SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

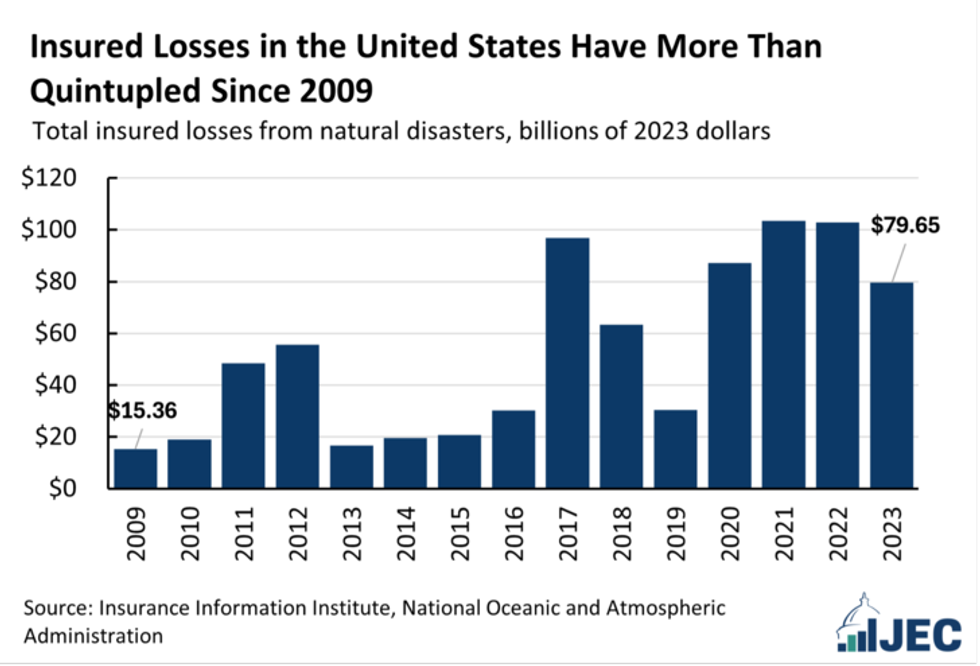

After at least two dozen U.S. disasters with losses exceeding $1 billion during a year that is on track to be the hottest on record, a congressional committee on Monday released a report detailing how the fossil fuel-driven climate emergency poses a "significant threat" to the country's housing and insurance markets.

"Climate-exacerbated disasters, such as wildfires, hurricanes, floods, drought, and excessive heat, are increasing risk and causing damage to homes across the country," states the report from Democrats on the Joint Economic Committee (JEC). "Last year, roughly 70% of Americans reported that their community experienced an extreme weather event."

"In the 1980s, the United States experienced an average of one billion-dollar disaster (adjusted for inflation) every four months; now, these significant disasters occur approximately every three weeks," the document continues. "2023 was the worst year for home insurers since 2000, with losses reaching $15.2 billion—more than twice the losses reported in 2022."

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief."

The insurance industry is already responding to that stress. The publication highlights that "insurers are pulling out of some states with substantial wildfire or hurricane risk—like California, Arizona, Florida, and North Carolina—leaving some areas 'uninsurable,'" and "in many regions, even if the homeowner can get insurance, the policy covers less than the actual physical climate risks (for example, rising sea levels or more intense wildfires) that their home faces, leaving them 'underinsured.'"

JEC Democratic staff found that last year, "the average U.S. homeowners' insurance rate rose over 11%," and from 2011-21, it soared 44%. Researchers also documented state-by-state jumps for 2020-23. For increases, Florida was the highest ($1,272), followed by Louisiana ($986), the District of Columbia ($971), Colorado ($892), Massachusetts ($855), and Nebraska ($849).

The highest premiums for 2023 were in Florida ($3,547), Nebraska ($3,055), Oklahoma ($2,990), Massachusetts ($2,980), Colorado ($2,972), Hawaii ($2,958), D.C. ($2,867), Louisana ($2,793), Rhode Island ($2,792), and Mississippi ($2,787).

The report ties the rising premiums to "surging" prices for repairs, reinsurers also hiking rates, insurance litigation issues, and rate caps in some states pushing higher costs off to states that regulate the industry less. While JEC Democrats focused on the United States, as Common Dreams reported last week, the climate threat to the insurance industry is a global problem.

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief," the new report warns. "Given this rising threat, innovations in climate mitigation and adaptation, insurance options, and disaster relief are essential for protecting Americans and their finances."

