SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Deep enough that it was able to survive the emerging problems it created. When pollution dimmed cities in the 1960s, that gave rise to the first Earth Day—and to the catalytic converters and the smokestack filters that reduced the problem enough that it never challenged hydrocarbon dominance: We could have our cake and breathe it too. The oil shocks of the 1970s threatened that dominance in the targeted US but didn’t quite topple it; the Reagan program of dramatically increased drilling, and the extension of America’s military shield to the Middle East, gave us enough sense of safety that we stayed on course.

Rising fears about climate change seemed set to tarnish fossil fuel—after all, it now threatened an end to the physical future of our civilizations—but the effects of global warming have in the early stages been sporadic and local, and when the heatwave fades or the fire goes out or the flood recedes we’ve generally reverted back to the perceived and comforting inevitability of fossil fuel. It’s what we’ve known, and hence we’ve put up with a lot to keep the relationship going.

Donald Trump has managed to break the two-century-old grip of fossil fuel on the human imagination.

But there’s been nothing sporadic or local about the effects of this war. As tanker traffic through the Strait of Hormuz slowed and then stopped, the effects have been dramatic, immediate, and global. In Thailand farmers report they can’t find diesel to keep the pumps that irrigate rice paddies running; in Myanmar, as fertilizer prices soar, the World Food Program has warned that food production costs could double compared with last year’s harvest, in a country where a quarter of the population is already facing acute hunger. There are things we can change to cut energy use (the Thai prime minister said AC units should be set at 80°F, and that bureaucrats should stop wearing neckties “except for ceremonies”) but other customs are harder to rearrange: Bodies are piling up at Thai temples because they’re out of fuel for cremations. In Bangladesh, the prime minister has turned off most of the lights in his office, and economic life is changing by the week:

“I used to do 15 trips a day. Now I spend hours just looking for a pump that’s open, and sometimes I go home empty,” said Sohel Sarker, 38, a ridesharing biker in Dhaka. “I don’t know from one day to the next whether I’ll find fuel.”

These anecdotes add up to much more. As a team from the Financial Times concluded after a global inventory of the shifts:

High fuel prices and shortages force consumers to buy fewer goods. Businesses invest less and governments conserve scarce resources, causing economies to experience weaker growth. The enduring disruption of an energy shock can trigger the destruction of demand, driving economies toward stagnation and recession.

But that’s the macro level. At the micro level, it’s as much about psychology as anything else. The Guardian published an excellent account of how fuel shortages are affecting daily life around the world, and I found myself thinking about the words of another Thai, Teerayut Ruenrerng, owner of a mobile grocery truck:

At about midday, I return home from my morning selling session. I’ll pass three gas stations on the way and stop at each one. Sometimes I can get fuel, sometimes I can’t. Sometimes they will only give me 300 baht or 500 baht (US$9.15 to US$15.25) worth. At lunchtime I take a break, and sleep for about an hour. I start work at midnight.

If I’m able to fill up a full tank, I can relax because I know I don’t need to search for gas for at least three days and it’s guaranteed I can go out and sell. But if I can’t find any, I start to get stressed and panic about what I’ll do if I can’t get fuel.

Here’s an interior designer in Sydney:

It’s frightening, because you don’t know how long it’s going to go on for.

I just started looking for jobs, because I don’t know whether people are even going to want to spend money on renovating right now, or are going to want a designer. I’m pretty much throwing everything at it, which I think is part of the panic setting in.

And here’s a warehouse worker in Delhi:

As I get ready for work, my eyes keep returning to the gas stove. I last ate yesterday afternoon, some lentils with chapatis. It has been more than a day. I am very hungry, but there is only enough gas left for four or five meals. I hold back, saving it for worse days. There are a couple of cucumbers and tomatoes. I will cut them, add salt, and eat that, and save one more day.

Now, just think of that for a moment. The gas stove, to an Indian, is suddenly a symbol of scarcity, deprivation, fear. The stuff that supplies it comes from somewhere distant over which he has no control—if President Donald Trump gets an idea, or the Islamic Republican Guards get an idea, then the flow on which it depends can stop, and then he goes hungry, counting how many meals his canister might still contain. Multiply this by a few billion people and a few key facets of each life—dinner, commute, heat, cold—and you end up with a profoundly different mindset.

