SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Now he and his team has enlarged their analysis to include the 21st century’s novel dilemma—that we are steadily and rapidly overheating the planet—and the result is this report, which I read in certain ways as the data-rich companion to Naomi Klein’s 2014 classic This Changes Everything, an investigation of whether it is possible to imagine prosperity without ruinous growth. Much has changed in the years since those volumes—most importantly, the plummeting price of solar and wind energy and of batteries to store that power has opened up a much larger escape hatch. And it’s from that premise that Piketty’s new work really proceeds.

There’s an ever-better case for taxing the hell out of billionaires even if all you do is bury the resulting money in a hole in the ground.

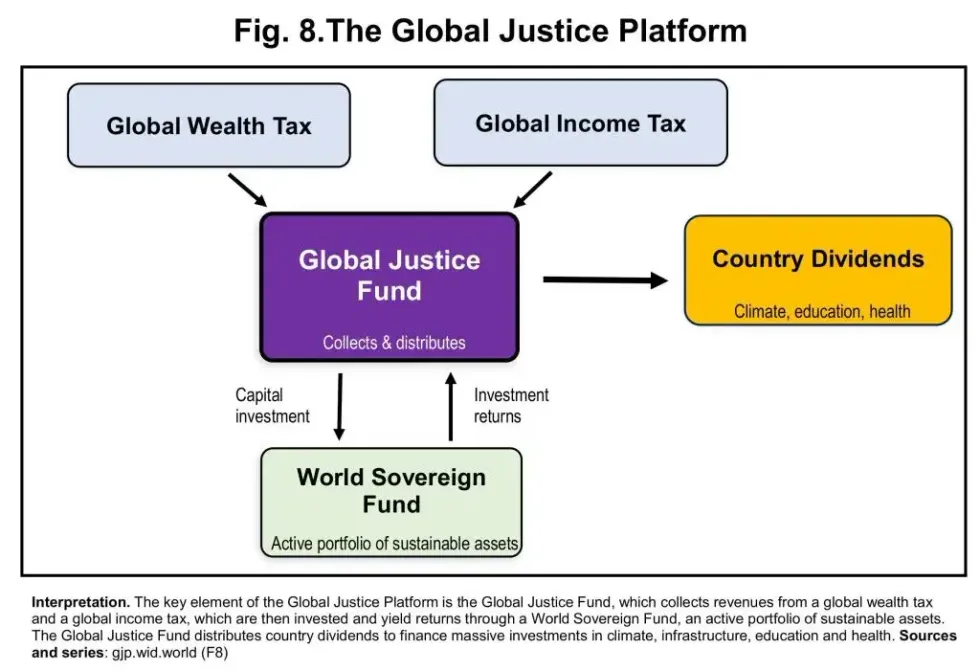

The Global Justice Project says that rapid decarbonization is a must, and that it needs to be paid for by the rich, and that that payment should come in the form of a global wealth tax and a global income tax, which funnel fairly large sums of money from the north to the south. They aim for a “sufficiency” world, in which all have enough and where the share of wealth owned by the richest 1% drops dramatically—a kind of globalized Sweden, I’d say, in which people work half the hours we do at present, and consume more education and healthcare and less stuff. They view it as an alternative to “degrowth” scenarios, and also to our current unrestrained growth model, and say that it leaves the world with lower temperatures than either of those schemes.:

To avoid climate catastrophes, we show that sufficiency is required: a structural transformation of the economy involving shorter working hours, a lower material footprint, a shift from material-intensive sectors toward relatively immaterial sectors such as education and health, and major changes in food systems and land use. Rapid decarbonization of energy systems is also necessary, as is the sharp compression of income and wealth inequality. This compression is both a social justice objective and a condition for financing necessary climate investment and human capital expenditure and for sustaining political support from bottom- and middle-income classes in both the North and the South.

Here’s a little diagram they provide of the basic outline.

I have a certain sympathy for the argument—expressed most pithily by David Roberts on Bluesky—that this kind of sky-castle architecture doesn’t amount to much; I too am more fascinated by the daily drumbeat of technological innovation. And I think that the accumulation of that innovation may undermine part of Piketty’s argument; I have a feeling that the investment required for decarbonization is going to be easier to come by, as the price for good stuff just keeps falling, and the economic logic of paying for fossil fuel becomes ever smaller.

But I also think that the climate crisis is not the only ecological threat we face, nor indeed the only threat period. I think it’s pretty clear that democracy can’t survive inequality; there’s an ever-better case for taxing the hell out of billionaires even if all you do is bury the resulting money in a hole in the ground. One possibility is that the mega rich will succeed in their current project of deliberalizing the planet, and we’ll all get to live in our own nasty little sovereignties; another is that the Bernie Sanderses resident in most parts of the world will figure out how to combine their efforts and that over time we’ll get something that looks a bit like what Piketty (or for that matter Kim Stanley Robinson in Ministry for the Future) imagines. One tell for me that this team is not entirely politically detached came in this paragraph about what would happen if America (or China) predictably refused to join in such a scheme:

If necessary, the Global Justice Platform can be implemented with an incomplete coalition of countries, including the absence of the US and/or China. According to our projections, the climate damages imposed by the US on other countries would be about 3% of world GDP per year, on average, over the 2026-2100 period if the US does not participate in the GJP. Under simplifying assumptions, other countries should impose a corrective tax of approximately 80% on all US exports to collect tax revenues approximately equivalent to the damage. Given the projected decline of the US share in world GDP—from 30% in 1945 to 15% in 2025 and 5-10% by 2100—it is likely that such tariffs would induce the US to join the GJP. The same conclusion applies to the case of China, but with a higher tariff (180% or more).

