SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

Sen. Warren decried Republicans for helping "squeeze" struggling families and warned that the "latest attack on the CFPB would let big banks rake in huge profits by slamming working people with outrageous overdraft fees."

All but one Republican in the U.S. Senate voted Wednesday night to advance a joint resolution that would nullify a cap on overdraft fees, a protection put in place by the Consumer Financial Protection Bureau to prevent Wall Street banks from making billions more in profits on the backs of vulnerable American consumers.

" Republicans in the Senate voted tonight while no one is watching to fatten Wall Street profits by jacking up overdraft fees on you," said Sen. Elizabeth Warren, following the 52-47 vote that fell almost strictly along party lines. "So much for lowering costs," she added.

Not one Democrat voted in favor pushing the rule forward, while only Sen. Josh Hawley (R-Mo.) voted against and Sen. Brian Schatz (D-Hawaii) did not vote.

In a speech on the Senate floor ahead of the vote, Sen. Warren decried Republicans for helping Wall Street "squeeze" struggling families and warned the "latest attack on the CFPB would let big banks rake in huge profits by slamming working people with outrageous overdraft fees."

Senate Republicans’ latest attack on the CFPB would let big banks rake in huge profits by slamming working people with outrageous overdraft fees.

I spoke on the Senate floor to fight back—because American families deserve a system that works for them, not just Wall Street. pic.twitter.com/W0VzO3cX1I

— Elizabeth Warren (@SenWarren) March 26, 2025

The draft rule was put in place in the final months of the Biden administration as a way to curb excessive fees and provide reasonable protections for consumers who overdraft their accounts. As The Atlanta Journal-Constitution reports:

In 2023, big banks made $5.8 billion from overdraft and non-sufficient fund fees, according to the Consumer Financial Protection Bureau. CFPB announced a new rule capping those fees in December, shortly before [President Joe] Biden left office, that is slated to take effect in October.

The rule gave banks three options: cap overdraft fees at $5; if offering overdraft as a service, rather than for profits, charge a fee that covered the bank's costs and losses; or if looking to make a profit off an overdraft loan, disclose the loan terms to consumers beforehand.

For households that pay overdraft fees, the rule was expected to save them $225 a year.

Sen. Raphael Warnock (D-Ga.) joined Warren in slamming his Republican colleagues over the vote.

"If we leave this $5 cap for overdraft fees in place, guess what, [the banks will] still be doing just fine,” Warnock told the Journal-Constitution. "But if we overturn it, families that are already being squeezed by inflation and by tariffs and a whole range of bad policies that are putting them in jeopardy are going to be squeezed even more."

According to the watchdog group Accountable.US, lifting the rule will allow large Wall Street banks and other financial institutions "to continue exploiting American families" with little or no recourse for relief from such predatory and profit-seeking practices.

"Senate Republicans are siding with big banks to make it easier for them to trick their customers into paying excessive fees," said Tony Carrk, the group's executive director, on Thursday. "The CFPB's overdraft rule limits abusive fees and puts money back in the pockets of consumers. Any vote against the rule is a gift to Wall Street special interests at our expense."

With the

"The U.S. Senate just gave Elon Musk a green light to throw consumers to the online wolves."

Despite warnings of a "blatant gift" that would be bestowed on the world's richest man while harming everyday consumers, the GOP majority in the U.S. Senate on Wednesday passed a resolution that would block the government's Consumer Financial Protection Bureau from regulating online payment systems like Venmo, Google Pay, Apple Pay, and—when it comes to Elon Musk—his proposed X Money, an extension of the social media giant he owns.

The vote on the resolution in the Republican-controlled Senate was 51 to 47, with two senators not voting. Every member of the Democratic caucus, including Independent Sens. Bernie Sanders of Vermont and Angus King of Maine, voted against the measure while every Republican but one, Sen. Josh Hawley of Missouri, voted in favor.

The legislation, if also approved by the GOP-controlled House and signed by President Donald Trump, would nullify a rule put forth by the Biden administration allowing the CFPB to more closely monitor the growing army of online payment services.

Critics of Republican efforts to destroy the rule, as well as broader efforts to undermine the CFPB's ability to serve as a watchdog for the financial industry, have said that restricting the agency's oversight in this sector would be a direct giveaway to Musk due to his pronounced personal interest in the online payment space that could be worth billions of dollars in future profits.

"The U.S. Senate just gave Elon Musk a green light to throw consumers to the online wolves," said Emily Peterson-Cassin, corporate power director at Demand Progress, a progressive advocacy group.

"In no way should X, a platform already swarming with bots and crypto scams, be allowed to accept real-time payments without having to follow the same consumer protection oversight that major banks have to follow," Peterson-Cassin added. "Without CFPB supervision, X Money users who are hacked, scammed, or want to dispute fraudulent payments could be left to fend for themselves. We call on the House to stand on the side of consumers, and not online scammers, by voting against this corrupt, reckless bill."

In a statement on Wednesday following the vote, Sens. Elizabeth Warren (D-Mass.) and Adam Schiff (D-Calif.) said the resolution was akin to a "Get Out of Jail Free Card" for Musk.