In the very short run, that may mean that countries like India lurch toward coal—fairly cheap, and fairly easily available. The forecast for May and June in India is even hotter than usual before the monsoon descends, and according to Bloomberg the country is preparing to burn more of the black rocks to keep air conditioners running. Even a few years ago, that would have been the country’s only real recourse: belt-tightening, and shifting to a different fossil fuel. But the Trumpian revelations about the undependability of fossil fuel come at a significant moment in human history, a moment when we have—again, suddenly—a very different choice. As David Fickling reports:

With the LNG [liquefied natural gas] drought pushing up electricity prices and photovoltaics providing a cheaper, easier alternative, a boom in rooftop solar is far more likely than a return to coal. Don’t look under the ground for the solution to the LNG crisis. The answer is in the skies.

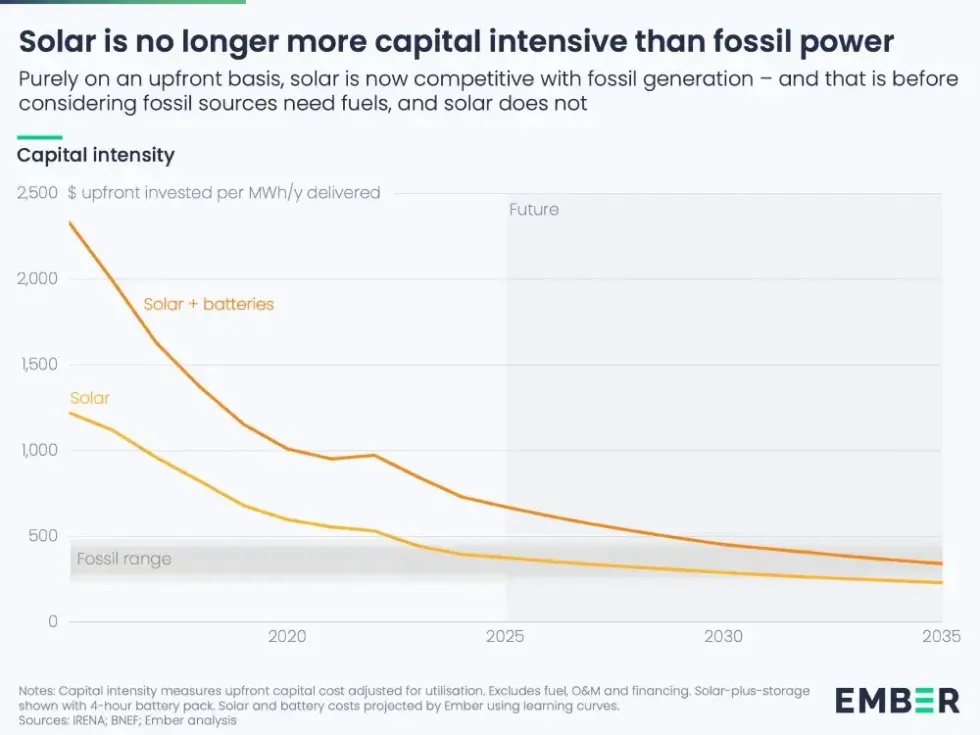

Here’s a chart worth looking at, from the think tank Ember. It requires a bit of explaining. The old story about clean energy—that is, the story of the last five years—is that it was cheaper to operate than fossil fuel power, because the fuel (sunshine) was free, but that the upfront costs were higher because you had to build those solar panels. But now it’s so cheap to build the solar panels that from the jump it make sense to switch. That gray band at the bottom is the price of the fossil fuel system, and that orange line is solar with batteries, which provides the same reliable power. Again, this is the upfront cost—in the long run, of course, the solar system is hugely cheaper, because, again, the sun delivers the energy for free when it rises above the horizon.

Anyway, let’s think about India and stoves again. For a long time if you wanted to cook your food in India, you needed to go out and gather firewood or dung, something that took a long time (and was a chore usually assigned to women). When you burned it, you had to tend the fire carefully, and you (and your kids) breathed a lot of bad stuff. There have been many attempts to supply alternative cookstoves, but they never worked very well. But now—well, now, the government is moving quickly to boost production and import of induction cooktops. An induction cooktop—I’m simmering chowder on mine as I write—produces heat for cooking without much electricity, and that electricity can be supplied by solar panels and batteries, which are cheap. Suddenly the stuff we want from energy comes more easily, more dependably, and more affordably from the sun and wind.

This is happening, all of a sudden, everywhere and with everything. Here’s a Pakistani farmer explaining why, with a solar panel to run his irrigation pump, he no longer cares about the supply of gas from the Gulf:

“Now, I don’t care if the prices of diesel increase,” he says, proudly pointing to the sun above. “As long as there is this sun, I can grow my watermelons.”

