SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"Every day the consequences of GOP healthcare cuts get worse," said one campaigner.

Health insurance companies that offer plans on the Affordable Care Act marketplace are proposing double-digit premium increases for 2027, signaling the second consecutive year of out-of-pocket cost hikes following President Donald Trump and congressional Republicans' refusal to extend enhanced subsidies that lapsed last December.

The health policy research group KFF and the Peterson Center on Healthcare released an analysis on Wednesday showing that ACA marketplace insurers "are proposing a median premium increase of about 14% in 2027." While that would represent a decrease compared to the median finalized premium increase of 20% for 2026, it marks "the second-highest requested rate change since 2018, as premium growth had been relatively flat in this market for several years," the analysis notes.

"If these early indications of median premium increases for 2027 hold, typical premiums for insurers participating in the ACA marketplaces will have jumped by more than one-third over a two-year period," KFF and the Peterson Center found, pointing to the significance of Trump and the GOP's deciseion to oppose an extension of enhanced ACA premiums that were established in 2021 during the Biden administration.

KFF and the Peterson Center explain:

As anticipated, many healthier enrollees left the ACA Marketplaces in 2026 as their subsidies decreased—leading to an average increase in premium payments after subsidies of 58% this year—leaving behind an enrollee base that is on average somewhat sicker and more expensive to cover. For 2026, this dynamic was estimated to drive rates an average of four percentage points higher than they otherwise would have been, and insurers are now building 2027 rates on top of that adjusted, less-healthy risk pool—compounding the effect into next year’s premiums as well.

Leslie Dach, chair of the advocacy group Protect Our Care, said in a statement Wednesday that the analysis underscores "just the latest hit on hard-working families struggling to get by after Republicans ripped away the tax credits that helped millions of Americans afford coverage."

"Every day the consequences of GOP healthcare cuts get worse," said Dach. "This was a deliberate choice by Republicans who took away affordable coverage from millions of people to help fund tax breaks for billionaires and big corporations. The damage is already being felt at kitchen tables across America, and these new premium hikes show the worst is still ahead. And Republicans will pay the political price. Healthcare is already the driving issue leading up to the elections, and as the consequences mount, it will only mobilize voters further.”

Since the start of President Donald Trump's second White House term, ACA enrollment has declined by more than 5 million people as a growing number of Americans are priced out of coverage by surging premiums.

For 2027, at least 20 insurers across states that have submitted rate filings so far have proposed premium increases exceeding 20%, according to the KFF-Peterson Center analysis.

Kendall Witmer, the Democratic National Committee's rapid response director, said in a statement Wednesday that "healthcare is unaffordable for millions of Americans because Donald Trump and Republicans sold them out to give billionaires even bigger tax cuts."

"Working families are already grappling with sky-high prices for groceries and gas, and growing medical bills are putting them over the edge," said Witmer. "Healthcare for Americans has never been more expensive—and Trump and Republicans are squarely to blame."

Leor Tal, campaign director for the advocacy group Unrig Our Ecnomy, echoed those arguments and called for GOP lawmakers, who still control the House and the Senate, to act.

“Millions have already lost access to health insurance, and these planned premium hikes will only escalate this crisis," said Tal.

"We need Republicans in Congress to restore the health care tax credits they took away from millions. Otherwise, when their premiums rise again, Americans will know who is at fault.”

The shortcomings of US healthcare are painfully apparent throughout Rep. Casten’s district, so why won't he co-sponsor the Medicare for All Act?

Ten years ago, when reflecting on his signature legislative achievement, President Barack Obama famously encouraged Americans to think of the Affordable Care Act as a “starter home.” For as much good as the ACA did—expanding coverage to millions, offering policies to people with “preexisting” conditions—it is clear that the foundation of this starter home is starting to crack.

As an emergency medicine physician who has practiced throughout the Chicagoland area for nearly 50 years, I have seen these fault lines up close. Health insurance corporations like Blue Cross Blue Shield and UnitedHealthcare have strayed far from their nonprofit roots, and now routinely delay and deny care for everyday Americans. Put simply, these insurers have an incentive—and even a duty—to skim hundreds of billions of dollars off the top.

Earlier this year, the Chicago City Council recognized this dynamic when it passed a resolution calling for a single-payer national health program, also known as “Medicare for All.”

The resolution passed without objection from any of the city’s 50 aldermen, and concluded by saying council members “enthusiastically support the Medicare for All Act of 2025 and call on our federal legislators to work toward its swift enactment.”

Under a single-payer national health program, Americans would no longer need to worry about what treatments their insurance would cover, what doctors they would be allowed to see, and how much they would be charged out of pocket.

Every representative whose district includes Chicago has already co-sponsored the Medicare for All Act in the US House, and every likely replacement for retiring members of Congress has promised to do the same, with one exception. Rep. Sean Casten (D-Ill.), whose district includes parts of the Garfield Ridge and Clearing neighborhoods west of Midway Airport, has committed to staying in the “starter home,” even though it is coming apart at the seams.

