5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

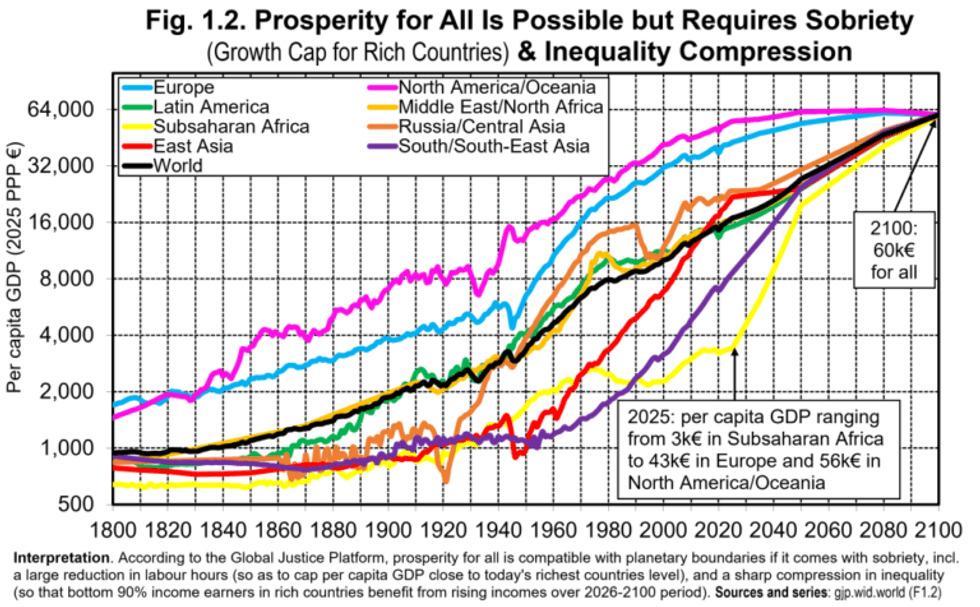

The core aim of the proposal is to achieve full income convergence across all countries by 2100, centered around a target level of €5,000 (about $5,700) per month for every person. To achieve this, the bottom 50% of humanity need to increase their global wealth share from 2-30%. The top 0.001%, in contrast, would see their wealth fall from 6% to 0.05%—a "striking redistribution," to quote the report, which would essentially abolish the billionaire class.

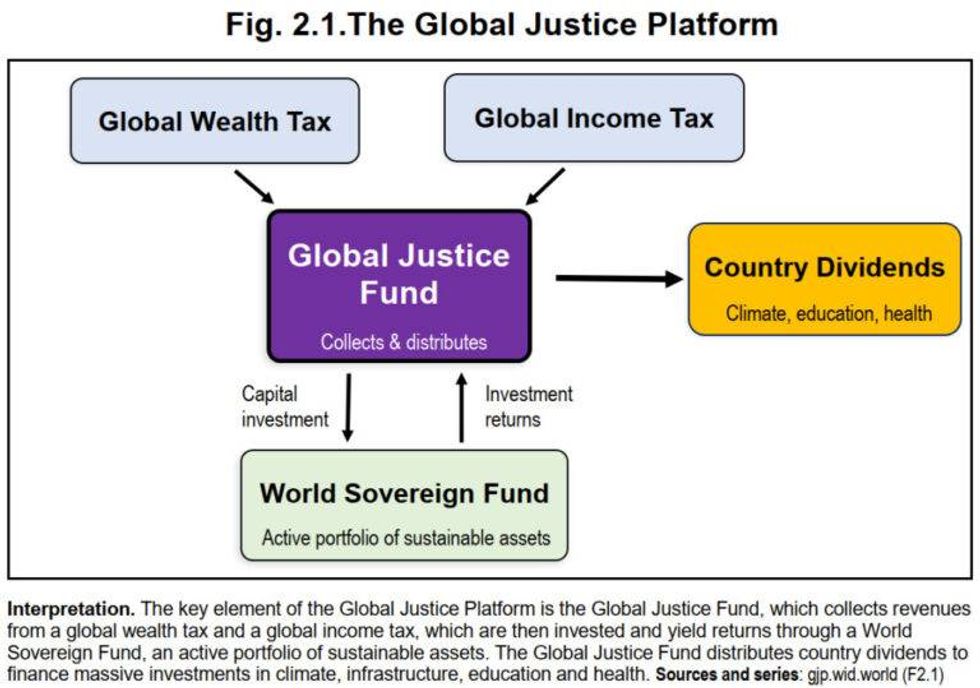

A Global Justice Fund serves to administer this immense effort at international economic sharing, financed by a global wealth tax and a top income tax levied on the richest 1% of the world’s population. Some of the revenue raised would go into a World Sovereign Fund, which is projected to accumulate assets equivalent to 60% of world GDP and replace tax revenue as the main source of financing. Country dividends are designed to be distributed on an equal per-capita basis, therefore providing more resources to poorer than richer countries and vastly more resources than currently allocated to development aid. These funds also come with strong conditionalities in terms of climate investments, inequality targets, and health and education expenditures.

