SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

Data center development depends on imported critical conflict minerals and massive amounts of electricity generated by fossil fuels, which contribute directly to US-backed conflicts and war.

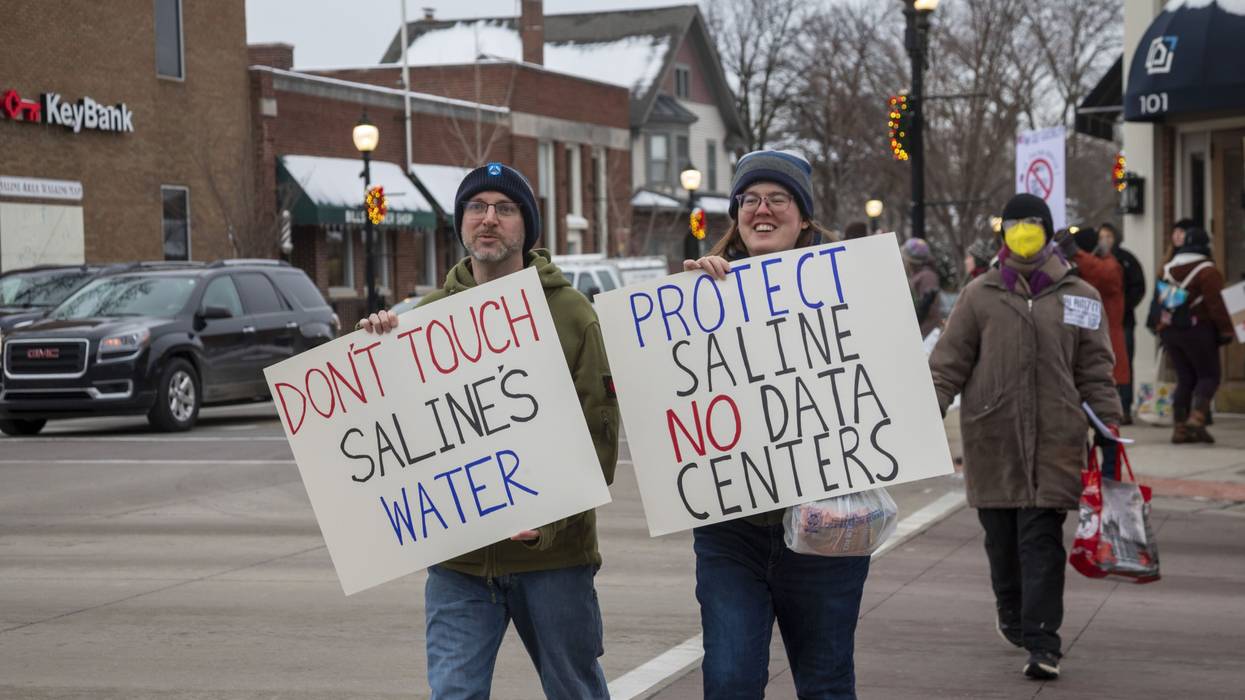

“We’re used to people saying ‘fuck no’ and doing it anyway.” These words were seemingly spoken by our very own Gov. Gretchen Whitmer earlier this month, caught on a hot mic chatting with Oracle executive Clay Magouryk. The two were celebrating breaking ground on the controversial new AI data center in rural Saline, Michigan—currently the largest data center project in the country. Gov. Whitmer is apparently happy to sell Michigan out to military tech giants OpenAI and Oracle.

This is the latest in a series of data center projects being forced into communities that have made their opposition crystal clear. Michiganders are "fighting like hell" because they understand exactly what is at stake; Southwest Michigan residents have already filed a class-action lawsuit for the 24/7 noise nuisance that disrupts daily life and reduces property values.

The development of AI data centers creates harm and destruction. The companies that drive this development, such as OpenAI and Palantir, have contracts with the US military and government agencies like Immigration and Customs Enforcement. Locally, the influx of these data centers provides infrastructure for mass surveillance and diverts municipal resources. Globally, the push for data center expansion demands massive amounts of minerals and fossil fuels from resource-rich countries in the Global South, which are obtained through US military intervention and US-backed militia groups. As such, we as Michiganders must continue to oppose these data center projects.

The harm these data centers inflict ripples across the world. Data center development depends on imported critical conflict minerals and massive amounts of electricity generated by fossil fuels, which contribute directly to US-backed conflicts and war on Venezuela, Iran, and in Congo. Tantalum, tin, tungsten, and gold, referred to as 3TG, are essential, and their extraction is linked to financing armed groups and militias. The struggle for control over mineral-rich areas has led to prolonged violence in Congo, contributing to millions of deaths and leaving entire regions destabilized.

Gov. Whitmer’s hot mic comment confirmed what we already suspected: Our voices and opposition are flat out ignored in favor of destructive corporations.

Detroit is becoming a hub for technology, manufacturing, and the military-industrial complex, where events like the annual Reindustrialize conference bring together defense contractors, surveillance firms, and policymakers to strategize a future built on automated warfare and mass data extraction. Palantir, Lockheed Martin, and Boeing attended, representing key pillars of the US defense and surveillance industry. Palantir’s Project Maven and Where’s Daddy track individuals and automate kill chain recommendations with little human oversight. Lockheed Martin and Boeing produce the missiles, bombs, warcraft, and strike systems that turn algorithmic targeting into genocide.

It’s understandable that some Michiganders might think the development of AI data centers is a good thing, or at least an inevitability. Gov. Whitmer, for one, claims that if Michigan does not lead the charge on these data centers, “they’ll be done elsewhere… with lower wages in a way that abuses the natural resources and jacks up energy prices.” Thus far, this seems to mean that companies that develop these data centers can receive tax breaks and circumvent public input, which sets a disadvantageous precedent.

These data centers, furthermore, are not an inevitability, and they can drastically impact resource usage in their regions. At the Saline data center, even with the closed-loop cooling system to reduce on-site water consumption, water will be consumed indirectly: Increased electricity needs increase the need for water and oil consumption for local power plants. There is also no guarantee that any jobs created will be given to local residents. None of the reported advantages are worth the imperialism needed to supply resources to these data centers, nor the mass surveillance apparatus that comes with them.

Gov. Whitmer’s hot mic comment confirmed what we already suspected: Our voices and opposition are flat out ignored in favor of destructive corporations. Michiganders across the state have stood up and said, "Fuck no" to data centers and more war, yet projects keep moving forward. Residents deserve better than politicians who prioritize tech billionaires and war profiteers over their own people.

Private creditors’ current power to disrupt sovereign debt resolution has negative ripple effects on our own people in the US, especially the most vulnerable.

Amid a succession of financial shocks, the Middle East war being only the most recent, developing countries’ debt levels are alarmingly high and continuing to rise. These burdens make it even more difficult for governments in the Global South to meet the basic needs of their populations. And because the world is interconnected through international trade and financial markets, these developing country debts boomerang back to harm ordinary people in the United States and other advanced economies as well.

To effectively address this growing crisis, we need to recognize that the debt landscape is very different today than it was in the late 1990s and early 2000s, when global leaders agreed on relief initiatives worth more than $130 billion. Back then, private creditors held only about 5% of developing country debt. The rest was in the hands of public creditors, including the United States, UK, Germany, and other Group of 7 rich country governments, as well as multilateral financial institutions such as the International Monetary Fund and the World Bank, which the G7 largely control.