The publication points out that "a previous JEC report on climate financial risks discussed other potential solutions like parametric insurance (a supplemental insurance plan that can pay homeowners faster), community-based catastrophe insurance that incentivizes community-level resilience efforts, and attempts to use risk-pooling, data, and AI to better price risk."

The new document also promotes the Wildfire Insurance Coverage Study Act, introduced by JEC Chair Sen. Martin Heinrich (D-N.M.) "to address these data needs and study wildfire risk, insurance, and mitigation to help Americans make more informed decisions about the risks to their homes," and the Shelter Act, which "would create a new tax credit, allowing taxpayers to deduct 25% of disaster mitigation expenditures."

The report further recommends improvements to several Federal Emergency Management Agency (FEMA) programs, including:

The JEC publication comes as the country prepares for President-elect Donald Trump to take office next month after running a campaign backed by billionaires and fossil fuel executives and pledging to "drill, baby, drill," which would increase planet-heating pollution as scientists warn of the need for cutting emissions. Republicans will also have control of both chambers of Congress.

Heinrich on Monday called out the GOP for its climate record, saying that "Republicans have denied that climate change is real for over 40 years, and as a result, homeowners are seeing their insurance costs rise."

"Homeowners in New Mexico have seen their premiums increase by $400 over the last three years because of Republicans' refusal to act," he added, citing the 2020-2023 data. "The longer climate deniers keep up this charade, the more expensive things will get."

After at least two dozen U.S. disasters with losses exceeding $1 billion during a year that is on track to be the hottest on record, a congressional committee on Monday released a report detailing how the fossil fuel-driven climate emergency poses a "significant threat" to the country's housing and insurance markets.

"Climate-exacerbated disasters, such as wildfires, hurricanes, floods, drought, and excessive heat, are increasing risk and causing damage to homes across the country," states the report from Democrats on the Joint Economic Committee (JEC). "Last year, roughly 70% of Americans reported that their community experienced an extreme weather event."

"In the 1980s, the United States experienced an average of one billion-dollar disaster (adjusted for inflation) every four months; now, these significant disasters occur approximately every three weeks," the document continues. "2023 was the worst year for home insurers since 2000, with losses reaching $15.2 billion—more than twice the losses reported in 2022."

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief."

The insurance industry is already responding to that stress. The publication highlights that "insurers are pulling out of some states with substantial wildfire or hurricane risk—like California, Arizona, Florida, and North Carolina—leaving some areas 'uninsurable,'" and "in many regions, even if the homeowner can get insurance, the policy covers less than the actual physical climate risks (for example, rising sea levels or more intense wildfires) that their home faces, leaving them 'underinsured.'"

JEC Democratic staff found that last year, "the average U.S. homeowners' insurance rate rose over 11%," and from 2011-21, it soared 44%. Researchers also documented state-by-state jumps for 2020-23. For increases, Florida was the highest ($1,272), followed by Louisiana ($986), the District of Columbia ($971), Colorado ($892), Massachusetts ($855), and Nebraska ($849).

The highest premiums for 2023 were in Florida ($3,547), Nebraska ($3,055), Oklahoma ($2,990), Massachusetts ($2,980), Colorado ($2,972), Hawaii ($2,958), D.C. ($2,867), Louisana ($2,793), Rhode Island ($2,792), and Mississippi ($2,787).

The report ties the rising premiums to "surging" prices for repairs, reinsurers also hiking rates, insurance litigation issues, and rate caps in some states pushing higher costs off to states that regulate the industry less. While JEC Democrats focused on the United States, as Common Dreams reported last week, the climate threat to the insurance industry is a global problem.

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief," the new report warns. "Given this rising threat, innovations in climate mitigation and adaptation, insurance options, and disaster relief are essential for protecting Americans and their finances."

The publication points out that "a previous JEC report on climate financial risks discussed other potential solutions like parametric insurance (a supplemental insurance plan that can pay homeowners faster), community-based catastrophe insurance that incentivizes community-level resilience efforts, and attempts to use risk-pooling, data, and AI to better price risk."

The new document also promotes the Wildfire Insurance Coverage Study Act, introduced by JEC Chair Sen. Martin Heinrich (D-N.M.) "to address these data needs and study wildfire risk, insurance, and mitigation to help Americans make more informed decisions about the risks to their homes," and the Shelter Act, which "would create a new tax credit, allowing taxpayers to deduct 25% of disaster mitigation expenditures."

