SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"Susan Collins cares far more about protecting bank executives’ millions than protecting the rest of us from BS overdraft fees," said Platner's campaign manager.

Graham Platner's campaign is accusing Sen. Susan Collins of siding with banking interests after she joined Senate Republicans in blocking a Democratic measure to protect consumers from unexpected overdraft fees.

On Wednesday, the GOP voted largely along party lines against a set of Democratic resolutions aiming to restore Consumer Financial Protection Bureau (CFPB) policies killed by the Trump administration.

In what its acting director, Russell Vought, has described as an effort to effectively dismantle the bureau, which has been credited with delivering more than $21 billion in consumer relief since its creation, he has rescinded 67 policies that protected Americans from junk fees, medical debt, lending discrimination, and other financial abuses.

One resolution voted down Wednesday would have restored a scrapped CFPB guidance against debt collectors hounding consumers over false or inflated medical debts. Another would have reaffirmed that the bureau can scrutinize financial companies for predatory credit practices aimed at military families.

These Democratic resolutions were not expected to pass in a Republican-controlled Senate, but were instead meant to force Republicans to put themselves on the record as standing against consumer interests.

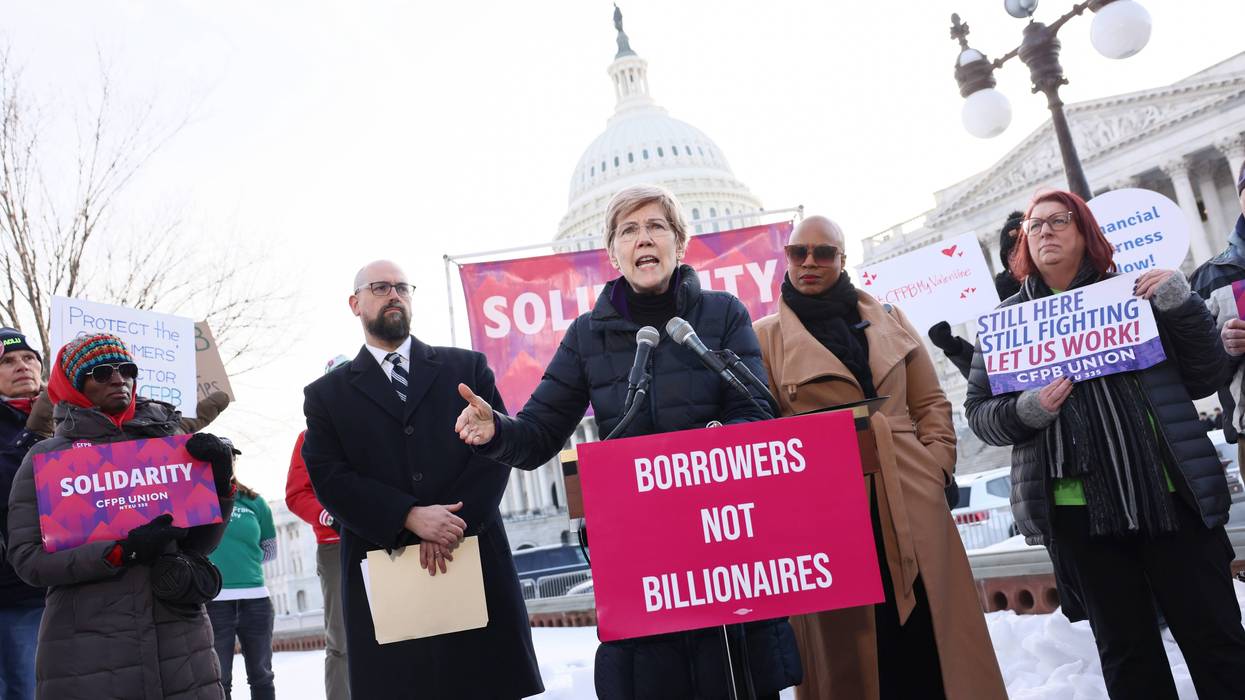

As President Donald Trump takes a beating from voters on the economy, the votes will serve as ammunition as Democrats run with the message that the GOP has "abandoned consumers and is making life more expensive for them," as the CFPB's architect, Sen. Elizabeth Warren (D-Mass), said on Wednesday.

