SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"No surprise at all, but still shocking news. Will temperatures drop below 1.5°C again? I have my doubts," said one climate scientist.

Data from the first 11 months of 2024 reaffirmed that the globe is set to pass a grim milestone this year, according to the European Union's earth observation program.

The E.U.'s Copernicus Climate Change Service (C3S) said in a report Monday that November 2024 was 1.62°C above the preindustrial level, making it the 16th month in a 17-month stretch during which global-average surface air temperature breached 1.5°C. November 2024 was the second-warmest November, after November of last year, according to C3S.

"At this point, it is effectively certain that 2024 is going to be the warmest year on record and more than 1.5°C above the pre-industrial level," according to a Monday statement from C3S. With data for November in hand, the service estimates that global temperature is set to be 1.59°C above the pre-industrial level for 2024, up from 1.48°C last year.

C3S announced last month that 2024 was "virtually certain" to be the hottest year on record after October 2024 hit 1.65°C higher than preindustrial levels.

"This does not mean that the Paris Agreement has been breached, but it does mean ambitious climate action is more urgent than ever," said Samantha Burgess, deputy director of C3S.

Under the 2015 Paris agreement, signatory countries pledged to reduce their global greenhouse gas emissions with the aim of keeping global temperature rise this century to 1.5ºC, well below 2°C above preindustrial levels. According to the United Nations, going above 1.5ºC on an annual or monthly basis doesn't constitute failure to reach the agreement's goal, which refers to temperature rise over decades—however, "breaches of 1.5°C for a month or a year are early signs of getting perilously close to exceeding the long-term limit, and serve as clarion calls for increasing ambition and accelerating action in this critical decade."

Additionally, a recent paper in the journal Nature warned of irreversible impacts from overshooting the 1.5ºC target, even temporarily.

Climate scientist and volcanologist Bill McGuire reacted to the news Monday, saying: "Average temperature for 2024 expected to be 1.60°C. A massive hike on 2023, which itself was the hottest year for probably 120,000 years. No surprise at all, but still shocking news. Will temperatures drop below 1.5°C again? I have my doubts."

The update comes on the heels of COP29, the most recent U.N. climate summit, which many climate campaigners viewed as a disappointment. During the summit, attendees sought to reach a climate financing agreement that would see rich, developed countries contribute money to help developing countries decarbonize and deal with the impacts of the climate emergency. The final dollar amount, according to critics, fell far short of what developing countries need.

"By the end of the UN climate talks, we must see at least a trillion dollars in public finance on the table," said one campaigner.

As the clock winds down at the UN climate summit taking place in Baku, Azerbaijan, green groups are sounding the alarm Thursday following the release of a draft climate finance deal that they say falls short of what's needed to support climate-vulnerable countries and adequately address the planetary crisis.

"The clock is ticking. COP29 is now down to the wire," said UN Secretary-General António Guterres on Thursday, just a day before the two-week conference is set to conclude.

Finance has been a major focus of this year's summit. Under the 20125 Paris Agreement, countries are supposed to come up with a "new collective quantified goal"—or NCQG in COP jargon—that will govern how much money from rich countries will be transferred to developing countries in order to help the latter cut their emissions and adapt to climate change.

No equivalent climate finance arrangement has been agreed to before, though countries at the summit broadly agree that richer countries, who are responsible for much of historic CO2 emissions, should help poorer and more climate-vulnerable nations deal with natural disasters and their transition to green energy.

The draft text that dropped early Thursday, however, was received poorly.

Oxfam International's climate justice lead, Safa’ Al Jayoussi, said "COP29 must do more than simply repeat the same threadbare promises. Rich countries have spent decades now stalling and blocking genuine progress on climate finance. This has left the Global South suffering the most catastrophic consequences of a climate crisis they did not create. The draft text scandalously misses the crucial element of declaring a clear public commitment to a new climate finance goal."

