SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"Everybody is hurt by what he's celebrating," one public employee union official told Common Dreams. "I guess it's just par for the course from this administration, but it's still a disgusting thing to hear."

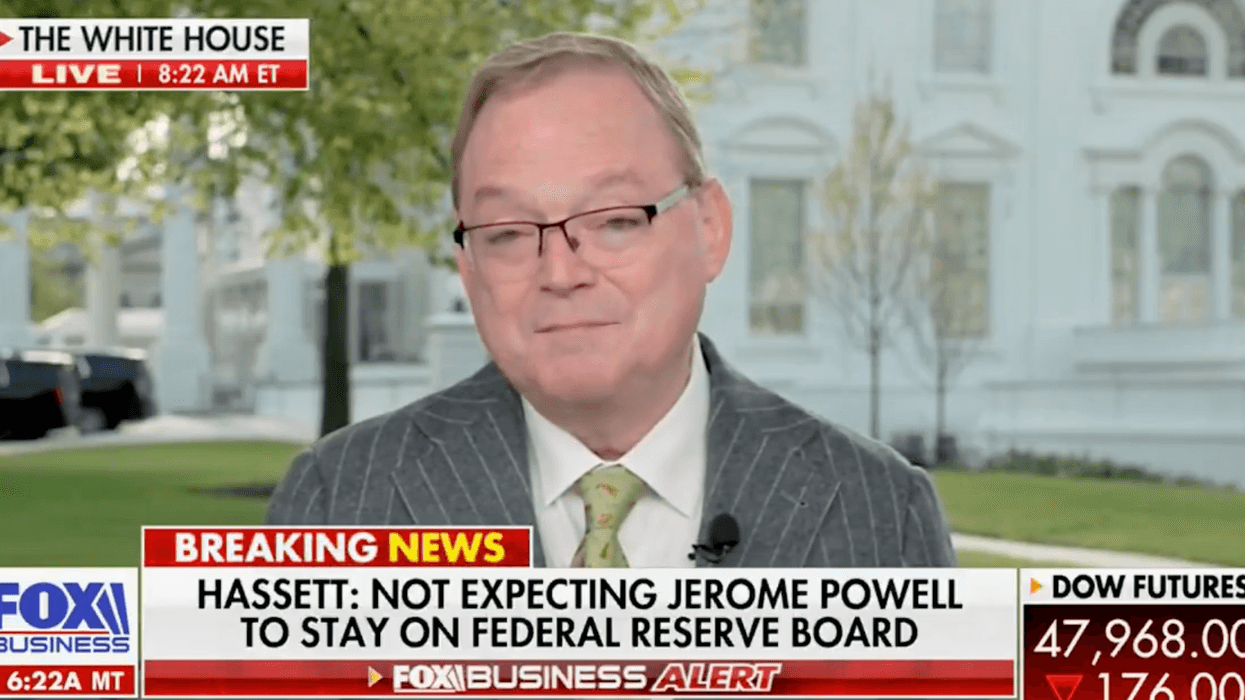

President Donald Trump's top economic adviser boasted on Fox Business Thursday that the government had slashed more than 300,000 "high-paying" jobs from the federal payroll during the president's first year back in office.

Asked by anchor Maria Bartiromo about the administration's efforts to cut government spending, National Economic Council Director Kevin Hassett said it had made "a huge amount of progress."

"I think the biggest thing that we can point to is that we've cut government employment by 300,000 workers," he said. "Those are jobs that are very high-paying that are gone forever."

He claimed the cuts reduced government spending by "an unthinkable amount of money," perhaps $1 trillion over the next ten years.

He also said that the administration "reduced the deficit last year by $600 billion" through a combination of higher-than-expected economic growth, tariff revenues, and "supply side effects" of Trump's massive tax cut, which mostly benefited the wealthiest Americans while gutting the social safety net.

Dean Baker, a longtime collaborator of Hassett’s despite their opposing political beliefs, wrote on social media that Trump’s economic adviser was dramatically exaggerating the deficit reduction that occurred during the administration's first year.

According to the Congressional Budget Office (CBO), the deficit was about $1.8 trillion for fiscal year 2025, just $41 billion less than the previous year and $56 billion lower than the $1.9 trillion deficit CBO projected in its most recent baseline.

"In the real world, the deficit fell... less than one-tenth of what Kevin claims," Baker said.

Trump has touted the layoffs of hundreds of thousands of government employees from their "boring federal jobs" as one of his crowning achievements.

Among the agencies hit by mass layoffs were the Department of Veterans Affairs, where more than 12,700 employees got the axe; the Department of Health and Human Services, which lost more than 14,400 workers; the Social Security Administration, whose staff shrank by more than 6,600; and the Environmental Protection Agency, which lost more than 4,000 employees.

Jacqueline Simon, policy director at the American Federation of Government Employees (AFGE), the largest labor union representing federal workers, told Common Dreams that even if slashing jobs did reduce the deficit as Hassett claimed, the harm far outweighs any such benefit—not only for the fired employees, but for the millions of Americans who depend on services they provide.

"When you say 300,000 jobs, it is a nice round number, and you link it to deficit reduction, which he was lying about," Simon said. "The fact of the matter is, the disappearance of those 300,000 jobs means degraded healthcare for our veterans; slower or nonexistent service at the Social Security Administration for the elderly and disabled who rely on Social Security for their income; and the elimination of huge swaths of the Environmental Protection Agency (EPA) that help ensure we have clean air to breathe and clean water to drink."

"You have federal prisons absolutely overwhelmed by too many inmates and too few corrections officers, endangering public safety," she continued. "Consumer product safety has been eviscerated. There are also serious public health concerns involving substance abuse, childhood nutrition, and vaccinations."

