SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

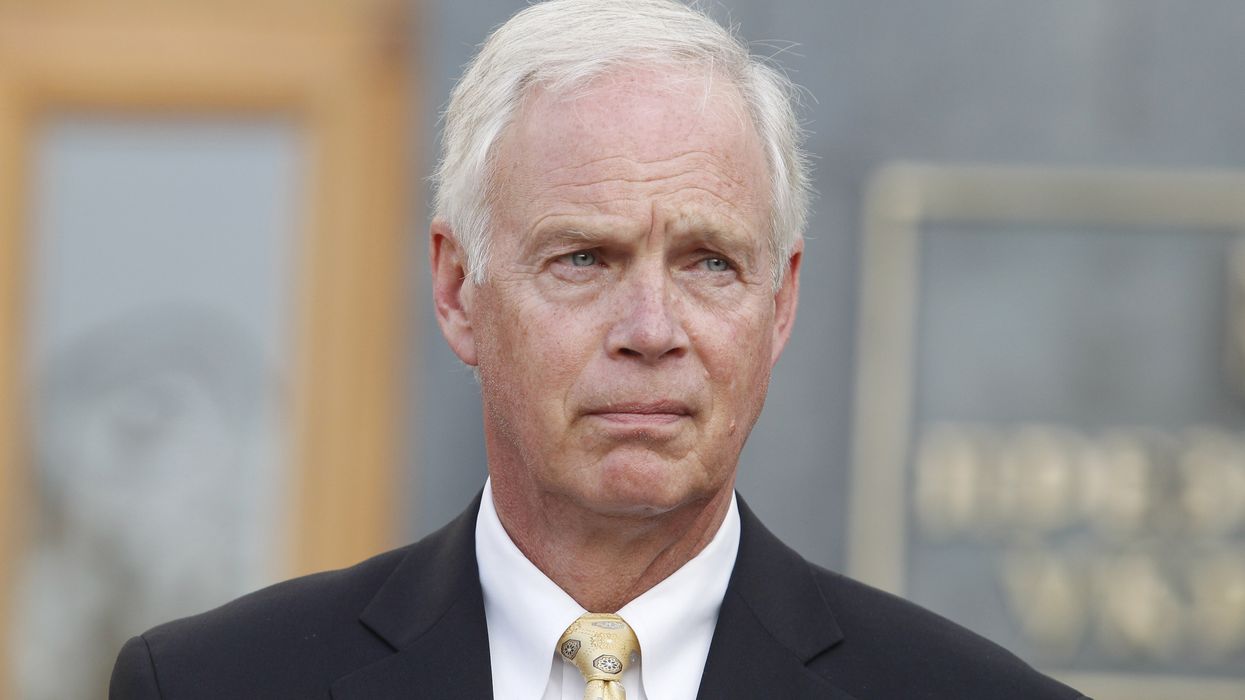

"Americans will pay a steep price if Republicans move forward with this disastrous agenda," said Sen. Ron Wyden.

The House Republican Study Committee on Tuesday released a blueprint for a new budget reconciliation package with the purported goal of making "life more affordable for working families."

However, according to an analysis by Washington Post economic policy reporter Jacob Bogage, two of the three most expensive items in the GOP budget blueprint would be the elimination of the federal estate tax, which would provide a massive windfall to the richest US households, and indexing capital gains to inflation, which even the conservative American Enterprise Institute contends "would further distort taxpayer decisions and increase the ability to shelter income from taxation."

Other items in the GOP blueprint include refilling the Strategic Petroleum Reserve with oil seized from Venezuela, blocking federal funds for abortion providers, and a new "excise tax on colleges that allow trans women in sports."

Sen. Ron Wyden (D-Ore.), ranking member of the Senate Finance Committee, wasted no time ripping the proposal from the largest right-wing House caucus to pieces.

"After passing the largest health care cut in American history, Republicans are doubling down on a failed agenda that benefits billionaires and giant corporations while ripping away food, healthcare and other basic necessities,” Wyden said. “This legislation will eliminate protections for Americans with preexisting conditions, place more red tape between families and their healthcare, and seize ideological trophies instead of focusing on making life more affordable. Americans will pay a steep price if Republicans move forward with this disastrous agenda.”

Richard Phillips, pensions and tax policy director for Sen. Bernie Sanders (I-Vt.), marveled at the GOP loading up a bill supposedly focused on working families with massive giveaways to the wealthiest Americans.

"As part of it's new affordability agenda for the American people the Republican Study Committee reveals its plan to give the wealthiest 0.2% of estates a $281 billion tax break?" he wrote in a post on X.

Chuck Marr, vice president of federal tax policy at the Center on Budget and Policy Priorities, similarly called the GOP blueprint "tone deaf."

"Nothing says attack the affordability crisis working-class people face than Rs calling for eliminating the estate tax for the wealthiest heirs in the country—just months after giving them a $30 million tax free exemption," he wrote.

The GOP's second attempt at a budget reconciliation package comes months after it passed the One Big Beautiful Bill Act, a reconciliation package that gave more tax breaks to the rich, but cut Medicaid spending by nearly $1 trillion over the next decade, while also slashing spending on the Supplemental Nutrition Assistance Program by nearly $200 billion over the same period.

The United States has no nobility, according to our Constitution. But our tax code does protect the very rich.

Pre-revolutionary French aristocrats—the “Second Estate”—didn’t pay taxes. Amazingly, America too has a second estate, billionaires who pay virtually no taxes. In her very outstanding recent book, law professor Ray D. Madoff shows how they get away with this.

The United States has no nobility, according to our Constitution. But our tax code does protect the very rich.