Instead of specifying how much annually should be funneled towards developing countries via climate finance, the NCQG draft text displayed "X" in place of any actual figures or monetary commitments.

Oscar Soria, a director at the Common Initiative think tank, told the Guardian: "The negotiating placeholder 'X' for climate finance is a testament of the ineptitude from rich nations and emerging economies that are failing to find a workable solution for everyone."

"By the end of the UN climate talks, we must see at least a trillion dollars in public finance on the table," added Andreas Sieber, 350.org associate director of policy and campaigns. Economists told the summit attendees last week that developing countries need at least $1 trillion annually by 2030 to deal with climate change.

A specific and shared concern from campaigners was the draft text's inclusion of carbon market schemes as a way "to scale up" climate finance. While the draft promotes "high-integrity voluntary carbon markets" and other "instruments that mobilize new sources of climate finance and private finance" as part of the equation, critics have long warned that these market-based approaches are nothing but false solutions designed to benefit corporate investors, wealthier nations, and the fossil fuel industry itself.

"Labelling carbon credits as climate finance—which they are unreservedly not—should be axed from the text or risk creating a dangerous escape route for polluters. The same goes for explicitly allowing investments in fossil fuel infrastructure. This is fundamentally incompatible with the goals of the Paris Agreement," said Laurie van der Burg, Oil Change International's global public finance manager, in response to the draft text.

While Article 6 of the Paris Agreement allows for the international transfer of carbon credits, groups warned the changes in the COP29 draft would dramatically strengthen the foothold of such schemes.

"Shockingly, COP29 is set to agree to carbon markets that are even worse than the voluntary carbon markets," said Kirtana Chandrasekaran, a climate campaigner with Friends of the Earth International. "We know these markets have failed. They are riddled with fraud and they do not reduce emissions or provide finance. Communities everywhere and, in fact, the planet itself is on the line."

Without addressing these concerns, advocates of a meaningful deal at the conference say COP29 is headed for failure.

As 350.org's Sieber argued, paying the "historic debt that rich countries owe will enable all nations to take action on climate at home and meet the collective goal agreed last year at COP28—to triple renewable energy, and transition away from fossil fuels. Right now, we only see cowardice and a void in leadership, ignoring the undeniable science that we can't keep polluting our planet with dirty oil, gas and coal."

"The time to course correct is now—the European Union and other rich countries must stop playing poker with the planet and humankind's future at stake," Sieber added. "It's time to put their cards on the table and commit real, transformative funding—no more excuses, no more delays, it's time."

Indebted middle-income countries like Ukraine should not be expected to subsidize IMF lending when better alternatives exist. And the U.S. has more than enough influence to help the international lending body change course on these counterproductive policies.

The United States has a chance to save Ukraine billions of dollars, and at no cost to U.S. taxpayers, by pushing for an end to the unfair and harmful surcharge policy of the International Monetary Fund (IMF).

The IMF is currently reviewing this surcharge policy, which hits Ukraine—and other highly indebted borrowers like Kenya, Ecuador, Argentina, Barbados, and Egypt—with additional charges on top of standard interest and service fees. Human rights and development experts consider surcharges to be counterproductive and contrary to international human rights law. The IMF should take this opportunity to permanently end its surcharge policy for highly indebted borrowers.

Surcharges are penalty fees levied on middle-income countries with high levels of IMF debt. There are two types of surcharges exacted by the IMF: level-based surcharges and time-based surcharges. Level-based surcharges add 2 percentage points in fees to a country’s outstanding IMF credit when it surpasses 187.5% of a country’s quota to the Fund. Time-based surcharges add another percentage point of fees when a country’s IMF debt exceeds this threshold for over 36 or 51 months, depending on the lending facility. Some countries, including Ukraine, are paying both surcharges, amounting to an additional 3% points of fees.

In Ukraine’s case, surcharges will add nearly $3 billion to the war-ravaged country’s debt burden over the next decade even as it needs an estimated $9.5 billion in emergency financing for recovery and reconstruction just this year.

