SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

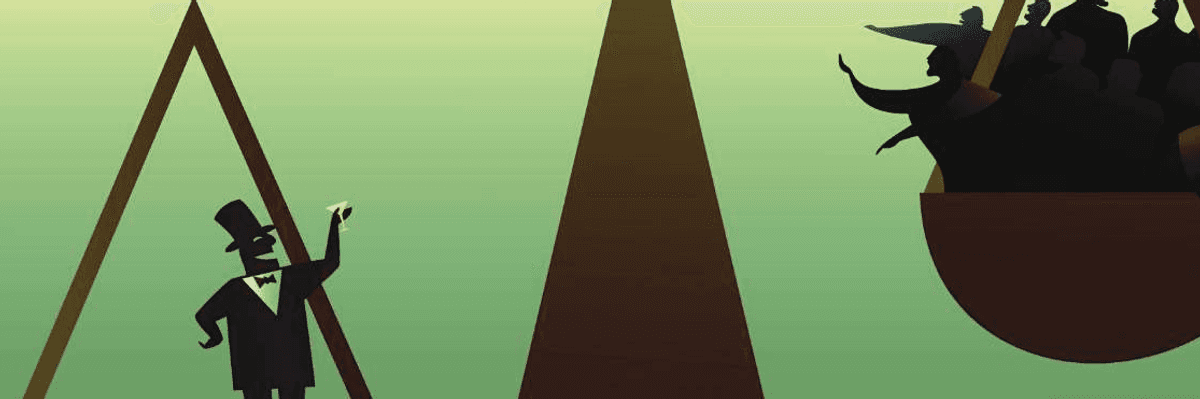

This trend not only magnifies the risk of economic stagnation and market failures; political changes around the world suggest that it has also become a profound threat to democracy. (Photo: Getty Images)

Since reducing inequality became an official goal of the international community, income disparities have widened. This trend, typically blamed on trade liberalization and technological advances that have weakened the bargaining power of labor vis-a-vis capital, has generated a political backlash in many countries, with voters blaming their economic plight on "others" rather than on national policies. And such sentiments of course merely aggravate social tensions without addressing the root causes of worsening inequality.

But in an important new article, University of Cambridge economist Jose Gabriel Palma argues that national income distributions are the result not of impersonal global forces, but rather of policy choices that reflect the control and lobbying power of the rich. In particular, Palma describes the significant recent increase in inequality in OECD countries, the former socialist economies of Central and Eastern Europe, and China and India, as a process of "reverse catching-up." These countries, Palma says, increasingly resemble many unequal Latin American economies, with rent-oriented elites grabbing most of the fruits of growth.

In his earlier work, Palma showed how middle and upper-middle income groups' share of total income has remained remarkably stable in most countries over time, at about one-half. Changes in aggregate income distribution, therefore, resulted largely from changes in the respective shares of the top 10% and the bottom 40% of the population (the ratio between these shares is now called the "Palma ratio").

In other words, the huge variation in inequality across countries, and particularly between middle-income economies, is essentially the outcome of a fight for around one-half of national income involving one-half of the population. Only in cases of extreme inequality (such as South Africa) did the top 10% also manage to encroach on the income share of the middle.

It is misleading, therefore, to view rising per capita incomes in middle-income countries as indicating a general improvement in standard of living. In unequal middle-income economies such as those in Latin America, the incomes of the top 10% are already on par with those of their rich-country counterparts. The incomes of the bottom 40% are closer to the Sub-Saharan African average.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources.

The driving force behind these trends is market inequality, meaning the income distribution before taxes and government transfers. Most OECD countries continually attempt to mitigate this through the tax and transfer system, resulting in much lower levels of inequality in terms of disposable income.

But fiscal policy is a complicated and increasingly inefficient way to reduce inequality, because today it relies less on progressive taxation and more on transfers that increase public debt. For example, European Union governments' spending on social protection, health care, and education now accounts for two-thirds of public expenditure, but this is funded by tax policies that let off the rich and big corporations while heavily burdening the middle classes, and by adding to the stock of government debt. As Palma puts it, "in their new tax status, corporations and the very rich now prefer to part-pay/part-lend their taxes, and part-pay/part-lend their wages."