She decried Hassett's comments as "ignorant" in light of his false claims about deficit reduction, but also "just demonstrably pretty cruel and disdainful" given the impact these job losses have on individuals, families, communities, and society as a whole.

"It's cruel," Simon said, "not only on the people who held those jobs—about a 100,000 of whom are military veterans—but the impact of the disappearance of those jobs also falls on children, the elderly, anybody who consumes agricultural products, breathes air, or relies on clean water."

"Everybody is hurt by what he's celebrating," she added. "I guess it's just par for the course from this administration, but it's still a disgusting thing to hear."

"It's a disgraceful law that forces working families to pay the price so the ultra-rich can profit," said Rep. Brendan Boyle.

The nonpartisan Congressional Budget Office on Monday said the Republican budget package that President Donald Trump signed into law last month will push up interest rates and add at least $4.1 trillion to the deficit over the next decade—largely due to the measure's massive tax cuts for the rich and large corporations.

According to the CBO, growing interest payments on the national debt will account for $718 billion of the estimated $4.1 trillion total deficit increase. Economist Josh Bivens has noted that it would cost the federal government $4.1 trillion to send a $12,000 check to every adult and child in the United States.

If temporary tax provisions of the highly regressive Trump-GOP law are made permanent, the estimated deficit impact would soar to nearly $5 trillion, CBO Director Phillip Swagel—a Republican—wrote in a letter to Sen. Jeff Merkley (D-Ore.) on Monday.

"Each and every analysis from the nonpartisan Congressional Budget Office continues to show the same result regardless of how you look at it: this bill explodes the debt by trillions of dollars to fund tax breaks for billionaires," Merkley, the top Democrat on the Senate Budget Committee, said in a statement. "Republicans can't spin the fact that this bill is bad policy that kicks more than 15 million people off of their health insurance, will force millions of kids to go hungry, and explodes the national debt by $5 trillion over the next 10 years—pushing the cost of this bill onto future generations to ensure billionaires can pay less in taxes."

"It is the height of hypocrisy coming from the party that claims to be fiscally responsible," Merkley added.

The deeply unpopular Republican law includes the largest cuts to Medicaid and federal nutrition assistance in U.S. history, alongside major handouts to profitable corporations—including oil and gas firms, pharmaceutical giants, and tech companies.

Zion Research Group estimates that 369 companies in the S&P 500 are set to reap a combined $148 billion in cash tax savings this year as a result of the Trump-GOP law, which extends tax breaks in Republicans' 2017 Tax Cuts and Jobs Act. Just four companies—Amazon, Meta, Alphabet, and Microsoft—are expected to rake in 38% of the $148 billion total.

The poorest 40% of Americans, meanwhile are set to see their taxes rise next year under the Trump-GOP bill, mostly due to Republican lawmakers' refusal to extend Affordable Care Act tax credits.

Wow, Amazon, Microsoft, Meta, and Google are getting 38% of the total cash savings from the part of Trump’s tax law going to corporations. That’s $15.7B to Amazon alone! https://t.co/l9AZth20RJ pic.twitter.com/XFVekRmrrp

— Matt Stoller (@matthewstoller) August 5, 2025

Rep. Brendan Boyle (D-Pa.), the ranking member of the House Budget Committee, said the new CBO analysis "yet again confirms Republicans' Big Ugly Law is as expensive as it is cruel."

"It explodes the deficit by over $4 trillion to pay for massive tax breaks for billionaires, while ripping healthcare and food assistance away from millions of Americans," said Boyle. "It's a disgraceful law that forces working families to pay the price so the ultra-rich can profit."

Scott Bessent's "3-3-3" agenda "requires brutal cuts to health and nutrition and higher costs for families at the grocery store," said analysts at the Center for American Progress.

At his confirmation hearing on Thursday, hedge fund manager and U.S. treasury secretary nominee Scott Bessent told the Senate Finance Committee that at the helm of the Treasury Department he would usher in an "economic golden age."

But a report by two policy analysts details how Bessent's signature "3-3-3" plan would only be achievable by gutting programs for some of the nation's most vulnerable households—extending the "golden age" only to wealthy people and corporations for whom the Trump administration plans to slash taxes.

At the Center for American Progress, senior director of economic policy Brendan Duke and senior director of federal budget policy Bobby Kogan completed "the accounting to determine what it would take to achieve" Bessent's 3-3-3 agenda, particularly his plan to cut the federal budget deficit down to 3% of the gross domestic product (GDP). The plan also calls for real GDP growth to reach 3% and the production of 3 million barrels of oil by 2028.

While reducing the budget deficit and simultaneously protecting programs American families rely on is a "laudable goal," wrote Duke and Kogan, Bessent has "explicitly stated that extending the expiring 2017 tax cuts is a priority, and he would likely rule out tax increases on the wealthy to pay for them"—suggesting that the Treasury nominee's 3-3-3 agenda would require new taxes on imported goods and "massive cuts to anti-poverty programs."

The Congressional Budget Office has projected that the budget deficit will represent 5.8% of the nation's GDP in 2028.

"The president-elect is stacking his cabinet with one goal in mind: more tax breaks for his billionaire boys club and major corporations."

With Bessent proposing an extension of the 2017 tax cuts—which are projected to grow the budget deficit by about $4 trillion over a decade—the elimination of Inflation Reduction Act energy investments, and a pause on nondefense discretionary spending increases, said Duke and Kogan, Bessent's plan would "actually increase the projected 2028 budget deficit from 5.8 to 6.0% of GDP, or $1 trillion above the 3% target.

