SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

A Greenpeace representative urged governments to recognize the "once-in-a-generation opportunity to make those most responsible for the climate, nature, and inequality crises we are facing pay their share.”

As world governments meet at the United Nations for another round of negotiations on a first-of-its-kind "Global Tax Treaty," economic justice campaigners are urging them to think big or risk leaving on the table trillions of dollars that could help alleviate global inequality and the climate crisis.

The fifth round of negotiations for the treaty began in New York on Monday, with countries ironing out its language line by line as they seek a global framework to more fairly tax the rich and multinational corporations and crack down on tax avoidance.

Jenny Ricks, the general secretary of the Fight Inequality Alliance—a global coalition of anti-inequality groups—said the framework, which was first conceived in 2022 at the urging of poorer nations in Africa, "aims to make global tax governance more inclusive, transparent, and equitable, shifting it away from the Organization for Economic Cooperation and Development (OECD) and giving the global majority a genuine say in rules that have long been set by wealthy states."

The first drafts of the proposed tax convention were released in late July in advance of this month's negotiations. Advocates at Greenpeace International, however, argue that they contain many gaps that fail to adequately tax fossil fuel companies driving the climate crisis or other multinational corporations and extremely wealthy individuals.

In a briefing document released to media organizations, Greenpeace argued that the text lacks clear language linking taxation to sustainable development, despite it being demanded by 24 countries, and that it lacks provisions requiring polluters to bear the public cost of environmental damage.

The group also criticized the weakening of an article covering taxes on high-net-worth individuals, the lack of a minimum tax on multinational profits, and the absence of specific rules for taxing extractive industries such as oil, gas, and mining.

The oil and gas industry, the group pointed out, is in the midst of a boom, with companies reporting record profits as President Donald Trump's war against Iran drives global oil prices higher.

"The money is right there," said Nina Stros, Greenpeace International's global senior policy expert. "It is about time governments recognized this once-in-a-generation opportunity to make those most responsible for the climate, nature, and inequality crises we are facing pay their share, and reclaim trillions of dollars to invest in our shared future.”

An open letter from Tax and Fiscal Justice Asia, a group of over 50 civil society organizations across 13 Asian countries, emphasized many of the same concerns that the conference could end up merely affirming broad principles without creating concrete rules.

They said representatives of Asian nations at the negotiating table needed to push for a shift in taxing power away from wealthy countries where corporate headquarters are located and toward poorer ones where much of the workforce and resources are concentrated. They also argued for a move away from regressive consumption taxes that disproportionately fall on lower-income people.

"The majority of states in Asia were among the 125 states that voted in November 2023 to adopt a resolution for a UN Framework Convention on International Tax Cooperation (UNFCITC)," the letter said. "The vote has brought forth a historic opportunity to leave behind unjust systems and build a new global tax architecture."

The companies avoided more than $26.7 billion in income taxes last year, enough to give free school lunches to every child in America.

Dozens of America's most profitable corporations avoided paying any federal income taxes in 2025, according to an analysis out on Tuesday from the Institute on Taxation and Economic Policy.

The 88 companies—which include Tesla, Southwest Airlines, Live Nation, Palantir, Citigroup, and many others listed in the S&P 500—brought in a collective $105 billion in pretax income last year.

ITEP found that 2025 saw a spike in corporate tax avoidance, enabled in part by new loopholes created by the One Big Beautiful Bill Act signed by President Donald Trump and by his 2017 Tax Cuts and Jobs Act, which reduced the corporate tax rate to 21% from its previous 35%.

The One Big Beautiful Bill Act is expected to hand the wealthiest 1% of Americans $117 billion in tax cuts this year, while those in the bottom 95% are set to pay more in taxes while facing across-the-board cuts to social safety net programs like Medicaid and the Supplemental Nutrition Assistance Program.

It also allowed multimillion- and billion-dollar corporations to find new ways to avoid paying taxes. More than half of the tax-avoiders listed in the report used a provision in the new tax law allowing companies to immediately write off capital investments, reducing their collective taxes by $11.4 billion.

Pharmaceutical and tech companies, meanwhile, were able to take advantage of tax write-offs for research and development, exempting them from approximately another $4.4 billion.

In total, the corporate tax avoidance documented in 2025 by the researchers helped to rob the public coffers of yet another $26.7 billion, enough to give every public school student a free lunch for a year, according to a University of Missouri analysis of the National School Lunch Program.

The researchers said that the full scale of corporate tax avoidance remains unclear, since corporate tax returns are not publicly available. Some companies were also excluded because they are not part of the S&P 500 or have not yet reported their 2025 taxes.

“These findings are not isolated cases—they reflect systemic deficiencies in the corporate tax code,” said Amy Hanauer, the executive director for ITEP. “Without meaningful reform, profitable corporations will continue to pay less than their fair share.”

Billionaire tax avoidance stems directly from the reality that America’s tax on capital gain income remains a steeply regressive tax.