The report further recommends improvements to several Federal Emergency Management Agency (FEMA) programs, including:

The JEC publication comes as the country prepares for President-elect Donald Trump to take office next month after running a campaign backed by billionaires and fossil fuel executives and pledging to "drill, baby, drill," which would increase planet-heating pollution as scientists warn of the need for cutting emissions. Republicans will also have control of both chambers of Congress.

Heinrich on Monday called out the GOP for its climate record, saying that "Republicans have denied that climate change is real for over 40 years, and as a result, homeowners are seeing their insurance costs rise."

"Homeowners in New Mexico have seen their premiums increase by $400 over the last three years because of Republicans' refusal to act," he added, citing the 2020-2023 data. "The longer climate deniers keep up this charade, the more expensive things will get."

After at least two dozen U.S. disasters with losses exceeding $1 billion during a year that is on track to be the hottest on record, a congressional committee on Monday released a report detailing how the fossil fuel-driven climate emergency poses a "significant threat" to the country's housing and insurance markets.

"Climate-exacerbated disasters, such as wildfires, hurricanes, floods, drought, and excessive heat, are increasing risk and causing damage to homes across the country," states the report from Democrats on the Joint Economic Committee (JEC). "Last year, roughly 70% of Americans reported that their community experienced an extreme weather event."

"In the 1980s, the United States experienced an average of one billion-dollar disaster (adjusted for inflation) every four months; now, these significant disasters occur approximately every three weeks," the document continues. "2023 was the worst year for home insurers since 2000, with losses reaching $15.2 billion—more than twice the losses reported in 2022."

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief."

The insurance industry is already responding to that stress. The publication highlights that "insurers are pulling out of some states with substantial wildfire or hurricane risk—like California, Arizona, Florida, and North Carolina—leaving some areas 'uninsurable,'" and "in many regions, even if the homeowner can get insurance, the policy covers less than the actual physical climate risks (for example, rising sea levels or more intense wildfires) that their home faces, leaving them 'underinsured.'"

JEC Democratic staff found that last year, "the average U.S. homeowners' insurance rate rose over 11%," and from 2011-21, it soared 44%. Researchers also documented state-by-state jumps for 2020-23. For increases, Florida was the highest ($1,272), followed by Louisiana ($986), the District of Columbia ($971), Colorado ($892), Massachusetts ($855), and Nebraska ($849).

The highest premiums for 2023 were in Florida ($3,547), Nebraska ($3,055), Oklahoma ($2,990), Massachusetts ($2,980), Colorado ($2,972), Hawaii ($2,958), D.C. ($2,867), Louisana ($2,793), Rhode Island ($2,792), and Mississippi ($2,787).

The report ties the rising premiums to "surging" prices for repairs, reinsurers also hiking rates, insurance litigation issues, and rate caps in some states pushing higher costs off to states that regulate the industry less. While JEC Democrats focused on the United States, as Common Dreams reported last week, the climate threat to the insurance industry is a global problem.

"Rising premiums and this issue of uninsurability could seriously disrupt the housing market and stress state-operated insurance programs, public services, and disaster relief," the new report warns. "Given this rising threat, innovations in climate mitigation and adaptation, insurance options, and disaster relief are essential for protecting Americans and their finances."

The publication points out that "a previous JEC report on climate financial risks discussed other potential solutions like parametric insurance (a supplemental insurance plan that can pay homeowners faster), community-based catastrophe insurance that incentivizes community-level resilience efforts, and attempts to use risk-pooling, data, and AI to better price risk."

The new document also promotes the Wildfire Insurance Coverage Study Act, introduced by JEC Chair Sen. Martin Heinrich (D-N.M.) "to address these data needs and study wildfire risk, insurance, and mitigation to help Americans make more informed decisions about the risks to their homes," and the Shelter Act, which "would create a new tax credit, allowing taxpayers to deduct 25% of disaster mitigation expenditures."

The report further recommends improvements to several Federal Emergency Management Agency (FEMA) programs, including:

The JEC publication comes as the country prepares for President-elect Donald Trump to take office next month after running a campaign backed by billionaires and fossil fuel executives and pledging to "drill, baby, drill," which would increase planet-heating pollution as scientists warn of the need for cutting emissions. Republicans will also have control of both chambers of Congress.

Heinrich on Monday called out the GOP for its climate record, saying that "Republicans have denied that climate change is real for over 40 years, and as a result, homeowners are seeing their insurance costs rise."

"Homeowners in New Mexico have seen their premiums increase by $400 over the last three years because of Republicans' refusal to act," he added, citing the 2020-2023 data. "The longer climate deniers keep up this charade, the more expensive things will get."