The IMF and Treasury Secretary Yellen have previously claimed that surcharges incentivize timely repayment to the IMF. However, countries are struggling to repay the IMF due to exogenous shocks, not a lack of appropriate incentives. Surcharges are counterproductive as they push countries facing crises—including war, the COVID-19 pandemic, and climate disaster —further into debt. It is no coincidence that, prior to the pandemic, only eight countries were paying IMF surcharges; today 23 countries are paying these fees.

In Ukraine’s case, surcharges will add nearly $3 billion to the war-ravaged country’s debt burden over the next decade even as it needs an estimated $9.5 billion in emergency financing for recovery and reconstruction just this year. Experts say efforts to relieve Ukraine’s debts could change the course of the war. Ukraine recently reached a much-needed deal to restructure its debts. Keeping surcharges in place would diminish the benefits of this restructuring, as it sends $3 billion that could be spent on recovery, reconstruction, and defense back to the IMF. Surcharges have already cost Ukraine $621 million between 2018 and 2023. Discontinuing surcharges would save Ukraine billions of dollars in its hour of need.

Following intense criticism of surcharges by leading economists, developing countries, and U.S. members of Congress, the IMF announced earlier this year that it would carry out a review of the controversial policy. Following consultations with IMF stakeholders— in particular, the US Treasury Department—the Fund is expected to announce the results of its review, and any recommendations of changes to the policy, before the IMF’s Annual Meetings in October. It’s worth noting that the IMF has previously recognized the profoundly harmful and counterproductive consequences of similar past policies, moving to discontinue them in 1974, 1981, and 1992.

Yet, among wealthy countries, there appears to be resistance to terminating, or even significantly reforming, the current surcharge policy. It is particularly troubling that much of this resistance appears to be rooted in the hope that the income from surcharges can supplement projected funding shortfalls for the IMF’s Poverty Reduction and Growth Trust (PRGT) facility, which offers low-income countries interest-free and concessional loans. The IMF, the US Treasury, and other observers have previously discussed surcharges as a source of income for IMF lending via the PRGT.

Among wealthy countries, there appears to be resistance to terminating, or even significantly reforming, the current surcharge policy.

Post-pandemic funding needs have depleted PRGT resources and the program is in need of replenishment. It may be necessary for the IMF to increase its lending through the PRGT in response to the growing needs of developing countries. However, squeezing highly indebted countries such as Ukraine to do so would be a perverse solution. These same middle-income countries have also largely been left out of pandemic-related debt relief initiatives and are struggling to recover under the weight of a failing international financial architecture. Funding for the PRGT shouldn’t come at the expense of these countries.

There are better and more effective alternatives to relying on surcharges to fund the PRGT. These include: donations from the U.S. and other advanced economies, gold sales, and changes to the IMF’s internal accounting practices. Surcharges are infinitesimal compared to the IMF’s much-vaunted $1 trillion lending firepower. The IMF has vast reserves of gold that remain largely undervalued. These gold reserves are currently valued at the 1960s rate of approximately $47 per ounce. Valued at current market rates of approximately $2,556 per ounce, the IMF’s gold reserves would be worth $228 billion. The IMF could sell a portion of these reserves or adopt mark-to-market accounting practices to fund the PRGT.

Indebted middle-income countries like Ukraine should not be expected to subsidize PRGT lending when better alternatives exist. A permanent end to surcharges would eliminate an increasingly significant barrier to sustainable recovery in many developing countries. Given that the U.S. holds a de facto veto over IMF policy changes, the stance of the U.S. Treasury Department will be instrumental. Refusing to change the surcharge policy today would be a major missed opportunity for Secretary Yellen and the world.

The United States' contribution of $17.5 million, in particular, was denounced as "embarrassing" for the wealthiest country in the world.