The main novelty of the report is to put the concept of sufficiency at the center of its analysis, rightly arguing that we cannot stay within a 2°C carbon budget if the entire human population adopts a rich-world lifestyle of high private consumption. Sufficiency, as the report defines it, therefore requires more than halving average working time to 1,000 hours, roughly the equivalent of a two-and-a-half-day standard week.

This needs to be accompanied by a significant shift from material to immaterial sectors, such as health and education, which in turn would help refocus the economy toward low-consumption activities. A substantial change in food habits and reduced meat consumption could also allow for a strict deforestation ban, freeing up arable land while scaling down high-emitting agricultural practices. At the same time, sufficiency in production and consumption patterns must be combined with rapid decarbonization of the energy system, as spurred and enabled by the Global Justice Fund.

All this can read, at times, as a wish list of sustainability concepts and policies long espoused by environmental thinkers. But the work of the Global Justice Project is far wider in scope than Piketty’s best-selling tome, Capital in the 21st Century, which famously used vast historical and economic data to argue the case for a progressive global tax on wealth. Back in 2015, we at Share the World's Resources and others criticized the book for failing to take seriously the ecological limits to growth and planetary boundaries. So it’s inspiring to see the World Inequality Lab authors directly engaging in this debate, fully denouncing the rhetoric of "green growth" that assumes we can address environmental challenges by indefinitely increasing the size of the pie without reducing inequality, consuming less, or sharing resources globally.

Their new report argues that technology alone is not enough to achieve rapid decarbonization. They acknowledge that to manage the green transition globally within a strict carbon budget, it will be necessary for today’s richest countries to radically downscale their resource and energy demands with near-zero growth in GDP. This will clear the ecological and carbon space needed for poorer countries of the Global South to continue growing their economies, enabling a fast energy transition while guaranteeing essential public services and a decent standard of living to all people.

It is hardly a novel framing of the issue, but the report emphasizes how their Sustainable Convergence Scenario entails a form of "class-based reparatory justice," in that the very rich—who have benefited the most from fossil-based global economic growth in recent decades—will primarily fund the Global Justice Platform. What’s more, the proposal is somewhat aligned with the concept of climate equity, and effectively translates the principle of "common but differentiated responsibilities" into quantitative policies for addressing climate change.