The report concludes that

A habitable, equal 21st century is materially possible. What stands in the way is not technical impossibility but political choice and the hard but crucial work of building a coalition behind it.

I think that’s a worthy goal to keep in the back of our minds as we proceed with the daily work of building the infrastructure for this new world; every election is a chance to get us a little closer, by electing the kind of people who understand the need for this kind of compression of wealth.

But the infrastructure is the part we can do something about right now, and on that score there’s some equal mix of encouraging maddening news, all of it again on a large scale.

On the one hand, our farcical war in the Gulf continues to serve as the recruiting sergeant for the renewable revolution. As a Bloomberg team reports in a long and important essay, the Gulf War has been “Asia’s Ukraine”:

About two hours from Manila there’s a solar power plant capable of powering 60,000 homes. Surrounded by fields growing okra and eggplant, it had been sitting idle since August, waiting for a connection to the grid—stuck in a queue just like many other renewable energy facilities around the world as power networks struggle to catch up with rising electricity demand.

Then the Iran war cut off the Philippines’ supply of imported liquefied natural gas. Immediately, the government cut fuel taxes and offered free bus rides to the public. Then a few weeks later, as the Strait of Hormuz remained blocked, officials began deploying policies toward a deeper, more structural plan to reduce the country’s dependence on fossil fuels.

One strategy was to fast track more than 30 renewable plants by the end of April. One of those was that 125-megawatt solar plant, built by Citicore Renewable Energy Corp, which is now supplying clean energy to the grid. It is “good timing,” said Joselito Ernst Cañete, operations manager at Citicore, just as electricity demand increases to power air conditioners during the peak summer months.

What happened in the Philppines isn’t an isolated example. With their energy supplies threatened, countries across Asia and Europe have chosen to speed up deployment of renewables and electrification.

Meanwhile, the cheerful solar guru Danny Kennedy chimed in from a conference in Singapore where he found the Western politicians and analysts way behind the Asian curve. I will quote from his account at some length because it’s important:

Philippines. After declaring a national energy emergency in March, the government activated a whole-of-government mandate for energy security. Regulatory bottlenecks for renewables are being dismantled. Rooftop solar inquiries are up 500% since the crisis began. This is not a green ambition. This is a survival response.

Vietnam. The country has revised its power development plan, targeting a minimum of 47% renewable electricity generation by 2030. Vietnam is already the region’s largest EV market, and its government has expanded EV tax incentives in direct response to the Iran War’s impact on fuel prices. HSBC recently extended $4 billion in clean-tech financing to Chinese firms, much of it flowing into EV and solar exports to Vietnam and ASEAN.

Indonesia. Beyond the factory I visited in Batam, the government is engineering a broad fiscal shift—expanding EV incentives with a target of 2 million electric cars and 12 million electric two-wheelers on the road by 2030. With the world’s largest nickel reserves, Indonesia is positioning itself to replace diesel imports with a domestic battery ecosystem. The logic is national sovereignty as much as climate policy. We’ve also talked about their 100GW solar archipelago plans.

Thailand. Advanced its net zero target by 15 full years, to 2050. Solar generation surged 72% in 2025. The country is adding 50 GW of renewables and 14 GW of energy storage by 2037. A major 1 GW module supply deal between China’s GCL-SI and Thailand’s Getz Energy was just signed to support that buildout.

Singapore itself. Already scaled solar to 1.7 GW and is executing multi-gigawatt cross-border subsea clean electricity cables from Indonesia, Cambodia, and Vietnam—with a requirement that developers bundle storage at origin for 24/7 firm power delivery. Singapore, to its credit, is acting. The conference, perhaps, just needed a bigger window.

We already know China and India—the two largest energy consumers in Asia—reached a historic tipping point together in 2025. For the first time, fossil fuel generation fell in both countries simultaneously: China down 0.9%, India down 3.3%. These are not small numbers. These are inflection points.

And yet even as this good news is happening, the Chinese are also beginning to shutter many of the solar panel factories that are at the heart of this revolution, because they’re not making enough money. This is, on the hand, understandable, and on the other entirely maddening—these factories are the single most important industrial asset on Earth—they are factories for lowering the temperature of the Earth. As readers are doubtless painfully aware, I’ve been beating this drum for a good long while, but I’m glad to see others joining in. Adam Tooze, the interesting bricoleur in charge of the Chartbook newsletter, wrote in the FT this week, it would be understandable if we were talking about some mundane commodity like cement:

But solar panels? Since when were solar panels just another commodity? They are a technological miracle. They make us into farmers of the sun. For the past half century, research labs around the world, starting in the 1970s with NASA spin-offs and the big US energy research push under Jimmy Carter, have been straining to reach this point. Together with batteries, which are also rapidly approaching the point of excess supply, they are the key to a sustainable future.

As Tooze points out, it cost China very little in subsidies ($18 billion) to build this behemoth (though one should probably add in the subsidies that, say, Germany provided to its citizens to buy the early models, underwriting the startup of China’s engineering miracle).

I’ve long argued that on a rational world, trying everything it could to head off the worst of global warming, we would “globalize” these factories, running them 24/7 and then piling up the panels on every railroad siding and wharf on the planet so that people could come take them away. This would be, I think, a backdoor way of achieving a fair amount of what Piketty has in mind, far messier than his global scheme but somewhat more plausible. By some calculations, 10 years production from those plants would produce enough panels to provide all the power the world currently uses.

If my sense that the coming El Niño will revive the world’s focus on the climate crisis—well, this is the easiest possible route forward. And it comes not just with more power, but with different power. Elon Musk may be rushing his IPO for data centers in space or whatever the heck he’s currently selling, but some of us will hole up here on Earth, quite sufficient with the solar panels in our yards.