SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

“At a time of extreme and growing inequality," said one critic, "today’s proposals will drain lending away from Main Street families’ needs and priorities and further enrich the already wealthy on Wall Street."

The Trump administration and Federal Reserve unveiled proposals Thursday that would significantly reduce capital requirements for the largest banks in the United States, potentially setting the stage for another financial industry collapse as the US-Israeli war on Iran destabilizes the global economy and jacks up prices for consumers.

Under the new rules proposed by the Fed, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency, large banks would have to hold nearly 5% less capital on average. The advocacy organization Better Markets noted that the proposals—combined with other deregulatory actions taken by the Trump administration and the Fed over the past year—would return Wall Street banks' capital requirements "to the irresponsibly low 2007 levels they had just before the 2008 crash."

“At a time of extreme and growing inequality, when tens of millions of Americans are struggling to pay their bills, today’s proposals will drain lending away from Main Street families’ needs and priorities and further enrich the already wealthy on Wall Street and the top 10% of Americans they focus on serving," Dennis Kelleher, the president of Better Markets, said in a statement. "The banking agencies’ proposals to loosen capital rules are a victory for Wall Street lobbying, and claims to the contrary are nothing more than an attempt to mislead the American people."

Fed Gov. Michael Barr, who was nominated by former President Joe Biden, was the central bank board's lone dissenting voice against the new rules, a product of years of aggressive Wall Street lobbying for less stringent regulations in the wake of the Great Recession.

"Today's proposals, if adopted, would harm the resilience of banks and the US financial system," Barr warned in a statement. "There are suggestions that liquidity requirements could also be reduced. Additionally, Federal Reserve supervisory staff have been cut by over 30%, and supervisory practices have been weakened. Banking is built on trust. I worry greatly that these actions are rapidly eroding that trust."

The new deregulatory package, which will be subject to a 90-day public comment period before it's finalized, comes as President Donald Trump is waging an expensive and deadly war on Iran with no end in sight and attacking social programs at home, from Medicaid to nutrition assistance.

“With private credit markets cratering, AI transforming the workforce, and Trump’s Iran war threatening the world economy, we need healthy, resilient, well-capitalized banks," said Bartlett Naylor, an economist for the consumer advocacy group Public Citizen. "Lessons learned after millions lost their jobs, homes, and savings following the 2008 megabank crash must not be ignored."

"Trump’s bank regulators propose to tear at the already tissue-thin layer of solvency levels at the nation’s banks," said Naylor. "Lowering solvency standards won’t generate more loans; it will only send banks closer to failure."

Matt Stoller, an anti-monopoly researcher and author of the BIG newsletter, wrote that the juxtaposition of a quagmire in Iran, Wall Street deregulation, and millions of Americans losing health insurance "tells the story" of the Trump administration.

Today's WSJ front page tells the story of the Trump admin.

#1: Hegseth Says ‘No Time Set’ on Ending Operations in Iran

#2: U.S. Regulators Propose More Lenient Capital Rules for Big Banks

#3: Millions of Americans Are Going Uninsured Following Expiration of ACA Subsidies pic.twitter.com/26jKsQuNc4

— Matt Stoller (@matthewstoller) March 19, 2026

The effort to curb banks' capital requirements was spearheaded by Fed Vice Chair for Supervision Michelle Bowman, a Trump appointee whose nomination last year was criticized by watchdogs as a "gift to the banking industry."

Kelleher of Better Markets said Thursday that "such counterproductive, shortsighted, and wrongheaded rulemaking isn’t a surprise given that the interests of Wall Street’s biggest banks are driving the priorities at the banking agencies, rather than facts, merit, and the public interest."

"The worst is at the Federal Reserve, where the senior regulatory staff comes from Wall Street’s top DC lobbyist (the Bank Policy Institute), Goldman Sachs, and one of Wall Street’s top law firms (a former partner is now the director responsible for supervising and regulating his recent Wall Street clients)," Kelleher observed. "That’s why mindless deregulation, especially for the biggest Wall Street banks, is at the top of the agenda, just as it was in the years before the 2008 crash."