The shortcomings of US healthcare are painfully apparent throughout Rep. Casten’s district, where more than 40,000 of his constituents lacked health insurance before the expiration of enhanced ACA subsidies and the implementation of federal Medicaid cuts. That’s to say nothing of his constituents with sky-high deductibles and limited provider networks who cannot afford to use the coverage they do have.

During my years in the emergency department, I have seen the awful impacts of delayed care. When I practiced at Michael Reese Hospital many years ago, it was distressingly common for me to treat young men with kidney failure. Why? Because their high blood pressure went untreated due to a lack of health coverage to pay for doctor visits and simple medications. They waited until their health issues became unbearable—and much more expensive to treat.

We can do so much better than this, and growing numbers of Americans—including 90% of Democrats in a recent Gallup poll—are starting to demand that we replace our “starter home” with a much more durable healthcare system.

Under a single-payer national health program, Americans would no longer need to worry about what treatments their insurance would cover, what doctors they would be allowed to see, and how much they would be charged out of pocket. I enjoyed a glimpse of this during my 20 years at the Captain James A. Lovell Federal Health Care Center in North Chicago, where I was able to care for veterans, active-duty members of the US military, and their families—without worrying about what their insurance would cover or whether they could afford to pursue treatment.

As Dr. Claudia Fegan, who recently retired as the chief medical officer of Cook County Health, testified before the Chicago City Council, a system like Medicare for All is well within our grasp.

“We already spend enough money on healthcare in this country,” Dr. Fegan said, “we just allow too many people who do none of the work of delivering healthcare to take profit from it. By eliminating the waste and greed of private insurance, we can afford to cover everyone in our country for all necessary care, and end the scourges of surprise bills, skipped medications, and medical bankruptcy.”

Rep. Casten has declined to co-sponsor the Medicare for All Act during his four terms in office, but his position has become increasingly lonely within the Democratic Party, the Illinois Congressional Delegation, and the US medical profession.

Thankfully, it is never too late to do the right thing.

"Privatized Medicare plans are denying patients the care they need, while defrauding the government of billions a year," said one advocacy group. "Donald Trump is giving them even more taxpayer money."

The federal agency now headed by former television host Mehmet Oz announced Monday that it is substantially boosting payments to privately run Medicare Advantage plans, a boon for an industry notorious for overcharging taxpayers and denying patients necessary care.

The Centers for Medicare and Medicaid Services (CMS) said it is jacking up payments to Medicare Advantage (MA) plans by more than 5% for 2026—an increase of over $25 billion. That's more than double the increase proposed by the Biden administration.

Health insurance company stocks jumped in response to the news of the Trump administration's payment hike, with shares of UnitedHealth Group—the largest provider of Medicare Advantage plans—rising more than 6% following the CMS statement.

Oz, whom the Republican-controlled Senate confirmed in a party-line vote last week, previously reported holding tens of millions of dollars worth of stock in companies with interests before CMS, including UnitedHealth.

Social Security Works, a progressive advocacy group that campaigns against Medicare Advantage,

said Monday that "privatized Medicare plans are denying patients the care they need, while defrauding the government of billions a year."

"Trump is giving them even more taxpayer money," the group wrote on social media. "Trump-Musk don't care about 'efficiency.' They care about stealing our money."

"Medicare Advantage is wasteful and inefficient relative to traditional Medicare and everyone knows it."

One industry analyst, Chris Meekins of the financial services firm Raymond James, told Axios that the payment boost for Medicare Advantage "leads one to believe that DOGE"—the Elon Musk-led advisory commission also known as the Department of Government Efficiency—"does not care about MA."

Healthcare writer Natalie Shure

called the payment increase a clear "illustration that this administration's goal is upward wealth distribution and the dismantling of public goods, not 'efficiency.'"

"Medicare Advantage is wasteful and inefficient relative to traditional Medicare," Shure added, "and everyone knows it."

The CMS announcement came weeks after Oz told Sen. Elizabeth Warren (D-Mass.) during his confirmation hearing that he is concerned about and prepared to "go after" Medicare Advantage upcoding, the practice of making patients appear sicker than they actually are to reap larger government payments.

The Wall Street Journal reported Monday that the Trump administration did opt to "stick with a Biden administration policy change that limits certain billing practices that have boosted payments to Medicare Advantage insurers," despite industry objections to the policy.

But Oz's record, including his past support for a proposal dubbed "Medicare Advantage for All," has led watchdog groups to doubt that he intends to aggressively take on large-scale overpayments and fraud in the program. According to one estimate from 2023, Medicare Advantage plans are overcharging U.S. taxpayers by up to $140 billion a year.

Robert Weissman, co-president of Public Citizen, warned after his Senate confirmation that Oz will "seek to further privatize Medicare, increasing the risk that seniors will receive inferior care and further threatening the long-term health of the Medicare program."

"Dr. Oz is joining a team of snake oil salesmen and anti-science flunkies that have already shown disdain for the American people and their health," said Weissman.

In addition to Oz and Robert F. Kennedy Jr. at the Department of Health and Human Services, which oversees CMS, Trump appointed former Medicare Advantage lobbyist Don Dempsey as associate director for health at the Office of Management and Budget, another signal that the administration intends to be an ally to the MA industry.

