SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"While seemingly minor, these little annoyances add up."

Corporate profits in the US have surged in recent decades, with subscription-based businesses reporting some of the biggest revenue growth as more Americans use streaming services and sign up for "subscribe and save" models in a quest for ease and convenience.

While promising consumers that subscribing to a service will save them money and time, subscription-based businesses have made canceling the services increasingly difficult, contributing to Americans spending 60% longer on the phone with customer service lines than they did two decades ago.

And although corporations hardly need the extra money, making cancellations more arduous for customers can boost their revenue by anywhere from 14% to over 200%, according to the think tank Groundwork Collaborative, which released a report Monday on what it calls "the annoyance economy."

The labyrinthine processes that millions of Americans face each year when they try to cancel subscription services is just one part of the annoyance economy, according to Groundwork, which detailed the seemingly endless time, money, and patience people spend "just trying to get basic things done"—as well as efforts by corporations and the Trump administration to make sure it stays that way.

While millions are struggling with the rising costs of groceries, healthcare, housing, childcare, and just about everything else, the report explains how—thanks to corporate greed and a White House intent on enabling it—Americans are also shelling out at least $165 billion per year in fees as well as lost time.

In addition to cancellation processes, the annoyance economy includes the $90 billion people across the US spend every year on junk fees when they buy concert tickets, make hotel reservations, and order food delivery; rental application fees that keep people from even attempting to move to new housing that could put them closer to work or school; and administrative healthcare tasks like obtaining coverage information and resolving questions about premiums and deductibles.

"While seemingly minor, these little annoyances add up," wrote Groundwork policy fellow Chad Maisel and Stanford University economist Neale Mahoney, the authors of the report, who cited a 2019 survey that found 1 in 4 respondents delayed getting healthcare or avoided it altogether specifically because of the administrative tasks they had to complete in order to get an appointment and make sure it was covered.

"All told, American workers collectively spend about $21.6-billion-worth of time each year dealing with healthcare administration, between calls, claims, explanations, and paperwork, according to a recent analysis."

Another new poll from Data for Progress found that nearly 80% of Americans reported "at least a little frustration" when coordinating their healthcare and filling out health insurance paperwork.

"All told, American workers collectively spend about $21.6-billion-worth of time each year dealing with healthcare administration, between calls, claims, explanations, and paperwork," reads the report, citing another recent analysis. "Polling confirms this: More than 1 in 3 Americans report dealing with health insurance headaches more than 20 times per year."

With frustration over health insurance companies' practices increasingly common, reads the report, "policymakers are missing important opportunities to take on a handful of egregious and particularly annoying practices."

Lawmakers could require insurance companies to make it easy for patients to fill out and submit claims online—instead of downloading, printing, and physically mailing claim forms with itemized receipts as Cigna requires patients to do.

Congress could also create a "healthcare sludge unit" to monitor and root out "needless friction throughout the healthcare experience."

Such a project could leverage tools "like 'blind shopper' experiments, public feedback lines, and direct engagement with industry to surface and fix barriers that waste patients’ time and erode trust."

The report also takes on the spam texts and calls that have become all-to-familiar to anyone with a cellphone.

"Text messaging, once reserved for conversation with friends and family, now resembles our email spam folders, dominated by unsolicited offers from companies, politicians, and fraudsters," wrote Maisel and Mahoney, who shared that on the day they wrote about spam in the report, "one of us received five spam calls, a text from 'Victoria' offering a $500-a-day job, and two breathless fundraising messages from political candidates we’ve never supported—or even heard of."

Those spam communications were some of the more than 130 million scam and illegal marketing calls Americans receive each day and the nearly 20 billion texts that were sent each month over the past year—leading "virtually all respondents" to Data for Progress' poll to report that the calls and texts are at least "a little frustrating" and 68% call them "very frustrating."

State and federal lawmakers could and should take action against spam calls and texts, said Maisel and Mahoney. Congress should modernize the Telephone Consumer Protection Act (TCPA), which was passed in 1991—well before companies began inundating Americans' inboxes with the newest robocalling and texting software.

"If a platform automatically dials from a stored list of numbers, it’s now exempt from the TCPA’s rules," reads the report. "The result: far more robocall and spam text operations can legally target people without their consent. Congress should update the definition of autodialer to include any callers and texters who automatically contact stored numbers, unless there’s real human involvement in sending each message."

Former President Joe Biden's Federal Communications Commission tried to close the "lead generator loophole,” which allows third-party marketers to collect people's contact information and sell it to dozens, sometimes hundreds, of businesses, but companies sued over the FCC's action and won in court.

President Donald Trump could issue an executive order directing federal agencies "to leverage all available resources and authorities to end robocalls and spam texts once and for all," said Maisel and Mahoney.

But the authors noted that the Trump administration's mass layoffs across the government would make enforcement more difficult.

"The Department of Justice also needs to prioritize enforcement against bad actors," they wrote. "While the FCC can levy fines for violations, it cannot pursue their collection without the DOJ. Of the eight robocalling forfeiture orders referred by the FCC, the DOJ has pursued only two for collection."

In the case of the hoops consumers are made to jump through in order to cancel subscriptions and services, the report emphasizes that the federal government has made significant inroads before to help the public.