The recent wedding of Jeff Bezos and Lauren Sánchez in Venice set off quite the furor over tax avoidance. An enormous banner in the Piazza San Marco put the matter plainly: “If you can rent Venice for your wedding, you can pay more tax.”

That banner prompted a commentary from Phoebe Liu at Forbes on how much tax Bezos does indeed pay. For the year 2024, according to a Forbes estimate, Bezos paid about $2.7 billion in tax on the gain from his sale of $13.6 billion worth of Amazon stock. That stock—the heart of the Bezos fortune since he started Amazon in 1994—originally cost him no more than $13,600.

In other words, some 99.9999% of the proceeds of the Bezos stock sale last year counted as a taxable long-term capital gain. This Forbes tax estimate took into account charitable contributions of Amazon stock that Bezos likely claimed as a 2024 deduction.

The Bezos $2.7 billion income tax payment, Liu noted in her Forbes analysis, represented only 4.5% of the 2024 increase in his personal net worth—approximately $60 billion—and barely more than 1% of his overall $230 billion net worth.

We have a tax system, in short, that favors the wealthiest Americans and fosters extreme wealth concentration.

Props to Liu for her reporting. She has helped shine a light on how undertaxed America’s billionaires have become even in years when they pay billions of dollars in tax.

But I wonder: What would the reporting have looked like if Bezos had sold all $200 billion or so of his Amazon stock? Would we be reading that he paid $40 billion in tax—a sum equal to over 20% of his net worth—with a suggestion that he paid his fair tax share? Yeah, we probably would. Not necessarily from Liu, but apologists for the ultra-rich would have been all over it.

Which raises the question: Should our view of how much the ultra-rich pay in tax turn on how much of their investments—as a share of their total wealth—they sell in a given year or on how much their overall wealth happens to increase in that specific year?

Bezos, for example, has sold over $600 million of Amazon shares so far this year, with the apparent intention to sell a bunch more. The value of Amazon shares this year has not increased much. He may well pay more in tax on those sales than his wealth increase for the entire year. Would that mean he’s overtaxed? Of course not.

So how can we better understand billionaire tax avoidance? By focusing only on billionaire taxable transactions, without reference to irrelevant data such as their total wealth or the annual increase in their total wealth.

Consider just the Amazon shares Bezos sold last year, shares worth an astounding 1 million times what he had paid for them 30 years earlier. The average annual increase in the value of those shares, when you do the math, turns out to be 58.5%, an incredible performance.

Now assume Bezos paid the full 23.8% tax rate on his gains, without taking those charitable contributions into consideration. That would leave him with $10.36 billion after tax, a total that translates to an after-tax average annual rate of increase of 57.1% and a reduction of less than 2.5% from his pre-tax annual rate of increase.

This means that the maximum federal income tax Bezos could have paid on the gain from his 2024 Amazon stock sales amounts to the same end result as would an annual tax on the increase in value of his Amazon shares of 2.5%, assuming the tax were paid from sale of the stock. And the result would be the same—an effective annual tax rate of 2.5%—had Bezos sold all his Amazon shares last year or if 2024 happened to be a year when his wealth didn’t increase much.

Tax avoidance by billionaires, these numbers help us see, doesn’t essentially come from the amount of income these rich report in a given year compared to their wealth or even the amount of income they report in a year compared to that year’s increase in their wealth. Billionaire tax avoidance stems directly from the reality that America’s tax on capital gain income remains a steeply regressive tax.

As I’ve noted previously, the longer a deep pocket holds an investment and the greater the annual rate of increase in value that investment yields, the lower the effective annual federal income tax rate will be when the investment finally gets sold. The effective annual tax rate on long-term, high-yield investments can end up at less than one-fifth the rate on short-term, low-yield investments.

More than all other taxpayers, our wealthiest find themselves easily able to hold investments for long periods of time. We have a tax system, in short, that favors the wealthiest Americans and fosters extreme wealth concentration.

And if we can’t figure out how to reform that tax system soon, heaven help us.

"Accountability is an existential threat to their business model, and their business model is an existential threat to all of us, and that’s the bottom line," said Meghan Sahli-Wells, the former mayor of Culver City.

As devastating wildfires continue to burn in the Los Angeles region on Wednesday—placing tens of thousands of Californians under evacuation orders and causing over $250 billion in economic damages by one estimate—a pair of new reports highlight how fossil fuel companies have dodged responsibility for their role in the destruction and hampered the state's ability to fight back by depriving it of funds.

California's fossil fuel industry deployed lobbying muscle to kill legislation that would compel polluters to pay into a fund that would help prevent disasters and aid cleanup efforts, and has taken advantage of a tax loophole to deprives the state of corporate tax revenue, thereby "putting climate and social programs in peril." In the case of the former, California's biggest fossil fuel trade group, the Western States Petroleum Association, recently launched a digital campaign that appears aimed at throwing cold water on any such legislative efforts.