The provider has—for good reason—become the most powerful lightning rod for patient and medical staff critiques of how private insurers operate.

Healthcare is big business in the United States. So big it can be hard to wrap your head around.

America’s largest healthcare company, the UnitedHealth Group, pulled in over $100 billion in revenue in just the fourth quarter of 2024 alone. For the full year, the giant’s insurance division, UnitedHealthcare, just reported record revenue of $298.2 billion.

These staggering revenue totals actually fell below investor expectations. Right after the announcement, UnitedHealth Group shares slipped 6% on the New York Stock Exchange.

The outpouring of anger after the December killing of UnitedHealthcare CEO Brian Thompson—anger not at the shooting but at the company Thompson represented—shows just how many Americans are currently suffering under our privatized healthcare system.

That tells you a lot about what’s important in the healthcare industry: profit, not care. Health insurance companies in particular can only profit by paying out less in claims than they collect in premiums. And that means denying patients coverage for the care they need.

Just outside the New York Stock Exchange, victims of our for-profit healthcare system—doctors and patients alike—recently braved freezing temperatures to call out the suffering that engineered UnitedHealth’s exorbitant earnings.

One of those demonstrators, Jenn Coffey, has been battling complex regional pain syndrome (CRPS), a condition so incredibly painful that it’s often called the “suicide disease.”

UnitedHealth denied her the prior authorization needed to have her critically important treatment adequately covered. “UnitedHealthcare would rather leave me in torture than grant me the peace my infusions bring,” says Coffey. “I’m asking for a life worth dignity. I’m left begging for a life worth living.”

Several other speakers shared their deeply personal experiences with a healthcare system that far too often treats patients as disposable.

Dr. Toutou Moussa Diallo, a New York-based researcher and healthcare activist, detailed how insurance denials led to subpar treatment for his broken ankle that only made the initial injury more debilitating. Nephrologist Cheryl Kunis shared the story of a patient who died after UnitedHealthcare refused to cover a PET scan of a malignant neck tumor.

These experiences amount to much more than isolated one-off incidents. The outpouring of anger after the December killing of UnitedHealthcare CEO Brian Thompson—anger not at the shooting but at the company Thompson represented—shows just how many Americans are currently suffering under our privatized healthcare system.

The ongoing campaign protesting how UnitedHealth does business began well before Thompson’s headline-grabbing killing. The Care Over Cost mobilization, led by People’s Action, has been organizing rallies protesting America’s biggest private insurers for years.

UnitedHealth has—for good reason—become the most powerful lightning rod for patient and medical staff critiques of how private insurers operate. The company’s gargantuan profits rest on decisions that regularly exploit patients at every opportunity.

Just a few snippets from recent news accounts offer a vivid picture about how UnitedHealth goes about making its billions.

UnitedHealth Group’s pharmacy benefit manager, Optum RX, marked up some cancer treatments by over 1,000%. UnitedHealthcare systematically limited access to critical treatments for children with autism to cut costs. And along with two other insurers, the company intentionally denied nursing care to patients covered by Medicare Advantage—all to maximize profit.

And how has the UnitedHealth Group been spending all its ill-gotten gains? One telling stat: UnitedHealth Group CEO Andrew Witty pocketed an astonishing $23.5 million in 2023 compensation.

As the rally in front of the New York Stock Exchange ended, protesters called on UnitedHealthcare to publicly release its claim denial rates, oppose federal tax cuts that would result in Medicaid service reductions, and end the company’s care-denying prior authorization requirements.

Those eminently reasonable demands for the company. Meanwhile, the rest of us should consider whether we want healthcare to be a tool for the public good—or just private profit.

"It is totally fair for people to identify private insurers as the key bad actor in our current system," writes Matt Bruenig of the People's Policy Project. "The quicker we nationalize health insurance, the better."

Last week's murder of UnitedHealthcare CEO Brian Thompson brought to the surface a seething hatred of the nation's for-profit insurance system—anger rooted in the industry's profiteering, high costs, and mass care denials.

But that response has led some pundits to defend private insurance companies and claim that, in fact, healthcare providers such as hospitals and doctors are the real drivers of outlandish U.S. healthcare costs.

In an analysis published Tuesday, Matt Bruenig of the People's Policy Project argued that defenders of private insurers are relying on "factual misunderstandings and very questionable analysis" and that it is reasonable to conclude that the for-profit insurance system is "actually very bad."

"From a design perspective, the main problem with our private health insurance system is that it is extremely wasteful," Bruenig wrote, estimating based on existing research that excess administrative expenses amount to $528 billion per year—or 1.8% of U.S. gross domestic product.

"All healthcare systems require administration, which costs money, but a private multi-payer system requires massively more than other approaches, especially the single-payer system favored by the American left," Bruenig observed, emphasizing that excess administrative expenses of both the insurance companies and healthcare providers stem from "the multi-payer private health insurance system that we have."