Federal taxes on income and estates—intended to fund government and prevent development of a hereditary financial aristocracy—were enacted early in the 20th century and originally worked well.

But since about 1980, the estate tax—infested with loopholes—has been nearly abolished for practical purposes and now produces trivial income.

Madoff wants to get rid of the ability of ultra-rich people—billionaires—to avoid having any taxable income in the first place.

Madoff suggests that the estate tax should be completely eliminated because its existence deceives the public about what is really going on. People falsely think that billionaires who pay no federal income tax will at least pay the estate tax when they die. In fact, they are paying neither kind of tax.

Billionaires avoid the income tax by arranging to have no taxable income.

Before 1982 ultra-rich people could not avoid paying income tax. Their income consisted of dividends and capital gains harvested by selling shares of stock, the price of which had increased. Dividends and capital gains are taxable income.

But in 1982 federal regulators weakened a rule prohibiting corporations from buying back their own stock. Since then, many corporations have used profits to buy back stock shares instead of issuing dividends. With fewer shares of stock outstanding and the value of the corporation increasing, the value of each share of stock began increasing dramatically.

What used to be taxable dividends turned into large capital gains benefiting the stock owners, including very rich ones. If shareholders need cash and sell appreciated stock, of course they would owe income taxes on the capital gains (selling price of the stock minus how much the shares cost them). But capital gains are taxed at a much lower rate than normal income like salaries, bank interest, and returns on bonds.

As Madoff points out, however, billionaires need not sell any stock to get cash to live on. Instead, they can borrow the money, using their stock as collateral. Borrowed money is not taxable income, so they owe no tax while living extravagantly.

And when they die, the stock they bequest to their heirs gets a stepped up “basis,” so if their heirs sell the stock they will owe no taxes because the stepped up basis leaves no taxable capital gains.

And inherited money is not considered taxable income. Someone who earns $50,000 pays significant income (and payroll) taxes on it, while someone who inherits $1 billion pays no income or payroll tax on it.

Madoff rightly objects to this situation, but she is not arguing that we should “soak the rich” with higher income tax rates at the top. She points out that there are two kinds of “rich” people. One is the working rich, skilled professionals earning high salaries and, usually, already paying very high taxes. A high percentage of all income tax receipts come from these people.

Increasing the high tax rates these “rich” people are already paying would produce insignificant extra revenue for the government.

Instead, Madoff wants to get rid of the ability of ultra-rich people—billionaires—to avoid having any taxable income in the first place. She wouldn’t tax them while they are alive, but would tax whoever inherits from them.

Rather than trying to fix the estate tax, Madoff would abolish it, eliminate the stepped up basis for inherited stock, and make inherited money and other gifts received taxable income for the recipients.

Assuming an exemption for small gifts (to allow birthday presents and the like), this could be a reasonable reform. It would bring in very large amounts of taxes while reducing today’s extreme economic inequality.

For further details, see Ray D. Madoff, The Second Estate: How The Tax Code Made An American Aristocracy. This is one of the two best books I have read since retiring in 2000.

Funny how these same apologists for our richest don’t have much sympathy for ordinary Americans who lack the “wherewithal” to pay for medical care, adequate housing, and other necessities.

The most gaping loophole in our tax law? The tax-free compounding of gains on investments.

This classic loophole enables the two most lucrative inequality-driving income tax avoidance strategies. The first, buy-borrow-die, allows wealthy Americans to avoid income tax entirely on even billions in investment gains.

These wealthy need only hold on to their appreciated assets until death. What if they need cash before then? They merely borrow against the appreciated assets, typically at very low interest rates.

Are rich Americans, including billionaires, truly unable to pay tax on their investment gains before they sell the assets yielding those gains? Wanna buy a bridge?

The second avoidance strategy, buy-hold for decades-sell, lets wealthy investors pay a super low effective annual tax rate on investments that appreciate at high rates over long periods of time. These investors typically experience decades of compounding gains without taxation.

The effective tax rates involved in this second strategy won’t reach buy-borrow-die’s zero tax, but may in some cases get as low as a 4% effective annual rate. A 4% effective annual tax rate would have an investment with a pre-tax growth rate of 20% per year enjoying an after-tax growth rate of 19.2% per year.

Congressional apologists for the ultra-rich on both sides of the aisle regularly claim that their wealthy patrons should be entitled to endless tax-free compounding of investment gains. Without this tax-free compounding, the argument goes, our richest wouldn’t have the “wherewithal to pay” tax on their investment gains before their assets get sold. U.S. Sen. Ron Johnson (R-Wis.) invoked this tired canard at a recent Senate Finance Committee hearing.

Funny how these same apologists for our richest don’t have much sympathy for ordinary Americans who lack the “wherewithal” to pay for medical care, adequate housing, and other necessities. Average wage earners, under current law, can’t even wait until year-end to pay Uncle Sam their taxes. Those taxes come out of each paycheck, wherewithal to pay or not.

Are rich Americans, including billionaires, truly unable to pay tax on their investment gains before they sell the assets yielding those gains? Wanna buy a bridge?

Let’s start with the easiest case: a publicly traded investment that can be sold in smaller units, an investment in stocks, for instance. Say Rich, a wealthy investor, buys 1 million shares of Nvidia at $100 per share, and those shares, by year’s end, increase in value to $120 per share.

Our investor Rich now has a $20 million gain. If that annual gain faced a 25% tax rate, Rich would have a $5 million tax liability. To raise the cash to pay that tax, Rich could sell off 41,667 of his shares, leaving him with 958,333 shares, now worth just under $115 million.