Today, more than 60% of developing country debt is owed to private creditors who typically have the power to sue for full payment even when collective talks or international community initiatives for debt relief are ongoing. The mere threat of litigation gives these private creditors disproportionate leverage that puts debtors at a disadvantage and erodes debt relief gains. During Ethiopia’s prolonged struggle to access debt reductions under the G20 Common Framework, for example, private bondholders threatened to sue rather than make an effort similar to that of public creditors.

What can be done? One promising approach involves working the levers of power in the jurisdictions that govern private debt contracts. More than 90% are issued in New York and the UK. And over the past year, a bill to crack down on predatory private creditors gained real traction in the New York legislature. The “Champerty Fix Act” would prevent private creditors with debt contracts in that state from purchasing heavily discounted debt and then litigating to collect in full, instead of constructively engaging in debt negotiations. The bill would also significantly cut the high interest rates that debt crisis countries pay on claims under litigation.

Lifting the burden of unsustainable debts is the morally right thing to do—and it is in our interest.

With support from a coalition of religious, business, union, anti-poverty, environmental, development, and diaspora organizations, the bill passed the New York Senate and had enough support to pass in the Assembly, but that chamber’s leader chose not to bring it up for a vote by the time the session ended in early June. Supporters continue to demand that the Assembly be re-opened for a vote on the matter before the end of the year.

This legislation would be a huge win for the billions of people in countries where high debt payments divert essential financing for poverty reduction, social services, and development progress. It would also benefit workers, savers, consumers, and taxpayers in advanced economies—including the United States. Private creditors’ current power to disrupt sovereign debt resolution has negative ripple effects on our own people, especially the most vulnerable.

When debt crises affect US trade partners, jobs and wages that depend on import- and export-dependent companies in the United States inevitably suffer. And when inflation goes up due to supply chain disruptions in countries undergoing debt crises, consumers quickly feel it in the prices of their groceries and other everyday goods.

Pensions and other savings vehicles in the United States have exposure to indebted developing economies either directly—when they invest in instruments they issue—or indirectly—when they invest in US companies that have trade or investment in such countries. Reducing the time it takes a country to go from a debt crisis to a lasting restructuring—which currently averages 10 years—would significantly improve returns for our pensions and savers.

Taxpayers also have a stake in ensuring that taxpayer-funded debt relief does not bail out private creditors unwilling to negotiate fairly. In current restructuring deals, private creditors typically get repayments that are 20 percentage points higher than those received by public lenders.

Debt relief for the poorest has strong religious foundations that cut across multiple faith traditions and has been a landmark bipartisan pillar of US policy under every administration since the late 1990s.

Last year, Treasury Secretary Scott Bessent and his counterparts in all G20 countries adopted a declaration on debt sustainability. As the United States took over this year’s Presidency of the G20, he reaffirmed this direction by making the improvement of debt restructurings and debt transparency a priority. Building checks on private creditors in jurisdictions whose courts they use as leverage would go a long way toward supporting these goals by facilitating successful debt renegotiations.

Lifting the burden of unsustainable debts is the morally right thing to do—and it is in our interest.

It is time to count the true cost of the climate crisis, and for those responsible to pay their fair share.

Big Oil and Gas CEOs are raking in obscene profits from the energy shock triggered by the war in Iran, in some cases rivaling the GDP of entire African nations. Meanwhile, ordinary people are left to shoulder the consequences: soaring energy bills, rising food prices, higher costs for medicine, and even the closure of schools. If this crisis does not expose who truly benefits from the world’s dependence on fossil fuels, nothing will.

Wealthy countries justify cutting aid budgets by pointing to fiscal constraints, yet continue to pour vast sums into supporting fossil fuel production. In 2024 alone, implicit fossil fuel subsidies amounted to an estimated $6.7 trillion. But when communities on the frontlines of climate impacts call for reparations or compensation for the losses and damages they have suffered, the conversation suddenly becomes politically contentious and financially unthinkable. The irony is not lost on ordinary people.

This double standard is at the heart of the climate justice debate. It is time to count the true cost of the climate crisis, and for those responsible to pay their fair share.

The International Court of Justice’s (ICJ) recent advisory opinion on climate change offers hope for environmental justice. The world's highest court affirmed what communities have said for decades: Countries have a legal obligation—not just a moral one—to prevent environmental harm, and those harmed may be entitled to reparations. It is telling that some leaders needed the ICJ to remind them of their duty to care for our common home. After 30 climate conferences relying on voluntary, unaccountable processes, we hope this opinion brings real accountability to the United Nations Framework Convention on Climate Change.

Reparations are not charity; they are a necessary investment in the future of people historically harmed by environmental destruction.

As the negotiations in Bonn continue, amid political tensions, a standing agenda item on loss and damage, a theme which has been missing from the majority of the negotiations, will ensure compliance with legal obligations, including on climate reparations, as clarified by the ICJ.

Developing countries must stand their ground. We need an honest, collective reckoning about who causes the harm, who is most affected, and who must pay for the damage. These principles underpin any fair legal system, and there is no justification for treating them as optional

I, along with many others, have argued that dependence on fossil fuels drives rising inequality. Just as importantly, climate change—caused by burning those same fuels—disproportionately devastates vulnerable communities. What happens in the Strait of Hormuz doesn't end there; it ripples through our global energy security. As the war looms in Iran, frontline communities worry about the impending fossil fuel crisis.

The world’s energy dependency is built on extraction, profit, and vulnerability. But who pays the price? It is always the same people on the losing end of this broken system—the very same communities brutally affected by the climate crisis. Those least responsible for conflict pay the price for disruptions to the fossil fuel supply chain, threatening agricultural access and food security. Similarly, those who contribute the least to the climate crisis pay the highest price for its impacts. The system thrives on their vulnerability.

Fossil fuels account for about 86% of global carbon emissions. They are not just an insecure energy source vulnerable to weaponized interdependence; they are the primary driver of climate breakdown. They have disrupted weather patterns and accelerated disasters like intense droughts and devastating floods, harming food systems, cultural heritage, water access, and critical infrastructure like hospitals. This continuous burning has escalated climate injustice in the Global South, Indigenous territories, and Black communities in the United States.

This unequal distribution of burdens is unconscionable. According to Oxfam, a person from the richest 0.1% produces more carbon pollution in a day than someone in the bottom 50% produces all year. Developed countries have already exhausted their carbon budgets, yet they continue expanding extraction. Nations like the US—responsible for over 20% of historical CO2 emissions—carry a massive climate debt that must be repaid.

Meanwhile, developing countries are paying a devastating price for a crisis they did little to cause. Africa is responsible for less than 4% of global historical emissions, yet a single climate disaster can wipe out 5-15% of an African nation’s annual GDP, leaving communities to rebuild alone. This devastation is a lived reality in the Horn of Africa, where millions face climate-induced malnutrition, and in Southern Africa, which is battered by an unending pattern of floods and cyclones.

At the same time, these nations are trapped under mounting debt burdens as they confront escalating impacts with little financial support. It is a harsh reminder that not everyone reaps what they sow. Those on the winning side often do not care, so long as the harm stays far from their doorstep. Someone once asked me if the world would respond to the climate crisis if there was a "major tragedy." My instant thought was that major tragedies are already unfolding in Indigenous territories and the Global South.

The question of reparations remains highly contested because it speaks truth to power and demands true justice. Climate harm has been primarily driven by corporations and Global North governments. The rich nations that benefited from burning coal, oil, and gas must pay their fair share for repair. Through movement assembly work led by Taproot Earth, frontline communities defined what climate reparations must entail: the restoration of healthy relationships, debt cancellation, and accountable systems grounded in Black and Indigenous sovereignty.