According to The Guardian, the Polluters Pay Climate Cost Recovery Act of 2024 appeared on 76% of the 74 lobby filings submitted in 2024 by the oil company Chevron and the Western States Petroleum Association.

The legislation—which didn't make it out of the state senate in 2024—would, if enacted, create a recovery program forcing fossil fuel polluters to pay their "fair share of the damage caused by the sale of their products" during the period of 2000 to 2020, according to the nonprofit newsroom CalMatters.

According to The Guardian, the filings from those two firms that included this specific bill totaled over $30 million—though lobbying laws do not require a breakdown that would make clear how much was spent specifically on the "polluter pay" law.

With Los Angeles burning, there's renewed interest in passing the bill, The Guardian reports, citing supporters of the legislation. But Western States Petroleum Association isn't sitting idly by. On January 8, the group launched ads that suggest measures like the "polluter pay" bill would force them to increase oil prices. The ads, which appear to have been taken down, do "not specifically mention the polluter pay bill, it echoes the 2024 campaign that did," wrote The Guardian.

"Accountability is an existential threat to their business model, and their business model is an existential threat to all of us, and that’s the bottom line," said Meghan Sahli-Wells, the former mayor of Culver City who currently works for the environmental advocacy group Elected Officials To Protect America, told the paper.

Meanwhile, another report from The Climate Center—a think tank and "do-tank" focused on curbing pollution—has thrust a tax loophole long used by multinational oil and gas companies, into the spotlight.

The report released last week details how "years of litigation and lobbying by oil and gas majors like ExxonMobil, Chevron, and Shell Oil" are responsible for a large corporate tax avoidance policy that is known as the "Water's Edge election" that became law in 1986.

The law allows multinational corporations to "elect" avoid taxes on earnings they designate as beyond the "water's edge" of the borders of states in which they operate, according to The Climate Center.

"Closing the loophole as it applies to the oil and gas industry could put anywhere between $75 to $146 million per year back into the state’s budget," the report states.

For context, California closed a $46 billion budget shortfall last year, including by enacting cuts to climate and clean air programs.

"The water's edge tax loophole allows multinational fossil fuel corporations to dodge paying their fair share of taxes that can help fund vital environmental projects, which could include wildfire preparedness," California Assemblymember Damon Connolly (D-12) told the progressive outlet The Lever, the first outlet to report on the findings.

California lawmakers last year passed a bill that took aim at some aspects of the loophole, but an advocacy group whose board of directors includes representative from the oil and gas industry has filed lawsuit challenging the constitutionality of the reform, according to the The Climate Center.

The bill would end two of the ultra rich’s favorite tax-avoidance strategies: “Buy-Borrow-Die” and “Buy-Hold for Decades-Sell.”

America’s ultra-rich today love to play tax-avoidance games. One of their favorites goes by the tag “buy-borrow-die,” a neat set of tricks that lets billionaire households avoid any taxes on the gains they make from their investments.

The simple rules of the buy-borrow-die game: buy an asset—with your millions or billions—and watch it grow. If you have a hankering to pocket some of that gain, don’t sell the asset. Any sale would trigger a capital gains tax. Just borrow against that asset instead, a simple move that lets you avoid capital gains levies so long as you live.

And what happens when you die? Nothing! Your asset’s untaxed gains vanish for income tax purposes under a tax code provision known as “stepped-up basis.”

Thanks to this buy-hold for decades-sell, the effective tax rate on the multi-billion dollar gains of America’s Bezoses, Gateses, and Buffetts, even when they do sell assets before they die, approaches zero.

This buy-borrow-die, progressive lawmakers like U.S. Sen. Ron Wyden from Oregon believe, amounts to a game plan for creating dynastic fortunes. Wyden has proposed an antidote, dubbed the “Billionaires Income Tax,” which would require billionaires to pay tax annually on the gains they make from tradable assets like the corporate shares that list on stock exchanges.

Gains from non-tradable assets would go untaxed, under Wyden’s proposal, but only until the assets get sold, at which point the tax rate would be increased to account for the tax-free compounding of annual gains. And those who inherit millions and billions from billionaires would no longer, under Wyden’s bill, be able to benefit from our current tax code’s magical stepped-up basis.

Closing the buy-borrow-die loophole would, all by itself, be reason enough for passing Wyden’s Billionaires Income Tax bill. But buy-borrow-die may only be the second leakiest loophole Wyden’s proposal would close. His Billionaires Income Tax proposal would also shut down a far less well-known loophole I like to call “Buy-Hold for Decades-Sell.”

How does this loophole work? Consider two rich taxpayers, Jack and Jill. Each invests $10 million in a stock they hope will grow at a 10% annual long-term rate, a good but not great return for a rich investor. Investors in Berkshire Hathaway, for example, have seen average annual returns of about 20%.

Our Jack goes on to hold his stock for 30 years and realizes exactly the 10% annual return he hoped to achieve.

