SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

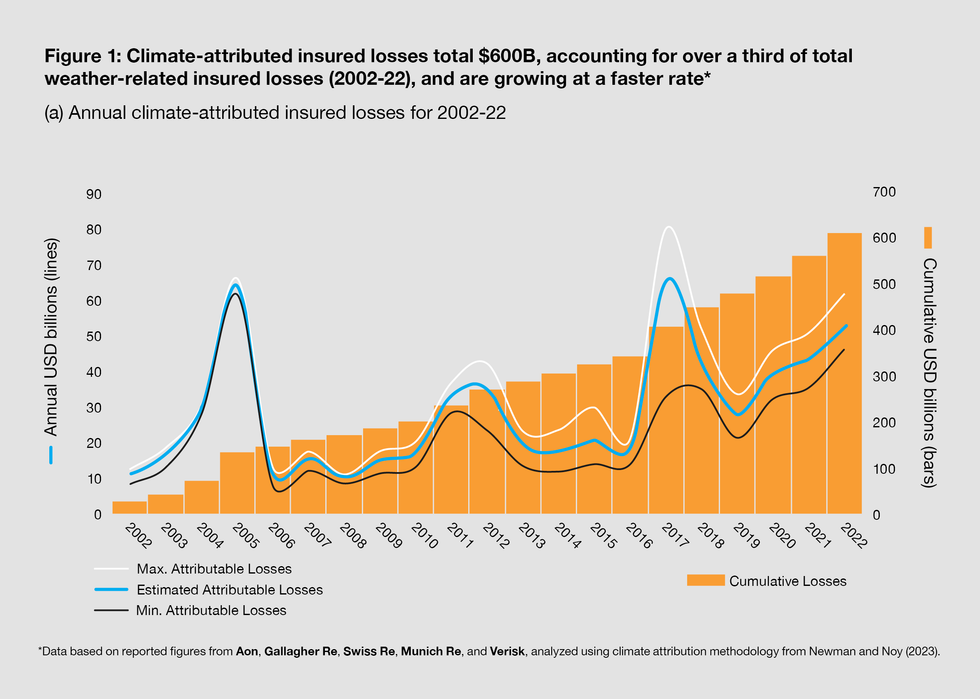

A report out Tuesday shows that the fossil fuel-driven climate emergency accounts for an estimated $600 billion of global insured weather losses over a recent two-decade period, which a campaign targeting the insurance industry called "an immense climate price tag that insurers have long been passing on to policyholders."

Insure Our Future, the international campaign behind the eighth annual scorecard, is supported by advocacy groups including Ekō, Greenpeace, Mazaska Talks, Public Citizen, Rainforest Action Network, Reclaim Finance, the Sunrise Project, and Waterkeeper Alliance.

The report—titled, Within Our Power: Cut Emissions Today To Insure Tomorrow—"examines what 20 years of climate attribution science reveals about today's insurance crisis, explores the status of gross direct premiums from insuring fossil fuels and renewable energy activities, and analyzes the coal, oil, and gas policies of 30 leading primary insurers and reinsurers."

While climate-attributed losses from 2002 to 2022 worked out to around $30 billion annually, the financial burden was not evenly spread out over those 20 years. Instead, the report says, such losses "have recently accounted for a growing share of insured weather losses, showing how decarbonization is crucial to contain soaring insurance costs."

"The climate-attributed share of insured weather losses rose from 31% to 38% over the last decade on average, and their annual growth (6.5%) significantly outpaced thegrowth of the insured losses (4.9%)," the publication explains. "In 2022, $52 billion out of $132 billion was climate-attributed."

The other key findings are:

The report acknowledges that its findings arrive amid scientists' warnings that 2024 is on track to be the first full year to breach 1.5°C—the Paris agreement's target for temperature rise this century. The latest meeting for countries signed on to that treaty, held in Azerbaijan last month, concluded with what critics called a "big F U to climate justice."

Like activists and experts outraged by the conclusion of COP29, Ilan Noy, a professor focused on the economics of disasters and climate change at New Zealand's Victoria University of Wellington, stressed the importance of bolder global action in response to the Insure Our Future report.

"Insurers are fundamentally misunderstanding climate risk by failing to recognize how greenhouse gas emissions have driven up losses throughout this century," Noy said in a statement. "Unless we cut emissions sharply this decade, climate damages will grow exponentially and could overwhelm both insurers and economies."