Reparations are not charity; they are a necessary investment in the future of people historically harmed by environmental destruction. Current climate finance systems perpetuate injustice by offering loans instead of grants. True climate reparations demand both the abolition of debt and the provision of grant-based finance.

The most vulnerable populations of the Global South are suffering ever-increasing distress, while most of the world has been experiencing rising inflationary pressures and increasing interest rates on government bonds.

For all the uncertainty about what will happen next on the military and diplomatic front in the Iran war, there is certainty about what has already happened on the economic front. And it is not good.

The world has seen a spike in oil prices that has been moderated so far by large drawdowns in global oil reserves. In addition, the most vulnerable populations of the Global South are suffering ever-increasing distress, while most of the world has been experiencing rising inflationary pressures and increasing interest rates on government bonds. And even if the US stock market appears relatively unperturbed, a version of this unpleasant mix has also hit the United States.

Global oil prices are much higher than they were before the war, with the financial market benchmark price of Brent crude late last week (down to $91 on weekend news of a possible deal), well above the $60 per barrel of early January. That said, crude prices have been relatively stable within a broad range over the last two months despite a dramatic drop in energy shipments out of the Persian Gulf since the war began.

According to the International Energy Agency (IEA), as of May 13, the cumulative shortfall in global oil deliveries from the Gulf was roughly 1 billion barrels. This shortfall has been absorbed by reduced oil demand (a consequence of higher prices); increased production outside the Gulf; and by a drop in global oil inventories of roughly 250 million barrels, as these were released to hold down prices in the absence of new production from the Gulf coming to the market. However IEA head Fatih Birol warned last week that inventories were dropping at an unsustainable pace, particularly with summer driving season approaching in the Northern Hemisphere.

For all that US energy exporters might benefit from higher global oil prices, US consumers do not.

The biggest shock from the higher cost (and outright shortage) of fuel, petrochemicals, and fertilizers is being felt by the poorest in the Global South. A recent story in The New York Times described how the price for transporting corn into refugee camps in Somalia had doubled or even tripled, as had the price of water at diesel-powered public tubewells. Meanwhile, protests this week in Kenya against fuel price hikes have led to four deaths, and political and financial stresses are mounting across the continent.

In India, sharp jumps in the price of Liquid Petroleum Gas have hit urban households hard, particularly those whose breadwinners work in small-scale industrial establishments. Many such enterprises rely on LPG as fuel and have shut down, displacing a workforce composed of recent migrants from the countryside. And because informal migrant workers in the city do not have access to India’s price-controlled public distribution systems, they have been forced to purchase cooking fuel on the black market at exorbitant rates. The combination has sparked fears of a repeat of a mass return to the countryside, as happened in the Covid-19 summer of 2020.

Stories like these abound across the Global South. A report from the World Food Program (WFP) two months ago (when the war was two weeks old) projected that 45 million more people could be thrust into acute hunger if the war persisted. And a panel of global officials had already warned the world at the International Monetary Fund meetings in Washington in mid-April that even an immediate cessation of the war would require at least two months before global shipping approached a semblance of normalcy.

Weakness in the real economy of many developing countries has been compounded by financial pressures in the form of larger trade deficits driven by the jump in oil prices, higher inflation, depreciating currencies, drawdowns in central bank reserves, and the threat of central bank rate hikes to keep inflation in check even if the economy is weakening.

In the face of such pressures, many countries were forced to sell foreign exchange or gold reserves to defend their currencies from further depreciation. According to Bloomberg, losses in the Philippines amounted to 8.1% of all reserves, in India to 5.1%, and in Indonesia to 3.8%. India has also imposed stiff tariffs and other restrictions on gold imports, and Prime Minister Narendra Modi has urged Indians to avoid “unnecessary foreign travel,” in additional efforts to limit further pressure on the Rupee from non-energy imports or tourism. And Malawi is reportedly selling not just gold reserves but also semi-processed gold bars bought from local miners.

Europe is less dependent on Persian Gulf oil, with only 7% of it sourced there, as opposed to Asia, which draws roughly 60% of its oil from the region. Even so, it is not immune to the impact of higher prices, with the European Commission’s economic czar warning that the continent faces a stagflationary shock. As a relatively wealthy continent, the EU (and the UK) can afford to grant fiscal subsidies to affected businesses, thus reducing the pain there. However, such measures also force the need to reduce oil demand on the poorest countries that are unable to afford such backstops.

Latin America has proven more resilient to the shocks from the Iran war, helped by the fact that Argentina, Brazil, Colombia, and Ecuador are all net energy exporters, while Mexico runs a small energy deficit but buys most of its natural gas from the US. Chile is the sole large outlier on the front. Still, the energy trade might cushion most major Latin American currencies from sharp depreciation and financial stress, but as an agricultural exporter, the region is vulnerable to higher fertilizer prices and to inflation that could force central banks to raise interest rates.

In the United States, the administration has downplayed the impact of the war on the American people and emphasized how the dramatic increase in US oil production has led to a substantially lower reliance on imported energy. Treasury Secretary Scott Bessent has said that the administration's policies of “energy abundance” have helped the country withstand the shocks from the Iran War. And President Donald Trump said in April that “the United States imports almost no oil through the Hormuz Strait and won’t be taking any in the future…We don’t need it.”

In his recent remarks, Bessent observed that the war had also allowed the US to “focus on the opportunity at hand” as global demand for US energy surged. And, indeed the war has led to a dramatic increase in US exports of crude oil and downstream products. A recent piece in The New York Times noted that the US has exported an additional 145 million barrels of oil since the war began, leading to an increase in revenues of roughly $50 billion.

However, the flip side to this is that US consumers have reportedly spent an extra $40 billion on gasoline prices since the war began. For all that US energy exporters might benefit from higher global oil prices, US consumers do not. And research from the New York Fed suggests that lower-income households were hit much harder by higher energy prices, changing travel patterns in order to keep their gasoline budgets from getting out of hand.

American agriculture, meanwhile, has been hit with a double whammy as two major operating costs, fertilizer and diesel, have both seen sharp price increases. A report last month by the Farm Bureau suggested that 70% of all farmers say they are unable to afford all the fertilizer they need. This in turn could translate into lower crop yields and higher food prices—a worry that is even more pronounced among smallholders in the Global South, underlying the global effects of this war.

And while the US stock market has remained relatively buoyant through all this, boosted primarily by Artificial Intelligence and Semiconductor stocks, there are signs of deeper worries in global bond markets, including in the United States. Concerns over inflationary pressures driven by rising energy and food prices have combined with worries over the rising fiscal costs associated with increased defense budgets, fuel subsidies, and massive reconstruction needs to push global bond yields up significantly.

After annual consumer price inflation in the US jumped to 3.8% (far above the Federal Reserve’s 2.0% inflation target), the US Treasury’s 30-year bond hit its highest yield in 30 years last week. And while that might be good news for those who own newly issued bonds and will receive the interest paid on them, it is less favorable for those looking to buy or refinance a home as mortgage rates rise alongside US government bond yields.

Thus, the impact of this war within the US might not be as severe as that in large parts of the Global South, but even within America, there will be many more who lose than gain from the economic consequences of this war.

Reinvesting just 15% of global military spending, roughly $387 billion, would be more than enough to cover the annual costs of climate adaptation in developing countries. The money exists. The will does not.

Last week, the British government quietly informed the United Nation's Green Climate Fund that it would halve the contribution it pledged just two years ago, not because the climate crisis has eased, but because it is spending more on weapons. The move was framed as a "hugely difficult decision," not ideological, and necessary to deliver what United Kingdom Foreign Minister Yvette Cooper called "the biggest increase in defence spending since the Cold War." The planet, apparently, can wait.