Jill opts for a more aggressive investment strategy. After holding her stock for just over one-year, long enough to qualify her profits for the preferential tax rate available to long-term capital gains, Jill then sells at an 11% gain, pays tax on the gain, and invests the remaining proceeds in a stock she believes has more potential going forward. She successfully repeats this strategy each year for 30 years.

You might guess that Jill’s eventual nest egg at the end of 30 years, after paying federal income tax at the current long-term gains rate of 23.8%, would be larger than Jack’s. But, despite Jill’s superior investment acumen, Jack’s $135 million nest egg turns out to be 20% larger than Jill’s $112 million nest egg.

How could that be? Jack, to be sure, does pay the same 23.8% tax on his capital gain as Jill. But Jack’s money has had the benefit of 30 years of compounding before Jack has to pay that tax. That benefit far outweighs Jack’s lower annual investment return.

Jack’s whopping tax benefit from holding an appreciating asset for several decades should give us pause. After all, we want investors to seek the highest yielding investments, not the ones that get the best tax treatment. We don’t want developers of promising new technologies, for example, struggling to raise capital because our tax law confers higher returns on investors who just keep on holding old, under-performing investments.

In our example, Jill’s annual tax of 23.8% on her gains reduces Jill’s 11% pre-tax rate of return to an after-tax return of 8.38%. But Jack, because he gets to defer the tax on his 10% annual gains for 30 years, sees the after-tax return on his investment reduced by only 0.93 percentage points, to 9.07%.

As a result, Jack, a poorer investor than Jill, has millions more wealth on hand at the end of 30 years.

What tax rate would Jack have to pay annually on the growth in his stock value to place him in the same position at the end of 30 years as a one-time tax of 23.8% upon the sale of that stock? He’d only have to pay tax at a 9.3% annual rate. That 9.3% would actually run lower than the 10% income tax rate that our federal tax code currently expects Americans with incomes barely above the poverty level to pay.

In some extreme cases today, our super rich can enjoy an effective annual tax rate on their investments far lower than Jack’s.

Consider a lucky Berkshire Hathaway investor who bought 100 shares back in 1979 at $260 per share, a $26,000 investment. That investor’s shares would be worth about $70 million today. The annual pre-tax return on those shares would be 19.19%. If the investor sold the shares and paid tax at 23.8% on the long-term gain, the investor would be left with about $53.35 million.

The investor’s annual rate of return after-tax would be 18.47%, a trifling 0.72 percentage point reduction from this investor’s pre-tax rate of return. The effective annual rate of tax on the growth in the investor’s stock value would be 3.75%, less than one-sixth the 23.8% one-time rate on the investor’s compounded gains.

That about sums up perfectly the magic of buy-hold for decades-sell, the loophole that causes the effective annual tax rate on the growth in the value of investments to decline as the rate of return and length of holding period increase. Thanks to this buy-hold for decades-sell, the effective tax rate on the multi-billion dollar gains of America’s Bezoses, Gateses, and Buffetts, even when they do sell assets before they die, approaches zero.

We don’t need to just close the buy-borrow-die loophole. We desperately need to shut the buy-hold for decades-sell loophole just as firmly.

"Corporate tax avoidance occurs because Congress allows it to occur, and the Trump tax law made it worse," says a new study by the Institute on Taxation and Economic Policy.

Many large, profitable U.S. companies paid little to nothing in federal taxes during the first five years of the 2017 Trump-GOP tax law, an unpopular measure that slashed the corporate tax rate from 35% to 21% and introduced new loopholes that the rich and powerful rushed to exploit.

A study released Thursday by the Institute on Taxation and Economic Policy (ITEP) examines 342 companies that were profitable during each of the first five years of the tax law's enactment. The new research shows that corporate tax avoidance has been rampant under the law, with 23 of the companies included in the study paying nothing in federal taxes between 2018 and 2022 and 109 businesses paying nothing in at least one of the five years.

Kinder Morgan, NRG Energy, and T-Mobile were among the profitable companies that paid a 0% or negative effective tax rate during the study period.

"When President [Donald] Trump and congressional Republicans slashed the statutory corporate income tax rate from 35% to 21%, they could have maintained or even increased the effective rate paid by corporations by shutting down special breaks and loopholes in the corporate income tax," reads the new report. "But from the very beginning of the debate over the 2017 legislation, it was clear their goal was to allow corporations to contribute less to the public investments and the society that makes their profits possible."

Nearly a quarter of the companies analyzed by ITEP "paid effective tax rates in the single digits or less" during the law's first five years, including prominent corporations such as Netflix, Nike, and Citigroup.

ITEP found that the "industries enjoying the lowest five-year effective tax rates were utilities (negative 0.1%); oil, gas, and pipelines (2.0%); motor vehicles (3.2%); and telecommunications (7.7%)."

On average, the 342 companies included in the analysis paid an effective tax rate of 14.1% between 2018 and 2022—significantly less than the 21% statutory rate established by the Tax Cuts and Jobs Act.

