SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"This could ruin people's finances, while creating a financial incentive for insurers to deny coverage," said one Democratic congresswoman.

After the Republican Party's decision to terminate subsidies that had significantly reduced healthcare costs under the Affordable Care Act for 22 million people, the White House is considering a new way to—officials claim—"help" Americans who face massive medical bills, either due to high-deductible plans that don't cover routine costs or because of emergency expenses.

The proposal, though, could just shift "who [the patients] owe the debt to," as one doctor and researcher told The New York Times, which reported Thursday on the Trump administration's proposal to allow people to take out loans directly from their health insurance companies when they can't afford to pay a hospital or doctor's office out of pocket—and then pay the insurance company back, likely with interest.

"Hard to top this level of dystopia," said one writer in response to the Times report. "Have health insurance through the ACA? The Trump administration is going to turn your health insurer into a loan shark you borrow money from if you can't afford to pay your portion of medical procedures."

As the newspaper was reported, the provision is buried in a 1,121-page final rule issued last month regarding how the ACA will be regulated next year.

The Trump administration is planning to significantly expand the number of Americans who are eligible for high-deductible "catastrophic" health insurance plans that provide no coverage for day-to-day medical expenses.

"We note that multiyear and 1-year catastrophic plans may be able to offer relief from the high deductible and maximum annual limitation on cost sharing through other mechanisms," reads the final rule. "For example, issuers of catastrophic plans could consider financing the deductible by providing enrollees a loan."

Currently, the average annual deductible for people insured under the ACA is nearly $4,000, and about 40% of enrollees this year have "Bronze" plans, which have an out-of-pocket maximum that's over $10,000 for an individual, likely leaving many people having to pay thousands of dollars in medical expenses despite having coverage.

By 2028, as Common Dreams reported earlier this year, catastrophic plans with lower premiums could have deductibles as high as $31,000 for families.

The plan to shift more people onto expensive plans that provide less coverage for day-to-day medical care—and to push patients to take out loans from their insurers—comes as about one-third of Americans, even those with insurance, report skipping meals or cutting back on other expenses to afford their medical bills.

The Times reported that at least one major health insurer—UnitedHealthcare, the nation's largest—is already equipped to start lending patients money to cover unexpected medical bills. The company operates a bank that administers loans to doctors and offers health savings accounts.

Rep. Shontel Brown (D-Ohio) said the latest proposal from the White House shows that President Donald Trump "is destroying healthcare from all sides."

The advocacy group Protect Our Care said the "suggestion" buried in the Centers for Medicare & Medicaid Services' final rule "is not only out of touch, it is cruel—accruing medical debt only adds to families’ financial burdens."

“While working families drown in the high cost of living, the Trump administration’s answer to the healthcare affordability crisis they created is to throw people an anchor made of medical debt and call it relief," said Leslie Dach, chair of Protect Our Care. "Trump and Republicans had a simple, popular fix sitting right in front of their faces—extending the ACA tax credits—but they killed it anyway, triggering premiums to double, triple, or even quadruple for millions of working families, all to make billionaires and big corporations even richer."

"Americans are being bankrupted by crushing medical debt, and this administration isn’t lifting a finger to help—it’s busy shoveling more people into that hole," said Dach. "Voters will remember this foolishness at the ballot box in November, just you wait.”

Melanie D'Arrigo, executive director of the Campaign for New York Health, which advocates for a universal, single-payer healthcare system for New York state, suggested the proposal makes the latest case for a federal, government-funded healthcare program similar to those in other wealthy countries, which would end the healthcare profit motive by expanding the existing Medicare system to the entire US population.

"Letting Americans take out loans to afford healthcare forces Americans deeper into debt and drives up profits for the health insurance industry," said D'Arrigo. "Abolish the health insurance industry. Demand Medicare for All."

One consumer advocate said the effort adds "salt to the wound" as tens of millions of people face healthcare premium spikes that are likely to worsen the nation's medical debt crisis.

The Trump administration is moving to undercut state-level efforts to wipe medical debt from Americans' credit reports, just as millions across the country are facing massive healthcare premium increases stemming from congressional Republicans' refusal to extend Affordable Care Act subsidies.

On Tuesday, according to reporting by The Lever and Bloomberg Law, the Russell Vought-led Consumer Financial Protection Bureau (CFPB) will publish a nonbinding interpretive rule arguing that federal statute "generally preempts state laws that touch on areas of credit reporting."

The guidance aligns with views expressed by a Trump-appointed federal judge in Texas who, earlier this year, vacated a Biden-era CFPB rule that would have prohibited the inclusion of medical debt on consumer credit reports. The Trump administration, which has repeatedly violated court orders, is complying with the decision.