In Europe, the online marketplace Olx reported a huge jump in inquiries about electric vehicless—for instance, in France (up 50%), Portugal (up 54 percent), Romania (up 40%), and Poland (up 39%). From Jakob Steinschaden, news exported a total of 120,083 electric and hybrid vehicles in March 2026, an increase of 65% compared to March 2025. The Washington Post reported yesterday that shares in China’s biggest battery maker had jumped by nearly a third since the war began:

Indonesian President Prabowo Subianto said in March that his government would build 100 gigawatts of solar power in the next two years. Philippines’ state-owned pension is offering loans of up to $8,300 for members to buy and install solar power for their homes.

When Abraham Maslow first detailed the hierarchy of human needs, he put our physiological needs—food, shelter—at the bottom, and just above them our need for stability and security. There have been critiques of his theory, but the basic idea stands. What’s curious about renewable energy is that it’s always filled higher-order desires—for belonging, for esteem—better than fossil fuel; poll after poll shows that pretty much everyone understands that, all things equal, it’s better not to pollute the air. But now clean energy fills those most basic psychological requirements better too.

Think of the amount of money the fossil fuel industry has spent over the years to invest oil and gas with psychological power: Who could forget, for instance, the campaign that Rebecca Leber uncovered years ago that paid cash to influencers to gush about the homeyness of cooking with gas.

“#cookingwithgas makes food taste better,” says Camille, an LA-based foodie who poses artfully with her spatula, to her 16,700 followers.

But that’s not what cooking with gas means any more. Now it means wondering about the supply. The sun already provides us with warmth, with light, and via photosynthesis our supper—we have a pretty good psychological relationship with the sun already. When it comes out, we smile. And so the idea that it will happily supply us with all the power we need won’t be a hard sell.

Security fears keep ordinary people awake at night, but also elites. Here’s Frank Elderson, a member of the board of the European Central Bank, writing Tuesday in the bank’s official blog, and in the bloodless language of bureaucrats he says: More sun now:

Europe cannot eliminate geopolitical risk, but it can significantly reduce its exposure to it. The most effective way to do that is by cutting reliance on imported fossil fuels and accelerating an orderly shift to home‑grown clean energy. If Europe were to meet its sustainable energy targets, the link between domestic energy prices and volatile global energy markets would weaken substantially.

Donald Trump has managed to break the two-century-old grip of fossil fuel on the human imagination. As he explained to the GOP House caucus last month, “No other president can do some of the shit I’m doing.”

Understanding why rising electricity demand from data centers is a serious problem requires more than a glance at your latest utility bill. Energy isn’t just one of many inputs into the economy; in effect, it is the economy, since doing anything requires it. Of all the energy used in the US and globally, only a little over 20% is in the form of electricity; the rest entails the direct burning of fossil fuels (most electricity is generated also by burning fossil fuels; in the US, 60% of electricity comes from fossil fuel sources—mostly natural gas). Electricity is not a direct source of energy; it’s an energy carrier. But, for households and industries alike, it is an extremely useful way of conveying energy to end users. Just flip a switch or push a button, and electricity makes something happen. It does many things for us, but its role in enabling communications and data processing gives electricity a pivotal importance in the overall energy mix of modern society.

Energy usage for data processing and communications doesn’t tend to rise and fall in response to short-term changes in power prices; economists call it “inelastic.” So, when electricity prices soar, households and businesses must adjust. For households, that typically means buying fewer discretionary consumer products; for businesses, it means raising prices for services or goods. The whole economy grinds slower. We have a storied history of recessions in 1973, 1979, and 2008 that were related to rising fossil fuel prices impacting the entire economy (see photos of gasoline lines and shortages from 1973). What happened with fossil fuels could happen with electricity: As electricity assumes a central role in our energy system, future price spikes could conceivably be as crippling as the OPEC oil embargoes of the 1970s.

A bursting AI bubble could at least temporarily halt electricity price increases tied to new data centers. But it might be a dreadful “solution,” especially for people who are neither wealthy nor politically connected.

Growing electricity demand for data centers is also a problem because of climate change. Almost all of society’s “progress” in reducing emissions has been in the electricity generation sector (e.g., using solar panels instead of coal to generate electricity). But if electricity demand grows fast, that makes it harder to continue increasing renewables’ share of electricity generation: Demand spikes put utility companies in panic mode, so they deploy any new generating capacity they can quickly obtain—and, so far, they’re resorting to new natural gas turbines more often than new wind projects or solar arrays.