In a joint letter to acting director of the Office of Government Ethics, Secretary Doug Collins, Warren and Schiff demanded answers about Musk's conflicts of interest as he spearheads the Trump-invented Department of Government Efficiency, or DOGE, while that pseudo agency targets the CFPB.

According to the letter:

In addition to his role as head of DOGE, Mr. Musk is the primary owner of the social media company X. Since purchasing X, Mr. Musk has considered expanding the social media platform into digital payments. On January 28, X announced a partnership with Visa to process peer-to-peer payments and launch a digital wallet. Notably, the CFPB has taken steps in recent years to protect consumers from fraud on digital payment apps and collects proprietary information from the digital payment industry. Mr. Musk is also the founder and CEO of Tesla, which offers customers the option of working with Tesla to finance their auto purchases. The CFPB plays a critical role in supervising the auto lending industry and protecting consumers from corporate malfeasance and scams. Therefore, actions by Mr. Musk and DOGE at the CFPB have the potential to directly benefit X, Visa, and Tesla—and by extension, Mr. Musk.

Warren and Schiff argued that "potential criminal consequences" could be on the table for Musk, noting in their letter that if the right-wing billionaire "has taken actions in his federal role that will benefit his financial interests without receiving appropriate waivers and approvals, he may have violated the criminal conflict of interest statute."

"This is just the latest broken promise from Republicans, who have used their short time in power to already cater to special interests over hardworking Americans," said one watchdog leader.

A U.S. watchdog group on Tuesday slammed Republicans in Congress for trying to kill the Consumer Financial Protection Bureau's overdraft rule as U.S. President Donald Trump and billionaire Elon Musk target the CFPB as a whole.

The Accountable.US statement came in response to Senate Banking Committee Chair Tim Scott (R-S.C.) and House Financial Services Committee Chair French Hill (R-Ark.) recently introducing a Congressional Review Act (CRA) resolution to overturn the rule that capped most overdraft fees at $5, which was finalized in December, near the end of the former President Joe Biden's term.

"Overdraft fees affect a huge portion of American families with 17% of households with checking accounts paying overdraft or [nonsufficient funds] fees in 2023," Accountable.US noted. "This action would open the door for $35 overdraft fees—a decision that would cost American households an average of $225 each year."

The watchdog's executive director, Tony Carrk, declared that "undoing the CFPB's overdraft fee rule is a gift to big banks and a gut punch to the wallets of millions of Americans across the country."

"Deceitful and excessive overdraft fees cost Americans billions of dollars every year, but the Trump administration and Republicans in Congress don't seem to care any longer about lowering costs for Americans now that they're in charge," he continued. "This is just the latest broken promise from Republicans, who have used their short time in power to already cater to special interests over hardworking Americans."

When the Republican chairs introduced their CRA resolution last week, Scott called the Biden-era CFPB rule an example of the "pursuit of political headlines over sound policies," and Hill described it "midnight rulemaking" and "another form of government price controls that hurt consumers who deserve financial protections and greater choice."

Meanwhile, when the CFPB finalized the rule, the agency said that it "took action to close an outdated overdraft loophole that exempted overdraft loans from lending laws." At the time, the bureau was still directed by Biden appointee Rohit Chopra, who highlighted that large banks' exploitation of the loophole had "drained billions of dollars from Americans' deposit accounts."

The rule "was scheduled to become effective in October," but "because of acting Director Russ Vought's unlawful order stalling all CFPB work, the effective date has been suspended," The American Prospect reported Monday. "If Congress passes the CRA resolution, the overdraft rule could not come back in any 'substantially similar' form. So it matters if congressional Republicans decide to support allowing banks to impose additional junk fees worth billions of dollars."

The outlet also pointed out that "because CRA resolutions cannot be stopped by a filibuster, they represent some of the most likely legislative actions of the early Trump term," given Republicans' narrow majorities in Congress."

It's not just the rule that's in jeopardy; the entire agency is at risk. Trump and Musk, the leader of the president's Department of Government Efficiency (DOGE)—though perhaps not on paper—are working to gut the federal workforce and slash spending, and they have the CFPB in their crosshairs.

An agreement reached Friday in federal court halted mass firings at the CFPB and barred the bureau and its temporary leader, Vought—who also leads the Office of Management and Budget—from purging data or defunding the agency while the case moves forward. However, Trump and Musk are expected to continue their effort.

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," Corryn G. Freeman, executive director of the youth-focused Future Coalition, said Monday. "The CFPB should be strengthened, not eliminated. If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," said the head of one advocacy group.

A national nonprofit that aims to "empower young changemakers" on Monday called out U.S. President Donald Trump and his billionaire ally Elon Musk for attacking a federal consumer financial watchdog as "part of a broader, dangerous effort to privatize and dismantle the civil service, eroding the government's ability to protect working people from corporate exploitation."

"Musk, an unelected billionaire with no constitutional authority to restructure federal agencies, is wielding his influence in the Trump administration to gut consumer protections—just as he moves to expand his own financial empire through X Money," the nonprofit, Future Coalition, said in a statement about the assault on the Consumer Financial Protection Bureau (CFPB).