Without any cuts to Medicare and Social Security—which Trump has said he would exempt from cuts—or defense spending, says the analysis, Bessent's deficit target would require both:

"The combination of policies that would deliver the deficit reduction proposed in Bessent's 3-3-3 economic plan would raise taxes on low- and middle-income families and gut healthcare, nutrition assistance, and veterans' programs while still cutting taxes for the wealthy," wrote Duke and Kogan. "Such a plan would hike families' costs both because broad-based tariffs would increase prices and because Americans would have to pay more for healthcare and food due to cuts to federal programs that help lower the cost of living."

With families across the U.S. facing "brutal cuts to health and nutrition" and higher prices at the grocery store under Bessent's plan, said Duke, the wealthiest households would still get "a net tax cut."

At The Washington Post, columnist Catherine Rampell wrote that "the magnitude of cuts required to make Bessent's arithmetic work is breathtaking."

"If you add up all the tax-cut promises Trump made during his campaign, the budget hole swells to almost $10 trillion," wrote Rampell. "To compensate, government programs would have to shrink by two-thirds. Alternatively, Trump could raise taxes on the middle class. Pick your poison."

On social media, government watchdog Accountable.US denounced Bessent's defense of Trump's tax cuts—under which "the top 1% saw benefits nearly three times larger than families in the bottom 60%"—and of the president-elect's proposed tariffs, which leading economists say would "reignite" inflation.

"Scott Bessent's nomination isn't about helping American families," said the group. "It's about lining the pockets of the ultra-wealthy and doubling down on policies that hurt the middle class."

Meanwhile, critics of Bessent on Thursday pointed to new reporting from Politico that Senate Democrats have accused the Treasury nominee of dodging $910,182 in Medicare taxes for income he made through his hedge fund from 2021-23. A memo circulated by Democrats stated that Bessent argued that as a "limited partner" in his fund, he was not liable for taxes on certain income.

Sen. Ron Wyden (D-Ore.) addressed the memo at Bessent's hearing, saying: "Like a number of Wall Street fund managers, Mr. Bessent makes use of a tricky legal maneuver to opt out of paying into Medicare."

"The billionaire hedge fund manager Trump handpicked to oversee a massive tax giveaway for the ultra-wealthy doesn't pay his own taxes," said Lindsay Owens, executive director of Groundwork Collaborative. "It's almost too on the nose. The president-elect is stacking his cabinet with one goal in mind: more tax breaks for his billionaire boys club and major corporations."

If you want to make social investments, it's important to recognize that vast amounts of capital held by the rich are just sitting around waiting to be put to good social use.

Back in 1933, the journalist-turned-lawyer Wesley Lloyd turned into a new member of Congress from Washington State. Two months into his first term, Lloyd rose to address his fellow lawmakers. They had all, he related, so far applied little more than “palliatives” to the continuing Great Depression.

“We have subsidized the farmer and charged the cost to labor,” Lloyd observed, “and we are attempting to subsidize labor and propose to let the farmer pay the bill.”

What Congress needed to do instead: “lay the ax of legislative enactment at the tap root” of what had gone wrong in America and “place a definite limitation on the acquisition and ownership of wealth.”

“A startlingly small number of our people,” Lloyd charged, had come to enjoy a “vastly major proportion of our national wealth.” His answer: a constitutional amendment giving Congress the power “to limit the wealth” of individual Americans to no more than $1 million, the equivalent of about $23 million today.

“I propose in the main,” said Lloyd, “to bring up the poor and bring down the rich into the class of the average man, where all may find real happiness and where we may know a widespread national prosperity.”

Over the next dozen years, under Franklin Roosevelt’s New Deal, the United States would make historically unprecedented progress toward that greater equality Lloyd so deeply desired. By 1945, America’s richest faced a 94 percent tax rate on income over $200,000. Lloyd, sadly, wouldn’t be around to see that progress. He died early in 1936, midway through his second term.

But Lloyd’s tax-the-rich spirit lives on, especially today in his home Washington State. Earlier this year, 19 of the state’s senators and 43 state reps introduced legislation that would fix a first-ever 1 percent annual tax on stocks, bonds, and other forms of “intangible personal property” worth over $250 million. The Evergreen State currently hosts over 700 grand fortunes that top this quarter-billion mark.

The holders of these massive accumulations have — for now at least — dodged this proposed annual 1 percent tax on their “financial intangible property.” The proposal failed to get through the 2023 state legislative session. But that failure hasn’t left Washington’s deepest pockets feeling like celebrating. The reason? They’ve just become subject to another new tax, a measure that Seattle Times columnist Danny Westneat is describing as the state’s first-ever “wealth-related levy.”

This particular levy, a 7-percent excise tax on asset-sale profits over $250,000, actually became law two years ago, then got shelved when a county court ruled the new tax unconstitutional. This past March, a state Supreme Court ruling reversed that county ruling, and wealthy Washingtonians are now paying up on their new taxes due — at much higher levels than the state’s legislative number-crunchers had anticipated!

Those analysts had expected Washington’s new 7-percent capital gains tax to raise $440 million from the state’s richest. The new tax has instead so far raised $849 million, almost double the take originally anticipated.

Washington’s wealthy still, to be sure, have plenty to be thankful for at tax time. Washington, for instance, remains without an income tax. But no state, we need to remember, has yet come up with what analysts at the Washington, D.C.-based Center for Budget and Policy Priorities would see as a perfect package of tax reforms that prioritize “equity and fairness.”