Data centers may be a largely unforeseen disruption to an enormous project that energy planners call the energy transition. As society moves away from fossil fuels, more of its energy usage will occur via electricity—which is the energy output of solar panels, wind turbines, and hydroelectric dams. The transition depends on an ongoing electrification of the economy, starting with electric vehicles. With data centers sucking up so much electricity, it becomes all the harder to deploy electricity to other uses and sectors, which is what planners had been counting on.

Electricity prices can’t keep going up and up. Something’s got to give. Let’s first explore the more obvious solutions to the electricity price dilemma, and then the systemic limits and countervailing trends that will determine which of those solutions is more feasible and likely. I’ll finish by proposing a hybrid supply-demand response that would minimize the economic pain of high electricity prices while putting the country on a more sustainable path.

The obvious solution to rising electricity prices is to meet new demand with new supply. Just generate more power. What energy sources are available for that purpose?

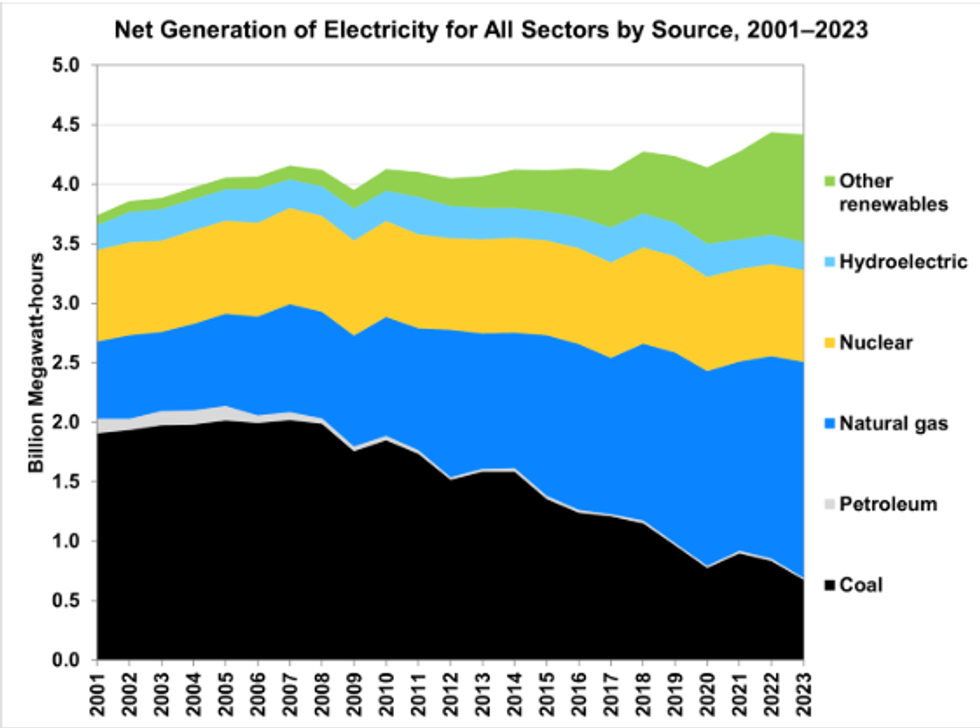

(US electricity generation by energy source, US Department of Energy. The Trump DoE may have stopped updating its data, as its website features no graph carrying these trendlines forward to 2024.)

(US electricity generation by energy source, US Department of Energy. The Trump DoE may have stopped updating its data, as its website features no graph carrying these trendlines forward to 2024.)

None of those supply solutions seems ideal. Moreover, before we try to choose a candidate and say, “Problem solved,” it’s essential that we examine limits and countertrends that could cause the current electricity price trajectory to shift.

US electricity prices could rise even faster, or the current trend could go into reverse and electricity could get cheaper. What are the foreseeable limits or countertrends that could lead to either of those outcomes?

One factor is natural gas prices, which have been relatively low and stable for the past couple of decades; indeed, adjusted for inflation, they have declined significantly. This has been due to rising North American shale gas supplies released by fracking. Cheap natural gas, in turn, has kept US electricity prices relatively stable until recently. Now, however, two factors are contributing to a likely increase in natural gas prices.