In rich countries, middle-income groups have largely maintained their share of national income. But their living standards have fallen, owing to the rising costs of essential goods and services (such as housing, health care, and education), falling real pensions, regressive taxation, and rising personal debt. Most emerging-economy governments, meanwhile, are not implementing significant fiscal measures to reduce market inequality.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources. Specifically, this increase in value extraction is the result of policies for which the rich have actively lobbied: privatization; deregulation of share buybacks that artificially inflate stock prices; patent laws that make drugs much more expensive; reduction or elimination of top marginal tax rates; and much else.

Giving the rich all this additional income has not resulted in higher investment rates in the OECD or in unequal middle-income countries. Instead, the rich are content to pluck the low-hanging fruit of rent extraction, market manipulation, and lobbying power. High profits therefore coexist with low investment and increasing market inequality, in a self-reinforcing pattern. This trend not only magnifies the risk of economic stagnation and market failures; political changes around the world suggest that it has also become a profound threat to democracy.

Addressing this dangerous state of affairs will require that governments use their power to tax and regulate to channel more private capital into productive spending and increase the amount of public investment financed by progressive taxation, along the lines of a Global Green New Deal. If policymakers fail to mount a response that is proportionate to the problem, the rich will continue to get richer, and the poor to get poorer, faster than ever. Who will address the problem then?

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

Since reducing inequality became an official goal of the international community, income disparities have widened. This trend, typically blamed on trade liberalization and technological advances that have weakened the bargaining power of labor vis-a-vis capital, has generated a political backlash in many countries, with voters blaming their economic plight on "others" rather than on national policies. And such sentiments of course merely aggravate social tensions without addressing the root causes of worsening inequality.

But in an important new article, University of Cambridge economist Jose Gabriel Palma argues that national income distributions are the result not of impersonal global forces, but rather of policy choices that reflect the control and lobbying power of the rich. In particular, Palma describes the significant recent increase in inequality in OECD countries, the former socialist economies of Central and Eastern Europe, and China and India, as a process of "reverse catching-up." These countries, Palma says, increasingly resemble many unequal Latin American economies, with rent-oriented elites grabbing most of the fruits of growth.

In his earlier work, Palma showed how middle and upper-middle income groups' share of total income has remained remarkably stable in most countries over time, at about one-half. Changes in aggregate income distribution, therefore, resulted largely from changes in the respective shares of the top 10% and the bottom 40% of the population (the ratio between these shares is now called the "Palma ratio").

In other words, the huge variation in inequality across countries, and particularly between middle-income economies, is essentially the outcome of a fight for around one-half of national income involving one-half of the population. Only in cases of extreme inequality (such as South Africa) did the top 10% also manage to encroach on the income share of the middle.

It is misleading, therefore, to view rising per capita incomes in middle-income countries as indicating a general improvement in standard of living. In unequal middle-income economies such as those in Latin America, the incomes of the top 10% are already on par with those of their rich-country counterparts. The incomes of the bottom 40% are closer to the Sub-Saharan African average.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources.

The driving force behind these trends is market inequality, meaning the income distribution before taxes and government transfers. Most OECD countries continually attempt to mitigate this through the tax and transfer system, resulting in much lower levels of inequality in terms of disposable income.

But fiscal policy is a complicated and increasingly inefficient way to reduce inequality, because today it relies less on progressive taxation and more on transfers that increase public debt. For example, European Union governments' spending on social protection, health care, and education now accounts for two-thirds of public expenditure, but this is funded by tax policies that let off the rich and big corporations while heavily burdening the middle classes, and by adding to the stock of government debt. As Palma puts it, "in their new tax status, corporations and the very rich now prefer to part-pay/part-lend their taxes, and part-pay/part-lend their wages."

In rich countries, middle-income groups have largely maintained their share of national income. But their living standards have fallen, owing to the rising costs of essential goods and services (such as housing, health care, and education), falling real pensions, regressive taxation, and rising personal debt. Most emerging-economy governments, meanwhile, are not implementing significant fiscal measures to reduce market inequality.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources. Specifically, this increase in value extraction is the result of policies for which the rich have actively lobbied: privatization; deregulation of share buybacks that artificially inflate stock prices; patent laws that make drugs much more expensive; reduction or elimination of top marginal tax rates; and much else.

Giving the rich all this additional income has not resulted in higher investment rates in the OECD or in unequal middle-income countries. Instead, the rich are content to pluck the low-hanging fruit of rent extraction, market manipulation, and lobbying power. High profits therefore coexist with low investment and increasing market inequality, in a self-reinforcing pattern. This trend not only magnifies the risk of economic stagnation and market failures; political changes around the world suggest that it has also become a profound threat to democracy.