The Center is now hoping to nudge state lawmakers nationwide further in that direction with a new online tool for developing “State Revenue Options for Advancing Equity and Prosperity.” State policymakers, the Center notes, don’t always understand “how much revenue different policies might raise, whether a tax will fall more on families with low incomes or people at the top.” The new Center tool aims to build that understanding.

Understanding, of course, only takes lawmakers so far. They still have to overcome the opposition of the richest among us to paying anything close to their fair tax share. Lawmakers can certainly do that overcoming — if enough of us push them. And if we do enough of that pushing, maybe our lawmakers will start sounding like Wesley Lloyd back when he proposed to limit the personal wealth of our super richest.

“I do not seek to destroy wealth or industry,” Lloyd told his fellow members of Congress, “but I do propose to place the burden of public expense and national development upon the shoulders of those best able to bear that burden and those who have profited most. I would have the strong help the weak rather than have the weak forever carrying the strong.”

This isn't a crisis. This is a plot.The corporate media refuses to tell the American people what this is: a cynical political and media strategy devised by Republicans in the 1970s, fine-tuned in the 1980s, and since then rolled out every time a Democrat is in the White House.

"The only thing wrong with the U.S. economy is the failure of the Republican Party to play Santa Claus." —Jude Wanniski, March 6, 1976

As the Fitch credit rating service puts the United States on “watch” for a possible downgrade and Democrats dither about the 14th Amendment, Republicans just declared the House of Representatives in a break because, from their point of view, there really is no crisis.

In fact, from the GOP’s perspective, it’s all going according to plan.

As Teagan Goddard’s Political Wire noted yesterday:

“RNC Chair Ronna McDaniel told Fox News that the U.S. potentially defaulting on its debt ‘bodes very well for the Republican field.’”

It’s no accident or coincidence that the threat of a failure to pay the nation’s bills never once happened during the presidencies of Reagan, Bush, Bush, or Trump. Or that it did happen every single time during the presidencies of Clinton, Obama…and, now, Biden.

You could even call it a conspiracy: there’s an amazing backstory — with a unique name — here. And it all started with a guy named Jude Wanniski, who literally transformed American politics with a plan that the American mainstream media, astonishingly, continues to ignore.

Here’s how it works, laid it out in simple summary:

To set up its foundation, Wanniski’s "Two Santas” strategy dictates, when Republicans control the White House they must spend money like a drunken Santa and cut taxes on the rich, all to intentionally run up the US debt as far and as fast as possible.

They started this during the Reagan presidency and tripled down on it during the presidencies of Bush and Trump with massive tax cuts for billionaires and increases in spending across-the-board.

Those massive tax cuts and that uncontrolled spending during Republican presidencies produced three results:

Then comes part two of the one-two punch: when a Democrat is in the White House, Republicans must scream about the national debt as loudly and frantically as possible, freaking out about how “our children will have to pay for it!” and “we have to cut spending to solve the crisis!”

The “debt crisis,” that is, that they themselves created with their massive tax cuts and wild spending.

Never again would Republicans worry about the debt or deficit when they were in office; but they knew well how to scream hysterically about it and hook in the economically naïve media as soon as Democrats again took power.

Do whatever it takes, the strategy goes: use the 1917 Liberty Bond debt ceiling to shut down the government, crash the stock market, and damage US credibility around the world if necessary.

This will force the Democratic president in the White House to cut his own social safety net programs and even the crown jewel of the New Deal, Social Security, thus shooting their welfare-of-the-American-people Santa Claus right in the face.

And, sure enough, here we are again with a Democrat in the White House.

Which is why, following Wanniski’s script, Republicans are again squealing about the national debt and saying they will refuse to raise the debt ceiling, possibly crashing the US economy.

And, once again, the media is preparing to cover it as a “Debt Ceiling Crisis!” rather than what it really is: a cynical political and media strategy devised by Republicans in the 1970s, fine-tuned in the 1980s, and since then rolled out every time a Democrat is in the White House.

Politically, it’s a brilliant strategy that was hatched by a fellow most people have never heard of: Jude Wanniski.

Republican strategist Wanniski first proposed his Two Santa Clauses strategy in The Wall Street Journal in 1974, after Richard Nixon resigned in disgrace and the future of the Republican Party was so dim that books and articles were widely suggesting the GOP was about to go the way of the Whigs.

There was genuine despair across the GOP, particularly when Jerry Ford couldn’t even beat an unknown peanut farmer from rural Georgia for the presidency.

Wanniski argued back then that Republicans weren’t losing so many elections just because of Nixon’s corruption, but mostly because the Democrats had been viewed since the New Deal of the 1930s as the “Santa Claus party.”

On the other hand, the GOP, he said, was widely seen as the “party of Scrooge” because ever since the 1930s they’d publicly opposed everything from Social Security and Medicare to unemployment insurance and food stamps.

The Democrats, he noted, had gotten to play Santa Claus for decades when they passed out Social Security and unemployment checks — both programs of FDR’s Democratic New Deal — as well as their “big government” projects like roads, bridges, schools, and highways that gave a healthy union paycheck to workers and made our country shine.

Even worse, Democrats kept raising taxes on businesses and rich people to pay for all that “free stuff” — and Democrats’ 91% top tax rates on the morbidly rich didn’t have any negative effect at all on working people (wages were steadily going up until the Reagan Revolution, in fact).

It all added, Wanniski theorized, to the public perception that the Democrats were the true party of Santa Claus, using taxes on the morbidly rich to fund programs for the poor and the working class.

Americans loved the Democrats back then. And every time Republicans railed against these programs, they lost elections.

Therefore, Wanniski concluded, the GOP had to become a Santa Claus party, too.