The Consumer Financial Protection Bureau (CFPB) intervened in 2023 and stopped Toyota Motor Credit from continuing its practice of routing all consumer calls through a hotline "where representatives were instructed to keep promoting products until a consumer asked to cancel three times, at which point they were told cancellation was only possible by submitting a written request."

Under the Biden administration, the Federal Trade Commission (FTC) was lauded by consumer advocates for its click-to-cancel rule in 2024, requiring sellers to “make it as easy for consumers to cancel their enrollment as it was to sign up."

But Trump's FTC last year delayed implementation of the rule after industry groups said that "it would take a substantial amount of time to come into compliance.” A federal appeals court then effectively killed the rule altogether.

While the fees that gradually trickle out of Americans' bank accounts into the annoyance economy are often small individually, the report emphasizes that they add up—and the consequences of these business practices and the government's failure to stop them "extend beyond wasted time and money."

"When life is reduced to jumping through an endless series of hoops—just to fix a billing error, secure a refund, or cancel a subscription—it breeds cynicism and disengagement," reads the report. "If the government can remove even a few of those obstacles, we can show the American people that someone is paying attention and begin the long process of rebuilding public trust."

"A policy of 'hear no evil, see no evil, punish no evil' is a sure-fire way to promote lawless behavior," said one advocate.

"Regulatory relief for small loan providers" was how the Trump administration described its decision not to prioritize enforcing a rule meant to protect people who are financially struggling from predatory payday lenders—but one consumer protection advocate said Monday that the announcement signals a policy that that is certain to "promote lawless behavior" by corporations.

The Consumer Financial Protection Bureau (CFPB), whose actions aimed at protecting working families and consumers from big banks and other corporations have been attacked for years by Republicans, announced last Friday that under the Trump administration, it will not enforce a rule meant to safeguard people from fees they accrue when payday lenders repeatedly attempt to debit their accounts.

Part of the 2017 payday loan rule, the bounced payment rule was set to go into effect on Sunday—barring payday lenders, "buy now, pay later" (BNPL) lending services, and other predatory lenders from continuing to make attempts to debit bank accounts after a loan customer's payment bounced twice. The lenders would be required under the rule to gain the customer's permission after two failed attempts to retrieve the payment.

When the CFPB announced last year that the rule was set to go into effect on March 30, 2025, it noted that it had "found one instance of a lender making 11 failed withdrawal attempts in one day"—subjecting the consumer to "a pile of junk fees" including nonsufficient (NSF) funds fees, overdraft charges, and others.

Adam Rust, director of financial services for the Consumer Federation of America, said Monday that the CFPB had "sided with bottom-feeder payday lenders at the expense of vulnerable borrowers struggling to make ends meet."

"The CFPB is designed to be a law enforcement agency," said Rust. "A policy of 'hear no evil, see no evil, punish no evil' is a surefire way to promote lawless behavior."

The agency said it would also not enforce rules applying to vehicle title loans, which can have high interest rates and are banned or limited in at least 30 states.

Lauren Saunders, associate director of the National Consumer Law Center, noted that former CFPB Director Kathy Kraninger, the U.S. Supreme Court, and the 5th Circuit previously upheld "the bare minimum protection against multiple NSF fees on unaffordable loans."

"It's outrageous that the CFPB will not enforce the law that prohibits payday lenders and other 200% APR lenders from continually debiting people's accounts, subjecting them to multiple NSF and overdraft fees," said Saunders. "Buy now, pay later lenders that make unaffordable loans should not be allowed to keep hitting your bank account after payments bounce twice. It's unconscionable to have greater protections for payday lenders than for people struggling to afford basic necessities."

A Pew survey in 2013 revealed that 1-in-4 payday loan customers faced an overdraft fee due to the lender's attempt to collect a payment from an account with insufficient funds.

The CFPB said it was contemplating "issuing a notice of proposed rulemaking to narrow the scope of the rule."

"By allowing payday lenders to repeatedly debit borrowers' empty bank accounts," Nadine Chabrier of the Center for Responsible Lending told Consumer Affairs, "the CFPB's political leadership is giving a free pass for payday lenders to kick people when they're down."

As we enter a period of our history defined by billionaire oligarchs and the rule of the richest, it’s more important than ever to have agencies that stand up for everyday people, not only the ultra rich class.

Imagine a high-stakes football game where one team is notorious for playing dirty, skirting the rules, and making the game about brute force, not fair play. Thank goodness for the referee, right?

Well, now imagine that right in the middle of the game, the ref gets yanked off the field. Unfortunately, that’s the situation American consumers are facing now—and the other team is free to play as dirty as they please.

Since its inception in 2010, the CFPB—the Consumer Finance Protection Bureau—has been America’s indispensable referee. It’s the fast-moving, watchful eye ensuring that big banks, online lenders, and credit agencies play fair with their customers.

Musk is trying to destroy the CFPB to enrich himself—and prevent the agency from holding him accountable for how he treats X-Money users.

But the Trump administration is now trying to kick that referee off the field—permanently.

Without the CFPB, megabanks, Big Tech, and small-time fraudsters will be free to break the rules unchecked, leaving everyday consumers defenseless in the face of the fraud, abuses, and junk fees that are so prevalent in consumer finance.

With Elon Musk’s minions in the vanguard, the Trump administration has taken its slash-and-burn approach to the CFPB, determined to dismantle any government institution that stands in the way of corporate greed. Musk and Trump are defending predators, scammers, and crooks because a strong CFPB means less profit for financial companies.