Addressing this dangerous state of affairs will require that governments use their power to tax and regulate to channel more private capital into productive spending and increase the amount of public investment financed by progressive taxation, along the lines of a Global Green New Deal. If policymakers fail to mount a response that is proportionate to the problem, the rich will continue to get richer, and the poor to get poorer, faster than ever. Who will address the problem then?

Since reducing inequality became an official goal of the international community, income disparities have widened. This trend, typically blamed on trade liberalization and technological advances that have weakened the bargaining power of labor vis-a-vis capital, has generated a political backlash in many countries, with voters blaming their economic plight on "others" rather than on national policies. And such sentiments of course merely aggravate social tensions without addressing the root causes of worsening inequality.

But in an important new article, University of Cambridge economist Jose Gabriel Palma argues that national income distributions are the result not of impersonal global forces, but rather of policy choices that reflect the control and lobbying power of the rich. In particular, Palma describes the significant recent increase in inequality in OECD countries, the former socialist economies of Central and Eastern Europe, and China and India, as a process of "reverse catching-up." These countries, Palma says, increasingly resemble many unequal Latin American economies, with rent-oriented elites grabbing most of the fruits of growth.

In his earlier work, Palma showed how middle and upper-middle income groups' share of total income has remained remarkably stable in most countries over time, at about one-half. Changes in aggregate income distribution, therefore, resulted largely from changes in the respective shares of the top 10% and the bottom 40% of the population (the ratio between these shares is now called the "Palma ratio").

In other words, the huge variation in inequality across countries, and particularly between middle-income economies, is essentially the outcome of a fight for around one-half of national income involving one-half of the population. Only in cases of extreme inequality (such as South Africa) did the top 10% also manage to encroach on the income share of the middle.

It is misleading, therefore, to view rising per capita incomes in middle-income countries as indicating a general improvement in standard of living. In unequal middle-income economies such as those in Latin America, the incomes of the top 10% are already on par with those of their rich-country counterparts. The incomes of the bottom 40% are closer to the Sub-Saharan African average.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources.

The driving force behind these trends is market inequality, meaning the income distribution before taxes and government transfers. Most OECD countries continually attempt to mitigate this through the tax and transfer system, resulting in much lower levels of inequality in terms of disposable income.

But fiscal policy is a complicated and increasingly inefficient way to reduce inequality, because today it relies less on progressive taxation and more on transfers that increase public debt. For example, European Union governments' spending on social protection, health care, and education now accounts for two-thirds of public expenditure, but this is funded by tax policies that let off the rich and big corporations while heavily burdening the middle classes, and by adding to the stock of government debt. As Palma puts it, "in their new tax status, corporations and the very rich now prefer to part-pay/part-lend their taxes, and part-pay/part-lend their wages."

In rich countries, middle-income groups have largely maintained their share of national income. But their living standards have fallen, owing to the rising costs of essential goods and services (such as housing, health care, and education), falling real pensions, regressive taxation, and rising personal debt. Most emerging-economy governments, meanwhile, are not implementing significant fiscal measures to reduce market inequality.

The dramatic increase in market inequality reflects the ability of the top 10% to extract more value created by others and to profit from existing assets - including those that should be public property, such as natural resources. Specifically, this increase in value extraction is the result of policies for which the rich have actively lobbied: privatization; deregulation of share buybacks that artificially inflate stock prices; patent laws that make drugs much more expensive; reduction or elimination of top marginal tax rates; and much else.

Giving the rich all this additional income has not resulted in higher investment rates in the OECD or in unequal middle-income countries. Instead, the rich are content to pluck the low-hanging fruit of rent extraction, market manipulation, and lobbying power. High profits therefore coexist with low investment and increasing market inequality, in a self-reinforcing pattern. This trend not only magnifies the risk of economic stagnation and market failures; political changes around the world suggest that it has also become a profound threat to democracy.

Addressing this dangerous state of affairs will require that governments use their power to tax and regulate to channel more private capital into productive spending and increase the amount of public investment financed by progressive taxation, along the lines of a Global Green New Deal. If policymakers fail to mount a response that is proportionate to the problem, the rich will continue to get richer, and the poor to get poorer, faster than ever. Who will address the problem then?