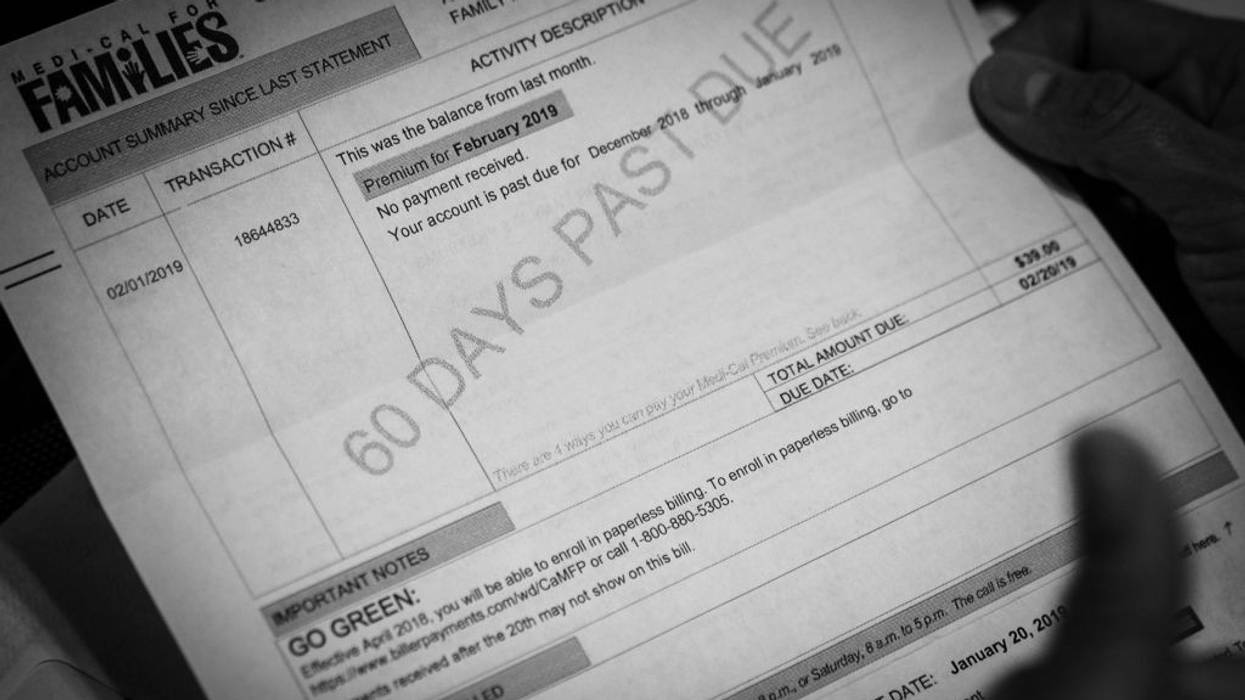

Medical debt is a growing crisis in the United States: Roughly 14 million adults owe more than $1,000 in medical debt, and an estimated 20% of Americans have medical debt on their credit reports.

Supporters of removing medical debt from credit reports argue it is not a reliable measure of creditworthiness. The Center for Consumer Law & Economic Justice at UC Berkeley notes that "medical debt often reflects the simple misfortune of getting sick unexpectedly and having to face a medical system that is rife with insurance stonewalling, delay, and mistakes."

More than a dozen states—including California, Colorado, and New York—have moved to curb the reporting of medical debt, which accounts for a significant percentage of personal bankruptcies in the US.

The Lever reported that the Trump administration's position that federal law overrides state laws is being echoed "by industry groups to advance their ongoing litigation to overturn the 15 state laws."

"For example," the outlet observed, "the Consumer Data Industry Association, which represents credit reporting companies like Equifax, Experian, and TransUnion, is likewise arguing that federal laws void state-level regulations of their conduct as part of their effort to block Maine's medical debt law."

Chi Chi Wu, an attorney at the National Consumer Law Center, told Bloomberg Law that the Trump CFPB's assault on efforts to remove medical debt from credit reports adds "salt to the wound" as tens of millions of people face surging healthcare premiums.

Writing for MSNBC over the weekend, Century Foundation president Julie Margetta Morgan warned that "the spike in premiums won't just blow an even bigger hole in families' future budgets."

"It will pour gasoline on the already raging fire of medical debt in this country," she added, "and government leaders at all levels are not prepared for it."

Medicare For All is broadly popular, supported by the majority of the population, and affects everyone in the country. So what are we waiting for?

Following the recent passage of U.S. President Donald Trump’s domestic policy agenda, there’s been a lot of discussion about how the bill will affect average Americans. One provision which has received a lot of attention in particular has been the proposed cuts to Medicaid.

Medicaid represents a crucial stopgap for working Americans, one of the few things keeping our healthcare system afloat as costs have skyrocketed. Cuts to the program could have devastating effects. For instance, many of the country’s rural hospitals (as well as nursing homes and community health clinics) rely heavily on Medicaid payments and could be forced to shut their doors without them. It’s estimated this could lead to thousands of deaths.

The Democratic Party has yet to come up with a viable alternative to this. Fortunately, there’s a solution. And it happens to be supported by the majority of Americans—embrace Medicare For All.

America is the only country in the developed world without a universal healthcare system. Our current model for care is bloated, wasteful, inhumane, and driven by corporate greed. According to a 2024 report by the Commonwealth Fund, the U.S. ranked last when compared with 10 other wealthy, industrialized nations on metrics such as life expectancy, preventable deaths, and access to care, despite spending by far the most on healthcare.

It’s essential that we transition to a system that prioritizes patient care over profit.

There are several reasons why America’s system is so expensive (high administrative costs, the government’s inability to negotiate drug prices), but one crucial reason is that we’ve opted for a patchwork system. America has four models for healthcare—one system for the workforce, one system for people over 65, one system for veterans, and no system at all for the roughly 8% of the country that remains uninsured.

Pretty much every other country has settled on one model for everyone, because it’s cheaper and less convoluted. That’s the sensible way of doing things. In 2020, a comparative analysis of 22 separate studies found that Medicare For All would save billions, if not trillions of dollars, for Americans.

Medicare For All is broadly popular, supported by the majority of the population, and affects everyone in the country. We know that it works and would do an enormous amount to relieve people’s financial burdens. The top cause of bankruptcy in America is medical debt. This program would also save tens of thousands of lives every year. If it were to pass, it might secure a voting base for the Democratic Party for at least a generation, the way Social Security and the original Medicare bill did.

It’s essential that we transition to a system that prioritizes patient care over profit. We must follow the example of every other developed country and guarantee healthcare coverage to all our citizens as a basic human right.

"This decision will hurt people's financial futures, including their ability to buy a home, care for their families, or even get a job," said the president and CEO of the nonprofit Undue Medical Debt.