The public knows the true value of the CFPB. According to a poll from Democratic and Republican pollsters, the CFPB is popular across the country—and even across party lines. Nearly 4 in 5 people say they support the agency, including 75% of Republicans and 86% of Democrats.

The agency’s popularity is no coincidence. It’s been earned through relentless dedication to standing up for people.

Since 2010, the CFPB has won more than $21 billion in restitution and cancelled debts to consumers who were scammed by financial institutions. The CFPB has also created safeguards against future financial crises, especially in housing, and cracked down on all manner of junk fees.

Congress established the CFPB as an independent agency to protect consumers from predatory financial practices. Now we have to defend the CFPB from political sabotage. In addition to Trump’s attacks, industry-friendly lawmakers are working to weaken the CFPB, threatening its ability to keep an eye on powerful financial actors.

Congress must reject these attacks and ensure the CFPB remains ready to do the job it has done so well. That includes defending the CFPB’s independence, funding, and integrity—as well as resisting attempts to roll back existing safeguards.

A CFPB measure to limit bank overdraft fees to $5, down from the typical $35 per transaction, would save 23 million households $5 billion annually. But that rule is now on the congressional chopping block. Additionally, Congress must protect CFPB’s measure to keep medical debt off the credit reports of the 15 million Americans burdened by unexpected medical expenses.

Before the Trump administration arrived, the CFPB also created protections for the millions of users of digital payment apps and wallets to prevent fraud, safeguard people’s sensitive personal information, and prevent Big Tech and other firms from freezing or deactivating accounts without notice or explanation.

Notably, this rule would apply to the partnership between Visa and X, Elon Musk’s social network formerly known as Twitter. Now, Musk is trying to destroy the CFPB to enrich himself—and prevent the agency from holding him accountable for how he treats X-Money users.

As we enter a period of our history defined by billionaire oligarchs and the rule of the richest, it’s more important than ever to have agencies that stand up for everyday people, not only the ultra rich class. People deserve a tough, honest referee in Washington that can stand up to Wall Street and other financial predators.

If the CFPB can’t blow the whistle, there’s no doubt they will play dirty.

"This is just the latest broken promise from Republicans, who have used their short time in power to already cater to special interests over hardworking Americans," said one watchdog leader.

A U.S. watchdog group on Tuesday slammed Republicans in Congress for trying to kill the Consumer Financial Protection Bureau's overdraft rule as U.S. President Donald Trump and billionaire Elon Musk target the CFPB as a whole.

The Accountable.US statement came in response to Senate Banking Committee Chair Tim Scott (R-S.C.) and House Financial Services Committee Chair French Hill (R-Ark.) recently introducing a Congressional Review Act (CRA) resolution to overturn the rule that capped most overdraft fees at $5, which was finalized in December, near the end of the former President Joe Biden's term.

"Overdraft fees affect a huge portion of American families with 17% of households with checking accounts paying overdraft or [nonsufficient funds] fees in 2023," Accountable.US noted. "This action would open the door for $35 overdraft fees—a decision that would cost American households an average of $225 each year."

The watchdog's executive director, Tony Carrk, declared that "undoing the CFPB's overdraft fee rule is a gift to big banks and a gut punch to the wallets of millions of Americans across the country."

"Deceitful and excessive overdraft fees cost Americans billions of dollars every year, but the Trump administration and Republicans in Congress don't seem to care any longer about lowering costs for Americans now that they're in charge," he continued. "This is just the latest broken promise from Republicans, who have used their short time in power to already cater to special interests over hardworking Americans."

When the Republican chairs introduced their CRA resolution last week, Scott called the Biden-era CFPB rule an example of the "pursuit of political headlines over sound policies," and Hill described it "midnight rulemaking" and "another form of government price controls that hurt consumers who deserve financial protections and greater choice."

Meanwhile, when the CFPB finalized the rule, the agency said that it "took action to close an outdated overdraft loophole that exempted overdraft loans from lending laws." At the time, the bureau was still directed by Biden appointee Rohit Chopra, who highlighted that large banks' exploitation of the loophole had "drained billions of dollars from Americans' deposit accounts."

The rule "was scheduled to become effective in October," but "because of acting Director Russ Vought's unlawful order stalling all CFPB work, the effective date has been suspended," The American Prospect reported Monday. "If Congress passes the CRA resolution, the overdraft rule could not come back in any 'substantially similar' form. So it matters if congressional Republicans decide to support allowing banks to impose additional junk fees worth billions of dollars."

The outlet also pointed out that "because CRA resolutions cannot be stopped by a filibuster, they represent some of the most likely legislative actions of the early Trump term," given Republicans' narrow majorities in Congress."

It's not just the rule that's in jeopardy; the entire agency is at risk. Trump and Musk, the leader of the president's Department of Government Efficiency (DOGE)—though perhaps not on paper—are working to gut the federal workforce and slash spending, and they have the CFPB in their crosshairs.

An agreement reached Friday in federal court halted mass firings at the CFPB and barred the bureau and its temporary leader, Vought—who also leads the Office of Management and Budget—from purging data or defunding the agency while the case moves forward. However, Trump and Musk are expected to continue their effort.