But because Republicans hated the idea of helping working people, they had to come up with a new way to convince average voters that the GOP, too, had the Santa spirit. But what?

“Tax cuts!” said Wanniski.

To make this work, the Republicans would first have to turn the classical world of economics — which had operated on a simple demand-driven equation for seven thousand years — on its head. (Everybody then understood that demand — “working-class wages” — drove economies because working people spent most of the money they earned in the marketplace, producing “demand” for factory-output goods and services.)

To lay the ground for Two Santa Clauses, in 1974 Wanniski invented a new phrase — “Supply-Side Economics” — and claimed the reason economies grew and became robust wasn’t because people had good union jobs and thus enough money to buy things (“demand”) but, instead, because business made things (“supply”) available for sale, thus tantalizing people to part with their money.

The more products (supply) there were in the stores, he said, the faster the economy would grow. And the more money we gave rich people and their corporations (via tax cuts) the more stuff (supply) they’d generously produce for us to think about buying.

At a glance, this 1981 move by the Reagan Republicans to cut taxes while increasing spending seems irrational, cynical, and counterproductive. It certainly defies classic understandings of economics. But when you consider Jude Wanniski’s playbook, it makes complete sense.

To help, Arthur Laffer took that equation a step further with the famous “Laffer Curve” napkin scribble he shared with Dick Cheney and Don Rumsfeld over lunch. Not only was supply-side a rational concept, Laffer suggested, but as taxes went down, revenue to the government would magically go up!

Neither concept made any sense — and time and our $32 trillion national debt have proven both to be colossal idiocies — but if Americans would buy into it all, they offered the Republican Party a way out of the wilderness.

Ronald Reagan was the first national Republican politician to fully embrace the Two Santa Clauses strategy.

He told the American people straight-out that if he could cut taxes on rich people and businesses, those “job creators” (then a newly-invented Republican phrase) would use their extra money to “build new factories” so all that new stuff “supplying” the economy would produce faster economic growth.

George HW Bush — like most Republicans in 1980 who hadn’t read Wanniski’s piece in The Wall Street Journal — was initially horrified. Ronald Reagan was proposing “Voodoo Economics,” said Bush in the primary campaign, and Wanniski's supply-side and Laffer’s tax-cut theories would throw the nation into debt while producing nothing to benefit average Americans.

But Wanniski had done his homework, selling “Voodoo” supply-side economics to the wealthy elders and influencers of the Republican Party.

Democrats, Wanniski told the GOP, had been “Santa Clauses” since 1933 by giving people things. From union jobs to food stamps, new schools to Social Security, the American people loved the “toys” and “free stuff” the Democratic Santas brought every year, as well as the growing economy the increasing union wages and social programs produced in middle class hands.

But Republicans could stimulate the economy by throwing trillions at defense contractors, oil companies, and other fat-cat donor industries, Jude’s theory went: spending could actually increase without negative repercussions because that money would trickle down to workers from the billionaires and corporate CEOs buying new yachts and building new mansions.

Plus, Republicans could be double Santa Clauses by cutting people’s taxes!

For working people, the tax cuts would only be a small token — a few hundred dollars a year at the most — but Republicans would heavily market them to the media and in political advertising. And the tax cuts for the rich, which weren’t to be discussed in public, would amount to trillions of dollars, part of which they knew would be recycled back to the GOP as campaign contributions from the rich beneficiaries of those tax cuts.

Every time a Democrat was in the White House, they’d be forced into the role of Santa-killers if they acted responsibly by raising taxes; or, even better, they’d be machine-gunning Santa by cutting spending on their own social programs.

There was no way, Wanniski said, that the Democrats could ever win again.

Every time a Democrat was in the White House, they’d be forced into the role of Santa-killers if they acted responsibly by raising taxes; or, even better, they’d be machine-gunning Santa by cutting spending on their own social programs.

Either one would lose them elections, and if Republicans executed the strategy right, they could force Democrats to do both!

Reagan took the federal budget deficit from under a trillion dollars when he was elected in 1980 to almost three trillion by 1988, and back then a dollar could buy far more than it buys today.

Republicans embraced Wanniski’s theory with such gusto that Presidents Reagan and George HW Bush ran up more debt in twelve years than every president in history up until that time, from George Washington to Jimmy Carter, combined.

Surely this would both “starve the beast” of the American government and force the Democrats to make the politically suicidal move of becoming deficit hawks.

And, with Newt Gingrich using the formerly obscure weapon of the “debt ceiling” — a vestige of the 1917 Liberty Bond Act that nobody had paid attention to in living memory — that’s just how it turned out.

Bill Clinton, the first Democrat they blindsided with Two Santas and the newly-discovered “debt ceiling,” had run on an FDR-like platform of a “New Covenant” with the American people that would strengthen the institutions of the New Deal, re-empower labor, and institute a national single-payer health care system.

A few weeks before his inauguration, however, Wanniski-insiders Alan Greenspan, Larry Sommers, and Goldman Sachs co-chairman Robert Rubin famously sat Clinton down and told him the facts of life: Reagan and Bush had run up such a huge deficit that he was going to have to both raise taxes and cut the size of government programs for the working class and poor.

Clinton buckled under the threat of the debt ceiling, raised taxes, balanced the budget, and cut numerous social programs. He declared an “end to welfare as we know it” and, in his second inaugural address, an “end to the era of big government.”

Clinton shot Santa Claus, and the result was an explosion of Republican wins across the country as GOP politicians campaigned on a “Republican Santa” platform of supply-side tax cuts and pork-rich spending increases.