He continued:

To get your head around why this is, think for a second about what happens to every $100 you give to a private insurance company. According to the most exhaustive study on this question in the U.S.—the CBO single-payer study from 2020—the first thing that happens is that $16 of those dollars are taken by the insurance company. From there, the insurer gives the remaining $84 to a hospital to reimburse them for services. That hospital then takes another $15.96 (19% of its revenue) for administration, meaning that only $68.04 of the original $100 actually goes to providing care.

In a single-payer system, the path of that $100 looks a lot different. Rather than take $16 for insurance administration, the public insurer would only take $1.60. And rather than take $15.96 of the remaining money for hospital administration, the hospital would only take $11.80 (12% of its revenue), meaning that $86.60 of the original $100 actually goes to providing care.

High provider payments, which some analysts have suggested are the key culprit in exorbitant healthcare costs, are also attributable to the nation's for-profit insurance system, Bruenig argued.

"Medicaid and Medicare are able to negotiate much lower rates than private insurance, just as the public health insurer under a single-payer system would be able to. It is only within the private insurance segment of the system that providers have been able to jack up rates to such an extreme extent," he wrote. "Given all of this, I think it is totally fair for people to identify private insurers as the key bad actor in our current system. They are directly responsible for over half a trillion dollars of administrative waste and (at the very least) indirectly responsible for the provider rents that are bleeding Americans dry."

"The quicker we nationalize health insurance," he concluded, "the better."

Bruenig's analysis comports with research showing that a single-payer system such as the Medicare for All program proposed by Sen. Bernie Sanders (I-Vt.), Rep. Pramila Jayapal (D-Wash.), and other progressives in Congress could produce massive savings by eliminating bureaucratic costs associated with the private insurance system.

One study published in the Annals of Internal Medicine in January 2020 estimated that Medicare for All could save the U.S. more than $600 billion per year in healthcare-related administrative costs.

"The average American is paying more than $2,000 a year for useless bureaucracy," said Dr. David Himmelstein, lead author of the study, said at the time. "That money could be spent for care if we had a Medicare for All program."

Deep-seated anger at the systemic and harmful flaws of the for-profit U.S. insurance system could help explain why the percentage of the public that believes it's the federal government's responsibility to ensure all Americans have healthcare coverage is at its highest level in more than a decade, according to Gallup polling released Monday.

"There's a day of reckoning that is happening right now," former insurance industry executive Wendell Potter, president of the Center for Health and Democracy, said in an MSNBC appearance on Monday. "Whether we're talking about employers, patients, doctors—just about everybody despises health insurance companies in ways that I've never seen before."

"Private insurance companies, including Medicare Advantage plans, are designed to generate profit. How do they do that? Take our money and then deny our care."

A pair of new stories examining the increasingly common but shadowy U.S. insurance industry practice of refusing to pay for certain treatments drew outrage Wednesday from patient advocates and Medicare for All proponents, who said the reporting further reveals the harms of for-profit healthcare.

The investigative outlet ProPublica focused its attention on the "galling" secrecy around insurance companies' claim denials, which frequently leave patients with massive medical bills and little clarity as to why their claims were rejected.

"How often insurance companies say no is a closely held secret," ProPublica's Robin Fields reported. "There's nowhere that a consumer or an employer can go to look up all insurers' denial rates—let alone whether a particular company is likely to decline to pay for procedures or drugs that its plans appear to cover."

"In 2010, federal regulators were granted expansive authority through the Affordable Care Act to require that insurers provide information on their denials. This data could have meant a sea change in transparency for consumers," Fields added. "But more than a decade later, the federal government has collected only a fraction of what it’s entitled to. And what information it has released, experts say, is so crude, inconsistent, and confusing that it's essentially meaningless."

The data that is available indicates claim denials are on the rise. According to a February KFF study of Affordable Care Act plans, "nearly 17% of in-network claims were denied in 2021."

Elisabeth Rosenthal of KFF Health News wrote in a column last month that declining to pay for patients' treatments is "a handy way for insurers to keep revenue high."

"Millions of Americans in the past few years have run into this experience: filing a healthcare insurance claim that once might have been paid immediately but instead is just as quickly denied," Rosenthal wrote. "If the experience and the insurer's explanation often seem arbitrary and absurd, that might be because companies appear increasingly likely to employ computer algorithms or people with little relevant experience to issue rapid-fire denials of claims—sometimes bundles at a time—without reviewing the patient's medical chart. A job title at one company was 'denial nurse.'"

ProPublica noted Wednesday that "some advocates say insurers have a good reason to dodge transparency."

Citing Wendell Potter, a former Cigna executive who now supports Medicare for All, ProPublica reported that "refusing payment for medical care and drugs has become a staple of their business model, in part because they know customers appeal less than 1% of denials."

"That's money left on the table that the insurers keep," Potter told the outlet.

With their companies' profits booming, the CEOs of the top seven private health insurance giants in the U.S. took home a combined $335 million in compensation last year.

Medicare Advantage providers—private insurers paid by the federal government to cover patient care—have become notorious for denying claims for medically necessary treatments as enrollment in the program continues to surge.

As The Lever's Matthew Cunningham-Cook reported Wednesday, "Medicare Advantage insurers are threatening the foundational premise of the government's healthcare safety net for seniors and people with disabilities: that people in Medicare should get the care that is recommended by a doctor."