"Musk, through his leadership of the Department of Government Efficiency (DOGE), has taken it upon himself to reshape federal agencies to suit his personal financial interests," the group continued. "The move to eliminate the CFPB is a glaring example of this corrupt power grab, where billionaires rewrite the rules to benefit themselves at the expense of everyday Americans."

"If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

Although the White House created confusion on Monday evening by stating in a declaration to a federal judge overseeing another case that Musk "is a senior adviser to the president" and "is not the U.S. DOGE service administrator," the world's richest billionaire is widely understood to be overseeing the Trump administration's attempts to gut the federal government.

At the CFPB specifically, that effort is currently at a standstill due to a legal challenge. A fight in federal court on Friday halted mass firings there and under the agreement, the agency and its temporary leader, Office of Management and Budget Director Russell Vought, must retain "vast troves" of data and refrain from defunding the bureau while the case proceeds.

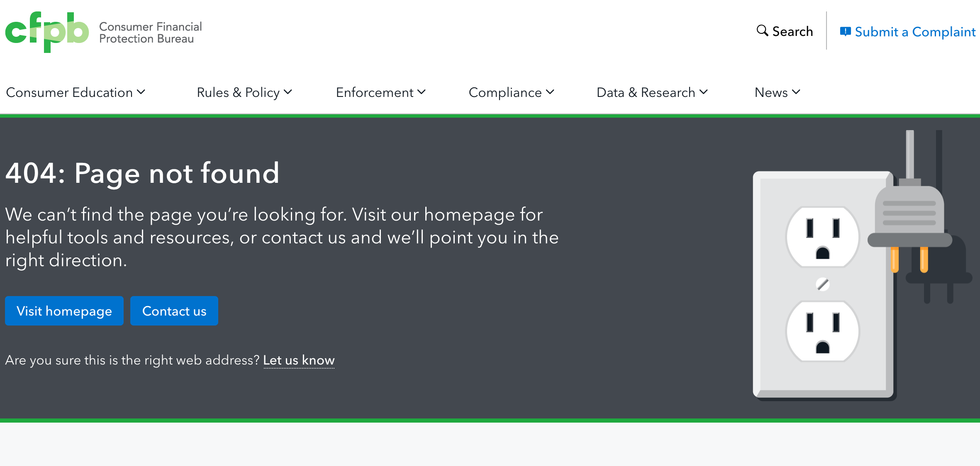

Still, there are signs that Trump and his allies will keep working to shutter the CFPB, including a "404: Page not found" message displayed on the homepage of the agency's website as of Tuesday afternoon. The message has been there for more than 10 days.

The Consumer Financial Protection Bureau's hompage displayed a "404: Page not found" message on February 18, 2025. (Photo: CFPB/screen grab)

The Consumer Financial Protection Bureau's hompage displayed a "404: Page not found" message on February 18, 2025. (Photo: CFPB/screen grab)

Critics of Trump, Musk, and DOGE continue to warn about how the "unprecedented corporate coup" targeting the CFPB would help the billionaire and various fraudsters while harming Americans. As Future Coalition highlighted Monday, anticipated consequences of ending the agency include the weakening of protections for student loan borrowers, the removal of protections against junk fees, and increases in predatory lending and financial fraud—from cryptocurrency schemes to mobile payment scams.

"Young people today are drowning in student debt, struggling to afford housing, and navigating a financial system rigged against them—yet conservative forces and big business have spent over a decade trying to dismantle the one agency designed to protect them," said Corryn G. Freeman, executive director of Future Coalition. "The CFPB is not the problem—corporate greed is."

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," Freeman added. "The CFPB should be strengthened, not eliminated. If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

U.S. Sen. Elizabeth Warren (D-Mass.), a former Harvard Law School professor who proposed and helped craft the CFPB before joining Congress, has delivered a similar message in recent days.

As The New Yorker's John Cassidy reported Monday:

A week ago, Elon Musk tweeted, "CFPB RIP." In short order, the Trump administration has shuttered the headquarters of the agency, halted most of its operations, and laid off some of its staff. Since Musk’s démarche, Warren—who was elected to the Senate as a Democrat from Massachusetts in 2013, and is now in her third term—has led the effort to save the CFPB, speaking at a rally outside its offices, tearing into the Tesla CEO in television interviews, and, in a Senate hearing, pressing Jerome Powell, the chairman of the Federal Reserve, to confirm that without the CFPB there is no government agency to insure that financial companies obey consumer-protection laws.

When I caught up with Warren on the phone, late last week, she recalled that prior to the creation of the CFPB, responsibility for enforcing these laws was split between six regulatory agencies. "It was nobody's first job, and nothing got done," she remarked. The founding of the CFPB brought consumer protection—regulation, supervision, and enforcement—under one roof. "For a dozen years, the CFPB has been the financial cop on the beat," Warren went on. "It has found more than $21 billion in fraud and scams, and scooped up that money and returned it directly to the people who were cheated. Now Elon Musk comes in and says, 'Let's fire the cops.' What could possibly go wrong?"

If the Trump administration succeeds in dismantling the agency, "it's open season on everyone who has a credit card, a mortgage, a car loan, a payday loan, a student loan, or uses an online financial app," Warren warned. The senator also offered a reason why the agency has faced attacks from Republicans since long before Musk decided to help Trump return to the White House.