Democrats had controlled the House of Representatives in almost every single year since the Republican Great Depression of the 1930s, but with Newt Gingrich rigorously enforcing Wanniski’s Two Santa Clauses strategy with brutal “debt ceiling” threats, they finally took it over in the middle of Clinton’s presidency.

State after state turned red, and the Republican Party rose to take over, in less than a decade, every single lever of power in the federal government, from the Supreme Court to Congress to the White House.

Newt had done his job in the House of Representatives. Looking at the wreckage of the Democratic Party all around Clinton in 1999, Wanniski wrote a gloating memo that said, in part:

“We of course should be indebted to Art Laffer for all time for his Curve... But as the primary political theoretician of the supply-side camp, I began arguing for the ‘Two Santa Claus Theory’ in 1974. If the Democrats are going to play Santa Claus by promoting more spending, the Republicans can never beat them by promoting less spending. They have to promise tax cuts...”

Ed Crane, then-president of the Koch-funded Libertarian CATO Institute, noted in a memo that year:

“When Jack Kemp, Newt Gingrich, Vin Weber, Connie Mack and the rest discovered Jude Wanniski and Art Laffer, they thought they’d died and gone to heaven. In supply-side economics they found a philosophy that gave them a free pass out of the debate over the proper role of government. ... That’s why you rarely, if ever, heard Kemp or Gingrich call for spending cuts, much less the elimination of programs and departments.”

Two Santa Clauses had fully seized the GOP mainstream.

Never again would Republicans worry about the debt or deficit when they were in office; but they knew well how to scream hysterically about it and hook in the economically naïve media as soon as Democrats again took power.

When Jude Wanniski died, George Gilder celebrated the Reagan/Bush adoption of his Two Santas “Voodoo Economics” scheme — then still considered irrational by mainstream economists — in a Wall Street Journal eulogy:

“Unbound by zero-sum economics, Jude forged the golden gift of a profound and passionate argument that the establishments of the mold must finally give way to the powers of the mind. ... He audaciously defied all the Buffetteers of the trade gap, the moldy figs of the Phillips Curve, the chic traders in money and principle, even the stultifying pillows of the Nobel Prize.”

Republicans got what they wanted from Wanniski’s work. Using the “debt ceiling” argument — essentially Two Santas in drag — Republicans have forced two Democratic presidents, and are about to force a third, to gut-shoot the Democratic Santa established by FDR.

They held power for forty years, transferred over $50 trillion from working class families into the money bins of the top one percent, and cut organized labor's representation in the workplace from around a third of workers when Reagan came into office to around 6 percent of the non-governmental workforce today.

Think back to Ronald Reagan, who more than tripled the US debt from a mere $800 billion to $2.6 trillion in his 8 years. That spending produced a massive stimulus to the economy, and the biggest non-wartime increase in America’s national debt in all of our history.

There was nary a peep from Republicans about that 218% increase in our debt; they were just fine with it and to this day claim Reagan presided over a “great” economy.

When five rightwingers on the Supreme Court gave the White House to George W. Bush in 2000, he reverted to Wanniski’s “Two Santa” strategy and again nearly doubled the national debt, adding several trillion in borrowed money to pay for his tax cut for billionaires, and tossing in two unfunded wars for good measure, which also added at least (long term) another $8 trillion.

Hopefully this time Democratic politicians and our media will, finally, call the GOP out on Wanniski’s and Reagan’s Two Santa Clauses scam.

There was not a peep about that debt from any high-profile in-the-know Republicans; in fact, Dick Cheney — who knew Wanniski personally — famously said, amplifying Wanniski’s strategy:

“Reagan proved deficits don’t matter. We won the midterms. This is our due.”

Bush and Cheney’s tax cuts for the rich raised the debt by 86% to over $10 trillion (and additional trillions in war debt that wasn’t be put on the books until Obama entered office, so it looked like it was his).

Then came Democratic President Barack Obama, and suddenly the GOP was hysterical about the debt again.

So much so that they convinced a sitting Democratic president to propose a cut to Social Security (the “chained CPI”). Obama nearly shot the Democrats’ biggest Santa Claus, just like Wanniski predicted, until outrage from the Democratic base stopped him.

Next, Donald Trump raised our national debt by over $7 trillion, and the GOP raised the debt ceiling without a peep every year for the first three years of his administration, and then suspended it altogether for 2020 (so, if Biden won, he’d have to justify raising the debt ceiling for 2 years’ worth of deficits, making it even more politically painful).

And now Republicans are using the debt ceiling debate to drop their Two Santas bomb right onto President Joe Biden’s head. After all, it worked against Clinton and Obama and the media never caught on. Why wouldn’t they use it again?

And if the GOP’s debt-ceiling default crashes the economy, all the better: Republicans can just blame Biden: it’ll increase the chances of Republican victories in 2024!

Americans deserve to know how we’ve been manipulated, and by whom.

Americans deserve to know how we’ve been manipulated, and by whom. Sadly, although I and others (it’s even detailed on Wikipedia!) have been calling out Wanniski’s strategy for decades, none of the national media have ever seriously examined this 40+ year GOP strategy.

Hopefully this time Democratic politicians and our media will, finally, call the GOP out on Wanniski’s and Reagan’s Two Santa Clauses scam. And put an end to it once and for all with the constitutional remedies of the 14th Amendment and the “take care” clause of the Constitution’s Article II.

If not, get ready for Biden to cave in just like Clinton and Obama did, demoralizing progressives and cutting Democratic turnout in 2024.

Or, even worse, if McCarthy can’t hold his caucus together, prepare for an all-out economic disaster — a second Republican Great Depression — followed by an openly fascistic second Trump presidency or something very much like it.