That doesn’t seem very painful.

Now, let’s say Rich didn’t want to sell any shares. He could instead just borrow $5 million against the shares to pay the tax.

Or what if Rich had bought a parcel of land instead of Nvidia shares and, for whatever reason, having him borrow to pay tax on his annual investment gains didn’t turn out to be feasible?

Still no problem for Rich. For gains on illiquid assets, Rich could defer the payment of tax until he sold the assets, but the tax could be computed as if it accrued annually. How might this work? Say, for example, that Rich’s $100 million parcel of land grew at an annual rate of 10% for 20 years, at which point he sold it at its appreciated value of $672,749,995.

Had Rich paid tax at 25% on his gain each year, his rate of return would have been 7.5% per year, and after 20 years his investment would be worth $424,785,110.

The $247,964,885 difference between his sale price and the value of his investment with its actual rate of return reduced by the tax paid would be his tax liability upon sale. Payment of that amount would leave Rich with the same sum, $424,785,110, had he been able to sell a small share of his parcel each year, to pay the tax on his investment gain.

Put another way, Rich would be left with the same amount using this tax computation as he would if he sold his parcel each year, paid tax on the gain, and reinvested the remaining proceeds in another parcel.

And if Rich died before selling his parcel? His income tax could be determined for the year of his death in the same fashion as if he’d sold the parcel for its fair market value at the time of his death. Or, in the alternative, his inheritors could step into his shoes and pay the same tax when they sold the parcel as Rich would have had he survived and sold it at that time.

The bottom line: If we closed the tax-free compounding of investment gains loophole, some situations might exist where the immediate payment of tax on investment gains could pose a problem. But we can address those situations by deferring payment of the tax until investments get sold and accounting for the tax-free compounding in the determination of the tax.

These problematic situations, in other words, don’t justify leaving a gaping loophole in place.

So the obstacle to shutting down buy-borrow-die and buy-hold for decades-sell has absolutely nothing to do with ultra-rich investors lacking the wherewithal to pay taxes. That obstacle remains the politicians in Washington, D.C. who lack the wherewithal to summon the courage to make our rich pay the taxes they owe our nation.

The Billionaires Income Tax proposal that Sen. Ron Wyden (D-Ore.) introduced last year would require billionaires to pay tax annually on the growth in their wealth—in the same way the rest of us pay tax on our salaries and wages.

America’s policymakers have been debating for decades now the fairness of the preferential tax rate for capital gains. The maximum federal income tax rate applicable to long-term capital gains currently sits a whopping 17 percentage points lower than the maximum rate applicable to ordinary income: 20% on long-term gains versus 37% on ordinary income.

Let’s note here at the outset that both ordinary income and capital gains may be subject to federal employment tax or the net investment income tax. But including those additional taxes does not change the essential tax-time gap between ordinary and capital gains income. So, for simplicity’s sake, let’s just here consider the gap between the 20 and 37% rates.

Eliminating the preferential rate for capital gains, many analysts maintain, would finally place investment income and wages on an equal footing tax-wise. But would that actually be the case? Unfortunately, no. Simply equalizing the basic tax rates on ordinary and capital gains income would leave in place the gaping “buy-hold for decades-sell” loophole.

If you had to choose between paying tax at 10% annually or paying 10% every 10 years, would you consider those two rates equal?

The framing of the debate over the current preferential treatment for capital gains makes this loophole quite difficult to notice. And that same framing leaves us accepting, incorrectly, the implied premise that the low nominal tax rate rich investors pay on their capital gains—barely half the rate applicable to other types of income—accurately describes the tax rate in an economic sense.

If we continue to focus solely on whether the 20% rate applied to billionaire gains should be raised to 37%, in other words, we won’t be questioning that accuracy.

A similar phenomenon arises when we’re discussing billionaire wealth. Most of us see the obscene fortunes of the world’s billionaires, as reported by Forbes and Bloomberg, and seldom consider the possibility that many of those fortunes may actually be higher than the published estimates. But think a moment: If you held a billion-dollar fortune and wanted to keep your tax bill as low as possible, would you want policymakers knowing the full extent of your wealth? Of course not.

But most of the rest of us don’t ask that question. We see a deep pocket’s wealth estimated at, say, $50 billion—about 50,000 times more than our own $100,000 net worth—and the last thought to enter our minds would be that this deep pocket’s wealth might really stand at $75 billion.

Just as the bloated level of estimates of billionaire fortunes causes us not to consider the possibility those fortunes may be actually even larger, the low tax rate nominally applicable to capital gains income leaves us unlikely to fully compare tax rates on ordinary and capital gains income.

The key to understanding how to make better comparisons: taking tax frequency into account.

Most of the income Americans make—wages and salaries, most notably—gets taxed annually. Capital gains, by contrast, get taxed only when the holders of investment assets decide to sell them. That reality turns a simple comparison of the 20% tax rate on capital gains with the 37% top tax rate on ordinary income into an apples-to-oranges comparison.

Or to put things another way: If you had to choose between paying tax at 10% annually or paying 10% every 10 years, would you consider those two rates equal?

We can overcome the difficulty in comparing the tax rates on ordinary and capital gains income once we begin to understand why we cannot consider these two situations the same.

Consider, for starters, what your tax liability would be if you inadvertently understated your income from a small business on your tax return by $50,000 and then reported the missing income three years later. You would end up paying the IRS not just the tax you should have paid on that income, but an interest charge as well—for deferring the payment of tax beyond the year you earned your income.

For the sake of discussion, let’s say you were required to pay $10,000 in tax and $2,500 in interest. You would then have paid tax at an overall 20% rate.