International campaigners who for years have demanded a global "loss and damage" fund to help developing countries confront the climate emergency were encouraged on Thursday as the 28th United Nations Climate Change Conference began with an agreement to make the fund operational—but said the details of the deal made clear that wealthy countries are still largely abandoning communities that have contributed the least fossil fuel emissions, only to suffer the worst climate injustices.

A recent study from the University of Delaware showed that "the unweighted percentage of global GDP lost" due to climate impacts such as long-lasting drought, catastrophic flooding, and wildfires is estimated at 1.8%, or about $1.5 trillion, and low- and middle-income countries "have experienced $2.1 trillion in produced capital losses due to climate change."

To meet the need, developing countries have said they already require about $400 billion annually in a loss and damage fund that could help governments rebuild communities, restore crucial wildlife habitats, or relocate people who have been displaced by the climate emergency—so advocates on Thursday were left wondering why the fund agreed upon at COP28 was expected to provide only about $100 billion per year by 2030.

The shortfall threatened to ensure the loss and damage fund will remain "an empty promise," said Fanny Petitbon, head of advocacy for Care France.

"We hope the agreement will result in rapid delivery of support for communities on the frontlines of the climate crisis," said Petitbon. "However, it has many shortcomings. It enables historical emitters to evade their responsibility. It also fails to establish the scale of finance needed and ensure that the fund is anchored in human rights principles."

"We urgently call on all governments who are most responsible for the climate emergency and have the capacity to contribute to announce significant pledges in the form of grants," she added. "Historical emitters must lead the way."

The United States, the largest historical contributor of the planet-heating emissions that scientists agree are fueling the climate crisis, has objected to tying loss and damage funding to each wealthy nation's emissions—perhaps partially explaining why the Biden administration pledged only $17.5 million to the fund.

Such contributions are "a drop in the ocean compared to the scale of the need they are to address," said Mohamed Adow, director of Power Shift Africa.

"In particular, the amount announced by the U.S. is embarrassing for President [Joe] Biden and [Special Presidential Climate Envoy] John Kerry," said Adow. "It just shows how this must be just the start."

Campaigners also objected to the agreement's stipulation that the World Bank will host the fund for the first four years—a demand that had been made by the U.S. and other wealthy countries—with voluntary payments from powerful governments that will be "invited," not required, to contribute.

"Although rules have been agreed regarding how the fund will operate there are no hard deadlines, no targets, and countries are not obligated to pay into it, despite the whole point being for rich, high-polluting nations to support vulnerable communities who have suffered from climate impacts," said Adow.

"The most pressing issue now is to get money flowing into the fund and to the people that need it," he added. "The pledged funds must not just be repackaged commitments. We need new money, in the form of grants, not loans, otherwise it will just pile more debt onto some of the poorest countries in the world, defeating the point of a fund designed to improve lives."

The United Arab Emirates, which is hosting COP28, pledged $100 million to the fund, a sum that was matched by Germany. The United Kingdom committed to contributing 60 million British pounds, or about $75 million, while Japan pledged $10 billion. The U.S. also said it would provide $4.5 million to the Pacific Resilience Facility, which will offer loss and damage funding to Pacific Island nations, and $2.5 million for the Santiago Network, which will provide technical support to developing countries.

Izzie McIntosh, climate campaign manager at U.K.-based Global Justice Now, called the creation of the global loss and damage fund was called a "welcome, yet long overdue, step forward for our climate," and one that "reflects the utter devastation caused by climate change in the global south, and the need for rich countries to pay what they owe for their role in it."

Rich countries, however, "have weakened the commitment they made to climate justice by insisting on the World Bank as interim host," added McIntosh. "This decision risks both excluding countries due to its outdated rules and deepening the debt crisis if support is provided through loans, not grants. If loss and damage funding is to be truly impactful, it must be funded and designed adequately, or risk being all talk and no action."

At COP27 in Egypt one year ago, noted Christian Aid global advocacy lead Mariana Paoli, policymakers did not even place the loss and damage fund on the agenda.