A Trump-appointed judge axed a Biden-era rule on Friday that would have removed medical debt from credit reports and barred lenders from using certain medical information in loan decisions.

The rule, enacted under the authority of the Fair Credit Reporting Act, would have removed an estimated $49 billion in medical bills from the credit reports of about 15 million people.

But after a lawsuit brought by two industry groups with the support of Republicans in Congress who attempted to block it, Judge Sean Jordan of the U.S. District Court of Texas' Eastern District ruled that the Consumer Financial Protection Bureau (CFPB) had exceeded its authority in introducing the rule.

According to the CFPB, those with medical debt on their credit reports would have received a 20-point boost to their credit scores on average as a result of the rule. It would have led to an estimated 22,000 more mortgages being approved for people struggling with medical debt.

According to a report by the Peterson Center on Healthcare and KFF last year, roughly 1 in 12 adults has over $250 in unpaid medical debt.

"People who get sick shouldn't have their financial future upended," said CFPB Director Rohit Chopra at the time of the rule's passage in January 2025. "The CFPB's final rule will close a special carveout that has allowed debt collectors to abuse the credit reporting system to coerce people into paying medical bills they may not even owe."

The consumer reports industry lobbied furiously against the measure. Two industry groups—the Consumer Data Industry Association and the Cornerstone Credit Union League—brought the lawsuit before Judge Jordan. Meanwhile, reporting from Accountable.US in March revealed that Republicans on the House Financial Services Committee accepted a combined $867,000 from trade groups opposed to the rule.

Using the same talking points as the industry, they then attempted to block the rule, arguing that it would "weaken the accuracy and completeness of consumer credit reports."

However, according to research by the CFPB, medical debt on credit reports often has no bearing on a person's ability to pay back other loans.

Medical bills also frequently contain mistakes. According to a survey by the Commonwealth Fund last year, more than 45% of respondents were billed for a service they thought was covered by insurance. The trade magazine Becker’s Hospital Review, meanwhile, has estimated that 80% of medical bills contain errors that inflate costs.

"Medical debt unjustly damages the credit scores of millions, limiting their ability to obtain affordable credit, rent safe housing, or even get a job," said the National Consumer Law Center after the rule was introduced.

Now, as a result of its being struck down, the 15 million Americans who have medical debt on their credit reports will see an average of $3,200 remaining on their reports that would have otherwise been erased.

"The facts are clear: Medical debt is not predictive of creditworthiness," said Allison Sesso, the president and CEO of the nonprofit Undue Medical Debt, on Monday. "This decision will hurt people’s financial futures, including their ability to buy a home, care for their families, or even get a job—all because they got sick, injured, or were born with a chronic condition through no fault of their own. It will also further decrease their willingness to get the care they need."

The ruling also marks the latest attack by Republicans on the CFPB. In February, the Trump administration attempted to unilaterally and illegally shut down the consumer watchdog agency. His effort to dismantle it was later blocked by a federal judge.

Since its creation in 2011, the CFPB has relieved $21 billion worth of debt for nearly 200 million Americans. It recouped that money from powerful financial institutions and credit card companies that had engaged in predatory practices and saddled Americans with junk fees.

But by cracking down on corporate abuses, it became the bane of Republican lawmakers and their corporate donors. Many top Trump donors sought to kill the CFPB because it was coming after the actions of their companies.

Elon Musk's company Tesla was facing scrutiny over its auto loan policies, which had received hundreds of complaints from customers. His social media company, X, was also being examined for its payment policies.

Another top Trump donor, investor Marc Andreesen, launched a broadside against the bureau when it ordered a payday lending company he'd invested in to pay tens of millions worth of fines for engaging in predatory lending.

"Judge Sean Jordan, a Trump-appointed judge, joined congressional Republicans in making it easier for the Trump administration to raise costs on millions of Americans," said Accountable.US executive director Tony Carrk.

"Not only are they dismantling healthcare for 17 million through their big, ugly betrayal, but they're dooming millions more with low credit scores due to illness and injury," he continued. "Republicans are holding a grudge against the CFPB, and it's costing Americans money."

As we enter a period of our history defined by billionaire oligarchs and the rule of the richest, it’s more important than ever to have agencies that stand up for everyday people, not only the ultra rich class.

Imagine a high-stakes football game where one team is notorious for playing dirty, skirting the rules, and making the game about brute force, not fair play. Thank goodness for the referee, right?

Well, now imagine that right in the middle of the game, the ref gets yanked off the field. Unfortunately, that’s the situation American consumers are facing now—and the other team is free to play as dirty as they please.

Since its inception in 2010, the CFPB—the Consumer Finance Protection Bureau—has been America’s indispensable referee. It’s the fast-moving, watchful eye ensuring that big banks, online lenders, and credit agencies play fair with their customers.

Musk is trying to destroy the CFPB to enrich himself—and prevent the agency from holding him accountable for how he treats X-Money users.

But the Trump administration is now trying to kick that referee off the field—permanently.

Without the CFPB, megabanks, Big Tech, and small-time fraudsters will be free to break the rules unchecked, leaving everyday consumers defenseless in the face of the fraud, abuses, and junk fees that are so prevalent in consumer finance.

With Elon Musk’s minions in the vanguard, the Trump administration has taken its slash-and-burn approach to the CFPB, determined to dismantle any government institution that stands in the way of corporate greed. Musk and Trump are defending predators, scammers, and crooks because a strong CFPB means less profit for financial companies.

The public knows the true value of the CFPB. According to a poll from Democratic and Republican pollsters, the CFPB is popular across the country—and even across party lines. Nearly 4 in 5 people say they support the agency, including 75% of Republicans and 86% of Democrats.