"A 2022 investigation by the inspector general of the Department of Health and Human Services found that in 2019, 13% of the total prior authorization requests denied by Medicare Advantage plans would have been covered under traditional Medicare, leading to an estimated 85,000 additional care denials," Cunningham-Cook wrote. "That year, Medicare Advantage plans also wrongly denied 18% of payment claims—covering an estimated 1.5 million claims—reducing the likelihood that doctors will recommend the costliest yet often most effective care, for fear of not being paid."

Social Security Works, a progressive advocacy group that backs Medicare for All, tweeted in response to the new reporting Wednesday that "private insurance companies, including Medicare Advantage plans, are designed to generate profit."

"How do they do that? Take our money and then deny our care," the group added.

Cunningham-Cook opened his piece with the story of Jenn Coffey, a former Republican state representative in New Hampshire "who, like many GOP faithfuls, believed private insurers could solve the healthcare crisis if they were allowed to do things like sell policies across state lines."

But Coffey's views were shaken when UnitedHealth, her ultra-profitable Medicare Advantage provider, "constantly rejected or second-guessed the care options her doctors suggested for her cancer recovery and for a rare and painful secondary disease that has no standard treatment plan," Cunningham-Cook reported.

“Now I've realized that you can't fix or repair the system,” Coffey told The Lever. "The insurance companies don't offer anything. They serve as a roadblock."

"The only way forward," she added, "is Medicare for All."

UnitedHealth CEO Andrew Witty told investors he "appreciates" the Biden administration's decision to slow the implementation of its Medicare Advantage reforms.

The chief executive of UnitedHealth Group told investors Friday that he "appreciates" the Biden administration's decision to more slowly implement its crackdown on overbilling in Medicare Advantage, a privately run, government-funded program that the Minnesota-based insurance behemoth touted as a key profit driver in its newly released first quarter earnings report.

UnitedHealth, one of the largest Medicare Advantage providers in the U.S., reported $91.9 billion in revenue for the first three months of 2023—15% growth year-over-year—and more than $8 billion in earnings from operations, exceeding analysts' expectations.

UnitedHealthcare, UnitedHealth Group's insurance business, "is pacing strongly to its outlook for another year of market-leading growth in serving more people through its Medicare Advantage offerings," the company said in its earnings release. The company said Friday that it added 655,000 new Medicare Advantage members in the first quarter of the year.

UnitedHealth's earnings report came after the company helped lead an aggressive lobbying campaign against new Biden administration rules aimed at limiting Medicare Advantage insurers' ability to overcharge the federal government by making patients appear sicker than they actually are.

According to The New York Times, UnitedHealth CEO Andrew Witty appeared on Capitol Hill in person to lobby against the proposed changes, which the lucrative Medicare Advantage industry falsely characterized as cuts to the program that now provides insurance to nearly half of the overall Medicare population.

Late last month, the Centers for Medicare and Medicaid Services (CMS) offered a number of concessions to the industry, agreeing to impose its policy changes over a period of three years instead of all at once and boosting Medicare Advantage payment rates by more than expected.

As STAT reported last week, Wall Street investors were "overjoyed" by the Biden administration's move, which drew criticism from progressive lawmakers and healthcare analysts who warned the slow phase-in will allow Medicare Advantage plans to continue their abusive practices. UnitedHealth, like other Medicare Advantage insurers, has been accused of wrongfully denying or attempting to deny patients necessary care, in some cases utilizing artificial intelligence to determine when to end coverage.

When it comes to excess billing, CMS recently estimated that overpayments to Medicare Advantage totaled $11.4 billion in fiscal year 2022—a significant drain on the Medicare trust fund.

Citing one industry analyst, STAT noted that UnitedHealth could reap $900 million in additional profit next year alone thanks to the administration's decision to delay full implementation of the reforms.

In an analysis published in February, former insurance executive Wendell Potter noted that UnitedHealth is one of just seven large for-profit insurance companies that now control 70% of the Medicare Advantage market, which is dependent on taxpayer money.

According to Potter, who now heads the Center for Health and Democracy, insurance giants UnitedHealth, Cigna, CVS/Aetna, Elevance, Humana, Centene, and Molina saw their combined revenues from taxpayer-supported programs grow 500% between 2012 and 2022.

"They've essentially been bailed out by taxpayers," Potter said of for-profit insurance giants like UnitedHealth in a recent interview with The American Prospect. "And members of Congress, and various administrations, have been just standing on the sidelines, not paying attention to what's been going on."

"Robots should not be making life-or-death decisions," said healthcare campaigner Ady Barkan.

Sen. Elizabeth Warren joined healthcare campaigner Ady Barkan and others on Monday in sounding alarm over a recent investigation showing that Medicare Advantage insurers are using unregulated artificial intelligence systems to determine when to end payments for patients' treatments, a practice that has prematurely terminated coverage for vulnerable seniors.

STAT reported earlier this month that while "health insurance companies have rejected medical claims for as long as they've been around," AI is "driving their denials to new heights in Medicare Advantage," a privately run program funded by the federal government.