The difference between what companies would have paid in taxes if they were held to the 21% statutory rate and what they actually paid amounts to a major taxpayer subsidy, ITEP said. The 342 companies received a combined $275 billion in subsidies during the first five years of the Trump-GOP tax law, with the majority going to just 25 companies.

Bank of America received the largest tax break of all the companies analyzed—$23.89 billion.

"For many of the biggest corporations in America, our 21% tax rate is an accounting fiction," said Matt Gardner, a senior fellow at ITEP and the lead author of the new study. "Because of an array of special-interest tax breaks, the most profitable corporations in America routinely pay effective tax rates far below the legal rate."

"It does not have to be this way. Congress should take more steps to crack down on this widespread corporate tax avoidance."

While corporate tax avoidance certainly didn't begin with the 2017 tax law, ITEP's study notes that it "did little to change" the status quo—"except to allow companies to pay less than ever."

"Corporate tax avoidance occurs because Congress allows it to occur, and the Trump tax law made it worse," the analysis says.

Some notorious tax avoiders, such as Amazon, were excluded from the study because they reported a loss during at least one of the five years that ITEP examined. Amazon paid an effective tax rate of 8.9% between 2018 and 2022.

"Americans who heard President Trump and his supporters in Congress tout the 21% corporate income tax rate they enacted in 2017 may be alarmed to hear that so many corporations pay much less than that in reality," said Steve Wamhoff, ITEP's federal policy director and report co-author. "But it does not have to be this way. Congress should take more steps to crack down on this widespread corporate tax avoidance."

The report specifically advocates a global minimum tax that would require multinational companies to pay an effective rate of at least 15%, a proposed change aimed at cracking down on profit-shifting. The Biden administration negotiated a global minimum tax deal with other nations in 2021, but the divided U.S. Congress has yet to advance the proposal.

"Drafters of the Trump tax law made some token efforts to address these problems, for example, by imposing a weak U.S. tax on certain profits that American corporations claim to earn offshore," ITEP's report observes. "This left the corporate income tax in dire need of the Biden administration's efforts to reform it."

"What little credibility the OECD had is now in tatters," said one campaigner. "The OECD makes promises about ending global tax abuse but was evidently doing everything it could behind closed doors to protect tax abusers."

The Financial Times confirmed Friday that the Organization for Economic Cooperation and Development lobbied Australia to weaken a law that would have compelled about 2,500 highly profitable multinational corporations to reveal where they pay taxes, eliciting outrage from tax justice advocates.

Citing two unnamed people familiar with the discussions, FT reported that the Paris-based club of wealthy nations "pressured Australia's ruling Labor government to drop a crucial part of a new finance bill that would have required some multinationals to publicly disclose their country-by-country tax bills."

"This shows the true colors of the OECD."

According to the newspaper, "The OECD, which has driven efforts to force the world's largest companies to pay their fair share of tax, believed the bill would have undermined its own efforts to make multinationals' affairs less opaque."

Campaigners were incredulous given that the legislation the OECD enfeebled "would have delivered the biggest transparency breakthrough to date on the taxes of multinational corporations," as the Tax Justice Network put it.

The advocacy group estimates that multinationals shift more than $1.1 trillion of profit into tax havens annually, costing the world $312 billion per year in foregone corporate tax revenue. It also calculates that at least 1 of every 4 of those lost tax dollars could be saved if corporations were required to publish country-by-country reporting data.

"The OECD yet again doing the bidding for big business, the only winners here," tweeted Nabil Ahmed, economic justice director at Oxfam America.

Ahmed's observation was shared by Isabel Ortiz, the former director of social protection at the United Nations' International Labor Organization, who said, "This shows the true colors of the OECD and who [it is] serving."

Australia's original proposal "would have exposed unprecedented details about companies' tax affairs in each country they operate," FT reported, aiding efforts to crack down on tax evasion by forcing an estimated 21% of the world's multinational corporations—including many of the biggest firms in history—to come clean about "how much of their revenues are booked in low-tax jurisdictions."

As the newspaper explained:

The bill was expected to clear the Australian parliament in June and come into force on July 1. However, the version of the bill that passed last month removed crucial disclosures, with the Australian government announcing a delay of the planned public country-by-country tax reporting regime for a year.

People close to the decision said officials from the intergovernmental body had stressed to the Australian Treasury that countries that signed the 2015 OECD agreement did so on the basis the tax reports would not become public.

"This is not a good look for the OECD," the Fair Tax Foundation wrote on social media. "Their work is by definition consensus-based and often lowest common denominator. If a country wants to push on and do something more substantial, they should applaud, not oppose."

David McNair, executive director of global policy at the anti-poverty nonprofit One, argued that "this story seriously undermines the OECD's credibility in the one area that it was leading in recent years."

"I hope it prompts some soul searching on the mission and values of the organization," he added.

"OECD has put itself firmly on the side of secrecy—on the side of tax abuse—against one of its members. That's an extraordinary state of affairs."