Laurie Laybourn, director of the U.K.-based Strategic Climate Risks Initiative, similarly suggested that the climate emergency poses an existential threat to the insurance industry while discussing Insure Our Future's report with Forbes' David Vetter.

"Because insurance impacts are mounting and because we don't have an insurance system built for the way that climate change is evolving, this dynamic is only going to get much worse," Laybourn said. "As we're already seeing, governments are having to step in to effectively ensure that insurance can still exist in certain places."

"In Florida, you have a situation where flood insurance is increasingly receding and the government is having to make decisions about how and what to cover," he noted. "It's the case as well in the U.K., where major flooding events led to the creation of Flood Re, a government-backed reinsurance agency to cover places that are effectively uninsurable through private markets."

Warning of a potential "doom loop" in which climate impacts cause instability that impedes adequately ambitious action, Laybourn added that "we need systems that are more resilient so that we can continue to remain focused on decarbonization, even as things get more unstable."

The new report offers a roadmap to a more resilient insurance system. As the document points out, this is the first time Insure Our Future has included policy recommendations for lawmakers and regulators.

The publication urges insurance firms to immediately stop insuring new fossil fuel projects or any customers from the industry that have not published a transition plan for the 1.5°C goal. It also calls on insurers to set their own binding Paris-aligned targets and to divest from coal, gas, and oil companies.

The report further pushes insurers to align stewardship activities, trade associations membership, and public positions with a credible 1.5°C pathway; establish mechanisms to ensure clients fully respect human rights; and explore bringing fossil fuel companies to court "to make polluters rather than insurance customers pay."

A report out Tuesday shows that the fossil fuel-driven climate emergency accounts for an estimated $600 billion of global insured weather losses over a recent two-decade period, which a campaign targeting the insurance industry called "an immense climate price tag that insurers have long been passing on to policyholders."

Insure Our Future, the international campaign behind the eighth annual scorecard, is supported by advocacy groups including Ekō, Greenpeace, Mazaska Talks, Public Citizen, Rainforest Action Network, Reclaim Finance, the Sunrise Project, and Waterkeeper Alliance.

The report—titled, Within Our Power: Cut Emissions Today To Insure Tomorrow—"examines what 20 years of climate attribution science reveals about today's insurance crisis, explores the status of gross direct premiums from insuring fossil fuels and renewable energy activities, and analyzes the coal, oil, and gas policies of 30 leading primary insurers and reinsurers."

While climate-attributed losses from 2002 to 2022 worked out to around $30 billion annually, the financial burden was not evenly spread out over those 20 years. Instead, the report says, such losses "have recently accounted for a growing share of insured weather losses, showing how decarbonization is crucial to contain soaring insurance costs."

"The climate-attributed share of insured weather losses rose from 31% to 38% over the last decade on average, and their annual growth (6.5%) significantly outpaced thegrowth of the insured losses (4.9%)," the publication explains. "In 2022, $52 billion out of $132 billion was climate-attributed."

The other key findings are:

The report acknowledges that its findings arrive amid scientists' warnings that 2024 is on track to be the first full year to breach 1.5°C—the Paris agreement's target for temperature rise this century. The latest meeting for countries signed on to that treaty, held in Azerbaijan last month, concluded with what critics called a "big F U to climate justice."

Like activists and experts outraged by the conclusion of COP29, Ilan Noy, a professor focused on the economics of disasters and climate change at New Zealand's Victoria University of Wellington, stressed the importance of bolder global action in response to the Insure Our Future report.

"Insurers are fundamentally misunderstanding climate risk by failing to recognize how greenhouse gas emissions have driven up losses throughout this century," Noy said in a statement. "Unless we cut emissions sharply this decade, climate damages will grow exponentially and could overwhelm both insurers and economies."

Laurie Laybourn, director of the U.K.-based Strategic Climate Risks Initiative, similarly suggested that the climate emergency poses an existential threat to the insurance industry while discussing Insure Our Future's report with Forbes' David Vetter.

"Because insurance impacts are mounting and because we don't have an insurance system built for the way that climate change is evolving, this dynamic is only going to get much worse," Laybourn said. "As we're already seeing, governments are having to step in to effectively ensure that insurance can still exist in certain places."

"In Florida, you have a situation where flood insurance is increasingly receding and the government is having to make decisions about how and what to cover," he noted. "It's the case as well in the U.K., where major flooding events led to the creation of Flood Re, a government-backed reinsurance agency to cover places that are effectively uninsurable through private markets."

Warning of a potential "doom loop" in which climate impacts cause instability that impedes adequately ambitious action, Laybourn added that "we need systems that are more resilient so that we can continue to remain focused on decarbonization, even as things get more unstable."