The agency’s popularity is no coincidence. It’s been earned through relentless dedication to standing up for people.

Since 2010, the CFPB has won more than $21 billion in restitution and cancelled debts to consumers who were scammed by financial institutions. The CFPB has also created safeguards against future financial crises, especially in housing, and cracked down on all manner of junk fees.

Congress established the CFPB as an independent agency to protect consumers from predatory financial practices. Now we have to defend the CFPB from political sabotage. In addition to Trump’s attacks, industry-friendly lawmakers are working to weaken the CFPB, threatening its ability to keep an eye on powerful financial actors.

Congress must reject these attacks and ensure the CFPB remains ready to do the job it has done so well. That includes defending the CFPB’s independence, funding, and integrity—as well as resisting attempts to roll back existing safeguards.

A CFPB measure to limit bank overdraft fees to $5, down from the typical $35 per transaction, would save 23 million households $5 billion annually. But that rule is now on the congressional chopping block. Additionally, Congress must protect CFPB’s measure to keep medical debt off the credit reports of the 15 million Americans burdened by unexpected medical expenses.

Before the Trump administration arrived, the CFPB also created protections for the millions of users of digital payment apps and wallets to prevent fraud, safeguard people’s sensitive personal information, and prevent Big Tech and other firms from freezing or deactivating accounts without notice or explanation.

Notably, this rule would apply to the partnership between Visa and X, Elon Musk’s social network formerly known as Twitter. Now, Musk is trying to destroy the CFPB to enrich himself—and prevent the agency from holding him accountable for how he treats X-Money users.

As we enter a period of our history defined by billionaire oligarchs and the rule of the richest, it’s more important than ever to have agencies that stand up for everyday people, not only the ultra rich class. People deserve a tough, honest referee in Washington that can stand up to Wall Street and other financial predators.

If the CFPB can’t blow the whistle, there’s no doubt they will play dirty.

The agency "effectively dared the incoming Trump administration and its Republican allies in Congress to undo rules that are broadly popular," wrote one healthcare reporter.

Months after more than half of respondents to an Associated Press poll said it was "extremely or very important" for the federal government to take action to help people with medical debt, the Consumer Financial Protection Bureau on Tuesday finalized a rule to keep such debt off credit reports.

With broad public support, the rule appeared to be an uncontroversial slam dunk for the Biden administration in the last days of President Joe Biden's presidency—but Republicans, who now have majorities in Congress and are poised to take over the White House in less than two weeks, have signaled that they would take action to undo the CFPB's regulations, including the medical debt rule.

U.S. Sen. Tim Scott (R-S.C.), the new chair of the Senate Banking Committee, said last month that the CFPB should halt all rulemaking until President-elect Donald Trump takes office.

"It is paramount that President Trump can begin his administration on January 20 with a fresh slate to implement the economic agenda that the American people resoundingly voted for," Scott said.

The senator's comments suggested that Americans who voted for Trump did so in order to continue paying overdraft fees, having their personal information sold by predatory data brokers, and being penalized for owing medical bills—all of which the CFPB has taken action on since the November elections.

As Noam N. Levey wrote at KFF Health News, the CFPB on Tuesday "effectively dared the incoming Trump administration and its Republican allies in Congress to undo rules that are broadly popular and could help millions of people who are burdened by medical debt."

"People who get sick shouldn't have their financial future upended."

The new rule would remove $49 billion in unpaid medical debt from credit reports by amending Regulation V, which implements the Fair Credit Reporting Act.

Lenders are restricted from obtaining or using medical information to make lending decisions. But federal regulators have created an exception to that restriction, allowing companies to consider medical debt. The new rule ends that exception by banning medical bills on credit reports, which the CFPB said has led to a practice of using the credit reporting system to coerce payments even if bills are inaccurate, as they frequently are, according to the agency.

About 15 million people will be helped by the new regulation, said the CFPB, with credit scores of people with medical debt boosted by an average of 20 points.

An estimated 100 million Americans owe debt for healthcare they've obtained, forcing many to cut spending on groceries, housing, and other essentials.

An informal KFF Health News poll of people facing eviction or foreclosure in the Denver area in 2023 found that nearly half of people surveyed said medical debt played a role in their housing insecurity.

The inclusion of medical debt on credit reports by companies like Experian, Equifax, and TransUnion can harm Americans' ability to obtain jobs, mortgages, and rental apartments, even as CFPB research shows that medical debt is a poor predictor of whether a consumer will repay a loan.

"People who get sick shouldn't have their financial future upended," said CFPB Director Rohit Chopra. "The CFPB's final rule will close a special carveout that has allowed debt collectors to abuse the credit reporting system to coerce people into paying medical bills they may not even owe."

Billionaire Trump megadonor Elon Musk, who has become a top adviser to the president-elect and was picked to co-lead the proposed Department of Government Efficiency, has made clear that the CFPB would be a key target of the advisory body, calling for the agency to be "deleted" in November.

Despite Republicans' repeated claims that Trump will lead the party in securing an agenda that serves working families, lobbying by the credit reporting industry over the medical debt rule has made clear whose side the GOP is on.

Equifax said in August, two months after the CFPB proposed the rule, that the government is "not permitted" to regulate the industry in such a way.

House Financial Services Committee Chairman Patrick McHenry (R-N.C.) also called the proposal "regulatory overreach."

Chopra said last month that despite Republicans' objections, the CFPB would not "be a dead fish" ahead of Trump's term.

"We will continue to defend consumers' rights," he said, "and to hold companies accountable."

After UnitedHealthcare's Brian Thompson was gunned down, America’s health care powers feel and fear the U.S. public’s anger now more than ever.