"Behind the scenes, insurers are using unregulated predictive algorithms, under the guise of scientific rigor, to pinpoint the precise moment when they can plausibly cut off payment for an older patient's treatment," the outlet found. "The denials that follow are setting off heated disputes between doctors and insurers, often delaying treatment of seriously ill patients who are neither aware of the algorithms, nor able to question their calculations."

"Older people who spent their lives paying into Medicare, and are now facing amputation, fast-spreading cancers, and other devastating diagnoses, are left to either pay for their care themselves or get by without it," STAT continued. "If they disagree, they can file an appeal, and spend months trying to recover their costs, even if they don't recover from their illnesses."

Barkan, co-executive director of Be a Hero and an ALS patient who is acutely aware of the injustices at the heart of the United States' for-profit healthcare system, tweeted Monday that STAT's reporting is "outrageous and terrifying" and circulated a petition imploring the Biden administration to crack down on the Medicare Advantage industry's use of AI.

"This barbaric practice must end," the petition states. "We're calling on President Biden and the [Centers for Medicare and Medicaid Services] to stop this practice immediately."

Warren (D-Mass.), who blasted the huge profits of top Medicare Advantage insurers last week, echoed Barkan in a tweet of her own.

"Medicare Advantage insurers make patients look as sick as possible to overcharge taxpayers billions," Warren wrote, referring to a common industry practice known as upcoding.

"At the same time, they deny seniors and people with disabilities care—with the help of AI algorithms," the senator continued. "We must crack down on these abuses. No more #DeathByAI."

An analysis published last year in the Journal of Medical Internet Research found that "despite the plethora of claims for the benefits of AI in enhancing clinical outcomes, there is a paucity of robust evidence."

But that lack of evidence hasn't stopped hugely profitable private healthcare companies from increasingly using AI tools to "help make life-altering decisions with little independent oversight," STAT determined after reviewing secret corporate documents and hundreds of pages of federal records and court filings.

"Over the last decade, a new industry has formed around these plans to predict how many hours of therapy patients will need, which types of doctors they might see, and exactly when they will be able to leave a hospital or nursing home," STAT reported. "The predictions have become so integral to Medicare Advantage that insurers themselves have started acquiring the makers of the most widely used tools."

"Elevance, Cigna, and CVS Health, which owns insurance giant Aetna, have all purchased these capabilities in recent years," the outlet continued. "One of the biggest and most controversial companies behind these models, NaviHealth, is now owned by UnitedHealth Group."

"President Biden has the power to stop this. We're meeting with White House staff this week to discuss this outrage."

In 2020, a UnitedHealthcare algorithm determined that 89-year-old Dolores Millam—who broke her leg in a fall that year—would only need to stay in a nursing home for 15 days following surgery, STAT reported.

After the 15 days were up, Millam "received notice that payment for her care had been terminated." Millam's daughter, Holly Hennessy, told STAT that "she couldn't fathom UnitedHealthcare's conclusion that her mother unable to move or even go to the bathroom on her own—no longer met Medicare coverage requirements."

"Hennessy said she had no choice but to keep her mother in the nursing home, Evansville Manor, and hope the payment denial would get overturned," STAT reported. "By then, the bills were quickly piling up."

UnitedHealthcare rejected Millam and Hennessy's appeal, forcing them to pursue relief in federal court—an arduous process.

A federal judge finally ruled months later that UnitedHealthcare improperly denied Millam that she was entitled to full coverage.

The total bill for her nursing home stay was $40,000, according to STAT.

Barkan warned Monday that "insurance behemoths using AI to squeeze every cent out of us." Just seven healthcare companies control more than 70% of the Medicare Advantage market.

"President Biden has the power to stop this," Barkan wrote of Medicare Advantage plans' use of AI. "We're meeting with White House staff this week to discuss this outrage."

Private insurance giants are offering luxury vacations and other incentives for agents to "push seniors into the most expensive Medigap plans," the Massachusetts senator found.

Democratic Sen. Elizabeth Warren released a report Wednesday highlighting the splashy incentives—from luxury vacations to cash bonuses—that private insurance companies offer agents and brokers for enrolling seniors in potentially higher-cost Medigap plans.

Medigap is federally regulated supplemental health insurance offered by for-profit companies such as UnitedHealthcare, Humana, and Aetna.

According to Warren, the Medigap marketplace is rife with "incentive trips and other perks for brokers and agents" who—in pursuit of such rewards—could be motivated to "push seniors into the most expensive Medigap plans, regardless of whether those plans meet their needs."

The senator found that the estimated 32 private companies that entice agents with vacations and other incentives to boost Medigap sales provided the supplemental insurance to around 6.6 million people in the U.S. in 2021 and raked in nearly $16 billion in premiums from beneficiaries that year.

Warren acknowledged that her report "may underestimate the prevalence of incentives and rewards in the Medigap insurance industry" given that insurers and third-party companies are often not transparent about their incentive practices.

In a statement, Warren lamented the weak federal and state regulations that are giving insurance giants "free rein to scam millions of seniors in Medigap, offering agents lavish vacations to steer unknowing beneficiaries into more expensive plans."