Now compare that to the situation your rich friend encountered. She invested $50,000 in stocks and held that investment for four years. Say that investment doubled in value, to $100,000, in the first year—the same year you earned the $50,000 of income you failed to report—and then held that value for another three years. If your friend then sold her investment and paid tax at the 20% rate applicable to capital gains, she could claim to have paid tax at the same 20% rate you did.

But would that be accurate? Not really. Economically, your friend has obviously paid tax at a lower rate than you. Yes, you both realized $50,000 of income in the same year and you both paid tax on that income three years later. But you paid a total of $12,500, including interest, while she paid only $10,000.

What happened here? Economically, your friend’s $10,000 tax payment includes a charge for the privilege of deferring the payment of tax. By contrast, our tax system considers your $2,500 deferral charge on your $10,000 obligation a separate item. To make the comparison apples-to-apples, then, we might consider your friend to have paid tax at an effective annual rate of 16%, $8,000, plus a $2,000 deferral fee.

Now consider the case where you received your $50,000 of income—along with additional income necessary to place you in the top marginal tax bracket—in the same year your friend sold her $50,000 investment for $100,000, rather than the year she purchased it.

You would have paid tax on your $50,000 at the marginal rate of 37%, a total of $18,500—and likely have been laser-focused on having had to pay nearly double the tax rate that your ultra-rich friend paid–37% versus 20%—on the same $50,000 of income. In all likelihood, you would at the same time have failed to focus on the reality that the 20% rate applied to your friend’s gain actually overstated the rate she paid in comparison to the rate you paid.

Let’s expand our financial horizon. Say a rich investor purchases an asset for $1 million. Over the next 30 years, that asset grows in value at a steady pace of 10% per year, an average-ish return for a rich American investor. At the end of the 30 years, the asset would be worth about $17,450,000. If the investor then sold the asset and paid tax at 20% on the $16,450,000 gain, a total tax of $3,290,000, he would be left with about $14,160,000.

Suppose instead our investor had to pay tax annually on each year’s investment gains at the rate of just 7.65%. Suppose our investor each year sold a portion of the investment sufficient to pay the tax liability. At the end of the 30 years, the investor will have paid a total of $1,090,000 in tax and be left with the same amount, $14,160,000, that he would have been left with after paying tax at 20% upon a sale in year 30.

Why the $2,200,000 difference between the $3,290,000 total paid when taxed in year 30 and the $1,090,000 total paid when taxed annually? In economic terms, that’s what the investor paid for the privilege of not paying tax until year 30. In other words, interest.

Removing what economically amounts to a charge for the privilege of deferring tax allows us to make an apples-to-apples comparison. The investor effectively has paid tax at a rate of 6.63%. That’s a 30.37 percentage-point difference between the investor’s effective rate of tax and the 37% top tax rate on ordinary income.

How much would that 30.37 percentage-point gap be reduced if the investor’s $16.45 million gain were taxed at a 37% rate when he sold his investment after 30 years? About five percentage points. Of the investor’s 37% nominal tax rate—using the same method of analysis—about 25.34 percentage points would constitute interest, leaving only 11.66 percentage points, economically, as tax.

Should we equalize the tax rates applicable to capital gains and ordinary income? Absolutely. But let’s not kid ourselves. Making that change will not remotely eliminate the preferential tax treatment accorded to capital gains. We need a further change, at least for the billionaire class.

The Billionaires Income Tax proposal that Sen. Ron Wyden (D-Ore.) introduced last year would require billionaires to pay tax annually on the growth in their wealth—in the same way the rest of us pay tax on our salaries and wages. It’s high time to close the “buy-hold for decades-sell” loophole. Sen. Wyden’s Billionaires Income Tax would be one way to do just that.

The political left in Germany has a plan and strategy for the Elon Musk's of this world and maybe we should be learn from it.

Americans these days don’t much like billionaires. Our ultra-rich, Americans overwhelmingly believe, aren’t paying enough in taxes. Polling earlier this month found that nearly three-quarters of the nation’s likeliest voters — 74 percent — feel billionaires are paying “too little’ at tax time.

Just how concerned about billion-dollar fortunes have Americans become? Nearly half of us overall, Harris polling found last summer, would like to see a limit on “wealth accumulation.” Among Gen Z’ers, that support for limits on billionaire fortunes runs all the way up to 65 percent.

“Billionaires,” some 58 percent of Americans agreed in that same Harris poll, “are becoming more like dictators.”

The share of Americans equating billionaires with dictators — given Elon Musk’s current dominant role in the new Trump White House — is most likely running even higher today.

The best way to counter our ongoing billionaire coup? We might want to look east for some answers. In the run-up to Germany’s February 23 parliamentary elections, that nation’s Left Party, Die Linke, has proposed a detailed five-step set of initiatives designed to cut the super rich down to democratic size.

“We believe,” the Die Linke co-chair Jan van Aken notes simply in his intro to his party’s new plan, “that there should not be any billionaires.”

But van Aken and Die Linke understand quite well that no government can suddenly snap its fingers and make billionaires disappear. The party has instead melded ideas from all around the world into a coherent and common-sense package.

The Die Linke plan’s step one: restoring a “wealth tax.” Germany has been without one since the nation’s top court nixed the wealth tax in effect back in 1995. The proposed new version would revolve around an annual levy starting at 1 percent on wealth over 1 million euros — the equivalent of about $1.03 million — and rising up to 12 percent on wealth concentrations above a billion euros.

