SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

The Republicans in Congress, along with Trump on alternate days, are pushing plans that are supposed to give choice to individuals and somehow take it away from insurers. It’s not clear what they think they are saying. They seem to still envision that people will buy insurance, as they do now in the Obamacare exchanges, but somehow that they will have more control in the Republican option.

There is one story they could envision, which would make it much easier for insurers to skew their pool. The Affordable Care Act (ACA) restricted what sort of plans could be offered in the exchanges in order to limit the ability for insurers to avoid high-cost individuals.

It would be possible to relax these restrictions to allow insurers to cherry pick their enrollees. For example, they could offer high-deductible plans, say $15,000 in payments, before any coverage kicked in.

The Republican healthcare plan is a rerun of the bluff and lie strategy they have been doing for more than 15 years.

No person with a serious health condition would buy this sort of plan since they know they would be paying at least $15,000 a year in medical expenses, and then a substantial fraction of everything above this amount, in addition to the premium itself. On the other hand, a low-cost plan with $15,000 deductible might look pretty good to someone in good health, whose medical expenses usually don’t run beyond the cost of annual checkup.

The Republicans can look like the great promoters of individual choice by allowing insurers to market these high-deductible plans. The problem is that healthy people will all gravitate to high-deductible plans, leaving only the people with serious health issues—the 10%—to buy plans with more modest deductibles.

These plans will then be ridiculously expensive since insurers are not going to insure people at a loss. If they have a pool with four or five times the average per person healthcare costs, they will charge a premium that is four five times the average cost, plus a margin for administrative costs and profits. This means that cancer survivors, people with heart disease, and other serious health conditions will be screwed, given the option of ridiculously expensive insurance or none at all.

The most painful part of this story is that we have all been around the block many times on this story. Unless Trump and the Republicans are extremely ignorant, which can never be ruled out, they are simply lying and hope that the media will let them get away with it. They have no brilliant plan to lower healthcare costs. They are simply proposing a scheme that will lower premiums for healthy people by screwing the ones who need healthcare most.

It amounts to lowering costs by not providing care. It’s like reducing the cost of food by not letting people eat. But if the point of a healthcare system is to provide people with the healthcare they need, the Republican proposals are nonstarters.

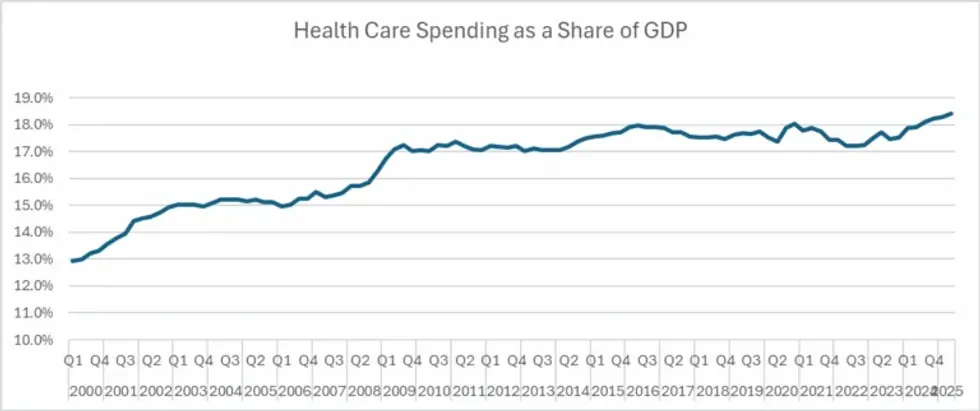

As a practical matter, contrary to what the Republicans and the media say, healthcare cost growth did slow sharply after Obamacare passed. That may not have been entirely due to Obamacare, but that is the reality. Too bad the Democratic consultants tell Democratic politicians not to talk about it.

We do pay way too much for healthcare in the United States, but it is not because of Obamacare. We pay twice as much for our drugs, medical equipment, and doctors as people in other wealthy countries. These high payments persist because they are supported by powerful lobbies.

Some of us had hope that the Trump administration might take some steps to reduce these prices, especially in the case of drugs, since RFK, Jr. had railed against corruption in the pharmaceutical industry. Unfortunately, his tirades were limited to an evidence-free crusade against long-proven vaccines, which are not even a major source of profit for the industry.

Donald Trump talked about reducing drug prices 1,500% (really), but this mostly amounted to getting his name on a drug discount website for a small group of patients. We were spending 6.4% more on drugs in September of this year than in the same month in 2024. (September is the most recent month for which data are available.)

Trump has shown no interest in doing anything to lower the cost of medical equipment. And he has said nothing about lowering doctors’ fees, although some reshuffling of the Medicare reimbursement schedules may reduce overpayments to specialists and better pay for family practitioners. His immigration policies are going the wrong way here, making it even more difficult for foreign-trained medical students and doctors to practice here.

And there are the insurers themselves, which gobble up close to 25% of the money they pay out to providers in the form of administrative costs and profits. A recent study found that If we add in the cost imposed by insurers on hospitals, doctors’ offices, and other providers, they take up close to a third of healthcare expenses.

Trump has shown no interest in reining in the insurance industry apart from his silly talking point about giving people money directly to… wait, wait, buy their own unregulated insurance. That will do nothing to reduce the money flowing into the industry’s pockets.

The Republican healthcare plan is a rerun of the bluff and lie strategy they have been doing for more than 15 years. Given the right-wing control of much of the media, it could work for them politically. The tragic part of the story is that millions could end up without the healthcare they need.