"The CFPB is living, breathing proof, every day, that we can make government work for regular people," she said. "That we can use government to level the playing field, so that students don't get cheated on their education loans, or a family can take out a mortgage to buy a house without worrying there's a trick back on page 36 that means they are going to lose the house in two years. That's government working the way it should, and it really gets under the skins of the most extremist Republicans."

The billionaire plotters did not bring guns, but they have entered the buildings. They are here.

A classic coup d’état has guns. Uniformed men run wild seizing government agencies and claiming control over what government does and who government serves.

But in our new cyber age, the Yale historian Timothy Snyder reflected this past week, a coup can unfold without any armed overthrow. We can have “a couple dozen young men go from government office to government office, dressed in civilian clothes and armed only with zip drives.”

These young men, operating upon “vague references to orders from on high,” can gain access to basic computer systems and “proceed to grant their Supreme Leader” effective power over just about everything that government does.

The historian Snyder is, of course, describing America’s current reality. He’s calling this reality a coup — and so are countless other defenders of America’s democratic faith.

We aren’t living through “a coup with tanks in the streets and mobs overrunning government offices,” charges former U.S. attorney and current Brennan Center senior fellow Joyce Vance. We’ve living through “a quieter coup, a billionaires’ coup.”

“The richest man on Earth is attempting to seize physical control of government payment systems and use them to shut down federal funding to any recipient he personally dislikes,” adds in the University of Minnesota Law School’s Will Stancil. “Elon Musk is directly usurping Congress’s most important authority, the power of the purse.”

The Musk legions now hacking their way through the nation’s capital, the New York Times reports, have already “inserted themselves” into the databases of 17 federal agencies. These legions include fervent Musk admirers like Akash Bobba, a software engineer less than three years out of high school who once interned with a tech firm chaired by fellow Musk billionaire Peter Thiel.

One by one, the federal agencies that keep our nation running have been falling — with the full backing and blessings of Donald Trump — under Musk’s effective control. Trump, meanwhile, is making headlines about taking over Gaza and Panama, in the process, notes Senator Chris Murphy from Connecticut, “distracting everyone from the real story — the billionaires seizing government to steal from regular people.”

The Trumpsters, agrees Senator Bernie Sanders from Vermont, are moving us “into an oligarchic form of society where extraordinary power rests in the hands of a small number of unelected multi-billionaires.”

Elected officials and progressive activists are pushing back in the courts against the Musk putsch and scoring some initial victories. One federal judge, for instance, has just blocked Musk’s access to the Treasury Department’s computer payments system. That access, the judge ruled, threatens “irreparable harm” to the personal and financial data of millions of Americans.

But lower-level court rulings may not pass muster with higher-level Trump-appointed judges. Stopping the Musk coup will require a broader popular mobilization, and that push back is indeed building, with protests drawing thousands in locales ranging from downtown Washington to a host of state capitols nationwide.

Our single best hope to counter the Musk coup’s billionaire corporate backers — “and their boundless options” to shape “our elections, legislation, and judicial appointments”? That may well be intensified trade union action, suggests a new analysis from long-time labor activist Michael Podhorzer — and that action is also building.

Labor’s national voice, the AFL-CIO, has just launched a new campaign, the Department of People Who Work for a Living, to challenge Musk and his “Department of Government Efficiency.”

“Government can work for billionaires,” points out AFL-CIO president Liz Shuler, “or it can work for working people — but not both.”

Recent days have seen a full-frontal assault on the Consumer Financial Protection Bureau and Trump's favorite billionaire has much to gain personally if the agency no longer has the ability to operate effectively on behalf of the American people.

The Trump administration's multi-pronged attack on the CFPB continues.

President Donald Trump's new acting director of the Consumer Financial Protection Bureau, Russell Vought, told the agency to cease nearly all its operations in a series of orders on Saturday night and the move is not just a gift to the broader financial industry and large Wall Street banks, say critical observers, but also a major potential gift to billionaire Elon Musk, the world's wealthiest person, who has a major vested interest in the agency's demise.

Vought, the right-wing architect of the anti-government Project 2025 who also now heads the powerful Office of Management and Budget, confirmed Saturday night he had taken control of the agency in an email to staff that called on them to halt most of their work.

"Musk wants to use the government to put more in his pockets. This is a blatant conflict of interest." —Sen. Ed. Markey

According to reporting by NBC News, which obtained a copy of the email,

Employees were instructed to "cease all supervision and examination activity," "cease all stakeholder engagement," pause all pending investigations, not issue any public communications and pause "enforcement actions."

Vought also told employees not to "approve or issue any proposed or final rules or formal or informal guidance" and to "suspend the effective dates of all final rules that have been issued or published but that have not yet become effective," among other directives listed in the email.

He said in the email that the directives are effective immediately, unless he approves an exception or a certain activity is required by law.

The agency has been a target for Republicans for years and the party has contested in court its source of funding, which unlike most other agencies is funded by the Federal Reserve as opposed to regular appropriations by Congress. That mechanism, however, was established by Congress when the CFPB was created—an approach that was designed to shield it from political interference—and has withstood all legal challenges, including one before the U.S. Supreme Court last year.