On top of that would come a special one-time wealth tax, also on a graduated scale, that would only impact Germans sitting on fortunes worth more than 2 million euros. This levy’s top rate would hit 30 percent for awesomely affluent Germans in the proposal’s highest wealth bracket.

Germany’s super rich would also see, under the Die Linke plan, a higher inheritance tax on the wealth they leave behind. On the annual income side, top corporate executives and other high-earners would face a 75-percent tax rate on their take-homes over a million euros.

The fifth and final plank of the Die Linke plan: replacing the current 25-percent flat tax on capital gains — the income from the sale of financial and other assets — with a graduated sliding scale of rates.

The overall goal of the Die Linke tax plan: a halving of the wealth of Germany’s wealthiest over the next decade. Three other German parties on the left side of German politics are also backing tax hikes on the wealthy, but at levels not nearly as significant as Die Linke.

Elon Musk’s favorite German party, meanwhile, sees nothing wrong in boosting the fortunes of Germany’s most fortunate. The ultra-far-right Alternative for Germany party, the Musk-backed Alternative für Deutschland, is pledging higher tax relief for capital gains and an end to Germany’s existing inheritance tax.

Current polling is making the former investment banker Friedrich Merz the favorite to become Germany’s next chancellor. His conservative Christian Democratic Union party favors lowering the corporate tax rate and is now polling support from near 30 percent of Germany’s voters. Polls have the anti-immigrant AfD at a bit over 20 percent.

Die Linke has been rising in the pre-election polling since the party unveiled its tax plan, and the party gained 11,000 new members in January. Analysts now see Die Linke likely to finish with about 6 percent of the overall vote tally, maybe enough to prevent Germany’s right-wingers from forming a new government. But the party’s bold tax plan, either way, has no shot at becoming the law of the land in Germany’s next legislative session.

Still, what seems no more than tax-the-rich pie-in-the-sky in one generation can become actual tax policy in the next. In 1917, for instance, a bold group of American progressives proposed a tax rate of 100 percent on annual income over $100,000, the equivalent of nearly $2.5 million in today’s dollars. A generation later, in 1942, President Franklin Roosevelt asked Congress to place that same 100-percent tax rate on America’s most affluent.

Lawmakers didn’t buy FDR’s 100-percent top rate, but they did pass legislation that had America’s richest facing a 94-percent tax on their top-bracket income by 1944. That U.S. top tax rate would hover around 90 percent for the next two decades, years that would see the United States become the world’s first-ever mass-middle-class nation.

“The wealthiest of the wealthy have figured out how to get richer and richer and richer and richer in ways that just don’t show up on a tax form," said Sen. Elizabeth Warren at a recent Senate hearing. It's time to change that.

The first televised U.S. presidential debate came way back in 1960. Few of us who happened to watch that debate remember much about it. But a look back at the transcript of that debate — a session that concentrated on domestic issues — shows that the evening’s proceedings mentioned not a single word about a stunning domestic transformation then about midway through its third decade.

That transformation? The United States had become a significantly more economically equal nation. With federal tax rates running as high as 91 percent on top-bracket income and unions representing more than a third of America’s private-sector workers — over five times today’s private-sector union share — the United States had given birth to the world’s first mass middle class.

In just a single generation, America had gone from a nation where the richest 1 percent held nearly half the nation’s wealth to a nation where that top 1 percent held only just over a fifth of that wealth.

This stunning reality came up nowhere in that first debate between the Democratic Party candidate John Kennedy, then a U.S. senator, and Richard Nixon, the nation’s Republican vice president.

But what if that debate had explicitly recognized that reality? What if that debate’s panel of journalists had asked the candidates whether they would encourage or discourage, strengthen or trim, the tax and labor policies that had created a much more equal United States?

If those journalists had asked questions along that line, would John Kennedy, once president, have dared to ask Congress, as he did in 1963, to drop the top-bracket tax rate on America’s richest down to 65 percent?

That Kennedy-era Congress would end up lowering the nation’s top tax rate, from 91 to 70 percent. A bit over two decades later, in Ronald Reagan’s second term in the White House, that top rate would sink all the way down to 28 percent.

The current top rate? On income over $731,201, married couples filing jointly face a 37 percent tax rate. Taxpayers making 100 times that $731,201, over $73 million, face that same 37 percent top rate. And on “capital gains,” the profits from the sale of stocks and other assets, these rich pay taxes at no more than a 20 percent rate.

At last week’s first — and probable last — debate between Kamala Harris and Donald Trump, the two candidates faced no questions on how little in taxes our contemporary tax code expects rich people to pay. Few noticed. But last week, at a Senate hearing on Capitol Hill, Finance Committee chair Ron Wyden from Oregon did his best to inject how much in taxes rich people don’t pay into America’s most high-profile political deliberations.

The bargain-basement tax rates on high incomes now in place, Senator Wyden made vividly clear, only hint at the tax windfalls our super rich are now regularly realizing.

Our billionaires, Wyden noted as he opened the hearing, can essentially “avoid paying taxes forever” through a neat trick tax justice advocates have come to label “buy-borrow-die.”

Our ultra-wealthy, Wyden went on to explain, are using their wealth to acquire valuable assets, then watching those assets appreciate and borrowing against the higher value of those assets to generate the cash they need to maintain their luxurious lifestyles. Eventually, of course, these deep pockets die, but any tax owed on their investment gains simply “disappears into the ledgers of history.” Their heirs face no tax whatsoever on the gains their benefactors have left them.

“This kind of tax trickery isn’t available to nurses and firefighters and tradesmen. Their taxes come straight out of every paycheck,” Wyden pointed out. “The ultra-wealthy get their own special set of rules.”