It cannot.

The UK's retreat from climate finance is not some isolated budget decision. It is part of a choice being made across the Global North: to rearm, to retreat from development commitments, and to leave the countries least responsible for the climate crisis to deal with its worst consequences on their own.

Global military expenditure reached $2.887 trillion in 2025, pushing the global military burden to 2.5% of GDP, its highest level since 2009. Europe's alone surged 14% to $864 billion, the highest level ever recorded for the continent. Meanwhile, the UN's own analysis found that reinvesting just 15% of global military spending, roughly $387 billion, would be more than enough to cover the annual costs of climate adaptation in developing countries. The money exists. The will does not.

More conflict and more military spending will only deepen the crisis and make millions more people vulnerable to it.

The UK's Green Climate Fund cut does not happen in a vacuum; the US has refused to deliver any further money to the GCF under President Donald Trump and has also given up its seat on the fund's board. According to the Organisation for Economic Co-operation and Development, international development assistance fell by 23.1% in 2025, the steepest annual decline on record, with the United States slashing its aid budget by 57%, Germany by 17%, and France and the UK by 11% each.

The countries that industrialized on the back of fossil fuels, with the highest historical emissions and the highest per capita carbon footprints, are the ones least bothered by any of this.

And yet for the Global South, the signal being sent today is unmistakable: The nations least responsible for the climate catastrophe bearing down on them will have to bear its consequences largely alone, watching the world burn while the architects of that burning pivot to missiles and military budgets. The prospect of just and equitable climate finance from the developed world is beginning to look not merely uncertain, but futile.

The same wars that are killing climate finance are generating record profits elsewhere. Oil and gas companies' profits are soaring as the Iran conflict continues. Chevron, Shell, BP, ConocoPhillips, Exxon, and TotalEnergies are projected to make $2,967 a second in profits in 2026, nearly $37 million more per day than in 2025, with total projected profits across the six companies reaching approximately $94 billion for the year. None of that windfall is going toward the energy transition. BP has slashed planned investment in renewable energy and increased oil and gas spending, Shell has watered down its 2030 climate targets, ExxonMobil has cut its planned low-carbon investment by a third, and TotalEnergies has declined to adopt a transition plan aligned with 1.5°C of warming.

If a handful of fossil fuel corporations are posting billions in profits in a single year, profits made possible by geopolitical instability, then holding them liable through regulation and taxation is not radical but logical. Windfall profit taxes on fossil fuel companies, long discussed and rarely enacted, could generate precisely the kind of revenue that developed governments claim they no longer have for climate finance.

A February 2026 report by Climate Action Network Europe shows the framework already exists, recommending a differentiated corporate tax on fossil fuel profits with revenues recycled directly into the energy transition and international climate finance. Oxfam makes the same case, calling for a Rich Polluter Profit Tax and an equity-based road map that reflects the historical responsibility and financial capacity of different states. The United States and Europe built their wealth on fossil fuels. Many countries in the Global South remain dependent on them not by choice, but by circumstance. Demanding they exit on the same timeline is neither fair nor realistic.

The tools and the arguments exist. What is missing is political will, and the Global South cannot afford to keep waiting for it. The path forward lies in demanding structural reform of the international tax regime that allows fossil fuel super profits and billionaire fortunes to escape accountability; of the debt architecture that forces climate-vulnerable nations to choose between servicing loans and financing adaptation; and of the COP process itself, which has too long allowed wealthy nations to treat climate finance pledges as suggestions rather than obligations.

So, while the world heats up and vulnerable countries face worsening heatwaves, floods, and disasters, while thousands lose lives and livelihoods, one thing is becoming painfully certain: More conflict and more military spending will only deepen the crisis and make millions more people vulnerable to it. The Global South did not start these wars. It should not be made to pay for them, not with its people, its economies, or its climate.

A global conference on transitioning away from fossil fuels has coincided with rising gas prices caused by Trump's Iran War, motivating many leaders to embrace renewables. Unfortunately, US policymakers aren't following their example.

Many of the people who’ve been working for years on climate issues assembled this week in Santa Marta, Colombia for a conference on how to get off fossil fuels. Sponsored by the Colombians and the Dutch, it was an outgrowth of December’s unhappy COP negotiations in Brazil: the 50 or so nations that actually wanted to move decisively past coal, gas, and oil scheduled a meeting of their own. By all accounts it was a kinder, gentler version of the regular climate talks, in part because fossil fuel lobbyists (who have become the largest “country” at the regular negotiations) were not welcome. The wonderful Irish diplomat Mary Robinson put it well: “COPs are more formal, negotiators have their lines and they will not cross them and it’s so different here,” she said, adding that participants “have felt more human together.”

By lucky accident, the gathering took on extra meaning because it coincided with President Donald Trump’s absurd misadventure in Iran. All of a sudden there was a new reason, past the destruction of the planet, for getting off fossil fuel: Gas is too damn expensive, assuming you can get it all. What we’ve done in the Strait of Hormuz is one of those accidents that changes history: As the head of the International Energy Agency, the venerable Fatih Birol, said last week:

The vase is broken, the damage is done—it will be very difficult to put the pieces back together. This will have permanent consequences for the global energy markets for years to come.

The pieces of that broken vase are scattered across the planet, especially in Asia and Africa, where fuel prices are soaring and fertilizer made with fossil fuel is suddenly either unavailable or ruinously expensive. As Reuters reported this week:

Agricultural bodies, including the International Grains Council, are already cutting their forecasts for the next harvests. And the United Nations, which is trying to negotiate shipping access for fertiliser through the Gulf, has sounded the alarm over food security in developing nations.

In 2022, after the invasion of Ukraine, high fertiliser costs contributed to exacerbated hunger in poor, import-dependent countries, and analysts say regions like East Africa are again vulnerable.

Australia may offer an early indication of the impact on production of global staples.

In the bread-basket state of Western Australia, one industry group now expects the wheat planting area to drop by 14% as growers shift away from the fertiliser-intensive, low-margin grain.

But the good news, of course, is that these countries are rapidly putting together a new and sturdier vase, this time based on energy from the sun and wind that doesn’t need importing. The Santa Marta conference focused on the financing needed to make this switch work—a very real problem, but in the face of the desperation caused by events in the Mideast those who can are going ahead. As Wing Kuang reported, “Chinese EV manufacturers reported an 82.6% rise in month-on-month sales in March.” As the business pages of the India Times reported yesterday:

Increasing penetration of EVs, especially two- and three-wheelers, and rapid deployment of Battery Electric Solar Systems across Southeast Asia and South Asia is now viewed as guaranteed by those in the industry.

The optimism was palpable at this week's Asia Battery Raw Materials & Recycling Conference in Hanoi, where much of the discussion among delegates was more how the region was going to source sufficient raw materials to make batteries, rather than how to increase demand from current levels.

That all this counts as irony is the one delicious lining to all the pain and suffering. Donald Trump, purchased underling of the fossil fuel industry, has managed through his own colossal incompetence and ego to nip the hand that feeds his bank account. Yes, at the moment the industry is soaring: BP reported the kind of grotesque returns Thursday that should have any rational government reaching for a windfall profits tax:

Maja Darlington, a climate campaigner for Greenpeace UK, said the war had been “an entirely predictable disaster for everyone except the oil industry. BP’s profits are booming, with Trump’s bombs bringing billions for them and bigger bills for us.”