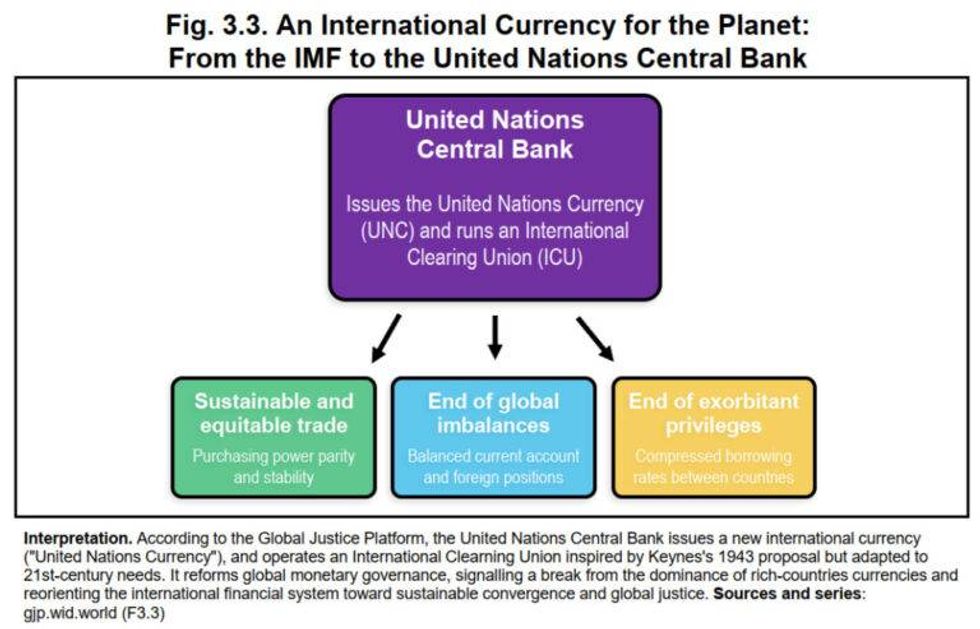

Another strength of the report is how it connects macroeconomic and environmental projections directly to questions of international institutional reform. It centrally highlights the need for a broader overhaul and democratization of the global economic and monetary system, including the reconstitution of the International Monetary Fund into a United Nations Central Bank that issues its own reserve currency. This would eliminate the exorbitant privilege of the US dollar and other major currencies that can borrow at much lower rates, ending a massive reverse redistribution of wealth from Global South countries to the Global North.

All other international institutions would be governed by strict rules and equal voting rights, further eradicating the special privileges and veto powers of dominant nations. A new international order would include the reform of World Trade Organisation rules and a reset of dispute settlement mechanisms. And the large financial resources allocated to the Global Justice Fund would de facto underwrite a major restructuring of the entire UN system, strengthening its many agencies, human rights protections and international laws.

As the report affirms, these proposals to transform global governance from "plutocracy to democracy" are closely related to many other existing frameworks and initiatives. The Bridgetown Initiative in 2022, for example, also stresses the complementary role of global wealth taxation and international monetary reform. The UN Tax Convention process also focuses on democratizing the international tax system and curbing illicit financial flows, while the G20 initiatives led by Brazil and South Africa also champion global wealth taxes to fund climate policies and green energy transitions.

There are numerous other networks and organizations that aim toward similar tax and governance reforms, such as the work of Progressive International with their Program of Action on the Construction of a New International Economic Order. The Stiglitz Commission of 2010 and Brandt Commission of 1980 are gladly cited by the Global Justice Report as complementary discussions surrounding the reform of the international monetary and reserve system.

Above all, the report authors deservedly mention the Roadmap for Eradicating Poverty Beyond Growth—a major project coordinated by the former UN Special Rapporteur on Extreme Poverty and Human Rights, Olivier De Schutter, that puts forward an exhaustive policy toolkit for building a global economy with human rights and ecological justice at its core. Thomas Piketty and many other prominent economists have put their names to this plan, which is one of the most comprehensive policy documents of recent years to define "living well within planetary boundaries" through increased South-South cooperation, reparative climate finance, and support for universal social protection floors. De Schutter’s pioneering proposal for a Global Fund for Social Protection is arguably a less utopian prospect for closing chronic financing gaps in low-income countries, building upon existing structures like the UN’s International Labour Organisation, and seeking more immediately viable sources of international financing.

The operative question, as always, is how the political conditions will arise to implement these policies as an alternative to the far-right techno-authoritarian vision being championed by reactionary political elites and their billionaire supporters. It’s certainly true, as Piketty and his team write in a Guardian op-ed, that technical impossibility is not what is standing in the way but rather “the absence of a shared vision of social progress, at once concrete and radical.” And both the Piketty and De Schutter road maps make clear that formidable forces will oppose any socioeconomic shift toward global sustainable convergence, with the fiercest resistance coming from the ultra rich.

Both reports also briefly outline the need to build countervailing power from the grassroots, explicitly supporting collective action from progressive political parties, labor unions, and civil society organisations. The Global Justice Report even gives its conclusion the subtitle: "A global citizen movement for social justice," and it modestly proffers its analysis to the broader collective mobilization that is already (if all too slowly) advancing at the world scale. So whatever limitations and shortcomings these reports may contain, we can only hope they spur the massive groundswell of popular support that is urgently needed to share the world’s finite resources before it’s too late.