Over 8,000 Americans, on average, die every day. Many of these Americans die unnecessarily. Their cause of death? The United States — our planet’s richest nation — still does not have in place a national health care system that guarantees everyone adequate medical attention.

One particular American’s death last week has refocused attention on that absence. On December 4, a gunman murdered the chief executive of a corporate insurance powerhouse that regularly registers hefty profits denying health help to sick people who desperately need it.

That chief exec — UnitedHealthcare’s 50-year-old Brian Thompson — died on a Manhattan sidewalk after a short hail of bullets from a still unidentified assassin.

The bullet casings from the shooting carried their own message. They read, according to police sources, “deny,” “defend,” and “depose,” a clear reference to the profit-first gameplan America’s giant insurers ever so relentlessly follow: deny the claim, defend the lawsuit, depose the patient.

Thompson stepped into the UnitedHealth empire over two decades ago and, notes the American Prospect journalist Maureen Tkacik, spent most of his career there “running its Medicare business, the cash cow around which much of the far-flung health care colossus essentially revolves.”

Our health care system, in the end, shouldn’t be making our rich richer.

Three years ago, Thompson became the CEO of this “cash cow,” UnitedHealth’s biggest branch. His UnitedHealthcare unit’s 140,000 employees last year pulled down over a quarter-trillion dollars — $281 billion — in revenue. That intake helped his company’s annual profits jump 33 percent over their 2021 level. Thompson himself last year pocketed $10.2 million in personal compensation.

The chief exec of the overall UnitedHealth operation, Andrew Witty, at his end collected some $23.5 million, enough to rank him the nation’s highest-paid health insurance CEO. Witty’s take-home equaled 352 times the pay of UnitedHealth’s typical employee.

What’s been making UnitedHealth’s operations so rewarding for execs at the company’s summit? UnitedHealth operates in the shadowy world of “Medicare Advantage,” the program that gives America’s senior citizens the option to contract out their Medicare to private health-service providers.

These private providers collect fixed fees from the federal government for each of the senior citizens they enroll. They make money when the cost of providing health care to those seniors amounts to less than what the U.S. Department for Health and Human Services pays them in fees. And that core reality gives private providers an ongoing incentive to limit the care their patients receive.

No Medicare Advantage provider, the American Prospect’s Maureen Tkacik points out, has done more than UnitedHealthcare to systematically seize the opportunity that incentive creates — “by simply denying claims for treatments and procedures it unilaterally deems unnecessary.” Industry-wide, Medicare Advantage providers deny 16 percent of patient claims. UnitedHealthcare, the Boston Globe has reported, last year denied patient claims at a 32 percent rate.

The massive advertising campaigns that Medicare Advantage inflict upon the American people never, of course, mention anything about denials or the limits Medicare Advantage plans place on which doctors their enrollees can see and which hospitals they can use. That advertising instead, the KFF health care think tank detailed last year, typically urges viewers to call a toll-free “Medicare” hotline that has no connection whatsoever with the federal government’s official Medicare hotline.

Many of the over 9,000 ads that Medicare Advantage outfits run daily during the annual fall open enrollment period, the KFF researchers add, misleadingly suggest that seniors may miss out on financial savings or benefits “if they don’t sign up for a Medicare Advantage plan.”

For the Medicare Advantage industry, all this advertising has paid off handsomely. Just over half of Medicare’s beneficiaries have now chosen to take privatized care over the original public Medicare.

Seniors with the good fortune to stay healthy usually don’t give their Medicare Advantage plans much of a second thought. But those seniors enrolled in Medicare Advantage who find themselves needing medical help all too often find themselves facing one frustration after another. Years of those frustrations erupted bitterly onto the national scene after Brian Thompson’s murder.

“Thoughts and deductibles to the family,” read one online reaction to a CNN posting of a shooting video. “Unfortunately my condolences are out-of-network.”

“Compassion withheld,” read another reaction, “until documentation can be produced that determines the bullet holes were not a preexisting condition.”

Within hours after Thompson’s death, a research institute at Rutgers University had found scores of similar-in-spirit posts that together reached 8.3 million viewers across multiple platforms. UnitedHealth’s official Facebook report on Thompson’s death, meanwhile, quickly drew 35,000 responses using the social networking “Haha” emoji — and only 2,200 emotes expressing “Sad.”

Some of the fiercest reactions to Thompson’s death came from within the medical community.

“This is someone who has participated in social murder on a mass scale,” a medical student wrote in one typical post.

“My patients died,” a nurse spat out in another, “while those bitches enjoyed 26 million dollars.”

“If there’s anything our fractured country seems to agree on,” mused Bloomberg’s Lisa Jarvis, “it’s that the health care system is tragically broken, and the companies profiting from it are morally bankrupt.”

“To most Americans,” agreed the New Yorker’s Jia Tolentino, “a company like UnitedHealth represents less the provision of medical care than an active obstacle to receiving it.”

That obstacle, the numbers show, has been devastatingly effective. The United States, a recent Commonwealth Fund study found, currently rates last in health among major high-income nations. Americans “die the youngest and experience the most avoidable deaths” despite living in a nation that spends almost twice as much on health care — as a share of gross domestic product — as any of its high-income peers.

Some 25 percent of Americans, Gallup polling adds, have people in their family who have had to delay medical treatment for a serious illness because they couldn’t afford the care. Some 79 percent of America’s nurses, for their part, say they’re working in inadequately staffed health facilities.

Thompson’s murder won’t change any of those stats. The system that enriched him lives on — and the incoming Trump administration figures to make that system even worse. The corporate-friendly Heritage Foundation, in its controversial Project 2025 blueprint for the second Trump term, is proposing that Medicare Advantage become the “default option” for all new Medicare enrollees.