Long-time tax attorney Bob Lord, the current senior advisor on tax policy for the Patriotic Millionaires network and an Institute for Policy Studies associate fellow, expanded on “buy-borrow-die” and assorted other lucrative tax dodges in his testimony today before Wyden’s panel. Those dodges could — and should — take center stage in 2025, he agreed, as America’s lawmakers debate whether to extend the 2017 Trump tax cuts for the rich set to expire by next year’s end.

Republican lawmakers on the Senate Finance Committee spent a huge chunk of their time at today’s hearing depicting America’s rich as noble souls doing their best to create jobs in the face of a tax system that harasses them at every turn. Senator Elizabeth Warren from Massachusetts disputed that depiction.

“The wealthiest of the wealthy have figured out how to get richer and richer and richer and richer in ways that just don’t show up on a tax form,” Warren noted. “The result: The top one-tenth of 1 percent pays about 3.2 percent of their wealth in taxes every year while the bottom 99 percent pays more than double that.”

The Biden-Harris administration, the Massachusetts senator added, has advanced a proposal that would subject Americans with net worths over $100 million — the nation’s wealthiest 10,000 people — to a minimum 25 percent tax on their income, well below our federal tax code’s current 37 percent top rate.

But these wealthy, Warren continued, are claiming that they don’t have the money to pay that tax because their wealth is sitting “all locked up in stocks.”

“Are these 10,000 mega-millionaires actually cash-poor?” Warren asked Robert Lord, the veteran tax attorney witness. “Are they living like monks?”

“I haven’t seen,” Lord smiled in reply, “many monks on yachts.”

"Harris seems to be making a policy choice based on the disproven, failed ideology of trickle-down economics, and giving petulant billionaires a gift in the process," said one progressive advocacy group.

Democratic nominee Kamala Harris broke with President Joe Biden on Wednesday by proposing a smaller capital gains tax increase for wealthy Americans, a decision that one progressive advocacy group decried as a "baffling capitulation to Wall Street billionaires" who have vocally complained about the vice president's embrace of higher taxes on the ultra-rich.

Harris said at a campaign event in New Hampshire on Wednesday that "if you earn a million dollars a year or more, the tax rate on your long-term capital gains will be 28% under my plan," broadly confirming earlier reporting by The Wall Street Journal.

"We know when the government encourages investment, it leads to broad-based economic growth and it creates jobs, which makes our economy stronger," said Harris, who previously signaled support for Biden's tax agenda.

A 28% top tax rate on long-term capital gains—profits from the sale of an asset held for more than a year—would be significantly lower than the 39.6% rate that Biden proposed in his most recent budget.

The Patriotic Millionaires, a group of rich Americans that advocates for a more progressive tax system, said it was "appalled" by Harris' decision to pare back Biden's proposed capital gains tax increase.

"Vice President Harris is making a catastrophic mistake by capitulating to the petulant whining of the billionaire class," said Morris Pearl, the group's chair. "Harris seems to be making a policy choice based on the disproven, failed ideology of trickle-down economics, and giving petulant billionaires a gift in the process."

"Both on the economics and on the politics, this is a serious unforced error."

Details of Harris' capital gains tax plan began to emerge days after ultra-rich investors and other major donors to the vice president's 2024 campaign took to the pages of The New York Times to express concerns about Harris' support for Biden's tax agenda, which also calls for taxing the unrealized capital gains of households worth over $100 million.

The Financial Times described Harris' break with Biden on long-term capital gains as "an olive branch to Wall Street"; The New York Times similarly characterized the move as a message to the business community that she is "friendlier than Biden."

But Pearl of the Patriotic Millionaires warned that the policy shift "demonstrates a concerning lack of commitment to reversing destabilizing economic inequality."

"Both on the economics and on the politics, this is a serious unforced error," said Pearl, the former managing director at the investment behemoth BlackRock. "You don't need my years of experience on Wall Street to grasp the obvious. Big investors invest to make serious money, not to save a few percentage points on their tax bill. No one has ever made a lucrative investment decision based on a preferential tax rate. The incentive to invest is making money, not lowering tax rates."

"This ill-advised, destructive policy is a giveaway to the ultra-rich," he added. "We hope Vice President Harris will reconsider her position."

Even with a smaller proposed capital gains tax increase, Harris' tax agenda stands in stark contrast to that of Republican presidential nominee Donald Trump, who has called for massive additional tax cuts for the rich and large corporations while attacking Harris' support for progressive—and widely popular—tax proposals.

While Trump has not yet outlined a capital gains proposal during the 2024 campaign, the former president said in the final year of his first term that he would propose cutting the top capital gains rate to 15% in a second term.

Steve Wamhoff of the Institute on Taxation and Economic Policy noted at the time that 99% of the benefits of such a cut "would go to the richest 1% of taxpayers."

Hillary Clinton is ahead in the polls, but it's more due to Donald Trump's many blunders than excitement with Mrs. Clinton. She has benefited from being the anti-Trump. But new allegations about the FBI finding another 15,000 missing emails and evidence of a possible "pay-to-play" donation system between her husband's Clinton Global Initiative and the Secretary of State's office raises old perceptions about her untrustworthiness and dishonesty.

Mrs. Clinton's campaign badly needs a bold issue that will fire voters' imaginations. Otherwise, if Trump stops the bloopers and regains his economic populism, this race could tighten very quickly.

What issue should Hillary Clinton focus on that will rally voters? Here's one that will neutralize her opponent's economic appeal: a dramatic expansion of Social Security.