As FT observed, "For the past decade the OECD has spearheaded global efforts to close loopholes and restrict the use of tax havens after it was asked by the G20 in 2013 to address the growing problem of corporate tax avoidance."

"While large multinationals already report some country-by-country data to tax authorities under an international agreement brokered by the OECD in 2015, the Australian proposal would have disclosed additional new data points," the newspaper noted. "And crucially the OECD country tax reports are not shared with the public."

FT's article corroborates earlier reporting by the Center for International Corporate Tax Accountability and Research (CICTAR) and the Tax Justice Network.

Two weeks ago, immediately after the Australian government unexpectedly postponed key components of its landmark bill, both groups suggested that "lobbying against the legislation by multinational corporations and their professional enablers may have been bolstered by the OECD itself—the organization which claims to set international tax rules in order to reduce corporate tax abuse."

In the wake of FT's bombshell story, Tax Justice Network chief executive Alex Cobham said in a statement that "what little credibility the OECD had is now in tatters."

"The OECD makes promises about ending global tax abuse," said Cobham, "but was evidently doing everything it could behind closed doors to protect tax abusers."

The Australian law opposed by the OECD – which may yet be adopted despite the delay – would force one 1 in 5 multinational corporations around the world to come clean about their profits and taxes. This includes many of the world’s biggest multinational corporations... pic.twitter.com/9j3KqNPee4

— Tax Justice Network (@TaxJusticeNet) July 8, 2023

Cobham called it "genuinely shocking to see it confirmed that the OECD has lobbied its own member country against introducing a key measure to fight corporate tax abuse."

"Public country-by-country reporting, when it arrives, will increase revenues around the world to the tune of billions of dollars, by exposing the most egregious profit shifting," Cobham continued. "Investors will benefit from reduced risk in their shareholdings, and employees will benefit both from lower risk and from the chance to negotiate fairly based on a true reporting of the profits of their work. Smaller and domestic businesses will benefit from a more level playing field, instead of a system that subsidizes multinationals' tax bills by effectively granting them immunity from abuse."

"OECD has put itself firmly on the side of secrecy—on the side of tax abuse—against one of its members. That's an extraordinary state of affairs," he added. "And it couldn't send a clearer signal to countries wondering whether the OECD's proposed tax rules will help them to curb tax abuse. They won't, and countries should pursue their own alternatives while preparing for negotiations to establish a proper tax body at the United Nations instead."

Supporters of UN tax leadership have pointed to the OECD’s failure to meaningfully include most countries in its rulemaking process – a concern unlikely to be eased by news of the OECD lobbying its own member against introducing a key measure to fight corporate tax abuse.

— Tax Justice Network (@TaxJusticeNet) July 8, 2023

As economic historian Adam Tooze pointed out, the OECD strong-armed Australia's left-leaning government while being led by Mathias Cormann, a right-wing Australian who previously served as the country's finance minister.

On Saturday, Cormann said in a statement that "the OECD has a proud record of facilitating global cooperation on tax policy and administration, to help ensure globally effective measures to tackle multinational tax avoidance."

"Suggestions the OECD pressured Australia into weakening legislation to tackle such tax avoidance are false," he claimed.

Cobham criticized Cormann's response, pointing out that the OECD secretary-general goes on to admit that the body's experts "raised a number of technical issues," after which Australian lawmakers watered down their proposal.

According to Cobham, the "possible unintended consequences" brought up by OECD experts are "flat wrong." He added that "Cormann seems to have confessed that the OECD did lobby Australia to weaken their proposals to fight corporate tax abuse... and also that they used a false threat to do so—one which, as experts in their own standard, they surely knew was erroneous."

The Republican Party's inability to agree on a new speaker is dangerous and ridiculous, but we can be glad to see it delay their destructive agenda.

Republicans’ inability to agree on a new Speaker of the House of Representatives is dangerous for a variety of reasons and an embarrassment to the country. But no one should shed any tears over the delay this creates for the House Republicans in passing their first legislative priority, a bill to facilitate tax crimes by the wealthy.

The “Family and Small Business Taxpayer Protection Act” would rescind 90 percent of the new funding for the Internal Revenue Service included in last year’s Inflation Reduction Act. This would eliminate the new law’s $45.6 billion to enforce the tax code for people making more than $400,000 and repeal an additional $26 billion in IRS funding that would include, among other things, a pilot for a free e-file program to make it easier for people with relatively simple tax returns to file. The slash-and-burn bill comes just weeks after Republicans forced a 2 percent cut in annual IRS funding as part of the omnibus spending plan.

The funding for tax enforcement is critical to allowing the IRS to do one of its most important jobs: crack down on tax evasion by the extremely wealthy and by big corporations. The IRS has had a hard time doing this lately – as evidenced by its failure to properly audit Donald Trump’s tax returns – because its enforcement budget was cut by about a fourth between 2010 and 2021, after adjusting for inflation. This led to a 40 percent drop in revenue agents – the auditors uniquely qualified to examine the returns of high-income individuals and corporations – over the same time. The number of revenue agents is the lowest it’s been since 1953.