But those billions are in the here and now; in the slightly longer term the opposite is happening. Big Oil’s only real growth strategy has been exporting liquefied natural gas to Asia. Bloomberg checked in the other day on how that’s going:

The near-closure of the Strait of Hormuz and the serious damage sustained by Qatar’s LNG export plant has sent prices higher and buyers scrambling for alternatives. Gas’ reputation as a reliable and affordable energy source has taken a serious hit, and plans for its speedy adoption in Asia’s developing nations have been derailed, with potentially long-lasting consequences.

“Every day this is extended, prices elevate, the market tightens, and demand destruction happens,” said Masanori Odaka, an analyst at Rystad Energy. “The longer this lasts, the more structural it becomes.”

Bloomberg News spoke to more than two dozen executives, traders, and analysts across Asia, who painted a picture of a region that had been thought of as the future of LNG, but is now rapidly losing faith in the super-chilled fuel. Most requested anonymity because they weren’t authorized to speak to media.

Importers in India and Bangladesh are already rethinking whether to keep the fuel as a center piece in future strategies. Countries like Vietnam and the Philippines that were expected to become large growth markets, are looking alternatives. A planned gas power project in Vietnam is looking to switch to wind and solar plus batteries. In Thailand policymakers are pushing for more renewables.

This is an appropriate reaction. Cheap renewable energy had already begun to fuel the remarkable energy transition I’ve been chronicling over the last four years in these pages. Now it’s been supercharged by events, and responsible leaders around the world are drawing the obvious conclusions. As Selwin Hart, the UN’s envoy to the Santa Marta talks, put it in his address to the gathering:

Renewables offer something fossil fuels never did: stability and sovereignty. There are no embargoes, price shocks, or tariffs.

But that’s not been the reaction, of course, in this country, where energy policy just keeps getting stupider. Read, for instance, Elizabeth Kolbert’s masterful takedown of Environmental Protection Agency commissioner Lee Zeldin:

In a little more than a year, Zeldin has transformed the EPA from an agency devoted to protecting human health and the environment into one that, more or less openly, sides with polluters…The EPA has not only abandoned its own efforts to rein in greenhouse-gas emissions; it has stepped in to prevent states from taking action. It has come out officially, if astonishingly, as pro-coal.

But here’s what’s astonishing. The person that Zeldin very nearly beat for governor of New York, Kathy Hochul, has been embarked on an environmental demolition project of her own. At the precise moment that gas prices are soaring, and as a new and supercharged El Niño brings climate concerns back to the center of public consciousness, Hochul is doing her very best to sink New York’s landmark climate law and stick the Empire State with more expensive gas. She’s not showing the policymaking chops of her peers in far poorer places like Pakistan or Bangladesh.

Donald Trump, purchased underling of the fossil fuel industry, has managed through his own colossal incompetence and ego to nip the hand that feeds his bank account.

The background here is long, and like all things in New York politics, opaque. Suffice it to say that New Yorkers passed a reasonably ambitious climate law, and that the governor has not done much to enact it. If you want some background, the redoubtable David Roberts interviewed the equally redoubtable Pete Sikora, who explains:

The governor just took everything that the Climate Action Council came up with—her own appointees—and ignored it. That’s the capsule summary. They didn’t do the policies, they didn’t do the regulations, they didn’t do the things that would have implemented the law. They did a few things here and there, but by and large, nothing that would have implemented the law correctly was done. Little bits and pieces. For example, the state passed ending oil and gas in all new construction. That’s fantastic. That’s really good.

As you pointed out, distributed solar is a real bright spot. The numbers are moving there. It’s good. The CHPE project is about to connect. That’s a big transmission project from Canadian hydropower to New York City. Very cool too. There’s good things happening. But by and large, the long list of things in the climate plan was not done—90% of it not done. The centerpiece was Cap and Invest. The governor pulled that back at the last second the same way she did on congestion pricing. It’s in this weird limbo where it’s paused now.

If you want a comprehensive list of the opportunities she’s missed, try here. Most political pros I’ve talked to—and I talked to some more this week because I was in New York this week to lobby on the state’s solar laws—seem baffled by what Hochul’s up to. She’s not in a tough election fight—after Trump pushed Rep. Elise Stefanik (R-NY) out of the GOP primary she faces only a Zeldin-lite Long Island pol, and in a year when an onion bialy could win in blue New York. My guess is that she’s about a year behind on her talking points; in the wake of Kamala Harris’ loss, a certain kind of moderate Dem decided that “affordability” was the new watchword and brought the idea that talking about climate was a mistake. (Not everyone went along—Gov. JB Pritzker in Illinois, for instance, has kept up the state’s clean energy momentum).

In New York’s case this may have been magnified by the sudden rise of Zohran Mamdani, who talked about affordability—but with a particular set of policies attached to it that made it more than rhetorical. For Hochul, an all-out push for wind and solar and batteries would have been wise since they are in fact affordable, but it was easier to go with the fracked gas lobby. So she’s fast-tracking new pipelines—in essence building the very infrastructure that New Yorkers rejected when they shut down fracking in the state. It’s all a tragic muddle, benefiting only Big Oil. Indeed, as Colin Kinniburgh reported last month:

A national industry group, led by some of the country’s largest pipeline builders and a slew of other gas interests, has recently entered the fray, tapping former state politicians to help advance Gov. Kathy Hochul’s “all of the above” energy strategy. Top of their agenda: pressing pause on the state’s climate targets.

New Yorkers can do a couple of things. One is press their state legislators to resist Hochul’s gutting of the climate law. The other is to lobby those same legislators to pass the ASAP and SUNNY laws, which would at least speed up solar permitting and allow balcony solar in the state.

And all of us can do a better job of demanding real action from our blue state leaders. Because this drift is not confined to New York—in Hawaii, for instance, Democratic Gov. Josh Green has called for a huge new liquefied natural gas project to supply the state’s electricity, ignoring the fact that the Aloha State is bathed in sunlight and washed by the steady trade winds that make it so delightful. Again, this is exactly the opposite tack that leaders across the rest of the world are taking, and in both states it will saddle residents with gas projects for decades to come.

I wrote about “climate-hushing” last week, and decisions like this are the inevitable result—on purely political grounds alone they surrender the high ground on what will be the most important issue of our century. And they surrender the gift that cheap renewables provide to both planet and consumer. They are exactly the opposite of what scientists told the Santa Marta conference was required—an end to new fossil fuel expansion. The next time a climate disaster strikes these states their governors will mouth the usual pieties, but they won’t mean much.

“Amid a tense geopolitical context and worsening climate extremes, Santa Marta helped spark a feeling of renewed energy, but delegates must now follow through to deliver action, not just words," said a senior climate adviser at Greenpeace.

Environmental activists are hopeful after a six-day climate summit in Colombia resulted in a coalition of more than 50 countries agreeing to start developing plans to move away from planet-heating fossil fuels. But they say action must now follow talk.

In marked contrast to the annual United Nations climate summits, which have been routinely overrun by oil and gas industry lobbyists and concluded with agreements that largely ignore the imperative to divest from fossil fuels, Shiva Gounden, the head of Greenpeace's delegation this week in Santa Marta, said the conference that concluded Wednesday "was a breath of fresh air, a real sign that the wind is finally shifting."

The 59 nations that attended the First Conference on Transitioning Away from Fossil Fuels did not ultimately end with a binding agreement to transition away from fossil fuels within a specific timeframe, which activists say is urgently necessary as global heating rapidly approaches 1.5°C above preindustrial levels.