Spread the word.

And under normal and rational circumstances, the Court would do what it did in 1935 and order the bills paid, citing the 14th Amendment's section on debt payment. However, these are not normal and rational times and this is not a normal and rational court.

Kevin McCarthy is playing with fire, and he’s on very shaky constitutional grounds.

He believes that he can hold hostage payments for goods bought and services already provided to the federal government — debts of the United States — in exchange for forcing the Biden administration to go along with draconian cuts to veterans benefits, food stamps (SNAP benefits), Medicaid, the Inflation Reduction Act (particularly its subsidies for green energy), and the permanent establishment of Trump’s massive tax cuts for billionaires.

Republicans started using the so-called “debt ceiling” — based on a law passed back in 1917 — as a cudgel to beat up Democratic presidents in 1995 during the Clinton administration. It was one of Newt’s “bright ideas.”

Clinton and Obama went along with the GOP, but now their demands have become so extreme that President Biden is threatening a veto (if the bill even gets through the Senate, which it probably won’t).

They’re doing this based on the 1917 Second Liberty Bond Act which established a ceiling for US government debt, a ceiling that’s been breached through amendment over 90 times in the past century.

The act gave the government the authority to issue Liberty Bonds to the public to help finance World War I, but put a cap on how much debt could be incurred through that issuance and other government functions. Today we call that the “debt ceiling.”

Just from 1962 to 2011 it was raised 74 times, including 18 times under Reagan, 8 during Clinton, 7 during Bush, 5 times during Obama’s presidency, and 4 times during Trump’s four years in office.

In the years since Gingrich, when Republicans are in the White House the debt ceiling is routinely raised. When Democrats are in the White House and Republicans control one or more houses of Congress, they hold it hostage — really, holding the full faith and credit of the United States hostage — in exchange for cuts in social programs and lower taxes for billionaires.

The last time House Republicans seriously threatened the full faith and credit of the United States this way was during Obama’s presidency in 2011 (they almost never do this when a Republican is in the White House, per Jude Wanniski’s “Two Santas” theory of politics).

That single 2011 stunt — just having House Republicans walk us up to the edge of default, resulting in a downgrade of our nation’s credit rating — cost working people trillions and caused widespread and long-lasting pain.

As the Treasury Department noted in 2013, looking back on that 2011 experience when Republicans held out until the last minute:

“In 2011, U.S. debt was downgraded, the stock market fell, measures of volatility jumped, and credit risk spreads widened noticeably; these financial market effects persisted for months. …

“The S&P 500 index of equity prices fell about 17 percent in the period surrounding the 2011 debt limit debate and did not recover to its average over the first half of the year until into 2012.

“Between the second and third quarter of 2011, household wealth fell by $2.4 trillion…”

The US government has never, in our country’s entire history, defaulted on its debt. Neither, in recent history, have most other advanced democracies. Debt default is very much a Third World kind of thing.

That’s why the US dollar and US government treasuries are at the core of the international financial system: we have always been considered the most reliable debtor, with the most stable currency and structurally sound economic system, in the world.

If the GOP takes us into default — even for a matter of hours — the consequences will be dire.

CBS News reports that Moody’s Analytics’ Chief Economist Mark Zandi says it would wipe out as many as 6 million jobs and destroy $15 trillion in household wealth. Unemployment would rapidly spike, he notes, to at least 9 percent, and the stock market would fall by a third.

We’ve known how bad it could become for a while. The Treasury Department, back in 2013, noted that:

“In the event that a debt limit impasse were to lead to a default, it could have a catastrophic effect on not just financial markets but also on job creation, consumer spending and economic growth—with many private-sector analysts believing that it would lead to events of the magnitude of late 2008 or worse, and the result then was a recession more severe than any seen since the Great Depression.

“Considering the experience of countries around that world that have defaulted on their debt, not only might the economic consequences of default be profound, those consequences, including high interest rates, reduced investment, higher debt payments, and slow economic growth, could last for more than a generation.”

Most Americans are not at all enthusiastic about Republicans in Congress causing economic damage that “could last for more than a generation,” although McCarthy yesterday seemed almost giddy waving about that threat.

But there may be a way out.

The Second Liberty Bond Act and the subsequent acts that followed or amended it have only been narrowly tested for constitutionality before the Supreme Court. And it failed that test. In the opinion of many constitutional scholars, it’s patently unconstitutional and unenforceable.

The 14th Amendment to our Consitution, written and ratified after the Civil War, has a section that deals with the federal government paying its debts. It’s there, in part, because the Civil War had threatened the confidence of both the nation and the world around America’s ability to pay its bills.

Section 4 of the 14th Amendment says:

“The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned.”

It was first tested in a dispute about payment of government debt, a $10,000 Liberty Bond that the holder, Mr. Perry, wanted redeemed with an additional $7,000 to cover changes in the value of gold.

This led to the 1935 Supreme Court ruling in Perry v United States, explicitly stating that the federal government must pay its debts as incurred.

The syllabus of the case states:

“11. Section 4 of the Fourteenth Amendment, declaring that, ‘The validity of the public debt of the United States, authorized by law, ...shall not be questioned,’ is confirmatory of a fundamental principle, applying as well to bonds issued after, as to those issued before, the adoption of the Amendment; and the expression ‘validity of the public debt’ embraces whatever concerns the integrity of the public obligations.

“The Joint Resolution of June 5, 1933, is a direct violation of §4 of the Fourteenth Amendment, expressly limiting the delegated powers of Congress, and making the public debt of the United States inviolable at the hands of Congress.”