Platner is already deploying that ammunition in one of November's marquee races, hammering Collins (R-Maine) for voting with the GOP against restoring a guidance enacted by the Biden administration that required banks to obtain customers' consent before charging overdraft fees for ATM and one-time debit card transactions.

"Last night, Susan Collins voted once again to make it easier for big banks to hit Maine families with predatory overdraft fees," his campaign said in an email on Thursday. "Her vote to block even a debate on restoring basic consumer protections was just the latest reminder of where Collins' real loyalties lie."

"There is no legitimate policy rationale for voting against basic consumer protections on overdraft fees,” said Platner's campaign manager, Ben Chin. “But Susan Collins cares far more about protecting bank executives’ millions than protecting the rest of us from BS overdraft fees. This vote is yet another example of this deeply unfortunate reality.”

According to data from OpenSecrets, Collins has received nearly $1.8 million this cycle in contributions from the financial sector, including more than $570,000 from private equity and investment firms, which the Platner campaign said were "among the most predatory actors in the American economy."

She's also received more than $44,000 from commercial banks and holding companies that have a particular interest in her stance on overdraft fees.

The Pine Tree Results PAC, which has thrown about $12.7 million behind Collins, likewise got nearly a third of its funding from figures in the financial sector, particularly in private equity and hedge funds with a broader interest in neutering the CFPB.

Congress can’t allow the White House to eliminate an agency that’s helped millions of Americans, with billions of dollars returned to them by scams, fraudsters, and megabanks that prey on low-income citizens.

Over the past year, the Trump administration has sought to gut the Consumer Financial Protection Bureau through cuts and layoffs, and by hamstringing its enforcement powers, claiming the agency is hurting large banks through overregulation. Acting CFPB Director Russ Vought has sought to reduce the agency's staff by 90% and to freeze spending since February.

A group of 21 states, plus the District of Columbia, sued the Trump administration in December to stop it from defunding the CFPB. The administration responded by telling the court that the government is legally barred from seeking new funding from the Federal Reserve, the bureau’s primary source of money, alluding to the fact that the agency will eventually go broke later this year. The next step in the case will be the DC Court of Appeals to hear arguments in late February.

The CFPB's enforcement actions, like the 22 pending cases against banks, highlight its vital role in safeguarding consumers from unfair practices, which the current threats jeopardize.

So, what does this mean for the country? The CFPB's weakening could leave consumers vulnerable to predatory practices, unfair fees, and fraud, risking their financial stability.

The Biden administration's pressure on banks and financial institutions on the issue led them to agree to refund more than $240 million to customers, a win secured by actual, formal regulation. Trump and Vought have rolled that back, too.

The CFPB’s Small Dollar Rule was created to curb abusive payday lending practices, especially repeated debit attempts that drain bank accounts and trigger cascading overdraft and Non-Sufficient Funds (NSF) fees. That goal is sound and worthy. The problem is not the rule’s intent, but how it operates alongside bank fee structures and in a financial marketplace devoid of smart, progressive-minded credit options.

The small dollar rule makes automatic repayments—which help keep the cost of borrowing to the bare minimum—incredibly tricky to execute. After two consecutive failed payment attempts, covered lenders generally cannot try again unless the borrower specifically authorizes another attempt, which can leave payments stalled when ordinary life disruptions intervene. Regulators have warned that charging multiple NSF fees tied to re-presented transactions can harm consumers. This is true not just because a single missed payment can still trigger NSF fee collection and financial harm, undermining a rule meant to protect borrowers acting in good faith. It’s also because lenders are now further limiting credit to the most high-risk borrowers, including gig economy workers, who are also those most in need of emergency credit, forcing them to borrow via ultra-expensive bank and credit union overdrafts and NSFs. And when payments are not made, inevitably, borrowers’ personal credit ratings take a hit. Of course, this affects poor people and those with bad credit harder than anyone else.