Sen. Elizabeth Warren (D-Mass.), credited with bringing the CFPB to life, said the orders from Vought make clear the Trump administrations intentions.

"Vought is giving big banks and giant corporations the green light to scam families," Warren said Saturday. "The Consumer Financial Protection Bureau has returned over $21 billion to families cheated by Wall Street. Republicans have failed to gut it in Congress and in the courts. They will fail again."

Vought, in his online post, said he also informed Fed Chairman Jerome Powell on Saturday that the agency would be requesting $0 for the upcoming draw period, claiming that no additional funds were needed to fulfill its work.

"The Bureau's current balance of $711.6 million is in fact excessive in the current fiscal environment," Vought claimed. "This spigot, long contributing to CFPB's unaccountability, is now being turned off."

Critics point out that Musk, who has been appointed by Trump to head the Department of Government Efficiency (DOGE), has serious conflicts when it comes to the Trump administration's targeting of the CFPB.

DOGE is not a real department but has claimed sweeping authority to access the sensitive workings of federal agencies—triggering an avalanche of legal challenges as a result. In addition to Vought's statements, the previous CFPB acting director, Treasury Secretary Scott Bessent, last week issued an internal stop work order that was challenged by Democratic lawmakers.

On Friday, as Common Dreams reported, Musk himself posted "CFPB RIP" on social media next to a picture of a gravestone and his detractors have argued his antagonism is not based solely on his ideological opposition to an agency that has returned over $20 billion to consumers over recent years from bad financial actors.

In an appearance Saturday on MSNBC, Lindsay Owens, executive director of the progressive advocacy group Groundwork Collective, explained that while Vought's targeting of CFPB can be explained by well-documented fealty to various corporate interests—and a desire "to destroy the government from the inside out"—Musk's motivations are likely "more sinister" and closer to home.

Elon Musk and Russ Vought have taken over the CFPB. That’s bad news for consumers.

Vought’s aim is to destroy govt from the inside out, and Musk's motive is more sinister. As he partners with Visa on a payment app, he has an interest in ensuring the CFPB doesn't get in his way. pic.twitter.com/C7FAFfG0xI

— Groundwork Collaborative (@Groundwork) February 8, 2025

Diminishing CFPB's ability to operate as well as getting a look at its trove of files, including the inner workings of those institutions it has been tasked with holding to account, said Owens, is a for Musk to "grease the skids for his new business interest."

"We know that Elon Musk is interested in starting his own payment app—he's partnered with Visa to do that," she explained, "and so he has a real interest in ensuring that the CFPB isn't blocking an effort like that."

Owens said that Musk's interest in the agency goes beyond that as well, because the CFPB has "trade secrets from enforcement actions against some of his likely future competitors."

On Friday, The American Prospect's David Dayen reported on the little-noticed Feb. 3 order that Bessent sent out to CFPB staffers which specifically halted new designation of non-bank entities, including "nondepository institutions," by the agency—a policy that could directly impact Musk's peer-to-peer payment venture he hopes to launch on X in partnership with Visa.

According to Dayen:

By stalling designation of nondepository institutions, Bessent ensures that X will not be designated for CFPB supervision, at least in the near term.

The more innocent explanation for the last-minute change is that Bessent was likely uninformed about what the CFPB does, and hastily added supervision later. But the inserted directive specifically bars designation of non-banks in the supervisory process, as a not-so-thinly-veiled shield for Big Tech payment app firms, and in particular the company run by special government employee Elon Musk.

Sen. Ed Markey (D-Mass.) expressed concerns along these grounds on Saturday night.

"Elon wants the CFPB gone so tech billionaires can profit from apps, like X, that offer bank-like services but don't follow financial laws that keep people’s money safe," charged Markey. "Musk wants to use the government to put more in his pockets. This is a blatant conflict of interest."

"The richest man in the world wants to shut down an agency that keeps people like him from ripping off the rest of us."

Defenders of a Consumer Financial Protection Bureau that has returned tens of billions of dollars to duped and defrauded U.S. consumers expressed outrage overnight and into Saturday after the independent agency was declared deceased by billionaire Elon Musk and its operations were handed over to the chief architect of the far-right Project 2025 Russell Vought.

Vought, who earlier this week was confirmed as head of the Office of Management and Budget by Senate Republicans, was named acting director of the CFPB by President Donald Trump, according to various reports.

The appointment of the far-right ideologue came less than a day after reports emerged that members of the Musk-led Department of Government Efficiency (DOGE) were granted access to key CFPB systems and Musk himself posted to his online social media X that the agency should "RIP," suggesting it was in the process of being dismantled or, in his mind, already killed.

"Since its creation, the Bureau has returned $21 billion to people's wallets by fighting against illegal financial charges, junk fees, debts, and fraud," said Mike Calhoun, president of the nonpartisan Center for Responsible Lending, in a statement on Saturday. Now, when people are already struggling to pay higher prices for necessities like eggs and milk, the Trump administration appears to have decided to deepen the pain by directly taking aim at the agency that helps keep our money safe."

"When people are already struggling to pay higher prices for necessities like eggs and milk, the Trump administration appears to have decided to deepen the pain by directly taking aim at the agency that helps keep our money safe."