The first is the growth of the US liquefied natural gas (LNG) industry. Currently Europe is, for political and security reasons, phasing out Russian natural gas delivered by pipeline. Instead, Europeans are buying more LNG imported by tanker, a costly substitute. Gas producers in the US, flush with shale gas, are eager to serve these new customers, who are willing to pay much more for natural gas than Americans do currently. So, new LNG export terminals are springing up on the US Gulf Coast, with some already shipping their first cargoes. With a growing share of US natural gas being exported (projected to be over 10% of total production by 2030), domestic prices for the fuel will likely rise, forcing gas-burning utility companies to hike up electricity prices further and faster.

When the people own the means of generation, they can collectively decide to promote renewables over fossil fuels as a source of power.

Meanwhile, America’s shale gas miracle may soon start to peter out. As I noted in a recent article, shale gas fields suffer from rapid depletion of individual wells and thus require high rates of drilling. Most US shale gas regions have already passed their peak of production and are in their plateau or decline phase of extraction. One prominent resource analytics firm forecasts that total US shale gas production will peak between 2027 and 2030. If natural gas production falls, it may be difficult for other electricity sources to grow fast enough to avert power supply problems or rate hikes.

A factor that could conceivably slow electricity price increases, or perhaps even cause prices to fall, is investors’ potential unwillingness to further finance the build-out of AI. In recent months, many Wall Street analysts have expressed dismay at the expanding gap between AI spending—projected to hit $1.5 trillion this year—and actual revenues for companies developing and using AI. Many investors now believe AI stocks are a financial bubble whose bursting could cause a recession or depression for the entire US economy, even the global economy.

A bursting AI bubble could at least temporarily halt electricity price increases tied to new data centers. But it might be a dreadful “solution,” especially for people who are neither wealthy nor politically connected. Past financial crises have been stanched with bailouts for banks and investors, thereby transferring wealth from the public to risk-taking entrepreneurs, while ordinary folks deal with job losses and vanishing retirement nest eggs.

Any realistic solution to soaring electricity prices must address both supply and demand.

Supply: Of the sources of energy for electricity generation, renewables make the most sense, even though they are subject to their own limits and drawbacks, including unsustainable requirements for scarce raw materials and major concerns about environmental, social, health, and security impacts.

Demand: Since materials limits mean that electricity generation from renewables cannot be scaled up indefinitely, it is essential that planners identify ways to reduce electricity demand over the long-term.

Investor-owned utilities have an incentive to sell more product so as to generate more profits and returns for investors. Investor ownership is therefore an impediment to stabilizing electricity supply at a sustainable scale over the long run. Fortunately, there are two other ownership models: electric cooperatives and publicly owned utilities. These kinds of power producers currently supply almost 30% of all US electricity, and typically charge their customers less for power.

When the people own the means of generation, they can collectively decide to promote renewables over fossil fuels as a source of power, as my own local provider, Sonoma Clean Power (SCP), already does.

Community-owned power companies can also promote the reduction of electricity demand. For example, SCP incentivizes the purchase of energy-efficient electric appliances, rooftop solar, and EVs. States can also help with demand reduction; for example, the State of California provides rebates for home efficiency measures.

Here’s another demand reduction strategy, one that’s tailored to the specifics of our current dilemma: States and counties could refuse to grant building permits for new data centers. Failing that, they could wall off AI’s rising electricity demand from electricity markets by requiring data center builders to provide dedicated power plants not connected to the grid. Some data center operators are already doing this, though only a tiny minority so far; most of the off-grid generators rely on natural gas.

This strategy will likely face pushback. The Trump administration is working on ways to keep individual states from regulating AI. Further, even if these efforts fail, AI companies can be expected to hire expensive lawyers and lobbying firms to oppose regulations such as a requirement for off-grid power.

But suppose all new data centers do supply their own off-grid generators. If those generators use natural gas, then competition for fuel with grid-tied power plants could raise natural gas prices, again likely causing electricity prices to soar. The best work-around would be to require data centers to build only renewable-energy generators (including deep geothermal). Again, expect pushback.

Altogether, it’s hard to see any of this happening without a broad base of public support, which would in turn require the public to be better informed on energy issues. It would also require leadership from grassroots activists and politicians. It’s a big ask, when there are already plenty of other priorities for problem solvers. However, unless more electric utilities come to be publicly owned, and a large majority of data centers start generating their own off-grid power from renewable sources, electricity price hikes for households and businesses are likely to continue until the AI financial bubble bursts or electricity prices rise enough to cripple the economy.

Electricity is our energy future, but the details of that future are still sketchy. Right now, the picture is being drawn by billionaire investors, but it looks dark and dystopian. Surely more imaginative artists could do better.