"It's a testament to the determination of developing country negotiators that we now already have the fund agreed and established," she said. "It's now vital we see the fund filled. People who have contributed the least to the climate crisis are already suffering climate losses and damages. The longer they are forced to wait for financial support to cover these costs, the greater the injustice."

Before COP28 wraps up on December 12, Paoli added, campaigners are hoping they will "see significant new and additional pledges of money to the loss and damage fund, and not just repackaged climate finance that has already been committed."

A fully funded, impactful loss and damage fund must be paired with a commitment by countries to end fossil fuel expansion, added Romain Ioualalen, global policy manager at Oil Change International, with rich countries "redirecting trillions in fossil industry handouts to triple renewable energy and double energy efficiency."

"We have had enough delays," said Ioualalen, "and this must happen now to secure a livable future."

Children suffer the most from fossil fuel burning.

Fossil fuel combustion and associated air pollution and carbon dioxide (CO2) is the root cause of much of children's ill health children today as well as their uncertain future. There are strong scientific arguments, as well persuasive economic ones, for reducing the world's dependence on energy generated by the burning of fossil fuels such as coal, oil, diesel and gasoline.

These include the 7 million adult deaths per year attributed to ambient air pollution, most of it from fossil fuel burning. Less recognized is the huge and largely silent toll on children's health and development from both air toxics and climate change.

Children, whose bodies and brains are especially vulnerable to harm as they develop in utero and in the first years of life, bear a disproportionate burden of disease from both air pollution and climate change. Exposure to toxic air pollutants released during fossil fuel combustion contributes to low birth weight, cognitive and behavioral disorders, asthma and other respiratory illnesses. Climate change is linked to increases in heat-related disease, malnutrition, infectious disease, physical trauma, mental health issues and respiratory illnesses.

While air pollution and the adverse health impacts of climate change affect us all, they are most damaging to children, especially the developing fetus and young child and particularly those of low socioeconomic status, who often have the greatest exposures and least amount of protection.

According to the World Health Organization (WHO), one-third of the global burden of disease is caused by environmental factors, and more than 40 percent of that burden is borne by children under the age of five. Likewise, nearly 90 percent of the global burden of disease caused by climate change is borne by the youngest inhabitants of our planet, with the bulk of that burden falling on people who live in developing countries.

Children in low-income communities in the U.S., as well as globally, suffer most due to disproportionately high exposures to polluting sources, which are more likely to be built in or near the neighborhoods in which they live. The poor are also more likely to live in areas vulnerable to drought and flooding exacerbated by climate change.

Harm from these exposures is magnified by other factors associated with poverty, such as poor nutrition, inadequate social support and psychosocial stresses associated with poverty and racism. Even in the United States, the world's most prosperous country, the child poverty rate is an astounding 22 percent.

Every day that we refuse to act compounds these problems. Inaction perpetuates the health damage from toxic air pollutants and delays and reduces our ability to thwart the increasingly severe consequences of climate change. And it carries long-term consequences for each and every new child conceived.

Exposure in utero and in early childhood to toxic emissions, famine, flooding and other disasters not only increases the risk for neurodevelopmental and mental health problems, stunting, respiratory and other health problems manifest in infancy and childhood, but also for heart disease, chronic obstructive pulmonary disease and cancer in adulthood.

Finally, a growing body of evidence suggests that early-life exposures to air pollutants, nutritional deprivation, and stress may impact the health of future generations, possibly by altering the regulation of genes involved in disease pathways.

Estimates of the economic costs are limited, but indicate the magnitude of potential benefits of action. The economic cost of preterm births attributable to airborne particulate matter in the U.S. was estimated to be over $4 billion/year in 2010. The estimated monetary cost of the health impacts attributable to air pollution from existing coal plants in the U.S. in 2010 exceeded $100 billion a year. The WHO has estimated that by 2030, the global cost of climate change from deaths and diseases (just from diarrhea, malnutrition, malaria and heat stress) will be $2-4 billion per year.