This popular program, which celebrated its 81st birthday on August 14, enjoys stratospheric support, even among 70% of Republican rank-and-file voters. It's the greatest anti-poverty program that the US has ever devised. Three-quarters of Americans depend heavily on Social Security in their elderly years, and nearly half would be living in poverty without it. It's been an especially important support system for minority and female retirees. During the 2008-09 economic crisis, when home ownership, private savings and the stock market collapsed, Social Security remained stable.

Despite its popularity, critics have stoked the fear that Social Security will face a financial shortfall sometime in the 2030s. But that is overblown, Social Security has an established trust fund that, legally speaking, cannot spend more than it takes in. Any future deficits could be made up from any number of revenue sources. It's all a matter of budgetary priorities.

In fact, the real problem with Social Security is not a shortfall but that its payout is so meager. Social Security is designed to replace only about 40 percent of a worker's wages at retirement, yet retirement experts estimate you will need almost twice that amount to live decently. With private retirement pensions, as well as personal savings centered on homeownership - the other two legs of the three-legged "stool of retirement" -still looking wobbly, and with incomes low and inequality high, tens of millions of retirees won't have much more than their monthly Social Security checks to live on.

Social Security is too stingy to function as the nation's single-pillar retirement system. As Senator Bernie Sanders pointed out during his presidential run, the obvious solution is to expand Social Security, not cut it. Numerous revenue streams would allow an increase in the monthly payout for the 43 million Americans who receive retirement benefits.

How much should we expand Social Security? Senator Sanders proposed adding about $68 per month per beneficiary - better than nothing, but not nearly enough to make a significant difference. The US needs a much more dramatic expansion.

If we design it correctly, we can afford to double the monthly benefit for every retiree, creating a new system that I call Social Security Plus. This would come much closer to providing sufficient income for the nation's retirees, and also put the US retirement system in line with the benefits provided by many other developed nations. As demonstrated in my recently published book Expand Social Security Now: How to Ensure Americans Get the Retirement They Deserve, there is so much waste in the US tax system that if we simply close many of the tax loopholes and deductions that disproportionately favor wealthier Americans, the nation could easily afford this.

Social Security Plus: How to pay for it

How much would it cost to doublethe monthly payout? Approximately $662 billion. That seems like a lot of money, but here's how we could do it.

1. Eliminate the unfair Social Security payroll cap. Currently, any income above $118,500 is not taxed for Social Security purposes. The cap's practical effect is that billionaire bankers and CEOs contribute a far lower percentage of their income to Social Security—much less than 1%—than their secretaries and chauffeurs, whose income is taxed at a rate of 6.2%.

The old rationale for this discrepancy is that Social Security is not welfare; instead, it is an earned benefit—the more you pay into it, the more you receive. According to this line of thinking, the maximum amount that a Social Security beneficiary can receive is capped at around $2600, and if the benefit is capped, so should the payroll deduction. If we are going to lift the payroll cap and tax wealthier Americans more, shouldn't they also receive more of a payout?

But that's not how Medicare works, nor private company pensions, nor any other tax-funded government service. Wealthy people don't receive more access to doctors, hospitals, roads, schools or airports just because they pay more in taxes. The rationale for treating Social Security so differently might have made sense when it was launched over 80 years ago, and there was little tradition of government providing a helping hand. But it makes much less sense today in this time of rampant inequality and greater acceptance of government acting as a counter-balance to unstable market economies.

So simply making the payroll contribution more fair and equal by requiring all income levels to contribute at the same rate of 6.2% on all of their earned wages would raise approximately $135 billion toward the targeted goal.

2. Apply a Social Security tax to investment income. Many wealthy Americans make a lot of their money through investment income instead of from wages. Yet they make zero Social Security contributions based on that income. By applying Social Security rules on this investment income -- which is how Medicare is partly funded -- we would raise another $50 billion more for doubling the Social Security payout

3. Eliminate tax shelters and loopholes for 1-percenter households and businesses. The loopholes crying out for elimination include capital gains and other types of investment income, such as 'carried interest' and the truly outrageous 'step-up in basis,' which exclusively benefits inherited wealth. These function as direct federal subsidies to mostly affluent Americans. And they cost the national treasury some $250 billion per year, with the Congressional Budget Office estimating that a whopping 70 percent of this subsidy is hoovered by Americans in the top 1 percent income bracket (and nearly 93 percent by the top 20 percent bracket).

The 'step-up in basis' exemption is particularly repugnant. When a yacht, mansion or any other type of expensive asset is sold, the seller's profit is subject to the capital gains taxation rate of 15-20 percent -- already only about half the 39.6 percent tax rate that the wealthiest pay on their wage income. Normally, the amount subject to taxation is the difference between the sale price and the amount that the seller originally paid for that particular asset. But for inherited property, the difference is calculated using the date that the previous owner died and left it to the heirs. As a result, the appreciation in value is a lot less, and so are the capital gains taxes. Rather than a 'step-up in basis,' this dodge might more accurately be termed a 'step-up in privilege.' In 2015, this rule reduced federal revenues by an enormous $63 billion.

Step-up in basis is one of the 10 largest federal tax expenditures in the entire individual and corporate income tax system. And most of it is pocketed by the wealthiest of Americans. Of course none of the investment income received from the sale of these inherited assets is taxed for Social Security purposes. If it were, at the usual 6.2 percent Social Security tax rate that all workers pay, it would generate another $19 billion for the Trust Fund.

President Barack Obama has done little to close these loopholes while in office, and Hillary Clinton has been mostly silent. Ironically, Donald Trump has been more outspoken about the unfairness of this system than most Democratic leaders. To his credit, Trump defended Social Security against budget cuts during the GOP presidential debates and primaries. So, Mrs. Clinton is vulnerable on this issue.