Trump and Vought's shuttering of the CFPB without fixing this situation, including by pushing banks hard to provide credit to consumers at lower cost and even by standing up a viable alternative to current credit options through something like Postal Banking, would make the problem of high-interest debt worse for Americans. Moreover, because Trump and Vought refuse to act against extortionate overdraft and NSF fees, as the Biden administration did, they’re exposing consumers to high-cost debt, where they effectively borrow from the bank, too. The Biden administration's pressure on banks and financial institutions on the issue led them to agree to refund more than $240 million to customers, a win secured by actual, formal regulation. Trump and Vought have rolled that back, too.

The CFPB has largely helped people when they have problems with a financial institution, product, or transaction by allowing customers to submit complaints, which the agency then works on their behalf. Since its inception, 98% of the 9 million total complaints have received “timely responses” from the institutions or companies to which customers reported them to the CFPB. Of all the complaints, almost 400,000 were submitted by US military members, and nearly 200,000 were submitted by seniors.

The results have been staggering. CFPB data as of December, 2024 shows a whopping $21 billion has been returned to more than 205 million Americans who were financially harmed by institutions. In addition, over $5 billion in civil penalties have been imposed on guilty banks and individuals.

Congress can’t allow the White House to eliminate an agency that’s helped millions of Americans, with billions of dollars returned to them by scams, fraudsters, and megabanks that prey on low-income citizens. And if the Trump administration is determined to do so, it’s time for congressional Democrats to focus on developing credit alternatives that can allow consumers to escape some of the financial madness.

"When you're counting the way that costs have gone up for American families over the last year, be sure to include the cost of getting cheated," said Sen. Elizabeth Warren.

The Trump administration's ongoing effort to dismantle the Consumer Financial Protection Bureau cost Americans nearly $20 billion in just a year, according to a report released Monday as Democratic lawmakers and campaigners marked the anniversary of the White House's hostile takeover and gutting of the CFPB.

The new report was assembled by Democrats on the Senate Banking Committee led by Sen. Elizabeth Warren (D-Mass.), an architect and champion of the CFPB. Citing bureau documents, publicly available data, and federal analyses, the report estimates that the Trump administration's mass dismissal of enforcement actions against abusive corporations, failure to distribute settlement payments, rescission of CFPB rules and guidance, and attack on the bureau's Consumer Complaint Program have collectively cost US consumers $19 billion over the past year.

That figure, the report emphasizes, "does not even begin to cover costs Americans could have been scammed out of due to a sidelined CFPB."

“Donald Trump promised to lower costs for Americans ‘On Day One.’ Instead, he is trying to shut down an agency that protects Americans from getting scammed out of their money by big banks and giant corporations,” Warren said in a statement. “As a result, Trump’s attempt to sideline the CFPB has cost families billions of dollars over the last year alone. We're going to keep fighting for the CFPB and against the billionaires who want to get rid of it.”

The report was released to mark one year since Russell Vought, the White House budget chief and acting CFPB director, ordered the bureau to effectively shut down its operations, including rulemaking and investigations into corporate wrongdoing.

Lawmakers have not confirmed Vought—a Project 2025 architect who has been explicit about his desire to kill the CFPB—as bureau chief, but he has remained in the acting director role thanks to White House legal maneuvers. In recent months, Vought has tried to starve the CFPB of funding—an effort that, for now, has been stymied in court.

"We want to put it out," Vought said in an interview late last year, boasting about mass firings that have left the consumer agency skeletal. "We will be successful probably within the next two or three months."

Another ridiculous price tag that Trump is forcing you to pay.

This is YOUR money.

You deserve a government that works for you, not against you and your financial interests. https://t.co/yd6hpYriXw

— Senator Andy Kim (@SenatorAndyKim) February 9, 2026

Prior to the start of President Donald Trump's second White House term, the CFPB had returned around $21 billion to US consumers scammed by banks and other corporations since the bureau's creation in the wake of the Great Recession.

"When you're counting the way that costs have gone up for American families over the last year, be sure to include the cost of getting cheated, because Donald Trump has driven that cost through the roof," Warren said during a rally with fellow Democratic lawmakers and advocates in Washington, DC on Monday.

"We are here today to remind Donald Trump and to remind all those Republicans who support him and enable him, to remind every one of them that they can kick this agency, they can try to hold this agency down, they can try to starve this agency, they can try to tie up the people who work at this agency, but at the end of the day, they will not kill this agency," said Warren. "We will stay in this fight, and we will win."