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," Corryn G. Freeman, executive director of the youth-focused Future Coalition, said Monday. "The CFPB should be strengthened, not eliminated. If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," said the head of one advocacy group.

A national nonprofit that aims to "empower young changemakers" on Monday called out U.S. President Donald Trump and his billionaire ally Elon Musk for attacking a federal consumer financial watchdog as "part of a broader, dangerous effort to privatize and dismantle the civil service, eroding the government's ability to protect working people from corporate exploitation."

"Musk, an unelected billionaire with no constitutional authority to restructure federal agencies, is wielding his influence in the Trump administration to gut consumer protections—just as he moves to expand his own financial empire through X Money," the nonprofit, Future Coalition, said in a statement about the assault on the Consumer Financial Protection Bureau (CFPB).

"Musk, through his leadership of the Department of Government Efficiency (DOGE), has taken it upon himself to reshape federal agencies to suit his personal financial interests," the group continued. "The move to eliminate the CFPB is a glaring example of this corrupt power grab, where billionaires rewrite the rules to benefit themselves at the expense of everyday Americans."

"If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

Although the White House created confusion on Monday evening by stating in a declaration to a federal judge overseeing another case that Musk "is a senior adviser to the president" and "is not the U.S. DOGE service administrator," the world's richest billionaire is widely understood to be overseeing the Trump administration's attempts to gut the federal government.

At the CFPB specifically, that effort is currently at a standstill due to a legal challenge. A fight in federal court on Friday halted mass firings there and under the agreement, the agency and its temporary leader, Office of Management and Budget Director Russell Vought, must retain "vast troves" of data and refrain from defunding the bureau while the case proceeds.

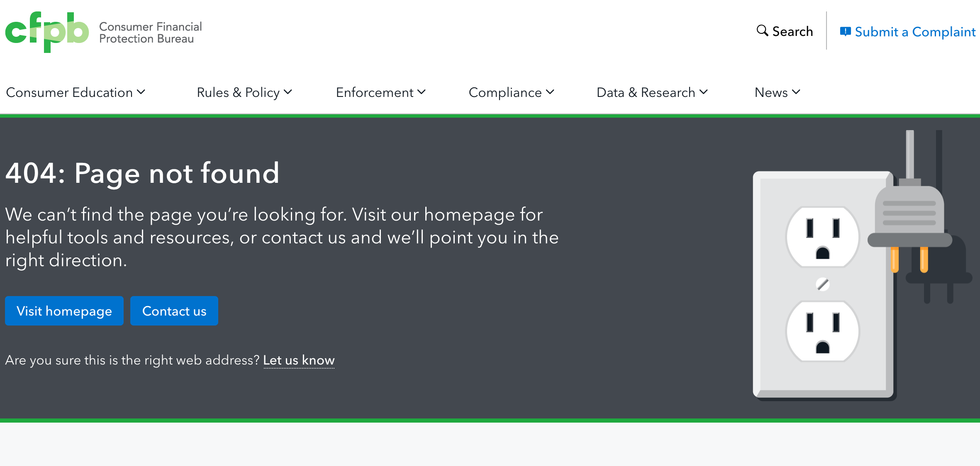

Still, there are signs that Trump and his allies will keep working to shutter the CFPB, including a "404: Page not found" message displayed on the homepage of the agency's website as of Tuesday afternoon. The message has been there for more than 10 days.

The Consumer Financial Protection Bureau's hompage displayed a "404: Page not found" message on February 18, 2025. (Photo: CFPB/screen grab)

The Consumer Financial Protection Bureau's hompage displayed a "404: Page not found" message on February 18, 2025. (Photo: CFPB/screen grab)

Critics of Trump, Musk, and DOGE continue to warn about how the "unprecedented corporate coup" targeting the CFPB would help the billionaire and various fraudsters while harming Americans. As Future Coalition highlighted Monday, anticipated consequences of ending the agency include the weakening of protections for student loan borrowers, the removal of protections against junk fees, and increases in predatory lending and financial fraud—from cryptocurrency schemes to mobile payment scams.

"Young people today are drowning in student debt, struggling to afford housing, and navigating a financial system rigged against them—yet conservative forces and big business have spent over a decade trying to dismantle the one agency designed to protect them," said Corryn G. Freeman, executive director of Future Coalition. "The CFPB is not the problem—corporate greed is."

"The same billionaires trying to kill the CFPB are the ones who profit off predatory loans, sky-high fees, and financial scams that target young people," Freeman added. "The CFPB should be strengthened, not eliminated. If Musk and his allies succeed in gutting this agency, it will be open season on young consumers with no one left to protect them."

U.S. Sen. Elizabeth Warren (D-Mass.), a former Harvard Law School professor who proposed and helped craft the CFPB before joining Congress, has delivered a similar message in recent days.

As The New Yorker's John Cassidy reported Monday:

A week ago, Elon Musk tweeted, "CFPB RIP." In short order, the Trump administration has shuttered the headquarters of the agency, halted most of its operations, and laid off some of its staff. Since Musk’s démarche, Warren—who was elected to the Senate as a Democrat from Massachusetts in 2013, and is now in her third term—has led the effort to save the CFPB, speaking at a rally outside its offices, tearing into the Tesla CEO in television interviews, and, in a Senate hearing, pressing Jerome Powell, the chairman of the Federal Reserve, to confirm that without the CFPB there is no government agency to insure that financial companies obey consumer-protection laws.