As a result, the gap between taxes owed and paid keeps growing, driven largely by sophisticated accounting tricks used by higher-income households and large corporations. The most recent estimated gross tax gap, for 2014 through 2016, was $496 billion – an increase of $58 billion from the previous estimate.

At the same time, the funding cuts Republicans seek would make it more difficult and expensive for non-wealthy people to file their taxes. Filing taxes should be a quick and painless process for people with straightforward income, so lawmakers included instructions in the IRA for the IRS to form a pilot for a free e-file program. Now, the GOP House majority wants to kill this program, inevitably pushing filers toward predatory private services like the TurboTax “Free Edition” that charged filers hundreds of dollars despite the clear implication of its advertising.

The funding cuts would also hit essential taxpayer services, meaning many people might end up waiting longer to receive refunds or get answers to questions. The bill includes more than $25 billion in cuts to “Operations Support” – things like communications and information technology that help the agency work better.

Republicans’ inability to agree on a new speaker is dangerous and makes the United States look bad. But we’re glad to see it delay their also-dangerous attempts to defund the IRS and to let wealthy tax criminals evade law enforcement.

"Yes. Dr. King was right," says the U.S. Senator from Vermont. "We have socialism for the rich, rugged capitalism for the rest."

Senator Bernie Sanders is not asking anyone to be shocked that Donald J. Trump was very good at not paying taxes, but he also wants people to know that the disgraced former Republican president is far from the only rich person or powerful corporation who gets away with paying little or nothing each year federal income tax.

In a tweet on Friday evening, Sanders said: "When it comes to tax avoidance, Trump is not alone."

Sanders then listed a handful of well-known and highly-profitable companies that paid nothing in federal income tax in 2020, the most recent year detailed figures are available for many companies.

"Yes. Dr. King was right," added Sanders: "We have socialism for the rich, rugged capitalism for the rest."

On Friday, the House Ways and Means Committee released to the public Trump's tax returns after a yearslong legal fight to obtain them from the IRS after the former president broke with precedent by refusing to release them voluntarily.

What the returns and associated documents released by the committee show is an inside look into how very wealthy individuals diminish their tax liability or pay nothing at all year after year.

Specifically in 2020, Trump—despite his vast business holdings—paid no federal income taxes at all. Also in 2020, despite repeated promises to the public that he would donate all his presidential salary to charity, the New York Times reported Saturday that the tax returns reveal he made no charitable gifts that year.

According to the Institute on Taxation and Economic Policy (ITEP), at least 55 major U.S. corporations—including those named by Sanders—paid $0 in federal taxes on massive profits in 2020.

ITEP's analysis shows that these 55 corporations "would have paid a collective total of $8.5 billion for the year had they paid [the staturory federal rate of 21 percent]." Instead, including by benefiting greatly from the tax law that Trump and a GOP-controlled Congress passed in 2017, those companies collectively "received $3.5 billion in tax rebates."

In all, that's $12 billion less in taxes paid by some of the most profitable and largest companies in the nation.

As numerous outlets have detailed, Bloomberg's reporting states how "massive losses and large tax deductions in Donald Trump's returns reveal how the former president was able to use the tax code to minimize his income tax payments." According to the outlet:

The records illustrate how Trump, as a business owner and a real estate developer, is eligible for a bevy of tax breaks that most taxpayers can’t claim. The filings, which cover 2015 to 2020, also detail how Trump was affected by the 2017 tax-cut bill he signed into law.

The documents further show the sheer complexity of the tax code. As for many US business owners, the filings span hundreds of pages to account for domestic and foreign assets, credits, deductions, depreciation, and more.

Warren Gunnels, a top aide and advisor to Sen. Sanders, said Friday night that far-reaching tax breaks is not the only benefit that Trump received which too many regular people are still denied in the United States: free, taxpayer-funded healthcare.

Throughout his presidency, including when he was suffering from Covid-19, Trump was provided care via the Veterans Administration.

"In 2020, not only did Trump pay nothing in federal incomes taxes, not only did he get a $5.47 million tax refund, he also paid ZERO for his hospital stay at Walter Reed—a 100% government-run hospital," tweeted Gunnels.

"Yes," he added, echoing Sanders. "Trump loves socialism for himself, rugged capitalism for the rest."

According to a groundbreaking report released this week, multinational corporations are taking advantage of global tax treaties to avoid paying their fair share, thereby fueling poverty worldwide.

The analysis by Johannesburg-headquartered ActionAid International shows how "rip-off tax treaties cost developing countries billions every year, tying the hands of governments, hurting some of the poorest people in the world, and deepening global inequality," said campaigner Savior Mwambwa.

These treaties dictate how much, and even if countries can tax multinational companies, "have no place in the 21st century," ActionAid declares in its report.

