sen. Bernie Sanders (I-Vt.) and Reps. Pramila Jayapal (D-Wash.) and Debbie Dingell (D-Mich.) have repeatedly introduced the Medicare for All Act in Congress, and support for it has grown among elected Democrats and the US public—as suggested by the new polling.

In a statement about the healthcare findings, the pollsters explained:

While eliminating insurance companies may sound like a radical change to healthcare, the share of Americans who want to replace private insurance with a government health plan (52%) is larger than the share who want to expand the existing Obamacare (the health coverage system established by the Affordable Care Act) (38%). The share who favor repealing Obamacare (28%) is about as large as the share who oppose replacing private insurance with a government plan (30%).

Americans who support a national healthcare plan do not universally see expanding Obamacare as a step in the right direction. Only a little more than half (56%) of the Americans who support creating a national health plan also support expanding Obamacare. On the other hand, most Americans who support expanding Obamacare would also support a national health plan that replaces private insurance (77%).

Although "only 8% of Americans would describe themselves as socialists," which is "smaller than the shares who describe themselves with several other ideological adjectives offered in a poll question, including progressive (17%), liberal (23%), and conservative (34%)," the pollsters also noted, "many policy proposals championed by democratic socialists draw significant support from Americans."

For example, majorities of respondents endorsed the government covering the cost of college tuition for all students (55%) and building public housing (57%).

When asked, "Do you think Donald Trump has had the right priorities or hasn’t paid enough attention to the country's most important problems?" 60% of respondents said the president "hasn't paid attention to the most important problems."

The polling comes just over four months away from the November midterm elections, in which Democrats hope to reclaim majorities in both chambers of Congress. Some Democratic candidates, including US Senate hopefuls Graham Platner in Maine and Abdul El-Sayed in Michigan, are explicitly running on support for Medicare for All.

After multiple progressives running to represent various New York districts in the US House of Representatives won their primaries last week, Sanders called their victories proof that Americans "are sick and tired of status quo politics," while Jayapal similarly celebrated that "bold, people-powered candidates took on the Democratic establishment and won."

"They ran on Medicare for All. On a public option for housing. On a foreign policy that centers human dignity over political convenience. And they won," Jayapal said. "This is what happens when movements build power. People-powered movements win."

Most Popular