4. Eliminate the tax exclusion that private employers receive for sponsoring their company's retirement plans. Not many people realize it, but every tax-paying American subsidizes the retirement plans provided by private companies, even though only a small slice of Americans -- about 15% of private-sector workers -- have pensions today. By implementing Social Security Plus, which would double the monthly benefit and make Social Security the de facto national retirement plan, employers would be liberated from having to provide retirement for their employees. So they will not need the substantial taxpayer-funded subsidies they receive from the federal government for their company's retirement plan. That will raise another $100 billion that can be used for Social Security Plus.

At this point, we have found nearly $600 billion in funding for Social Security Plus, nearly reaching our mark for doubling the monthly retirement benefit. So let's keep going and look for more sources of revenue for our increasingly expanded and financially sound national retirement plan.

5. Scrap other retirement tax breaks that disproportionately benefit wealthier Americans over middle class and poor Americans. Savings vehicles such as 401(k)s and IRAs have tragically failed to help most retirees for a very simple reason -- you can't put very much into your 401(k) if your wages are too low to save. And with aggregate wages in the US staying flat for the last three decades, the reality is that most middle- and poorer-class Americans haven't been able to sock that much away. Consequently, of the $165 billion that the federal government spends subsidizing individual retirement savings, nearly 80 percent goes to the top 20 percent of income earners. President Obama has proposed a universal 401(k), in which workers with no savings plan will be enrolled automatically in a 401(k) plan. But it seems pointless when wages are so low that the vast majority of middle class and poor Americans can't accumulate sufficient savings. Most Americans would be far better off if we scrapped the 401(k) and IRA subsidies and instead doubled the Social Security monthly benefit.

The same is true for federal underwriting of homeownership, which totaled $154 billion in 2014. The federal subsidy for the home mortgage interest deduction amounts to around $70 billion per year, with Americans in the top 10-percent income bracket receiving a massive 86 percent of it. The federal tax deduction allowed homeowners to mitigate the cost of paying state and local property taxes on their houses, which cost the federal budget another $32 billion in 2014; a study by the Congressional Budget Office found that Americans in the upper 20 percent income bracket reaped 80 percent of that federal subsidy.

Just to make sure everyone understands whom the tax code favors, homeowners also do not have to pay taxes on up to $250,000 of their capital gains profits when they sell their home, which doubles to $500,000 for married taxpayers. That exclusion amounts to another giant subsidy amounting to $52 billion per year. And here's the real kicker: these three subsidies for homeownership, which in aggregate mostly benefit higher-income people, cost the federal treasury nearly four times the $42 billion that the Department of Housing and Urban Development spends on all affordable housing programs for low-income people. Renters and most low-income Americans don't benefit at all from the subsidies, and while some middle-income people benefit, the total amount of their deductions is too small to help them much. They would benefit a lot more from a doubling of their Social Security payout.

Whose entitlement? Who's the 'welfare queen'?

Critics of Social Security have derogatorily labeled it an 'entitlement,' but in reality these tax-code favoritisms are nothing more than entitlements for wealthier people at the expense of everyone else. The affluent recipients of federal largess are the true 'welfare queens,' since these subsidies are mostly unavailable to middle- and lower-income Americans.

If we combine those budgetary add-backs with our previous savings, we now have reached nearly $900 billion, well over the $662 billion we need in order to enact Social Security Plus. And note that we were able to do this without spending a dime more in taxpayer money or national wealth than what is already spent on the retirement system, or on subsidizing the savings of better-off Americans. We are just shifting existing expenditures that right now benefit a small number of people, and redirecting these resources toward the vast majority of people.

Social Security remains one of the most popular government programs ever. It benefits not only the nation's retirees but also US businesses and the broader national economy. Retirees spend their income to live, providing customers for businesses even during an economic downturn. So, Social Security acts as an automatic stimulus that helps maintain consumer spending levels, which in turn helps stabilize the economy.

Moreover, expanded Social Security would be a better fit for the type of high-tech digital economy that is slowly taking root. More and more Americans are working as contractors, freelancers, temps and part-timers for multiple employers; many Americans now are working several part-time jobs to make ends meet. Social Security Plus would form a core part of a portable, universal safety net that is badly needed, providing a new kind of deal for American workers.

More members of Congress, led by Senators Bernie Sanders and Elizabeth Warren, as well as other political and media leaders and organizations like Social Security Works and the Progressive Change Campaign Committee, have come to the conclusion that we need to expand Social Security. So has President Obama, who initially disappointed his backers by supporting ill-advised cuts to the program and appointing an ill-fated commission that tried to enact cuts. Unfortunately, Hillary Clinton has been the worst kind of waffler on this issue. Her latest position is that she will support expansion, but only for those who need it the most, which means not many people. If she isn't careful, she is going to be leapfrogged by Donald Trump, who is unpredictable enough to take a bolder stand on Social Security.

The simple message is that we can pay for this expansion by enacting tax fairness, and ensuring that all Americans contribute their fair share to the nation's bounty and security. With support among even Republicans extremely high, there appears to be no political risk to Hillary Clinton being out front on this issue. And with her campaign teetering on the edge of a cliff of scandal and pay-to-play politics, the Clinton campaign needs a popular issue that excites voters. Social Security expansion provides a vision for not only how our nation will treat our retirees, but also for what kind of nation we want to be.

So, Mrs. Clinton should become a key catalyst in this movement for Social Security expansion by leading the way during this presidential election. What is she waiting for?