A move along that line, notes analyst Heather Cox Richardson, would “essentially privatize Medicare” and significantly raise the program’s cost.

With Thompson’s death, America’s health care powers feel and fear the American public’s anger now more than ever. These giants, Reuters reports, have already begun enhancing the security they provide their top execs.

The challenge for the rest of us? We need to help channel the anger about health care that so many Americans feel today toward ending the system that has so failed America’s health. We need to remake health care into a vital and vibrant public service.

Our health care system, in the end, shouldn’t be making our rich richer. Our richest instead should be paying enough in taxes to help all Americans stay healthy.

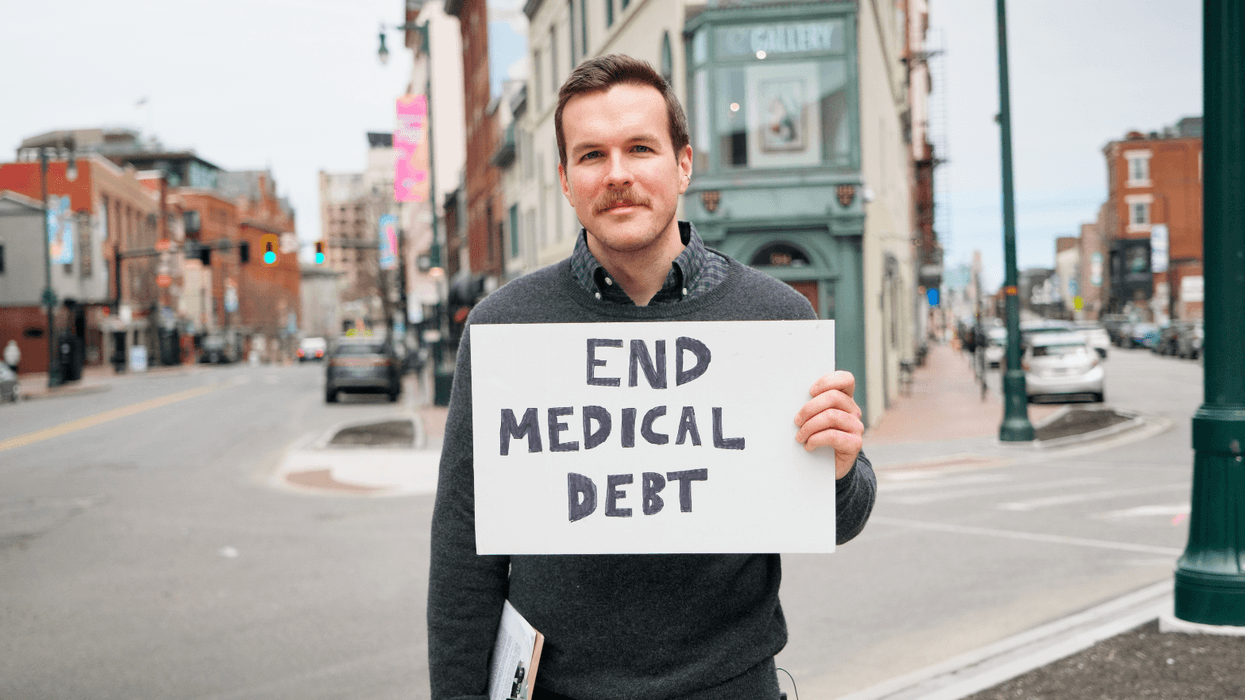

"This is just a drop in the bucket," a campaigner said. "Now, it's up to our lawmakers to make healthcare affordable for everyone in our state and to eliminate medical debt."

Mainers For Working Families, an advocacy group, announced on Thursday that it had partnered with a larger nonprofit to relieve $1.85 million worth of medical debt for 1,508 low-income people who live in Maine.

MFWF furnished a donation of $12,740 to Undue Medical Debt, a 501(c)(3) group formed by former collections executives, which bought the $1.85 million in debts; such debt is sold at pennies on the dollar.

The recipients, spread all over Maine, were people who live four times below the Federal Poverty Level or for whom medical debt totals more than 5% of their annual income.

"We can't turn back the clock for these people, but we had to do something," Evan LeBrun, MFWF's executive director, said in a statement.

"This is just a drop in the bucket," he added. "Now, it's up to our lawmakers to make healthcare affordable for everyone in our state and to eliminate medical debt."

BREAKING: Mainers for Working Families is partnering with @unduemeddebt to purchase and forgive $1.8 million in medical debt for over 1,500 Mainers across the state. pic.twitter.com/gkf4QELoiA

— Mainers For Working Families (@ForMainers) October 24, 2024

MFWF has worked on healthcare affordability issues since 2021 and medical debt since last year, a representative told Common Dreams. The group recently released a series of videos on the topic based on interviews conducted around Maine.

Undue Medical Debt formed in 2014 following inspiration from debt cancellation projects undertaken by Occupy Wall Street participants, including activist-intellectuals such as Astra Taylor and David Graeber. The nonprofit, which drew donor attention after it was featured by comedian John Oliver on his HBO show in 2016, has now canceled nearly $15 billion in medical debt, according to its website. Oliver himself made a contribution to the group, which was previously known as R.I.P. Medical Debt.

Nationwide, nearly 100 million people are dealing with unpaid medical bills, according to federal data.

The push for change in the field of medical debt has yielded a series of small victories. Last year, the three major consumer report agencies—Equifax, Experian, and TransUnion—stopped including medical debts below $500 on their credit reports, according to the Consumer Financial Protection Bureau. In June, the CFPB moved to ban all medical debt from credit reports, drawing praise from progressives such as Sen. Bernie Sanders (I-Vt.).

Vice President Kamala Harris, the Democratic presidential nominee, has pushed medical debt cancellation in her current role and pledged, as part of her economic agenda, to work with states to states to cancel more debt if she wins in November.