Reducing our dependence on fossil fuels would undoubtedly achieve highly significant health and economic benefits for children worldwide, both immediately and well into the future—vastly improving the health and well-being of generations to come. Knowing this, we have a moral imperative to enact child-centered energy and climate policies that address the full array of physical and psychosocial stressors to which children are subjected due to fossil fuel combustion.

To do less than we can to protect them from preventable harm is nothing short of neglect. As their guardians and protectors, we must act responsibly.

According to a new BBC poll, people around the world are increasingly identifying as global citizens. The poll illuminates changing attitudes about immigration, inequality, and different economic realities.

Among the 18 countries where public opinion research firm GlobeScan conducted the survey, 51 percent of people see themselves more as global citizens than national citizens. This is the first time since tracking began in 2001 that a global majority identifies this way, and it is up from a low point of about 42 percent in 2002.

The poll found that the trend is particularly strong in developing countries, "including Nigeria (73%, up 13 points), China (71%, up 14 points), Peru (70%, up 27 points), and India (67%, up 13 points)."

Overall, 56 percent of people in emerging economies saw themselves as global citizens rather than national citizens.

"The poll's finding that growing majorities of people in emerging economies identify as global citizens will challenge many people's (and organizations') ideas of what the future might look like," said GlobeScan chairman Doug Miller.

In more industrialized nations, the numbers skew a bit lower. The BBC's Naomi Grimley writes:

In Germany, for example, only 30% of respondents see themselves as global citizens.

According to Lionel Bellier from GlobeScan, this is the lowest proportion seen in Germany since the poll began 15 years ago.

"It has to be seen in the context of a very charged environment, politically and emotionally, following Angela Merkel's policy to open the doors to a million refugees last year."

The poll suggests a degree of soul-searching in Germany about how open its doors should be in the future.

Not all wealthy nations were opposed to newcomers. In Spain, 84 percent of respondents said they supported taking in Syrian refugees, while 77 percent of Canadians said the same. A small majority of Americans--55 percent--were also in favor of accepting those fleeing the ongoing civil war.

As Grimley points out, the concept of "global citizenship" can be difficult to define, making it difficult to determine answers about identity.

"For some, it might be about the projection of economic clout across the world," she writes. "To others, it might mean an altruistic impulse to tackle the world's problems in a spirit of togetherness--whether that is climate change or inequality in the developing world."

GlobeScan interviewed 20,000 people in 18 countries between December 2015 and April 2016.

According to a groundbreaking report released this week, multinational corporations are taking advantage of global tax treaties to avoid paying their fair share, thereby fueling poverty worldwide.

The analysis by Johannesburg-headquartered ActionAid International shows how "rip-off tax treaties cost developing countries billions every year, tying the hands of governments, hurting some of the poorest people in the world, and deepening global inequality," said campaigner Savior Mwambwa.

These treaties dictate how much, and even if countries can tax multinational companies, "have no place in the 21st century," ActionAid declares in its report.

As the Mistreated (pdf) report explains, "Tax revenue is one of the most important, sustainable and predictable sources of public finance there is. It is a crucial part of the journey towards a world free from poverty--funding lasting improvements in public services such as health and education." In particular, the group points out, many poor countries are asking for public funds to be put toward "the realization of women and girls' human rights."

Yet thanks to what Mwambwa calls the "broken tax treaty system," global corporations "pay little or no tax in poor countries."

In turn, he said, "Women and children in poverty pay the price when crumbling public services like schools and hospitals are starved of possible funding."

Indeed, after examining more than 500 binding tax treaties that low- and lower-middle-income countries in sub-Saharan Africa and eastern and southern Asia signed with other countries from 1970 until 2014, the International Development Organization concluded that many such pacts "are ensuring that money flows untaxed from poor to rich countries, making the world more unequal and exacerbating poverty."

ActionAid identifies the UK and Italy as the countries that have entered into the highest number of "very restrictive" tax treaties with African and Asian countries since the 1970s, followed by Germany. The organization notes that China, Tunisia, and Mauritius also have a rapidly growing number of similar treaties with some of the world's poorest countries.