"'Let them eat debt' is not a strategy for making America great again," Calhoun added, "and weakening the CFPB certainly isn't the way to keep working families, our financial markets, or our economy strong."

Stacy Mitchell, co-director of the Institute for Local Self-Reliance, which challenges corporate encroachment on the common good, said, "Obviously this isn't about 'efficiency.' It's about dismantling law enforcement that protects Americans from corporate power."

Congressional Democrats also reacted with contempt to Musk's message and the news that the agency's systems—like those of other agencies DOGE has put its hands on—were under threat.

"Here is the richest man in the world bragging about eliminating an agency that has delivered $21 billion back to working-class families since its inception," said Democrats on the House Committee on Financial Services, led by Ranking Member Maxine Waters of California. "Even most Republicans want the CFPB to continue protecting them from being ripped off by abusive big banks and predatory lenders."

"Here are the FACTS: 81% of voters, both Republicans and Democrats, support the CFPB and want the agency to continue its work," said Rep. Juan Vargas (D-Calif.), also a member of the committee. "Even so, Trump has moved to freeze the CFPB to take money out of YOUR pocket to line those of his billionaire friends."

In a letter sent to the CFPB on Friday—addressed to the previous acting director, Treasury Secretary Scott Bessent, whose first act of business was reportedly to order a halt of "all meaningful work"—Waters, Vargas, and 79 other Democratic members of the House said they were "deeply alarmed and troubled that you appear to be launching the Trump Administration's plan to contravene the will of Congress and unlawfully 'delete' this popular consumer watchdog that enjoys the broad bipartisan support of four out of five Americans."

According to the letter:

... we understand that you have ordered staff to halt all meaningful work of the CFPB, including ordering staff to stop investigating violations of consumer financial protection laws or settling enforcement actions, basically letting bad actors off the hook. We also understand that you have arbitrarily ordered the suspension of all CFPB rules that have yet to take effect, which would delay billions of dollars in savings and credit opportunities for consumers, if not rob them entirely.

We urge you to immediately rescind what appears to be an illegal stop work order and allow the public servants at the CFPB to get back to work for the American people as required by law.

As of this writing, the CFPB's homepage (www.consumerfinance.gov) prominently displayed a 404 error message, though portions of the site appeared to be active.

In a Saturday statement, the Democrats on the House Finance Committee said the 404 image on the CFPB website was intentionally "deceptive," calling it "a brazen attempt to fool consumers and the public about the status" of the agency.

"As of this moment, links and pages are still up and functional on the website," the statement said, "including the Consumer Complaint portal and database and Home Mortgage Disclosure Act (HMDA) database. Various aspects of the CFPB's web content is required by statute to be published and available on the CFPB's website."

"Let's be clear: the people cheering this the loudest are scammers and people who don't want you to keep your hard-earned dollars. So much for lowering costs."

Nadine Chabrier, counsel at the Center for Responsible Lending, said the "deeply troubling" developments at the agency will "undermine the CFPB's mission to protect consumers from financial misconduct" of various kinds.

"CFPB has returned more than $20,000,000,000 to consumers since it was founded," said Rep. Gabe Amo (D-R.I.) on Friday evening in response to Musk's tweet. "Let's be clear: the people cheering this the loudest are scammers and people who don't want you to keep your hard-earned dollars. So much for lowering costs."

"If Chopra continues to make life miserable for financial operators and oligarchs—Big Tech has been one of his main concerns—the pressure to dump him will grow," wrote one journalist.

The editorial board of The Wall Street Journal vented its frustration Thursday that Rohit Chopra, the director of the Consumer Financial Protection Bureau, is still in his post at the end of the first week of U.S. President Donald Trump's second White House term.

"Why Is Rohit Chopra Still Employed at the CFPB?" reads the headline of an editorial the Journal published late Thursday, hours after the Chopra-led bureau announced that it is opening a docket for public comment on credit card interest rates and other terms.

"Americans owe well over $1 trillion in credit card debt, and many feel crushed by sky-high interest and fees," Chopra wrote in a social media post Thursday morning.

Morgan Harper, director of policy and advocacy at the American Economic Liberties Project, said in a statement that "the only groups opposing this effort are big banks and credit card companies, which would rather see the agency sit idly by as they rake in excess profits from consumers through fees and interest rates that often surpass 30%."

Chopra was chosen by former President Joe Biden to lead the CFPB, a frequent target of attacks from Republicans and Trump allies, including billionaire Elon Musk. During his first White House stint, Trump attempted to gut the CFPB by installing an opponent of the bureau to lead it.

But while Chopra has packed up his office in Washington, D.C., Trump has yet to fire the CFPB chief—a fact that is reportedly making Wall Street nervous.

"It's just amusing that the time hasn't come yet. Amid all the other wreckage, watching Wall Street squirm a bit is at least a tiny bit of solace."

The Journal's editorial board, a reliable mouthpiece for big business, complained Thursday that Chopra "has spent his tenure advancing progressive hobbyhorses, including rules that ban medical debt on consumer credit reports and cap bank overdraft fees."