A working paper published by the National Bureau of Economic Research in April called into question the premise of Undue's work, finding that recipients of debt relief had no better credit scores or mental health than a control group. A co-author said the results had "disappointed" the researchers.

However, research has shown strong benefits to other forms of debt relief, and a 2023 survey conducted by Undue and other groups did show that medical debt negatively affected mental health for most people and caused 42% to delay further medical care.

Medical debt disproportionately affects people who are poor, Black, or disabled, according to Peterson-KFF Health System Tracker. About 3 million Americans have more than $10,000 in medical debt.

One is a woman named Kim, a resident of Old Town, Maine, whom MFWF interviewed in a recent video. She lives off of $26,200 per year and has roughly $2 million in debt, thanks to her fight with Addison's disease, a chronic endocrine disorder.

"I am really hoping that someone sees what is actually happening out there," she said. "God, I hope so."

Efforts to address the issue at the Maine state level have achieved mixed success. A modest reform bill that prevents debt accrual on medical debt did pass in Augusta in April.

"This for-profit system leads to higher rates of death and disease and lower life expectancies—all while Americans spend more and more trying to get the care they need."

Congresswoman Pramila Jayapal on Thursday night responded to a new analysis exposing the failures of the for-profit U.S. healthcare system by renewing her call for Medicare for All.

Jayapal (D-Wash.) and Sen. Bernie Sanders (I-Vt.) are the lead sponsors of the Medicare for All Act. When they reintroduced the bill last year, they highlighted research showing that it could save 68,000 lives and $650 billion per year.

The Commonwealth Fund report—titled Mirror, Mirror 2024: A Portrait of the Failing U.S. Health System and released Thursday—adds to the mountain of evidence that, as Jayapal said in a series of social media posts, "our healthcare is broken."

Noting that "41% of Americans hold medical debt" and "millions are uninsured," the Congressional Progressive Caucus chair declared that "we need universal, single-payer healthcare: Medicare for All."

"America's healthcare system is in dire need of an overhaul. It is largely run by private insurance companies who only care about increasing their profits and limiting choices for consumers."

As Common Dreams reported, the latest Commonwealth Fund analysis focuses on 70 health system performance measures in Australia, Canada, France, Germany, the Netherlands, New Zealand, Sweden, Switzerland, the United Kingdom, and the United States.

"All the countries have strengths and weaknesses, ranking high on some dimensions and lower on others," the report states. "Nevertheless, in the aggregate, the nine nations we examined are more alike than different with respect to their higher and lower performance in various domains. But there is one glaring exception—the U.S."

Jayapal made her case for Medicare for All with some details from the report, pointing out that "despite spending more, the U.S. ranked last in equity, access to care, and health outcomes—including acute illnesses, chronic diseases, and death. Of the countries studied, Americans live the shortest lives and face the most avoidable deaths."

"This is wholly unacceptable," she argued. "America's healthcare system is in dire need of an overhaul. It is largely run by private insurance companies who only care about increasing their profits and limiting choices for consumers."

"They refuse to pay for certain doctors, even as the average American spends tens of thousands of dollars every year on copays, deductibles, and private insurance premiums," she said. "Sometimes, they even have their own doctors override decisions about what you need for your own healthcare."

The congresswoman continued:

Medical debt and exorbitant costs regularly keep people from seeking necessary care, with a growing population of "underinsured" Americans—those who have health insurance but still aren't getting the care they desperately need.

This for-profit system leads to higher rates of death and disease and lower life expectancies—all while Americans spend more and more trying to get the care they need. In the richest nation on the planet, this simply should not and cannot be the case.

We need a system with comprehensive care for all, regardless of employment status, with no copays, deductibles, or private insurance premiums. A system where the [government] provides your insurance and doesn't allow private companies to override what your own doctor says you need.

We need comprehensive and improved Medicare for All that covers mental health, long-term care, reproductive care, dental, vision, and hearing. No hidden fees, no premiums, no copays, no deductibles. Just healthcare—when you need it, where you need it, so you can stay healthy.

"I'm so proud to be the lead sponsor of the Medicare for All Act, and I won't stop fighting until everyone can get quality healthcare without having to worry about what it might cost. Thank you so much to the 100+ members who have cosponsored our bill, H.R. 3421!" she added. "It's time for a healthcare system that actually works. Let's get Medicare for All done."

The bill, which has 14 co-sponsors in the Senate, has no chance of advancing in the current Congress and would likely face difficulty in the next one, even if Democrats won both chambers in the November election. Republican former President Donald Trump spent his first term attacking the U.S. healthcare system, while Democratic Vice President Kamala Harris has dropped her support for Medicare for All, saying recently that she wants to "maintain and grow the Affordable Care Act."

Still, patients, providers, and progressive lawmakers continue to demand a transition to a public system that serves all Americans—and Jayapal wasn't alone in pointing to the Commonwealth report as proof of the need for a major overhaul.

The other nine nations analyzed "have found [ways] to meet residents' basic healthcare needs, including universal coverage," University of California Health executive vice president Dr. Carrie L. Byington stressed on social media.

"The only clear outlier is the [United States], where health system performance is dramatically lower," Byington added. "Americans deserve better. #HealthcareForAll."

For-profit hospitals jacking up prices matches a similar story of predatory corporate practices on grocery costs and housing prices. It's not market supply and demand. Corporate giants have figured out how to rip people off more effectively.

Vice President Kamala Harris’ bold proposal to eliminate medical debt offers a window into the approach that informs the entire progressive economic agenda the Democratic nominee for President unveiled August 16.