Democrats have an opportunity "to raise the volume on bank reform and accountability—and be seen as challenging power on behalf of everyday people," the poll showed.

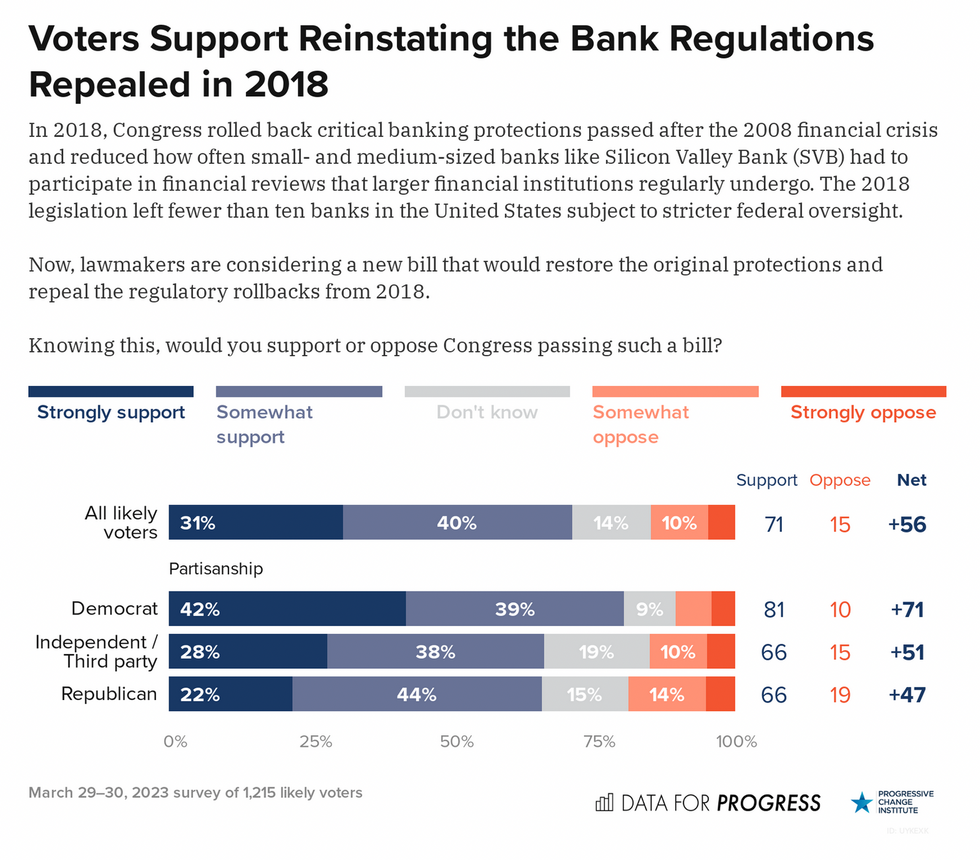

The largest U.S. bank collapse since the 2008 financial meltdown has left Americans especially eager for Congress to rein in Wall Street—and impatient with the power the financial sector has over lawmakers, according to polling released Monday.

A month after Silicon Valley Bank (SVB) failed following its decision to invest $91 billion of its deposits in long-term Treasury bonds before their value plummeted as the Federal Reserve raised interest rates, progressive think tank Data for Progress joined the Progressive Change Institute in polling 1,215 likely voters about the bank and banking regulations.

Nearly 7 in 10 respondents said they were "very" or "somewhat" concerned about the health of the banking industry following SVB's collapse, and 82% said they supported Congress taking action to strengthen banking rules in order to avoid another failure.

More than 70% said they would support the reinstatement of "critical banking rules" that were rolled back in 2018. Those rules weakened regulations for banks with between $50 billion to $250 billion in assets, and Sen. Elizabeth Warren (D-Mass.) and Rep. Katie Porter (D-Calif.) said last month that their repeal was a major driver of SVB's collapse as they introduced the Secure Viable Banking Act to impose the rules once again.