Many of the world's biggest polluters—including the United States, China, and India, as well as petrostates like Saudi Arabia, Qatar, and the United Arab Emirates—were also absent.

However, the summit did end with attendees, nearly half of whom are fossil fuel producers and who represent more than half of global gross domestic product, agreeing to form tangible "frameworks" for how they plan to transition away from a fossil-fueled model of capitalism that Colombian President Gustavo Petro decried as "suicidal."

Perhaps the single biggest breakthrough at the conference was France's unveiling of a national roadmap to phase out fossil fuels in the coming decades. It became the first developed nation to lay out such a plan, with the goals of removing coal from its national grid by 2027, phasing out oil by 2045, and fossil gas by 2050.

The French climate envoy, Benoit Faraco, described it not only as an obligation but an opportunity: “This process has made us realise we want to be an electro-superpower,” he said, according to The Guardian. “We want to be the electricity Saudi Arabia of Europe, selling green electrons to the UK, Ireland, Germany, and other countries.”

Many attendees also agreed that any collective movement away from fossil fuels would require addressing the debt crisis in the Global South, which many countries—especially those in Africa, where national debts have doubled in the past five years—have found themselves cranking up fossil fuel production to cope with.

While the conference concluded without any binding plan for debt forgiveness, which many delegates from developing countries had proposed, the participants agreed that poorer countries would need support to move out of debt and finance a green transition.

"Fossil fuel dependency deepens economic instability, fuels conflict, and traps countries in cycles of debt," said Bronwen Tucker, public finance lead for Oil Change International. "As long as Global South countries remain locked in this system, while Global North governments write the financial rules, public resources will continue to flow away from people and toward the systems driving crisis."

Laura Caicedo, the campaigns coordinator at Greenpeace Colombia, described the conference as "an important space to put the just energy transition on the agenda ahead of the Climate COP," which will take place in Turkey this coming November.

"There is willingness and a sense of fresh momentum that is worth celebrating," she said. "But this is only the beginning: more time is needed for this process to mature into a true platform for dialogue that can inform decision-making in this and other cooperation spaces on key energy issues."

The next conference on Transitioning Away From Fossil Fuels is set to occur early next year in Tuvalu, a low-lying Pacific island nation that is at risk of becoming uninhabitable within decades due to sea-level rise.

While climate activists were heartened by the progress made in Santa Marta, Gounden said countries need to come to Tuvalu with concrete plans.

“When we get to Tuvalu, the conversation has to change," she said. "We can’t just bring more ambition; we have to bring proof of implementation."

This week's conference took place against the backdrop of the US and Israel's war in Iran, where US President Donald Trump has suggested a key goal is to "take the oil" controlled by Iran. The obstruction of oil shipments has become a critical piece of strategic and economic leverage and simultaneously inflicted chaos upon the global economy, disrupting humanitarian aid for some of the world's poorest and most vulnerable people.

"Amid a tense geopolitical context and worsening climate extremes," said Rodrigo Estrada, Greenpeace International's senior climate adviser, "Santa Marta helped spark a feeling of renewed energy, but delegates must now follow through to deliver action, not just words."

While the war has sent energy companies' profits soaring, the climate advocacy group 350.org estimated this week that the continued blockade of the Strait of Hormuz could cost households and businesses an additional $600 billion to $1 trillion.

"It’s never been clearer that fossil fuel phase-out is imperative for stability and peace," Tucker said. "Every step away from fossil fuels weakens the outsized power and wealth that allows the US to wage illegal wars in the name of energy dominance."

At the next conference, she added, "The richest polluting countries must show they are serious. Canada, Norway, the UK, and the EU must make real plans to accelerate their fossil fuel phaseout at home and come to the table with real economic collaboration."

Mariana Paoli, the climate policy lead for Oxfam, said the lack of action by rich countries was "disappointing" and needed to change.

"Wealthy governments have still not stepped up to provide sufficient climate financing for poorer countries, which face the brunt of the impacts of the climate crisis," she said. "Rich countries hold the historical responsibility for the climate crisis, therefore they must not only move first and faster but also provide finance at scale for others to follow them."

"A just transition," she said, "must make rich polluters pay for the crisis they have caused."

Governments gathering for International Monetary Fund and World Bank meetings "have a clear responsibility," said a 350.org leader. "End this illegal war, stop the flow of destruction, and make the profiteers pay."

As the Spring Meetings of the International Monetary Fund and World Bank Group were held in Washington, DC during a two-week ceasefire between the United States, Israel, and Iran, over 130 civil society groups this week urged global governments to "secure a permanent end to the wars in South West Asia and break the chains of fossil fuel dependence."

The joint statement was coordinated by Fight Inequality Alliance and 350.org, which has been advocating for a windfall profits tax on oil and gas giants since the US and Israel launched their illegal war on Iran in late February, and the Iranian government responded by restricting traffic through the Strait of Hormuz, which sent fossil fuel prices soaring worldwide.

"While people struggle to afford food, fuel, and basic necessities, fossil fuel companies are profiting massively from the chaos. The IMF itself has warned of the risk of a global recession," said 350.org managing director Savio Carvalho in a statement.

"Governments gathering in Washington have a clear responsibility: End this illegal war, stop the flow of destruction, and make the profiteers pay," Carvalho argued. "Taxing windfall oil and gas profits could provide immediate relief to families and invest in the clean, affordable energy systems we urgently need. They profit, we pay. It's time to fix it now: no bombs, no barrels."

A permanent end to the war—which has killed people across the region—is the first demand of the open letter. The second is a windfall profits tax on fossil fuel giants, with the revenue being used "to guarantee public services, and provide immediate support to families and precarious workers hit hardest by soaring food and fuel prices."

Martha Tukahirwa, Fight Inequality Alliance's Africa coordinator, explained that "while thousands are killed in the war in Iran, millions of people across Africa are being crushed by soaring fuel prices that have made even the simplest meal unaffordable. In Nigeria, diesel has surged over 60%. In Malawi, the poorest households are forced to choose between cooking and eating."

"In Zimbabwe, the cost of public transport has soared, making it impossible for working people to earn a living," Tukahirwa continued. "This is no accident—fossil fuel companies and commodity traders are reaping massive profits from this crisis while our governments stand idle. Tax these obscene profits and redirect the money to shield our people from hunger and hardship. The time for half measures is over, the time for bold action is now."

The letter's third demand is to "make food and energy secure for all." The war has impacted the availability of not only fuel but also fertilizer. The coalition called on governments to "invest public money in sustainable local farming and homegrown renewable energy, and stop harmful handouts to weapons, fossil fuels, and fossil fertilizer."

The groups—which also include ActionAid International, Corporate Europe Observatory, Council of Canadians, Friends of the Earth International, GreenFaith, Greenpeace Japan, Make Polluters Pay, Oxfam in the Pacific, War on Want, and more—called for urgently rolling out "renewable energy solutions for farms, homes, schools, and clinics to protect them from this and future energy crises."

Rev. Fletcher Harper, executive director of GreenFaith, said that "our faiths call us to make peace with people and the planet alike, and to hold the powerful to account. Letting fossil fuel giants pocket windfalls while families struggle is a moral failure. Taxing windfall profits to provide energy relief is not radical. It is basic justice."

The fourth and final demand is to cancel debt payments for Global South countries, and agree to fairer debt rules. The coalition stressed that "after paying interest to Wall Street lenders, bankers, and rich governments, many Global South countries have no money left over to protect their people from this crisis."