When I caught up with Warren on the phone, late last week, she recalled that prior to the creation of the CFPB, responsibility for enforcing these laws was split between six regulatory agencies. "It was nobody's first job, and nothing got done," she remarked. The founding of the CFPB brought consumer protection—regulation, supervision, and enforcement—under one roof. "For a dozen years, the CFPB has been the financial cop on the beat," Warren went on. "It has found more than $21 billion in fraud and scams, and scooped up that money and returned it directly to the people who were cheated. Now Elon Musk comes in and says, 'Let's fire the cops.' What could possibly go wrong?"

If the Trump administration succeeds in dismantling the agency, "it's open season on everyone who has a credit card, a mortgage, a car loan, a payday loan, a student loan, or uses an online financial app," Warren warned. The senator also offered a reason why the agency has faced attacks from Republicans since long before Musk decided to help Trump return to the White House.

"The CFPB is living, breathing proof, every day, that we can make government work for regular people," she said. "That we can use government to level the playing field, so that students don't get cheated on their education loans, or a family can take out a mortgage to buy a house without worrying there's a trick back on page 36 that means they are going to lose the house in two years. That's government working the way it should, and it really gets under the skins of the most extremist Republicans."

"For all the claims Trump and the GOP have made about being the voice of working-class voters, firing Chopra... only satisfies unscrupulous corporations and unelected billionaires like Elon Musk," one advocate said.

U.S. President Donald Trump moved Saturday morning to fire Consumer Financial Protection Bureau Director Rohit Chopra, who had earned the praise of consumer advocates and the ire of Wall Street for his efforts to return more than $6 billion to ordinary Americans.

Chopra announced his firing on social media, also sharing a letter to the president in which he touted the work of the CFPB and outlined possible priorities for his successor.

"Every day, Americans from across the country shared their ideas and experiences with us," Chopra wrote to his followers. "You helped us hold powerful companies and their executives accountable for breaking the law, and you made our work better. Thank you."

In his letter, Chopra mounted a full-throated defense of the CFPB, which has often been attacked by Republicans and pro-Trump figures, including billionaire Elon Musk. He wrote that the 2008 financial crisis "made Americans question whether regulators and law enforcement would hold companies and their executives accountable for their mismanagement or wrongdoing," especially since many of the companies responsible for the crash only got larger and more powerful following a taxpayer-funded bailout.

"That's what agencies like CFPB work to fix: to make sure that the laws of our land aren't just words on a page," he wrote, adding that "with so much power concentrated in the hands of a few, agencies like the CFPB have never been more critical."

Chopra, who was appointed by former President Joe Biden to head the CFPB in 2021, said that he was "proud the CFPB had done so much to restore the rule of law" during his tenure.

"Since 2021, we have returned billions of dollars from repeat offenders and other bad actors, implemented dormant legal authorities and long-overdue rules required by law, and given more freedom and bargaining leverage to families navigating a complex and confusing financial system," he wrote.

"If civil society does its job, every person unnecessarily taken advantage of by a financial institution will attribute the blame to the right person—Donald Trump."

Chopra also touted the CFPB's regulation of junk fees, inaccurate medical bills, and digital surveillance by Big Tech. Under Chopra, the CFPB sued major financial institutions such as Bank of America and JP Morgan Chase and finalized a rule to strike around $49 billion worth of medical debt from credit reports, according to CNN.

With Chopra in charge, the bureau "has fought against junk fees, repeat offenders, big tech evasions, and corporate deception. It has championed competition, transparency, accountability, and consumer financial health," Adam Rust, director of financial services for the Consumer Federation of America, said in a statement reported by NPR.

Despite the fact that Chopra was originally appointed by Trump in 2018 to serve on the Federal Trade Commission, Chopra's firing was expected as soon as Trump took office, with both major banks and tech companies urging the new president to oust him.

While anticipated, the move was criticized by progressive advocates and lawmakers.

"For all the claims Trump and the GOP have made about being the voice of working-class voters, firing Chopra and attacking the CFPB only satisfies unscrupulous corporations and unelected billionaires like Elon Musk," Revolving Door Project founder and executive director Jeff Hauser said in a statement. "If civil society does its job, every person unnecessarily taken advantage of by a financial institution will attribute the blame to the right person—Donald Trump."

Rep. Pramila Jayapal (D-Wash.) called his firing "an enormous loss for the American people."

"My friend Rohit Chopra has done an incredible job leading the CFPB—standing up to big corporations, protecting consumer data, and saving money for poor and working families," Jayapal said on social media.

Former Labor Secretary Robert Reich wrote on social media: "Under Rohit Chopra's tenure, the CFPB continued to serve as a shining example of government working on behalf of the people. Chopra took on corporate greed, unnecessary junk fees, predatory lending, and other financial shenanigans. It's telling that Trump just fired him."

According to The New York Times, the CFPB under Trump is expected by financial industry officials to roll back some of Chopra's regulations and to issue fewer new rules and weaken enforcement.

However, Sen. Elizabeth Warren (D-Mass.) pointed out that this would run counter to Trump's own campaign rhetoric.