The Biden administration said after the collapse that it would take steps including creating an emergency fund to make sure all SVB deposits were covered and demanded that executives be held accountable for bonuses that were handed out in the hours before the bank failed, but 90% of respondents told Data for Progress that they had heard little or nothing about the proposed reforms.

"While voters strongly support reforms in the banking sector and the actions taken by the Biden administration in the wake of SVB's collapse, these results signal that the administration has room to expand communication on the subject and claim this issue for Democrats," said Data for Progress.

The organization noted that likely voters were more supportive of President Joe Biden's plan when told the administration had created an "emergency fund" than when the fund was described as a "bailout" and when they were told that SVB's client base, made up largely of "billionaire tech investors and multimillion-dollar companies," had been helped by the fund.

The poll indicates, said the Progressive Change Campaign Committee, that Democratic leaders have an opportunity "to raise the volume on bank reform and accountability—and be seen as challenging power on behalf of everyday people."

Jerome Powell "has failed," said Sen. Elizabeth Warren. "I don't think he should be Chairman of the Federal Reserve."

Sen. Elizabeth Warren this weekend called on federal officials to investigate the causes of recent bank failures and urged President Joe Biden to fire Federal Reserve Chair Jerome Powell, whom she has criticized for intensifying financial deregulation and imposing job- and wage-destroying interest rate hikes.

Asked on Sunday by Chuck Todd of NBC's "Meet the Press" about the possibility of Powell imposing yet another interest rate hike despite ongoing market turmoil, Warren (D-Mass.) said, "I've been in the camp for a long time that these extraordinary rate increases that he has taken on, these extreme rate increases, are something that he should not be doing."

Powell "has a dual mandate," said Warren. "Yes, he is responsible for dealing with inflation, but he is also responsible for employment. And what Chair Powell is trying to do, and he has said fairly explicitly, is that they are trying to, in effect, slow down the economy so that, this is by the Fed's own estimate, two million people will lose their jobs. And I believe that is not what the chair of the Federal Reserve should be doing."

Since the Covid-19 pandemic and Russia's invasion of Ukraine disrupted international supply chains—rendered fragile by decades of neoliberal globalization—powerful corporations in highly consolidated industries have taken advantage of these and other crises such as the bird flu outbreak to justify profit-boosting price hikes that far outpace the increased costs of doing business.

"Raising interest rates doesn't do anything to solve" a cost-of-living crisis driven primarily by "price gouging, supply chain kinks, [and] the war in Ukraine," Warren said Sunday. "All it does is put millions of people out of work."

"Jay Powell... has had two jobs. One is to deal with monetary policy, one is to deal with regulation. He has failed at both."

Powell, an ex-investment banker, was first appointed by then-President Donald Trump in 2018 and reappointed by Biden in 2021. Warren noted that she opposed Powell's nomination in both cases "because of his views on regulation and what he was already doing to weaken regulation."

"But I think he's failing in both jobs, both as the oversight and manager of these big banks, which is his job, and also what he's doing with inflation," said Warren.

Asked by Todd if Biden should fire Powell, Warren said: "My views on Jay Powell are well-known at this point. He has had two jobs. One is to deal with monetary policy, one is to deal with regulation. He has failed at both."

"Would you advise President Biden to replace him?" Todd inquired.

"I don't think he should be Chairman of the Federal Reserve," the Massachusetts Democrat responded. "I have said it as publicly as I know how to say it. I've said it to everyone."

Meanwhile, in a Saturday letter, Warren asked Richard Delmar, Tyler Smith, and Mark Bialek—respectively the deputy inspector general of the Treasury Department, acting inspector general of the Federal Deposit Insurance Corporation (FDIC), and inspector general of the Fed's board of governors—to "immediately open a thorough, independent investigation of the causes of the bank management and regulatory and supervisory problems that resulted in this month's failure of Silicon Valley Bank (SVB) and Signature Bank (Signature) and deliver preliminary results within 30 days."