As part of the debt demand, the coalition also urged governments to "support informal workers, farm laborers, women, and older people, and guarantee universal access to healthcare, education, and public transport."

David Archer, head of programs and Influencing at ActionAid, pointed to civil society's push for a United Nations treaty for restructuring sovereign debt.

"Billions of people across the Global South are living in countries already facing a debt crisis. This war will make their lives even harder, leading to rising prices and rising interest rates," Archer said. "We need urgent action to cancel debt and to take the power over debt away from the IMF and rich countries—through developing a UN Framework Convention on Sovereign Debt."

"Governments must restore their aid budgets, and shore up the global humanitarian system that faces its most serious crisis in decades," said an advocate with the international charity Oxfam.

The global anti-poverty group Oxfam International warned this week that US President Donald Trump’s decision to slash foreign aid by more than half could kill nearly 10 million people by the end of the decade.

Responding to new data released Thursday by the Organization for Economic Cooperation and Development (OECD) showing the largest annual drop in the history of official development assistance, Oxfam said “wealthy governments are turning their backs on the lives of millions of women, men, and children in the Global South.”

The OECD released preliminary data on international aid that was provided last year by member countries of the organization's Development Assistance Committee (DAC), finding the largest annual drop in the history of official development assistance.

OECD member countries provided $174.3 billion in aid last year, according to the new data, representing 0.26% of the countries' combined gross national income.

In 2024, the countries sent $215.1 billion, or 0.34% of their gross national income to developing countries, including across the Global South—helping to provide nutritional assistance and healthcare initiatives among other programs.

US foreign aid spending dropped by 56.9% after Trump dismantled the US Agency for International Development, cut smaller aid programs, and pushed Congress to rescind previously approved foreign assistance.

"At a time when aid cuts are already driving instability and fostering greater inequality, government donors are cutting life-saving aid budgets while financing conflict and militarization."

Overall, wealthy OECD countries provided 23.1% less in foreign aid last year than they did in 2024—a greater decline than what the Institute of Global Health in Barcelona projected in February when it released a study in The Lancet, evaluating the impact of development assistance funding declines around the world.

The institute found that aid cuts in 2025 alone, which it assumed would represent a 21% decrease in funding, would lead to 695,238 excess deaths. If cuts continued at the same rate, an estimated 9,416,417 people could die of preventable diseases like malaria and AIDS, starvation, and other impacts by 2030.

The drop in foreign aid spending would suggest even more people could be killed by the cuts over the next four years.

“We are in a time of increasing humanitarian needs; strong pressures on the poorest and most fragile countries; and facing growing global uncertainties and massive insecurity," said Carsten Staur, chair of the OECD's Development Assistance Committee (DAC), which compiled the data. "In this situation, the world needs more ODA, not less—to help fight extreme poverty, improve resilience, and mobilize more private resources."

Trump's cuts helped make Germany the largest provider of development assistance for the first time ever, providing $29.1 billion to countries in need. The US sent $29 billion while the United Kingdom provided $17.2 billion, Japan sent $16.2 billion, and France sent $14.5 billion. All five of the top ODA providers reduced their foreign aid spending, accounting for 95.7% of the total decline.

Eight out of the DAC's 34 member countries either maintained or increased their development aid spending, and four countries—Denmark, Luxembourg, Norway, and Sweden—exceeded the United Nations' target of spending 0.7% of their gross national income on ODA.

Didier Jacobs, development finance lead for Oxfam, emphasized that while "recklessly" cutting foreign aid, "the Trump administration has been preparing to ask Congress for tens of billions in additional funding for bombs, ammunition, and other military equipment relating to its unlawful war against Iran."

"At a time when aid cuts are already driving instability and fostering greater inequality, government donors are cutting life-saving aid budgets while financing conflict and militarization. Cuts from donors including Germany, France and the UK will be felt by the world’s poorest," said Jacobs.

In addition to slashing military spending instead of crucial foreign aid, he said, "there are other ways to find tens of billions, such as by taxing the $2.84 trillions of dollars that the super-rich hide in tax havens.”

"Governments must restore their aid budgets," he said, "and shore up the global humanitarian system that faces its most serious crisis in decades."

The only answer to Trump’s savage moves is resistance, the kind of resistance that is rising not only throughout the Global South but also in places such as Minnesota.

In the second year of Donald Trump’s second term, beginning with the kidnapping of Venezuelan President Nicolás Maduro on January 2, 2026, followed by the war of choice he has waged against Iran alongside Israeli Prime Minister Benjamin Netanyahu, the US president has continued his demolition of the 80-year-old global order set up by Washington in the aftermath of the Second World War.

That dying regime is a structure of rules, practices, and policies maintaining the hegemony of the United States and the rest of the capitalist West that was promoted with the rhetoric of freedom, free trade, and democracy. In remarkably candid words, the gap between the reality of this so-called multilateral order and the ideology that justified it was captured by the leader of a country, Canada, whose elite benefited from it. In his speech in Davos on January 20, 2026, Prime Minister Mark Carney admitted:

For decades, countries like Canada prospered under what we called the rules-based international order. We joined its institutions, we praised its principles, we benefited from its predictability. And because of that, we could pursue values-based foreign policies under its protection.

We knew the story of the international rules-based order was partially false, that the strongest would exempt themselves when convenient, that trade rules were enforced asymmetrically. And we knew that international law applied with varying rigor depending on the identity of the accused or the victim.

This fiction was useful, and American hegemony, in particular, helped provide public goods, open sea lanes, a stable financial system, collective security, and support for frameworks for resolving disputes.

So, we placed the sign in the window. We participated in the rituals, and we largely avoided calling out the gaps between rhetoric and reality.

The order Carney describes is over, with the hegemon replacing its rules and practices, already unfair to the Global South as they were, with the unilateral exercise of coercion and force, with no rules at all except the rule that might makes right. Perhaps the essence of the new order is best captured by the words of US Defense Secretary Peter Hegseth during the US-Israeli bombing of Teheran: “This was never meant to be a fair fight, and it is not a fair fight. We are punching them while they’re down, which is exactly how it should be.”

In the first three months of 2026, Trump has already succeeded in dismantling the political fictions of the old regime, among them the central principle of the United Nations that expressly prohibits “the threat of the use of force against the territorial integrity or political independence of any state, or in any other manner inconsistent with the Purposes of the United Nations.” The kidnapping of Maduro and the assassination of Iran’s Supreme Leader Ali Khamenei were the hegemon’s announcement to the world that no country is exempt from outright, brazen intervention should Trump see it fit to do so, and there would not even be the fig leaf of constructing a “Coalition of the Willing” to prettify it, as George W. Bush did prior to his invasion of Iraq in 2003. Nor were foreign territories belonging to close allies, such as Greenland, immune from annexation should Trump decide it is in the US national interest to grab them.

Despite denunciations and votes against its aggressive initiatives at the General Assembly, through its veto power at the Security Council and its threat to withhold its financial contributions to the organization’s budget, the United States has neutered the UN.

But before dismantling the political-military fiction of the old regime, Trump assaulted its economic fiction in 2025. More accurately, he resumed the transformation of the multilateral economic order that he began during his first presidency, from 2017 to 2021. During that earlier period, he continued the policy of his predecessor, Barack Obama, of blocking appointments and reappointments to the Appellate Court of the World Trade Organization (WTO), effectively paralyzing the body. But even more brazenly, he declared a unilateral trade war against China, undermining the system of rules and conventions of global trade that the United States led in institutionalizing in 1994, with the founding of the WTO.