The editorial goes on to claim, citing anonymous sources, that Chopra has "sought to ingratiate himself with [Vice President] JD Vance in hopes of serving out his term," which officially ends in October 2026.

News reports suggest that Trump's team has "struggled to make selections to replace" Chopra—a difficulty that one watchdog said is unsurprising.

"Being the hatchet person for the sort of chiselers and grifters that the CFPB fights against is not exactly a fun job—especially as some elements within MAGA could potentially call you out," Jeff Hauser of the Revolving Door Project told The American Prospect.

In a column on Friday, the Prospect's David Dayen wrote that Chopra's continued presence at the helm of the CFPB is "freaking Wall Street out."

"Though it was expected that he would be quickly let go, his office continues to be active," Dayen noted. "On Tuesday, CFPB announced a settlement with Argus Information and Advisory Services, a TransUnion subsidiary, CFPB contractor, and serial violator of several financial and data privacy laws. Argus agreed to not seek any contracts with CFPB for five years. Then on Thursday, CFPB released a report showing growing instances of auto repossessions, well above the pre-pandemic level."

Over the past four years, the Chopra-led CFPB "managed to put over $6 billion back into the pockets of Americans," according to the Consumer Federation of America.

But Dayen wrote that "if Chopra continues to make life miserable for financial operators and oligarchs—Big Tech has been one of his main concerns—the pressure to dump him will grow."

"It's just amusing that the time hasn't come yet," Dayen added. "Amid all the other wreckage, watching Wall Street squirm a bit is at least a tiny bit of solace."

"When the Consumer Financial Protection Bureau is allowed to fully do its job, Americans only stand to benefit."

In the coming weeks, as President-elect Donald Trump's second term approaches and his pledge to dismantle key agencies potentially comes closer to fruition, 4.3 million consumers are set to receive checks from one of the agencies the incoming administration wants to "delete."

The Consumer Financial Protection Bureau (CFPB) announced Thursday that it will soon begin distributing a historic $1.8 billion to millions of people who were charged illegal junk fees or defrauded by credit repair companies including Lexington Law and CreditRepair.com.

The money will be distributed from the CFPB's victim relief fund, which was created by Congress and is financed entirely by civil penalties paid by companies and individuals who violate consumer financial protection laws.

The fund has distributed $3.3 billion to consumers since its inception, and the CFPB said the forthcoming payment will be its largest ever.

"Lexington Law and CreditRepair.com exploited vulnerable consumers who were trying to rebuild their credit, charging them illegal junk fees for results they hadn't delivered," said CFPB Director Rohit Chopra. "This historic distribution of $1.8 billion demonstrates the CFPB's commitment to making consumers whole."

A district court ruled in August 2023 that the two companies had violated the Telemarketing Sales Rule's prohibition on advance fees, which bars credit repair firms from collecting fees from consumers until they prove they have achieved the results they promise to their customers.

If the CFPB payments are divided equally among those who were wrongly charged fees by the two companies, each consumer would receive about $419.

The payments are being sent days after the CFPB proposed a rule aimed at reining in data brokers who sell people's personal information.

As Common Dreams reported, billionaire entrepreneur Elon Musk has expressed concern about the practices of data brokers—but as Trump's nominee to co-lead the Department of Government Efficiency (DOGE), a yet-to-be-created commission that would cut regulations and government spending, Musk has pledged to "delete" the CFPB.

Filmmaker and media activist Danny Ledonne said Musk and Vivek Ramaswamy, another businessman nominated to lead DOGE, likely want to do away with the CFPB because the agency acts "in the interest of regular people."

Liz Zelnick, director of the Economic Security and Corporate Power Program at government watchdog Accountable.US, said the upcoming $1.8 billion payout shows why the CFPB should remain in operation.

"When the Consumer Financial Protection Bureau is allowed to fully do its job, Americans only stand to benefit," said Zelnick. "Between surprise fees and misleading business practices, today's victory affirms the importance of the CFPB for defending people across the country from shady industry actors."

Rep. Mark Pocan (D-Wis.) said supporters of consumer protections in Congress will "fight any attempts to dismantle [CFPB], whether from Trump, Musk, or their billionaire buddies."

"The CFPB fights for everyday Americans against corporate greed, junk fees, and predatory lenders," he said. "This watchdog agency protects normal people like you and me."

"Of course Trumpers want to dismantle the only agency formed in decades dedicated to giving consumers a fair shake in a predatory economy," one journalist said in response to reporting on Republican plans.

Just hours after U.S. President Donald Trumpnamed a labor secretary nominee seen by some union leaders and advocates as genuinely pro-worker, The Washington Post on Saturday detailed what the incoming administration and Republican Congress have planned for a federal agency designed to protect everyday Americans from corporate abuse.

Initially proposed by Sen. Elizabeth Warren (D-Mass.) while she was still a Harvard Law School professor, the Consumer Financial Protection Bureau (CFPB) was created by the Dodd-Frank Wall Street Reform and Consumer Protection Act, which Congress passed in response to the 2007-08 financial crisis.

The first Trump administration was accused of "gutting the CFPB and corrupting its mission." However, as the Post noted, "its current Democratic leader, Rohit Chopra, has been aggressive" in his fights for consumers, working to get medical debt off credit reports and crack down on "junk fees" for everything from bank account overdrafts and credit cards to paycheck advance products—efforts that have drawn fierce challenges from the financial industry.