In addition to the proposals for re-instating and expanding the child tax credit with a baby bonus for new parents, federal support for affordable housing construction and a subsidy down payment for first time home buyers, much of the new focus and attacks have centered on what the Washington Post labeled the “first ever” ban on price gouging for groceries and food.

What makes that idea especially noteworthy is its correlation to the medical debt plan and caps on prescription drug costs and rent increases. A central cause of those inflated costs goes well beyond the usual claims of supply chain bottlenecks, government spending on social programs, and the disruption of the pandemic. In every case, there is a direct link to monopolization and big corporations exploiting those factors to jack up charges to extract higher, often record, profits, well beyond their own costs to produce or provide them.

Unpacking the crisis and main source of medical debt as well as for health care costs overall, including for prescription drugs, provides the tell.

For over two decades California Nurses Association/National Nurses United researchers have studied how hospitals inflate charges over their costs. Overall, the conclusion has been that hospital profit taking, augmented by corporate mergers, is a clear driver of medical debt.

A 2020 NNU study found that some hospitals had hiked their charges by as much as 18 times over their costs, exploding profits by 411 percent over the prior two decades. NNU’s forthcoming update on hospital charges will show that some hospitals by 2022/2023 were now setting charges at almost 24 times over their costs, doubling their charges over the past 20 years. Further, the biggest for-profit hospital chains set the highest prices and make the most profits from them. Among the 100 top hospitals with the highest charges, hospital giant HCA had six hospitals alone with a combined profit of almost $400 million for that fiscal year.

Big Pharma is the gold medal winner in profiteering which is why drug costs have become such a national scandal. The U.S. Senate Health, Education, Labor, and Pensions (HELP) Committee, chaired by Sen. Bernie Sanders, issued a Majority Staff Report in February documenting how three of the biggest pharmaceutical giants, Johnson & Johnson (J&J), Merck, and Bristol Myers Squibb (BMS), have prioritized profits over patient need, collectively piling up $112 billion in profits in 2022 through “unethical pricing strategies, relentless price hikes, manipulative patent tactics, and extensive lobbying efforts.”

That lobbying blocked years of efforts to allow Medicare to use its bulk purchasing power to negotiate lower drug prices, as most other industrial countries have achieved. It’s why President Biden’s Inflation Reduction Act to permit Medicare to bargain lower prices for 10 of the highest cost drugs that treat heart disease, cancer, diabetes, and blood clots was such a dramatic success. The White House this week announced it will save millions of Medicare recipients $1.5 billion in the first year of the program.

There’s a similar story of predatory corporate practices on grocery and housing prices. No they’re not just set by market supply and demand. “Is Harris right on the economics?” asked political economist Robert Kuttner on Friday in response to the announcement of Harris' plan.

"A detailed study by Groundwork Collaborative found that corporate concentration and increased profits accounted for more than half of the inflation felt by consumers in 2022 and 2023," Kuttner wrote. "First, it vividly connects with the issue of inflation where ordinary people feel it… Second, the plan reframes the issue … to how corporate concentration opportunistically drives price hikes…Third, the approach recasts the struggle as ordinary people vs. predatory corporations.”

“Today, everywhere consumers turn, whether they are shopping for groceries at the local Kroger or for plane tickets online, they are being gouged,” wrote David Dayan and Lindsay Owens in the lead to a major American Prospect series in June. “Landlords are quietly utilizing new software to band together and raise rents.”

In the “40 years from 1979 to 2019, nonfinancial corporate profits cumulatively drove about 11.4 percent of price growth. From April to September of last year,” Dayan and Owens continued, “that number was 53 percent.” Factors include corporate concentration, high-tech pricing practices, utilizing “technological innovations such as cloud computing, artificial intelligence, and surveillance targeting” of consumers to collect extensive personal information.

Jarod Facundo described a panoply of corporate grocery pricing practices including dominance of shelf space by the biggest chains, surge pricing, repackaging goods without changing prices, and tech driven personalizing pricing “for each shopping cart” that have been “the path to higher margins,” increased costs, and, of course, bigger profits.

Food company profit increases since inflation peaked, notes former labor secretary Robert Reich, include Cal-Maine, the largest U.S. producer and distributor of fresh shell eggs, whose profits soared 471 percent. Monopolization has also driven food inflation, Reich says: Just four companies control 85 percent of beef processing, 80 percent of corn seed distribution, 77 percent of fertilizer production, and 69 percent of grocery sales.

In an investigative report in October, 2022, ProPublica’s Heather Vogell described how Texas-based RealPage’s software facilitated price inflation on rental units. “Property managers across the United States have gushed about how the company’s algorithm boosts profits,” she wrote. “The nation’s largest property management company, Greystar, used the software to price tens of thousands of apartments.”

In the American Prospect, Luke Goldstein also zeroed in on the effect of RealPage’s practices to “maximize profits” in rental markets. “Clients accept the RealPage recommendations over 80 percent of the time, and the company includes provisions in its contracts to ensure rent hikes. It heavily pushes adoption to new clients of an ‘auto-accept’ feature that forces price increases automatically.”

Corporate price gouging has not gone unnoticed by the Biden administration, as Dayen and Owens note, citing the work of its agencies to aggressively target algorithmic price-fixing, corporate mergers and other practices, such as junk fees and corporate care interest rates that spark inflation.

Harris has been a voice on those initiatives as well, which have contributed to her economic proposals today. The proposals will face considerable assault from corporate lobbyists and the politicians they influence, of course, which will require a lot of political organizing to support.

Among those praising her initiative was Sen. Sanders, as staff writer Jake Johnson reported Friday for Common Dreams. Sanders called the Harris plan “an important step forward in making our country a fairer and more just society. I look forward to working with Vice President Harris when she becomes president to implement her economic agenda, and more, within her first 100 days in office."