"Regulators must act to make sure seniors aren't getting fleeced," said Warren, who noted that around 40% of Medigap enrollees had less than $40,000 in annual income in 2018.

The senator's report highlights several specific examples of the kinds of perks agents and brokers are being offered to peddle Medigap plans, which are often used to supplement traditional Medicare coverage.

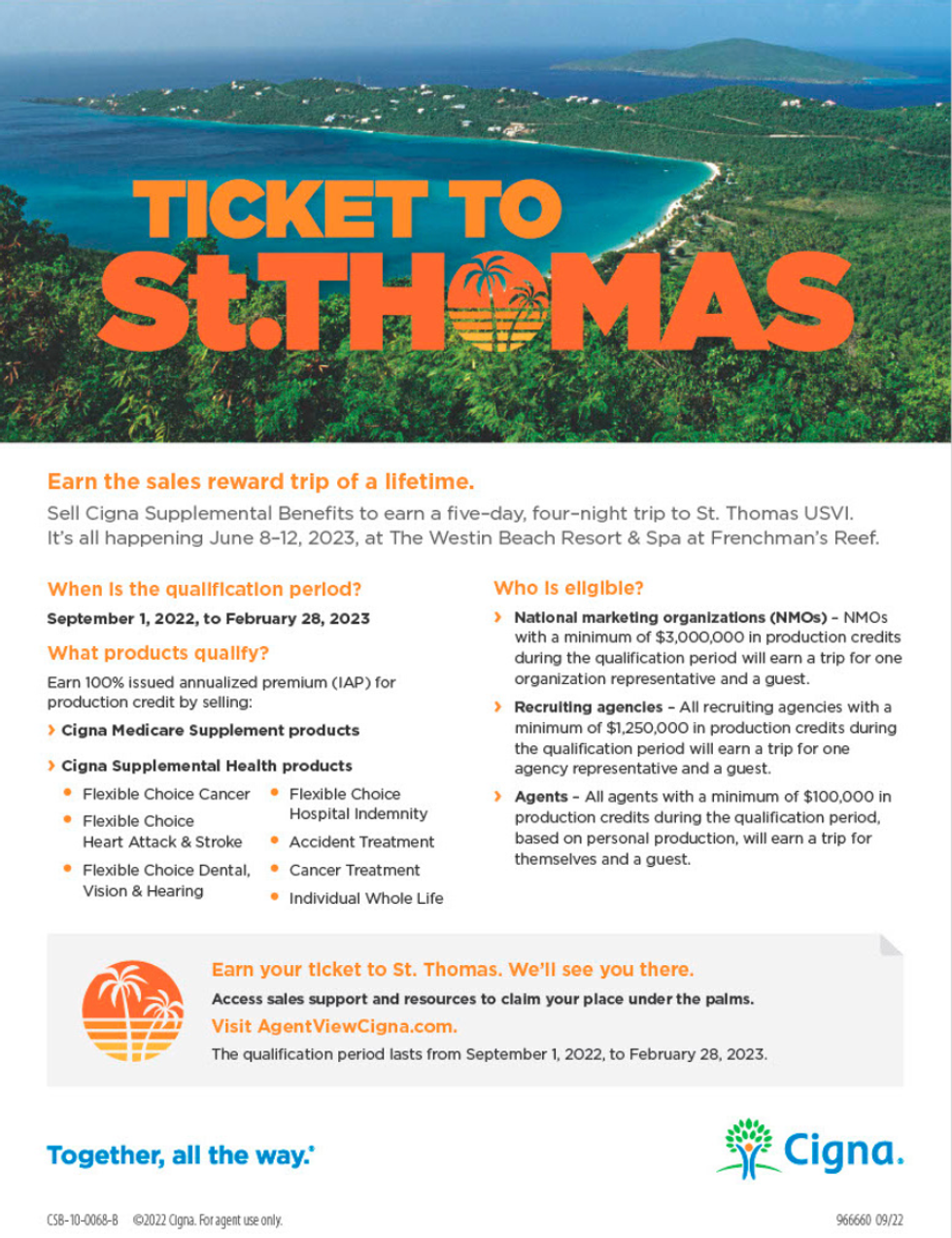

"Mutual of Omaha offered brokers and agents selling Medigap plans this year a chance to earn a 'Sunny San Diego trip' that included 'airfare, one double-occupancy standard hotel room, two hosted receptions, cash allowance, and airport transfers for two people,'" the report notes. "Cigna is currently offering brokers and agents the chance to 'earn the sales reward trip of a lifetime' to St. Thomas, U.S. Virgin Islands for sales made between September 2022 and February 2023."

Seniors receive much of their information about Medigap plans—which vary widely in price—from insurance agents motivated by undisclosed incentives, Warren's report notes, a dynamic that could be leading unsuspecting seniors to purchase higher-premium plans that they believe are best suited to their individual needs.