In 2025, Trump expanded what he did not hesitate to call his “trade wars” to some 90 other countries. Among them were 50 African countries, some of whom received some of the highest, most punitive tariff increases in the world, like Lesotho (50%), Madagascar (47%), Mauritius (40%), Botswana (37%), and South Africa (30%). There was little rhyme or reason to the rates imposed, though in the case of South Africa, it was partly as punishment for bringing Israel to the International Court of Justice for committing genocide in Gaza.

Trump’s rhetoric is aggressive, brazen, and full of bluster, but let’s not be fooled. His is a defensive imperialism, a fighting retreat.

Foreign aid as an instrument of US policy was a pillar of the old international regime. As Thomas Sankara, one of Africa’s foremost fighters for liberation, pithily observed, “He who feeds you controls you.” To please his far-right base, which did not see foreign aid as important for the maintenance of US hegemony and viewed it as a waste of resources, Trump in one of his first acts—undertaken with Elon Musk, the world’s richest individual—abolished the Agency for International Development (USAID). This move drew divergent responses from progressives and liberals. For some, this was a tragedy since USAID programs were allegedly funding important public health and reproductive health projects in the Global South. For others, it was no loss at all since most of the funds for these initiatives went to pay the US contractors delivering or managing them.

Despite their crowing about doing away with foreign aid, Trump and Musk did not make any move to dismantle or reduce the flow of US funds to the International Monetary Fund, the World Bank, and regional development banks through which the bulk of US money for dominating the Global South via “development assistance“ or “structural adjustment” was funneled. Most likely, the rationale was to hold these so-called multilateral organizations in reserve for the aggressive exercise of American power via Washington’s controlling interest or veto power in these institutions should this become necessary in the future.

In the meantime, these institutions continue to maintain poverty-creating structural adjustment programs, especially in Africa, promote wrong-headed “export-led industrialization” efforts even as the United States imposes massive punitive tariffs on imports from the Global South, and block all efforts to solve the massive indebtedness of developing countries to the tune of over $11.4 trillion, which threatens a rerun of the Third World debt crisis of the early 1980s.

Last November, the Trump administration released National Security Strategy 2025, which announced that the United States would focus its military, political, and economic initiatives to making the Western Hemisphere the primary US sphere of influence. Even before the release of the memorandum, Trump had announced US plans to annex Greenland and the Panama Canal.

Moreover, the “Trump Corollary” to the old Monroe Doctrine made it clear that this would mean aggressively putting an end or countering the activities of non-regional actors such as China in the hemisphere. Shortly after the National Security Strategy went public, the kidnapping of Maduro made it clear that Washington would not hesitate to brazenly intervene in the affairs of any sovereign state in the region, in violation of the central founding principle of the United Nations.

However, with its joint assault with Israel against Iran beginning February 28, Trump appeared to be forcefully telling everyone that the United States was not departing from the old liberal containment paradigm’s perspective that the whole world was Washington’s sphere of influence, as NSS 2025 seemed to have implied. Although Trump’s volatile personality is a factor behind his shifting moves, it is becoming increasingly clear that so long as an operation does not involve sending in ground troops and relies mainly on air power or naval power, Trump is willing to use US military power anywhere in the world, as he has done not only in Iran but also in northern Nigeria, with his bombing of Islamist forces there on December 25, 2025, calculating that with few soldiers returning home in body bags, the US public could be easily pacified into accepting new foreign military engagements.

But also central in accounting for Trump’s moves is the strong influence of Israel, as evidenced not only by the joint US-Israeli assault on Iran but also his full support of Netanyahu’s genocidal campaign against the Palestinian people in Gaza and the West Bank and his sponsorship of a US-led ethnic cleansing operation in Gaza via his deliberately misnamed “Board of Peace.”

A great majority of the people of the United States oppose the war on Iran. Even key figures in the MAGA Movement, such as Steve Bannon, Tucker Carlson, and Marjorie Taylor Greene, have complained that Trump’s recent actions in Venezuela and the Middle East represent his going back on his electoral promise never to get the United States into another “forever war.” Indeed, Carlson has denounced the Iran operation as “Israel’s war,” in which the United States has no business being involved.

Perhaps there is no better explanation for Trump’s subservience to Netanyahu than that provided by a leading figure of the American far right: Curt Mills, executive director of the American Conservative. According to Mills, Trump is

not saying no to Israel because he is fundamentally too agreeable or because he’s fundamentally corrupted. He’s agreeable. He is too close to them politically. And I think, yeah, I think he’s somewhat afraid of them. Why is he afraid of them? I think they’re an intimidating society. And I think people are afraid of Mossad. I think people are afraid of Israeli influence in foreign policy, they are afraid what it can do to people’s careers.

Whatever the cause or causes of his allowing himself to be lured into a war on Iran, it is now clear that this misadventure is a massive miscalculation that might lead to some fractures in his base.

To place things in perspective, though, Israel’s overweening influence began way before Trump. The United States forced the creation of the European settler colony by the United Nations in 1947. Since then, like Frankenstein’s monster, the creature has gradually but surely come to control its creator through the powerful Zionist lobby in Washington, to the point that subservience to its wishes has become a central characteristic of both Democratic and Republican administrations.

Whatever might be his immediate motivations, Trump’s moves are mainly directed at people and countries in the Global South—Palestine, Nigeria, Venezuela, Iran, and Cuba—the last of which he has threatened to assault next or strangle into submission. There is a logic to this strategy since it is mainly the Global South that has shifted the balance of global power and created the crisis of US hegemony. Among the landmarks in this historic process have been the rise of China to becoming the second most powerful economy in the world; the massive defeats of US arms in Iraq, Libya, and Afghanistan over the last 25 years; the rise of Iran as a regional power despite all the efforts of the United States and Israel to contain it; the ability of developing countries to stymie the WTO as an engine of trade liberalization; and the rise of the BRICS as a potential counterweight to the Western alliance.

Also central to the weakening of the hegemon has been the deepening crisis of the global capitalist regime of which Washington has been the global policeman, the key manifestations of which are the deindustrialization of the United State and Europe, the financialization of the leading capitalist economies where speculation rather than production has become the investment of choice, the astounding rise in global income and wealth inequality, and the sharpening contradiction between planetary survival and the ever more intensive drive for profits.

Trump’s regime of unilateralism is a savage world. But there is no going back to the old regime of US hegemony exercised through a multilateral order systematically biased against the Global South behind a façade of liberal democratic rhetoric.

Trump’s rhetoric is aggressive, brazen, and full of bluster, but let’s not be fooled. His is a defensive imperialism, a fighting retreat, a response to the overextension of American economic and political power and the comprehensive failure of capitalism to respond to the needs of humanity and the planet. The only answer to Trump’s savage moves is resistance, the kind of resistance that is rising not only throughout the Global South but also in places such as Minnesota, where people have rallied beyond race and ethnicity to form effective communities of solidarity to stop the brutal assault on migrant families.

The Italian thinker Antonio Gramsci had a saying related to the troubled 1930s that is also apt for our times: “The old world is dying, and the new world struggles to be born. Now is the time of monsters.” Trump’s regime of unilateralism is a savage world. But there is no going back to the old regime of US hegemony exercised through a multilateral order systematically biased against the Global South behind a façade of liberal democratic rhetoric. For the Global South, indeed, for all who are partisans of justice, peace, and planetary survival, there is no choice but to bravely meet the challenge of navigating the turbulent waters of this period of transition to get to the haven of a new global order that will serve the common interest of humanity and the planet, though there is no certainty regarding when or even if that arrival will come.