The body of the decision itself goes even deeper into asserting that our government must pay its debts:

“When the United States, with constitutional authority, makes contracts, it has rights and incurs responsibilities similar to those of individuals who are parties to such instruments. …

“In Lynch v. United States, 292 U. S.571, 580, with respect to an attempted abrogation by the Act of March 20, 1933 (48 Stat. 8, 11) of certain outstanding war risk insurance policies, which were contracts of the United States, the Court quoted with approval the statement in the Sinking-Fund Cases, supra, and said:

“’Punctilious fulfillment of contractual obligations is essential to the maintenance of the credit of public as well as private debtors. No doubt there was in March, 1933, great need of economy. In the administration of all government business economy had become urgent because of lessened revenues and the heavy obligations to be issued in the hope of relieving widespread distress.

“‘Congress was free to reduce gratuities deemed excessive. But Congress was without power to reduce expenditures by abrogating contractual obligations of the United States. To abrogate contracts, in the attempt to lessen government expenditure, would be not the practice of economy, but an act of repudiation.’” (emphasis mine)

The simple fact is that the Trump and Biden administrations have made obligations to pay for goods and services ranging from military hardware to Social Security, and McCarthy and his buddies in the Republican Party are trying to force a default on those debts.

Such a default, according to Treasury Secretary Janet Yellen and numerous finance experts, would be disastrous, perhaps even shaking the worldwide economy. America has never defaulted on her debts, and such a default could take decades to recover from.

It could throw America and the world into a depression as bad or worse than the Republican Great Depression of the 1930s.

President Biden is demanding that Congress pass a “clean” debt ceiling increase “without conditions.” It’s extremely unlikely McCarthy — weak as he is, with multiple members of the Sedition (“Freedom”) Caucus actually arguing that default would be a good thing because it would teach Democrats a lesson — will be able to get such a clean bill through the House.

As Tennessee’s Congressman Tim Burchett said:

“We just tell the world we’ve reached a limit. The consequences, of course, are shutting the government down.”

So far, because we’ve already hit the debt ceiling, Treasury Secretary Yellen has been “moving money around” to pay the most urgent bills, but the end of that road is just weeks away. Without congressional action, the next step would be default.

But what if the president were to call a press conference and say:

“The Constitution requires America to pay her bills. I fully intend to do that.”

If President Biden were to call McCarthy’s bluff and simply restart fully paying America’s bills, ignoring the Liberty Bond Act and the debt ceiling, Republicans will almost certainly sue him before the Supreme Court, which has original jurisdiction in disputes between the Executive and Legislative branches.

And under normal and rational circumstances, the Court would do what it did in 1935 and order the bills paid, citing the 14th Amendment’s fourth section as the basis for the decision.

These are not, however, normal and rational times, and this is not a normal and rational court. Clarence Thomas and Brett “Beerbong” Kavanaugh have both publicly declared a desire for revenge against Democrats, and Alito and Gorsuch are both visibly pissed off about their integrity being questioned.

Still, I believe it’s unlikely the Court would side with Congressional Republicans and force America into default (a similar lawsuit was tossed out in 2016, but for lack of standing).

This has the potential to get wild. Get some popcorn, but also buckle up tight…

"Once again," said Congressional Progressive Caucus Chair Pramila Jayapal, Republicans are "putting politics over poor and working people."

Progressive U.S. lawmakers on Monday took House Republicans to task after the Congressional Budget Office said the erstwhile deficit hawks' first bill before the 118th Congress—a measure critics say is meant to "protect wealthy and corporate tax cheats"—will swell the federal deficit by more than $100 billion.

"They all run on reducing the deficit and now the House GOP's first... bill will increase the deficit by $114 billion," tweeted Rep. Ilhan Omar (D-Minn.). "Make it make sense."

Increasing the federal deficit can help people and the economy. Republicans have been criticized for hypocritically pushing cuts to social safety net programs in the name of fiscal responsibility while being willing to raise the deficit to help corporations and the rich.

The nonpartisan Congressional Budget Office (CBO) estimated that the euphemistically named Family and Small Business Taxpayer Protection Act—which faces a vote as soon as Monday evening—would "decrease outlays by $71 billion and decrease receipts by $186 billion over the 2023-2032 period."

That's because the legislation would rescind $72 billion of $80 billion worth of new Internal Revenue Service (IRS) funding authorized under the Inflation Reduction Act (IRA) passed by the Demorcat-controlled 117th Congress and signed into law last year by President Joe Biden.

In a December 30 letter to colleagues, House Majority Leader Steve Scalise (R-LA) said the proposed bill "rescinds tens of billions of dollars allocated to the IRS for 87,000 new IRS agents" under the IRA, a GOP talking point that has been widely debunked.

"Today, Republicans in Congress demonstrated their commitment to 'fiscal responsibility,'" Sen. Elizabeth Warren (D-Mass.) sardonically tweeted. "The first bill advanced by the GOP adds $114 billion to the deficit—by allowing the super-wealthy to cheat their taxes while everyone else pays. Corporate lobbyists are popping champagne."

Congressional Progressive Caucus Chair Pramila Jayapal (D-Wash.) lamented that the "first order of business in the GOP House of Representatives" will be to "vote to increase the deficit $114 BILLION by letting tax cheats dodge paying what they owe."

"Once again," she added, "they're putting politics over poor and working people."

Advocacy groups also questioned GOP lawmakers' motives for introducing the bill, with Americans for Tax Fairness tweeting that "House Republicans are using their new majority to try and repeal IRS funding that will make rich and corporate tax cheats pay what they owe."

"The GOP wants to let their rich friends keep cheating the rest of us," the group added.