"Working- and middle-class people who voted for Trump did so for many reasons, but you'd be hard-pressed to find any who did so because they want higher overdraft fees."

Chopra, an appointee of outgoing President Joe Biden, isn't expected to stay at the CFPB, but Trump's recent win hasn't yet halted bold action at the agency. On Thursday, it announced plans "to supervise the largest nonbank companies offering digital funds transfer and payment wallet apps," which is set to impact Amazon, Apple, Block, Google, PayPal, Venmo, and Zelle, unless the Trump administration shifts course.

The Post reported that Republican leaders "intend to use control of the House, Senate, and White House next year to impose new restrictions on the agency, in some cases permanently," and "early discussions align the GOP with banks, credit card companies, mortgage lenders, and other large financial institutions."

According to the newspaper:

"There will be a pretty significant change from the direction the agency has been going in, and I think in a positive way," predicted Kathy Kraninger, who led the CFPB during Trump's first term. She now serves as chief executive of the Florida Bankers Association, a lobbying group whose board of directors includes top executives from Bank of America, JPMorgan Chase, PNC, and Truist.

Aides on Trump's transition team have started considering candidates to lead the CFPB who are expected to ease its oversight of banks, lenders, and tech giants. The early short list includes Brian Johnson, a former agency official; Keith Noreika, a banking consultant and former regulator; and Todd Zywicki, a professor at George Mason University's law school who has previously advised the bureau, according to four people familiar with the matter.

"Of course Trumpers want to dismantle the only agency formed in decades dedicated to giving consumers a fair shake in a predatory economy," Katrina vanden Heuvel, The Nation's editorial director and publisher, said in response to the reporting—which came just a day after Forbes similarly previewed "big changes coming to Elizabeth Warren's CFPB" when Trump returns.

"The number of CFPB regulatory advisories and enforcement actions will likely shrink" and "bank mergers and acquisitions could see a boost too," Forbes highlighted. "Even more noteworthy, the CFPB's funding structure could be at increased risk," with some congressional Republicans considering the reconciliation process as a path to forcing changes, following the U.S. Supreme Court's May decision that allowed the watchdog to keep drawing money from the earnings of the Federal Reserve System.

"Changing the CFPB's funding structure would be an uphill battle since it would be perceived by many as an attempt to take the bureau’s budget to zero," the magazine noted. "But the concept 'has been on every wish list I've seen from House Republicans for the last 10 years or more since its creation,' says a former Capitol Hill staffer who has worked with the House Financial Services Committee."

Warren, who won a third term in the Senate earlier this month, is optimistic about the agency's survival. "The CFPB is here to stay," she told the Post. "So I get there's big talk, but the laws supporting the CFPB are strong, and support across this nation from Democrats, Republicans, and people who don't pay any attention at all to politics, is also strong."

The senator's comments about the CFPB's popularity are backed up by polling conducted last weekend and released Thursday by Data for Progress. Although the progressive firm found that a plurality of voters (48%) lacked an initial opinion of the agency, they expressed support when introduced to major moves during the Biden administration.

"More than 8 in 10 voters support the CFPB's actions to protect Medicare recipients from illegal and inaccurate bills (88%), crack down on illegal medical debt collection practices like misrepresenting consumers' rights and double-dipping on services already covered by insurance (86%), publish a consumer guide informing consumers of the steps they can take if they receive collection notices for medical bills (84%), and propose a rule to ban medical bills from people’s credit reports (81%)," the firm said.

Data for Progress also found that voters back agency actions to "require that companies update any risky data collection practices (85%), rule that banks and other providers must make personal financial data available without junk fees to consumers (85%), confront banks for illegal mortgage lending discrimination against minority neighborhoods (83%), and state that third parties cannot collect, use, or retain data to advance their own commercial interests through targeted or behavioral advertising (80%)."

After learning about the watchdog's recent moves, 75% of voters across the political spectrum said they approve of the CFPB.

The polling came out the same day Warren addressed Trump's campaigning on a 10% cap for credit card interest rates.

"I can't imagine that President Trump didn't mean every single thing he said during the campaign," Warren

told reporters. She later added on social media: "If Donald Trump really wants to take on the credit card industry, count me in. The CFPB will back him up."

While Trump's latest electoral success was thanks in part to winning over key numbers of working-class voters, the president-elect has spent the post-election period filling key roles in his next administration with billionaires and loyalists, fueling expectations that his return to the White House—with a Republican-controlled Congress—will largely serve ultrarich people and corporations, reminiscent of his first term.

The recent reporting on the CFPB has further solidified those expectations. In a snarky social media post, Aaron Sojourner, a labor economist and senior researcher at the W. E. Upjohn Institute for Employment Research who served on the Council of Economic Advisers (CEA) during the Trump and Obama administrations, wrote: "#priorities Bringing back junk fees."

Joshua Smith, budget policy director for the Democrat-run Senate Budget Committee,

said that "working- and middle-class people who voted for Trump did so for many reasons, but you'd be hard-pressed to find any who did so because they want higher overdraft fees."