"President Trump campaigned on capping credit card interest rates at 10% and lowering costs for Americans. He needs a strong CFPB and a strong CFPB director to do that," she said in a statement. "But if President Trump and Republicans decide to cower to Wall Street billionaires and destroy the agency, they will have a fight on their hands."

Chopra himself, in his farewell letter to Trump, suggested steps the CFPB could take under new leadership. These included:

"We have also analyzed your promising proposal on capping credit card interest rates, and we see a path for enacting meaningful reform," he wrote to Trump. "I hope that the CFPB will continue to be a pillar of restoring and advancing economic liberty in America."

The Massachusetts Democrat has proposals on healthcare programs, Pentagon contracts, tax reform, and more.

While U.S. President Donald Trump's Department of Government Efficiency has faced intense criticism and even multiple lawsuits, some progressive groups and lawmakers are also engaging, including Sen. Elizabeth Warren on Thursday.

When Trump announced DOGE in November, he said the presidential advisory commission would work to "slash excess regulations, cut wasteful expenditures, and restructure Federal Agencies." Warren (D-Mass.) on Thursday detailed 30 proposals that would cut at least $2 trillion of government spending over the next decade.

In a lengthy letter to the chair of DOGE, billionaire Elon Musk, that was first reported by Time, Warren highlighted that "you have publicly called for sizable cuts in funding—from $500 billion in annual spending to 'at least' $2 trillion in cuts to federal spending—although recently, you said you may not actually be able to meet that goal."

"I have very serious concerns about both the DOGE process and the policies that you have publicly discussed to date," she wrote. "With regard to process, as I raised in a still-unanswered letter to President-elect Trump regarding Mr. Musk sent on December 16, 2024, it is not clear that you and other DOGE leaders are able to identify and mitigate your conflicts of interest and adhere to commonsense ethics standards. As a result, the committee appears to be a venue for corruption, allowing well-connected billionaires to put government policies in place that enrich them while hurting ordinary Americans."

"I am disturbed by the dangerous proposals you have discussed and released to date: proposals from you and your allies to cut Medicare, Medicaid, Social Security, veterans' benefits, and other programs."

"With regard to policy, I am disturbed by the dangerous proposals you have discussed and released to date: proposals from you and your allies to cut Medicare, Medicaid, Social Security, veterans' benefits, and other programs that tens of millions of Americans count on and rely on are unrealistic and cruel. It would be outrageous to cut these programs in the name of government thriftiness while handing out trillions of dollars in tax cuts for billionaires and big corporations," she continued. "But, your broad point—that the federal government spends trillions of dollars on wasteful spending is correct. And if you are serious about working together in good faith to cut government spending—in a way that does not harm the middle class—I have proposals for your consideration."

The letter features several recommendations to cut spending at the U.S. Department of Defense, which has never passed an audit. Specifically, it says: negotiate better contracts, recreate a renegotiation board to challenge excess profits, stop using the military to perform civilian jobs, end corporate welfare for Pentagon contractors and foreign governments, instruct the agency to stop gaming the budget process, boost energy efficiency and industry competition, tackle repair restrictions on military equipment, and "avert wasteful government spending on plutonium pit production at the Savannah River Site."

Warren also has suggestions for federal healthcare programs, such as curbing taxpayer abuse by Medicare Advantage insurers, engaging in more Medicare negotiations to lower prescription drug costs, supporting efforts to crack down on pharmacy benefit managers, quashing patent abuses by the pharmaceutical industry, exercising march-in rights to reduce medication prices, breaking up conglomerates, and keeping private equity out of the industry.

To save on education, the senator called for eliminating or reducing funding for the federal Charter Schools Program and making for-profit colleges ineligible for federal grant aid. On the taxation front, she advised fully funding the Internal Revenue Service as well as clawing back tax expenditures and closing loopholes for the wealthy.

Her letter further suggests keeping the federal government's cloud and other information technology markets competitive, reducing waste in unnecessary federal arrests and detention programs, and working with the Government Accountability Office, inspector general offices, and other watchdogs "to detect and combat fraud, waste, and abuse."

"DOGE's agenda has focused on limiting the size of the federal government to increase efficiency and save taxpayer dollars. As the list above indicates, there are many opportunities for identifying savings that would not hurt the middle class, and that would eliminate wasteful special interest spending," Warren wrote. "But focusing solely on cutting federal budgets is myopic and counterproductive, and misses key ways in which the government can cut costs for ordinary Americans, saving them billions of dollars."

"For example, the federal government should continue its efforts to target abusive surprise fees charged by businesses across the economy," she noted, pointing to rules from the Consumer Financial Protection Bureau, U.S. Department of Transportation, and Federal Trade Commission (FTC) targeting "junk fees."

Empowering the U.S. Department of Justice and the FTC "to break up monopolies and ensure competition would have extraordinary benefits for families," the senator wrote. She also argued that "DOGE should ensure that federal agency contracts do not create monopolies that can hike prices for small businesses and consumers indefinitely."

"By making the tax code fairer, DOGE recommendations could provide a roadmap for additional government revenues that could be used for important investments or to cut the deficit," she added, spotlighting the anticipated benefits of ending tax breaks and loopholes for offshoring jobs and profits, raising the corporate tax rate and the corporate alternative minimum tax rate, and enacting her "Ultra-Millionaire Tax."