Until the Treasury Department, the Fed, and the FDIC "intervened to guarantee billions of dollars of deposits," the second- and third-biggest bank failures in U.S. history "threatened economic contagion and severe damage to the banking and financial systems," Warren noted. "The bank's executives, who took unnecessary risks or failed to hedge against entirely foreseeable threats, must be held accountable for these failures."

"But this mismanagement was allowed to occur because of a series of failures by lawmakers and regulators," Warren continued.

In 2018, several Democrats joined Republicans in approving Sen. Mike Crapo's (R-Idaho) Economic Growth, Regulatory Relief, and Consumer Protection Act, which weakened the Dodd-Frank Wall Street Reform and Consumer Protection Act passed in the wake of the 2008 financial crisis. Crapo's deregulatory measure, signed into law by Trump, loosened federal oversight of banks with between $50 billion and $250 billion in assets—a category that includes SVB and Signature.

"As officials sought to develop a plan responding to SVB's failure, Chair Powell muzzled regulators from any public mention of the regulatory failures that occurred under his watch."

Moreover, the Fed under Powell's leadership "initiated key regulatory rollbacks," Warren wrote Saturday, echoing criticisms that she and financial industry watchdogs voiced earlier in the week. "And the banks' supervisors—particularly the Federal Reserve Bank of San Francisco, which oversaw SVB—missed or ignored key signals about their impending failure."

It is "critical that your investigation be completely independent and free of influence from the bank executives or regulators that were responsible for action that led to these bank failures," Warren stressed. "I am particularly concerned that you avoid any interference from Fed Chair Jerome Powell, who bears direct responsibility for—and has a long record of failure involving—regulatory and supervisory matters involving these two banks."

"I have already asked Chair Powell to recuse himself from the Fed's internal investigation of this matter, but he has not yet responded to this request," wrote Warren. The progressive lawmaker said "this silence is troubling" in light of recent reporting that "as officials sought to develop a plan responding to SVB's failure, Chair Powell muzzled regulators from any public mention of the regulatory failures that occurred under his watch."

"Bank regulators and Congress must move quickly to close the gaps that allowed these bank failures to happen, and your investigation will provide us important insight as we take steps to do so," added Warren, who has introduced legislation to repeal a vital provision of the Trump-era bank deregulation law enacted five years ago with bipartisan support.

In appearances on three Sunday morning talk shows, Warren doubled down on her demands for an independent investigation into recent bank failures, stronger financial regulations, and punishing those responsible.

After lawmakers from both parties helped Trump fulfill his campaign promise to weaken federal oversight of the banking system, Powell "took a flamethrower to the regulations, saying, 'I'm doing this because Congress let me do it,'" Warren told ABC's "This Week" co-anchor Jonathan Karl. "And what happened was exactly what we should have predicted, and that is the banks, these big, multi-billion-dollar banks, loaded up on risk; they boosted their short-term profits; they gave themselves huge bonuses and big salaries; and they exploded their banks."

"When you explode a bank, you ought to be banned from banking forever."

"When you explode a bank, you ought to be banned from banking forever," said Warren, who acknowledged that criminal charges could be coming. "The Department of Justice has opened an investigation. I think that's appropriate for them to do. We'll see where the facts take them. But we've got to take a close look at this."

Not only did former SVB chief executive officer Greg Becker, who lobbied aggressively for the 2018 bank deregulation law, sell millions of dollars of shares as recently as late last month, but until federal regulators took control of the failed bank on March 10, he was on the board of directors at the San Francisco Fed—the institution responsible for overseeing SVB.

On Saturday, Independent Sen. Bernie Sanders of Vermont announced that he plans to introduce legislation "to end this conflict of interest by banning big bank CEOs from serving on Fed boards."

"We've got to say overall that we can't keep repeating this approach of weakening the regulation over the banks, then stepping in when these giant banks get into trouble," Warren said Sunday, arguing for stronger federal oversight to prevent the need for bailouts.