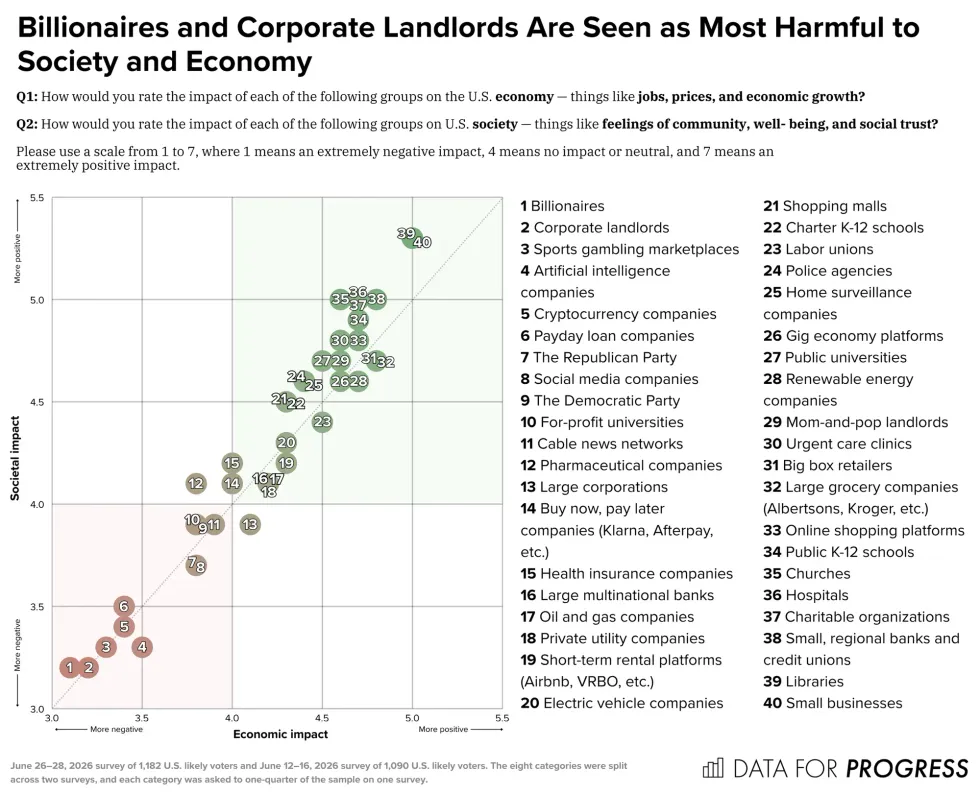

The top villains, according to respondents, are the nation's nearly 1,000 billionaires, then corporate landlords. Rounding out the top 10 were sports gambling marketplaces, artificial intelligence companies, cryptocurrency firms, payday lenders, the Republican Party, social media giants, the Democratic Party, and for-profit universities.

Respondents were asked to rank each group or industry on a seven-point scale from "extremely negative" to "extremely positive."

Those with the most positive views were small businesses, libraries, regional banks and credit unions, charitable organizations, hospitals, churches, public K-12 schools, online shopping platforms, large grocery companies, big box retailers, and urgent care clinics.

"Within categories, we see some meaningful differences between individual actors—mom-and-pop landlords, small regional banks, public K-12 schools, and renewable energy companies are viewed more positively than their counterparts: corporate landlords, multinational banks, charter K-12 schools, and oil and gas companies," the progressive polling firm noted.

With the November midterm elections just four months away, and Democrats trying to seize control of both chambers of Congress as progressives within the party notch key wins over more moderate candidates, Data for Progress executive director Ryan O'Donnell said that "effective populist messaging requires calling out the actors actually making life worse for Americans, and right now, that includes Big Tech and the billionaires behind it."

"As AI continues to impact people's lives directly—whether it's a data center in their backyard or a job replaced by automation—AI companies and tech billionaires are setting themselves up to be the next big villains in American politics," he added.

Earlier this week, as the US Supreme Court's right-wing supermajority "gave their blessing for billionaires to buy even more influence over the politicians who represent us," the watchdog Public Citizen released a report about soaring corporate political spending since the 2010 Citizens United v. Federal Election Commission ruling, including $517 million in this cycle so far.

Some of the top villains from Thursday's polling were key contributors to that figure: "Cryptocurrency, artificial intelligence, Big Tech, and online betting corporations have collectively spent $294 million to influence federal elections in the 2026 midterm cycle."

Blasting the corporate spending as "a disaster for democracy," the report's author, Rick Claypool, said that "if the current, broken campaign finance system remains unchallenged—and corporate spending is allowed to drown out the voices of real voters and real people—these corporate campaigns will keep multiplying, even as voting rights for individual Americans face escalating attacks."

That report and the Data for Progress polling were notably published as more than 250 million people across the United States faced high temperatures tied to the fossil fuel-driven climate emergency—and, as Common Dreams reported earlier Thursday, residents of communities with data centers are being asked to make sacrifices due to strained power grids.

Americans are also awaiting the fate of the bipartisan 21st Century ROAD to Housing Act—which includes a ban on corporate investors buying single-family homes to rent out—because Republican President Donald Trump has refused to sign it in an effort to bully GOP lawmakers into passing a legislative attack on voting rights.

In a comment that multiple congressional Democrats said shows Trump "does not care" about Americans' cost of living concerns, Trump on Monday called the affordable housing bill a "big yawn" compared with the Safeguard American Voter Eligibility, or SAVE America, Act that he wants Congress to send to his desk.