"In the interest of taking aggressive, bipartisan action to ensure sustainable spending, protect taxpayer dollars, curb abusive practices by giant corporations, and improve middle-class Americans' quality of life," Warren concluded, "I would be happy to work with you on these matters."

Warren's letter followed an

MSNBC op-ed that Rep. Ro Khanna (D-Calif.) wrote in December, offering Musk some recommendations, and a report that the watchdog Public Citizen released earlier this month identifying "what an efficiency agenda based on evidence, not ideology, would include," in the words of the group's co-president, Robert Weissman, who has formally requested to join DOGE to serve as a voice "for the interests of consumers and the public."

While some of Warren, Khanna, and Public Citizen's proposals could win bipartisan support, many would likely be met with strong resistance from the Trump White House and Republican-controlled Congress. As

Time put it, "Her missive might do more to make a point than spur an improbable collaboration."

Andrew Ferguson has opposed several major initiatives championed by Lina Khan, including FTC rules banning anti-worker noncompete agreements and making it easier for consumers to cancel subscriptions.

President-elect Donald Trump's pick to lead the Federal Trade Commission cast the lone no vote Tuesday against a newly finalized rule banning deceptive junk fees in live-event ticketing and short-term lodging.

The rule, according to an FTC release, "targets specific and widespread unfair and deceptive pricing practices in the sale of live-event tickets and short-term lodging, while preserving flexibility for businesses."

"It does not prohibit any type or amount of fee, nor does it prohibit any specific pricing strategies," the agency said. "Rather, it simply requires that businesses that advertise their pricing tell consumers the whole truth up-front about prices and fees."

FTC Commissioner Andrew Ferguson, Trump's choice to head the bipartisan agency, was the only member to vote against the junk fees rule. In his dissenting statement, Ferguson wrote that his opposition had "nothing to do with the merits" of the finalized rule but was rather a vote against any additional rulemaking by the Biden administration.

"It is particularly inappropriate for the Biden-Harris FTC to adopt a major new rule that it will never enforce, as the final rule will not take effect until many months after President Trump takes his oath of office," Ferguson wrote.

Ferguson has been a consistent opponent of causes championed by FTC Chair Lina Khan, including the agency's rules banning anti-worker noncompete agreements and making it easier for consumers to cancel subscriptions.

Nidhi Hegde, interim executive director of the American Economic Liberties Project, said in response to the newly finalized rule that "banning junk fees is broadly popular across the country because Americans are tired of being tricked by hidden costs that inflate prices and distort competition."

"Finalizing this rule with bipartisan support demonstrates Chair Khan and the commission's commitment to delivering real results for consumers, saving Americans both time and money," said Hegde. "We're pleased to see the FTC work to get this done, and encourage federal and state policymakers to build on this effort to put an end to junk fees once and for all."

With his dissent on Tuesday, Ferguson offered a glimpse of "how he plans to lead the FTC—and how the Trump administration plans to run the independent agencies put in the crosshairs by the Project 2025 plan," political reporter Matt Sledge wrote for The Intercept on Wednesday.

"While calling on the FTC to stop issuing rules until Trump takes office might win favor with the incoming president, it is sharply at odds with positions on the agency's independence that Republicans were putting out just weeks ago," Sledge noted. "As recently as October, the House Oversight Committee released a report dinging Khan for a supposed lack of independence from the Biden administration."

"Since Trump's election, however, Republicans have shown newfound enthusiasm for the idea of bringing independent agencies under executive control," he added. "That vision was laid out in Project 2025."

Since he's already a commissioner at the agency, Ferguson will not require Senate confirmation to become FTC chair once Trump takes office next month.

In his job pitch to Trump's team, Ferguson pledged to use his tenure as FTC chair to "reverse Lina Khan's anti-business agenda" and halt her "war on mergers."

One advocate called the CFPB's new rule "a major milestone in its effort to level the playing field between regular people and big banks."

The Consumer Financial Protection Bureau, one of President-elect Donald Trump's top expected targets as he plans to dismantle parts of the federal government after taking office in January, announced on Thursday its latest action aimed at saving households across the U.S. hundreds of dollars in fees each year.

The agency issued a final rule to close a 55-year-old loophole that has allowed big banks to collect billions of dollars in overdraft fees from consumers each year,

The rule makes significant updates to federal regulations for financial institutions' overdraft fees, ordering banks with more than $10 billion in assets to choose between several options:

The final rule is expected to save Americans $5 billion annually in overdraft fees, or about $225 per household that pays overdraft fees.

Adam Rust, director of financial services at the Consumer Federation of America, called the rule "a major milestone" in the CFPB's efforts "to level the playing field between regular people and big banks."

"No one should have to pick between paying a junk overdraft fee or buying groceries," said Rust. "This rule gives banks a choice: they can charge a reasonable fee that does not exploit their customers, or they can treat these loan products as an extension of credit and comply with existing lending laws."

The rule is set to go into effect next October, but the incoming Trump administration could put its implementation in jeopardy. Trump has named billionaire Tesla CEO Elon Musk to co-lead the Department of Government Efficiency, an advisory body he hopes to create. Musk has signaled that he wants to "delete" the CFPB, echoing a proposal within the right-wing policy agenda Project 2025, which was co-authored by many officials from the first Trump term.

"The CFPB is cracking down on these excessive junk fees and requiring big banks to come clean about the interest rate they're charging on overdraft loans."