As the Mistreated (pdf) report explains, "Tax revenue is one of the most important, sustainable and predictable sources of public finance there is. It is a crucial part of the journey towards a world free from poverty--funding lasting improvements in public services such as health and education." In particular, the group points out, many poor countries are asking for public funds to be put toward "the realization of women and girls' human rights."

Yet thanks to what Mwambwa calls the "broken tax treaty system," global corporations "pay little or no tax in poor countries."

In turn, he said, "Women and children in poverty pay the price when crumbling public services like schools and hospitals are starved of possible funding."

Indeed, after examining more than 500 binding tax treaties that low- and lower-middle-income countries in sub-Saharan Africa and eastern and southern Asia signed with other countries from 1970 until 2014, the International Development Organization concluded that many such pacts "are ensuring that money flows untaxed from poor to rich countries, making the world more unequal and exacerbating poverty."

ActionAid identifies the UK and Italy as the countries that have entered into the highest number of "very restrictive" tax treaties with African and Asian countries since the 1970s, followed by Germany. The organization notes that China, Tunisia, and Mauritius also have a rapidly growing number of similar treaties with some of the world's poorest countries.

Generally speaking, tax treaties that lower-income countries have signed with members of what ActionAid calls "the [Organization for Economic Cooperation and Development, or OECD] club of rich countries" take away more taxing rights than those with other countries. "Worryingly, the deals struck with OECD countries are getting worse," the group says.

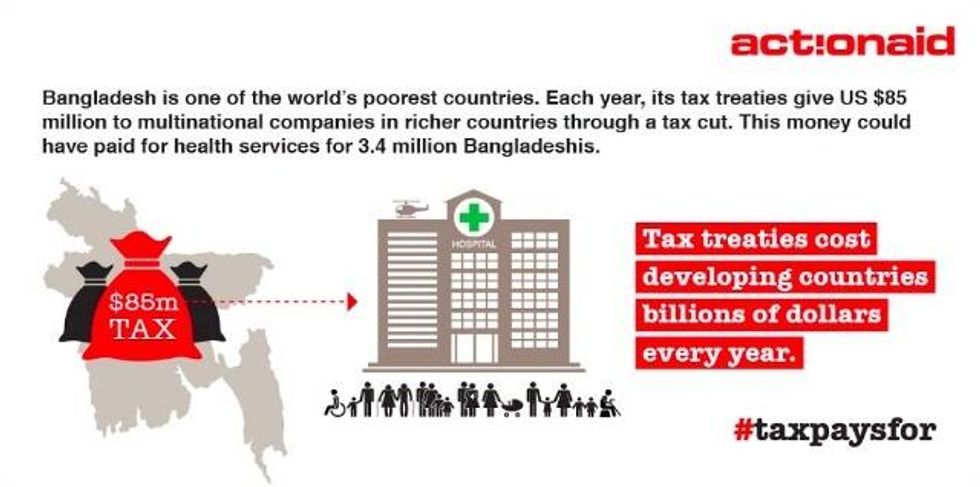

Meanwhile, Bangladesh has given up the most power to tax multinational companies. According to ActionAid, a single clause restricting the country's ability to tax dividends--money paid by companies to overseas shareholders--costs Bangladesh around US$85 million annually.

"This is a country where 66 million people live in extreme poverty--less than US$1.90 a day," the group points out.

The report comes as nations grapple individually and as a bloc with how to close corporate tax loopholes.

In January, Google agreed to a deal with British tax authorities to pay PS130 million (US$143.5 million) in back taxes and bear a greater tax burden in future, after coming under fire for its tax avoidance practices. On Wednesday, the UK Parliament's public spending watchdog criticized the settlement as "disproportionately small."

Indeed, as ActionAid policy advisor Anders Dahlbeck told the Independent last month, "The row over tax dodging by big companies like Google shows how strongly the British public feels that multinationals aren't paying their fair share." But as Mistreated clearly illustrates, "this is just part of a far larger global problem."

Late last month, the 31 OECD members signed an agreement to share information about multinationals' profits and taxation, a move "aimed at stopping firms from using complicated loopholes or moving money across borders to minimize or avoid paying corporate tax," Agence France-Presse reported at the time.

And just this week, it was reported that developing nations will join that effort, under a proposal that would open up the OECD's Committee on Fiscal Affairs to new, associate members that agree to implement certain tax reforms.

The news brought mixed reactions from development groups who said it was too little, too late. "Inclusion after the fact is a poor substitute for a voice in how the standards are designed," said Oriana Suarez of the Latin American Network on Debt, Development, and Rights. "Developing countries now being invited...did not have a say while the rules were being set."

"The OECD is certainly one part of the global fight against tax evasion and tax avoidance, but it's not well-positioned to be the sole standard bearer for the globe," added Porter McConnell of the Washington, D.C.-based Financial Transparency Coalition. "Having its members speak on behalf of the rest of the world's countries is patronizing, and it's ultimately ineffective."