"Sales agents must meet certain thresholds to qualify for vacations—for example, agents must sell $250,000 worth of coverage to qualify for Mutual of Omaha's vacation rewards," the report states. "Therefore, to meet that minimum threshold, there is a clear incentive structure to sell more expensive plans. This sets up a clear conflict of interest for agents in cases where the best option for seniors might be the least expensive plan."

A separate study published last week by the Commonwealth Fund came away with similar findings. "According to brokers and agents," the study notes, "the commission structure of Medigap plans incentivizes the sale of plans charging high premiums."

Warren attached her report to a letter urging Centers for Medicare and Medicaid Services Administrator Chiquita Brooks-LaSure and the head of the National Association of Insurance Commissioners to "act as quickly as possible to end health insurers'

promises of lavish vacations and other incentives to insurance agents and brokers in exchange for selling Medigap plans to seniors."

"This practice represents an abuse of the trust that seniors place in Medicare. Medigap insurance is not federally subsidized, but the terms and conditions under which Medigap plans are offered are regulated by CMS and state insurance regulators," Warren wrote. "Nowhere does CMS indicate that agents who sell these products may receive lavish vacations and other valuable perks in exchange for these sales."

"Regulators must act to close these loopholes," she added.

In this column, I've written extensively about anti-poverty policy. I've underscored the importance of minimum wages and work support, including child care and wage subsidies, SNAP (food stamps), housing, and health care. I've often stressed the critical role of criminal justice reform. I never shut up about the benefits of full employment.

But I've never said a word about reproductive rights.

I have long supported such rights. I've long recognized the decline in teenage pregnancy, particularly among poor girls, as an essential advance for social policy (see Belle Sawhill's work on access to contraception and its positive impacts on child/parent outcomes). But I've failed to connect the dots between access to comprehensive reproductive health care, including abortion, and economic security.

Thankfully, those dots are compellingly connected in this report from last year, "Two Sides of the Same Coin, Integrating Economic and Reproductive Justice." If you think the connection should be obvious, I agree. Having a child is much more than an economic event; it's also very much that, invoking significant direct costs and opportunity costs (and benefits, too, of course). Thus, the inability to control such costs due to lack of access to reproductive health care is a potentially poverty-inducing problem for low-income women and their families (and 69 percent of those who seek abortions are low-income). Conversely, increasing use of the birth control pill, for example, has been found to reduce the gender pay gap significantly.

I was particularly struck by the findings from a research project in progress called the Turnaway Study, a longitudinal study that follows women who sought but did not get abortions, comparing their outcomes to economically similar women who were able to access abortion services. This quasi-experimental study design is a good way to get closer to causal impacts versus correlations.

A key finding from the Turnaway Study in the economic security space is that relative to women who were able to get the abortion they sought, women denied an abortion were three times more likely to be poor. A year after they were turned away, these women were 10 percent less likely to be working full-time (58 versus 48 percent), and 76 percent of them received public assistance, compared to 44 percent of women who were able to access abortion.

These findings match up to the facts as to why women seek abortions. It's not often because they don't want to have kids; 60 percent of women who have abortions are raising children; of those turned away, 29 percent cited their need to focus on their other kids as the reason they were seeking an abortion. Once again, it's often economics: "Women typically cite multiple interrelated reasons for seeking an abortion, but the most common theme that arose in the Turnaway Study was not feeling financially prepared (40 percent), meaning that they had general financial concerns, were unemployed or underemployed, were uninsured or could not get welfare, or did not want government assistance."

Another reason why it's so essential for progressives to add reproductive access to our anti-poverty agenda is that public policy is pushing hard in the wrong direction, making abortions more costly and more complicated to find. Along with the publicized attack on Planned Parenthood, many states are making it harder for clinics that serve low-income women to stay open, such that abortion seekers stuck in those areas now face potentially high travel costs. In addition, restrictions on both public (Medicaid) and private insurance translate into significant out-of-pocket expenses. More than half of the women in the Turnaway Study (56 percent) who got abortions spent more than a third of their monthly income on the procedure and for travel.

As I was working on this piece, I happened to read an article about the restrictive Texas abortion case to be heard this week in the Supreme Court. The article told the story of an administrative assistant from Texas who, because of the state's aggressive attack on abortion access, had to take out a payday loan to fly to California to be able to schedule an abortion. She noted, "I took out a payday loan, which put me in debt for a little bit. But I think about women in the Panhandle or the [Rio Grande] Valley. Can they get on a plane, fly 1,500 miles away, and get an abortion? No."

In other words, this is not some hypothetical problem. It's real, and it's happening every day, which is why the "Two Sides" report concludes the following:

Anyone who wishes to advance the economic security of women and their families will not be able to do so effectively without integrating access to reproductive health care into a proactive policy agenda to achieve economic equality for women.

I think that's right. That means pushing back on state and federal laws limiting access and increasing costs, including insurance restrictions, like the Hyde Amendment. It means protecting the advances we've made under health reform regarding contraceptive coverage. It means fully funding and supporting family planning initiatives through Title X, including Planned Parenthood.

For low-income women to be able to take control of their economic lives, they must be able to access affordable, comprehensive reproductive health, including contraception and abortion. An anti-poverty agenda that fails to recognize that reality is woefully incomplete.