"It is critical that incoming and returning members of Congress and President-elect Trump side with voters struggling in this economy and support the CFPB's overdraft rule," said Lauren Saunders, associate director at the National Consumer Law Center (NCLC). "This rule is an example of the CFPB's hard work for everyday Americans."

In recent decades, banks have used overdraft fees as profit drivers which increase consumer costs by billions of dollars every year while causing tens of millions to lose access to banking services and face negative credit reports that can harm their financial futures.

The Federal Reserve Board exempted banks from Truth in Lending Act protections in 1969, allowing them to charge overdraft fees without disclosing their terms to consumers.

"For far too long, the largest banks have exploited a legal loophole that has drained billions of dollars from Americans' deposit accounts," said CFPB Director Rohit Chopra. "The CFPB is cracking down on these excessive junk fees and requiring big banks to come clean about the interest rate they're charging on overdraft loans."

Government watchdog Accountable.US credited the CFPB with cracking down on overdraft fees despite aggressive campaigning against the action by Wall Street, which has claimed the fees have benefits for American families.

Accountable.US noted that Republican Reps. Patrick McHenry of North Carolina and Andy Barr of Kentucky have appeared to lift their criticisms of the rule straight from industry talking points, claiming that reforming overdraft fee rules would "limit consumer choice, stifle innovation, and ultimately raise the cost of banking for all consumers."

Similarly, in April Barr claimed at a hearing that "the vast majority of Americans" believe credit card late fees are legitimate after the Biden administration unveiled a rule capping the fees at $8.

"Americans pay billions in overdraft fees every year, but the CFPB's final rule is putting an end to the $35 surprise fee," said Liz Zelnick, director of the Economic Security and Corporate Power Program at Accountable.US. "Despite efforts to block the rule and protect petty profits by big bank CEOs and lobbyists, the Biden administration's initiative will protect our wallets from an exploitative profit-maximizing tactic."

The new overdraft fee rule follows a $95 million enforcement action against Navy Federal Credit Union for illegal surprise overdraft fees and similar actions against Wells Fargo, Regions Bank, and Atlantic Union.

Consumers have saved $6 billion annually through the CFPB's initiative to curb junk fees, which has led multiple banks to reduce or eliminate their fees.

"Big banks that charge high fees for overdrafts are not providing a courtesy to consumers—it's a form of predatory lending that exacerbates wealth disparities and racial inequalities," said Carla Sanchez-Adams, senior attorney at NCLC. "The CFPB's overdraft rule ensures that the most vulnerable consumers are protected from big banks trying to pad their profits with junk fees."

"When the Consumer Financial Protection Bureau is allowed to fully do its job, Americans only stand to benefit."

In the coming weeks, as President-elect Donald Trump's second term approaches and his pledge to dismantle key agencies potentially comes closer to fruition, 4.3 million consumers are set to receive checks from one of the agencies the incoming administration wants to "delete."

The Consumer Financial Protection Bureau (CFPB) announced Thursday that it will soon begin distributing a historic $1.8 billion to millions of people who were charged illegal junk fees or defrauded by credit repair companies including Lexington Law and CreditRepair.com.

The money will be distributed from the CFPB's victim relief fund, which was created by Congress and is financed entirely by civil penalties paid by companies and individuals who violate consumer financial protection laws.

The fund has distributed $3.3 billion to consumers since its inception, and the CFPB said the forthcoming payment will be its largest ever.

"Lexington Law and CreditRepair.com exploited vulnerable consumers who were trying to rebuild their credit, charging them illegal junk fees for results they hadn't delivered," said CFPB Director Rohit Chopra. "This historic distribution of $1.8 billion demonstrates the CFPB's commitment to making consumers whole."

A district court ruled in August 2023 that the two companies had violated the Telemarketing Sales Rule's prohibition on advance fees, which bars credit repair firms from collecting fees from consumers until they prove they have achieved the results they promise to their customers.

If the CFPB payments are divided equally among those who were wrongly charged fees by the two companies, each consumer would receive about $419.

The payments are being sent days after the CFPB proposed a rule aimed at reining in data brokers who sell people's personal information.

As Common Dreams reported, billionaire entrepreneur Elon Musk has expressed concern about the practices of data brokers—but as Trump's nominee to co-lead the Department of Government Efficiency (DOGE), a yet-to-be-created commission that would cut regulations and government spending, Musk has pledged to "delete" the CFPB.

Filmmaker and media activist Danny Ledonne said Musk and Vivek Ramaswamy, another businessman nominated to lead DOGE, likely want to do away with the CFPB because the agency acts "in the interest of regular people."

Liz Zelnick, director of the Economic Security and Corporate Power Program at government watchdog Accountable.US, said the upcoming $1.8 billion payout shows why the CFPB should remain in operation.

"When the Consumer Financial Protection Bureau is allowed to fully do its job, Americans only stand to benefit," said Zelnick. "Between surprise fees and misleading business practices, today's victory affirms the importance of the CFPB for defending people across the country from shady industry actors."

Rep. Mark Pocan (D-Wis.) said supporters of consumer protections in Congress will "fight any attempts to dismantle [CFPB], whether from Trump, Musk, or their billionaire buddies."

"The CFPB fights for everyday Americans against corporate greed, junk fees, and predatory lenders," he said. "This watchdog agency protects normal people like you and me."