Generally speaking, tax treaties that lower-income countries have signed with members of what ActionAid calls "the [Organization for Economic Cooperation and Development, or OECD] club of rich countries" take away more taxing rights than those with other countries. "Worryingly, the deals struck with OECD countries are getting worse," the group says.

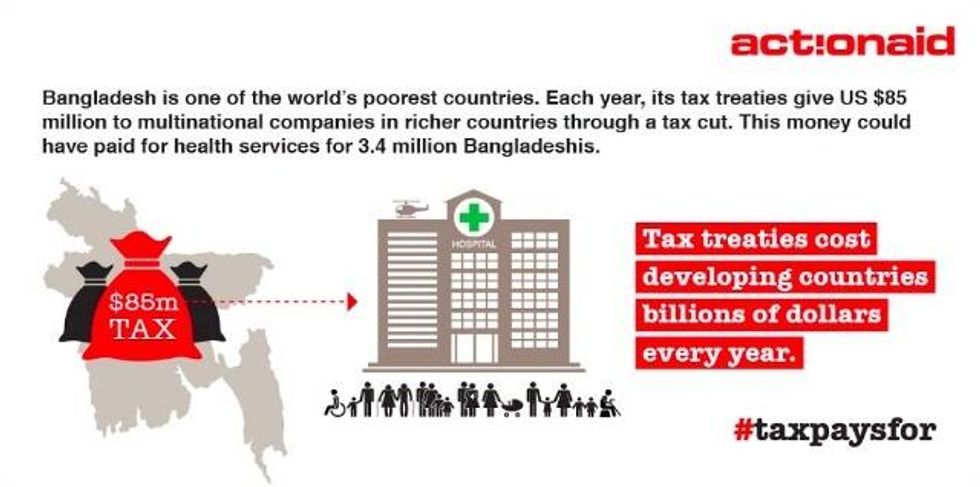

Meanwhile, Bangladesh has given up the most power to tax multinational companies. According to ActionAid, a single clause restricting the country's ability to tax dividends--money paid by companies to overseas shareholders--costs Bangladesh around US$85 million annually.

"This is a country where 66 million people live in extreme poverty--less than US$1.90 a day," the group points out.

The report comes as nations grapple individually and as a bloc with how to close corporate tax loopholes.

In January, Google agreed to a deal with British tax authorities to pay PS130 million (US$143.5 million) in back taxes and bear a greater tax burden in future, after coming under fire for its tax avoidance practices. On Wednesday, the UK Parliament's public spending watchdog criticized the settlement as "disproportionately small."

Indeed, as ActionAid policy advisor Anders Dahlbeck told the Independent last month, "The row over tax dodging by big companies like Google shows how strongly the British public feels that multinationals aren't paying their fair share." But as Mistreated clearly illustrates, "this is just part of a far larger global problem."

Late last month, the 31 OECD members signed an agreement to share information about multinationals' profits and taxation, a move "aimed at stopping firms from using complicated loopholes or moving money across borders to minimize or avoid paying corporate tax," Agence France-Presse reported at the time.

And just this week, it was reported that developing nations will join that effort, under a proposal that would open up the OECD's Committee on Fiscal Affairs to new, associate members that agree to implement certain tax reforms.

The news brought mixed reactions from development groups who said it was too little, too late. "Inclusion after the fact is a poor substitute for a voice in how the standards are designed," said Oriana Suarez of the Latin American Network on Debt, Development, and Rights. "Developing countries now being invited...did not have a say while the rules were being set."

"The OECD is certainly one part of the global fight against tax evasion and tax avoidance, but it's not well-positioned to be the sole standard bearer for the globe," added Porter McConnell of the Washington, D.C.-based Financial Transparency Coalition. "Having its members speak on behalf of the rest of the world's countries is patronizing, and it's ultimately ineffective."