The new report offers a roadmap to a more resilient insurance system. As the document points out, this is the first time Insure Our Future has included policy recommendations for lawmakers and regulators.

The publication urges insurance firms to immediately stop insuring new fossil fuel projects or any customers from the industry that have not published a transition plan for the 1.5°C goal. It also calls on insurers to set their own binding Paris-aligned targets and to divest from coal, gas, and oil companies.

The report further pushes insurers to align stewardship activities, trade associations membership, and public positions with a credible 1.5°C pathway; establish mechanisms to ensure clients fully respect human rights; and explore bringing fossil fuel companies to court "to make polluters rather than insurance customers pay."

A report out Tuesday shows that the fossil fuel-driven climate emergency accounts for an estimated $600 billion of global insured weather losses over a recent two-decade period, which a campaign targeting the insurance industry called "an immense climate price tag that insurers have long been passing on to policyholders."

Insure Our Future, the international campaign behind the eighth annual scorecard, is supported by advocacy groups including Ekō, Greenpeace, Mazaska Talks, Public Citizen, Rainforest Action Network, Reclaim Finance, the Sunrise Project, and Waterkeeper Alliance.

The report—titled, Within Our Power: Cut Emissions Today To Insure Tomorrow—"examines what 20 years of climate attribution science reveals about today's insurance crisis, explores the status of gross direct premiums from insuring fossil fuels and renewable energy activities, and analyzes the coal, oil, and gas policies of 30 leading primary insurers and reinsurers."

While climate-attributed losses from 2002 to 2022 worked out to around $30 billion annually, the financial burden was not evenly spread out over those 20 years. Instead, the report says, such losses "have recently accounted for a growing share of insured weather losses, showing how decarbonization is crucial to contain soaring insurance costs."

"The climate-attributed share of insured weather losses rose from 31% to 38% over the last decade on average, and their annual growth (6.5%) significantly outpaced thegrowth of the insured losses (4.9%)," the publication explains. "In 2022, $52 billion out of $132 billion was climate-attributed."

The other key findings are:

The report acknowledges that its findings arrive amid scientists' warnings that 2024 is on track to be the first full year to breach 1.5°C—the Paris agreement's target for temperature rise this century. The latest meeting for countries signed on to that treaty, held in Azerbaijan last month, concluded with what critics called a "big F U to climate justice."

Like activists and experts outraged by the conclusion of COP29, Ilan Noy, a professor focused on the economics of disasters and climate change at New Zealand's Victoria University of Wellington, stressed the importance of bolder global action in response to the Insure Our Future report.

"Insurers are fundamentally misunderstanding climate risk by failing to recognize how greenhouse gas emissions have driven up losses throughout this century," Noy said in a statement. "Unless we cut emissions sharply this decade, climate damages will grow exponentially and could overwhelm both insurers and economies."

Laurie Laybourn, director of the U.K.-based Strategic Climate Risks Initiative, similarly suggested that the climate emergency poses an existential threat to the insurance industry while discussing Insure Our Future's report with Forbes' David Vetter.

"Because insurance impacts are mounting and because we don't have an insurance system built for the way that climate change is evolving, this dynamic is only going to get much worse," Laybourn said. "As we're already seeing, governments are having to step in to effectively ensure that insurance can still exist in certain places."

"In Florida, you have a situation where flood insurance is increasingly receding and the government is having to make decisions about how and what to cover," he noted. "It's the case as well in the U.K., where major flooding events led to the creation of Flood Re, a government-backed reinsurance agency to cover places that are effectively uninsurable through private markets."

Warning of a potential "doom loop" in which climate impacts cause instability that impedes adequately ambitious action, Laybourn added that "we need systems that are more resilient so that we can continue to remain focused on decarbonization, even as things get more unstable."

The new report offers a roadmap to a more resilient insurance system. As the document points out, this is the first time Insure Our Future has included policy recommendations for lawmakers and regulators.

The publication urges insurance firms to immediately stop insuring new fossil fuel projects or any customers from the industry that have not published a transition plan for the 1.5°C goal. It also calls on insurers to set their own binding Paris-aligned targets and to divest from coal, gas, and oil companies.

The report further pushes insurers to align stewardship activities, trade associations membership, and public positions with a credible 1.5°C pathway; establish mechanisms to ensure clients fully respect human rights; and explore bringing fossil fuel companies to court "to make polluters rather than insurance customers pay."