SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Obama's miscalculation began in his first term, with his embrace of the premise that substantial deficit cutting was both politically expected and economically necessary, and his appointment of the 2010 Bowles-Simpson Commission as the expression of that mistaken philosophy. Although the Commission's plan was never carried out, its prestige and Obama's parentage of it locked the president into a deflationary deficit reduction path.

This past week, we've seen how the Republicans took advantage of Obama's self-inflicted wound. With the March 1 deadline looming, the White House assumed that if the president gave enough publicity to the harm of pending automatic cuts, the Republicans would just cave. But the Republican leadership calculated that the ensuing political and economic damage would be worse for Obama, so they hung tough.

Obama also assumed that military cuts would be enough to move Republicans to compromise. But with two wars winding down, most Republicans decided that this year they were deficit hawks more than defense hawks.

The president also played the populist card, calling for tax increase on the wealthy to spare the rest of the country program cuts. But that didn't move the Republicans either.

The Republican leadership also deftly evaded the risk of being blamed for shutting down the government. They offered the Democrats a continuing resolution to allow government to keep operating, but at $85 billion below current spending levels. That shifted the onus to Democrats if they refused to take the deal and Congressional leaders advised the president that they were not prepared to take that risk.

Finally, Republicans took some of the sting--and responsibility--out of the sequester by offering to give Obama new flexibility in how he implemented it, thus making it even more his problem.

Next to come is the long awaited grand bargain of the austerity lobby, in which Republicans agree to close some tax loopholes (which start out grotesquely swollen) and Democrats agree to breach the previously sacrosanct fortresses of Social Security and Medicare.

On all counts, advantage: Republicans.

Long term, colluding in the politics of budget austerity has left Obama with no real capacity to offer the public investment that the economy needs for a robust, broadly-based recovery, and leaves him with the prospect of a weak economy between now and the end of his term--unless he drastically shifts course and repudiates the entire view of the budget and the economy.

Faced with this budget squeeze, Obama has been able to offer only token new initiatives. His State of the Union speech was part lofty aspirations and part depressive fiscal assumptions. He laid out a bold agenda for rebuilding the middle class. But a decade of pending deficit cuts, mandated by the budget deal of 2011 (of which the sequester is the down-payment), renders most of these commitments hollow. There is no money to pay for new initiatives unless Obama radically changes the fiscal assumptions that have become conventional wisdom in both parties.

At stake are not just the programs that progressives care deeply about but also the recovery itself and the success of the Obama presidency. The automated

reductions of the sequester are only the prologue to a decade long drama, in which the economy faces one budget squeeze after another, all but guaranteeing a prolonged slump. Unless Congress repudiates the 2011 Budget Control Act, and President Obama blows up the entire paradigm that produced it, a fragile recovery will be the victim of budgetary masochism.

The 2011 act implemented the received thinking that is still pervasive--the idea that recovery requires us to achieve a particular ratio of public debt to gross domestic product. In line with Bowles--Simpson thinking, it sets budget caps that steadily ratchet down government outlay over a decade. Domestic discretionary spending--everything from Pell grants to Head Start to public health to protection of our coasts--will be cut from about 7 percent of GDP in 1976 to less than 4 percent this year, and just 2.5 percent by 2023, the lowest since Dwight Eisenhower was president.

The economic assumptions behind this logic are backward. The future debt ratio reflects not just the consequence of budget deficits but also the rate of economic growth. In a weak economy, too much deficit cutting raises the ratio of debt to GDP--because it reduces GDP. Yet the austerity lobby mistakenly assumes that a dollar of budget cut equals a dollar of improvement in the debt ratio. Cutting the debt ratio is the wrong target. The right one is getting growth back on track.

After calling for budget cuts totaling $4 trillion over a decade, the president now says that thanks to cuts already extracted, we only need another $1.5 trillion--budget cutting at a rate more than 50 percent larger than the sequester that has everyone so alarmed. Economically, that figure is still too deflationary. Politically, it just whets the conservative appetite. What we face is not a single decisive showdown but ongoing retrench warfare. With the centenary of World War I coming next year, the analogy is uncomfortably apt.

No matter what deficit reductions the president eventually accepts for this year, Republicans will be pressing for further cuts in fiscal year 2014 and fiscal year 2015 and on into the next decade.To all but the most dogmatic, the right has already lost the debate on the economics. As New York Times columnist Paul Krugman recently observed, the austerity lobby keeps crying wolf about the impact of deficits upon borrowing costs, but interest rates have stayed low. Europe continues to demonstrate the folly of belt-tightening as a strategy of recovery. And the federal deficit is already coming down of its own accord as the economy fitfully returns to life. The debt ratio is now roughly stable in the range of 70 percent to 80 percent of GDP. Several mainstream figures as moderate as former Federal Reserve Vice Chair Alan Blinder, International Monetary Fund Chief Economist Olivier Blanchard, and Financial Times columnist Martin Wolf have all written recently that austerity only breeds more austerity. Even Federal Reserve Chair Ben Bernanke has come close to declaring that the economy needs more fiscal stimulus, not less.

As if to put an exclamation point on these views, the economy shrank by a tenth of 1 percent in the last quarter of 2012, because of a reduction in federal spending. The Pentagon, prudently deferring outlays in anticipation of a possible January 1 sequester, cut spending in the fourth quarter by 22 percent. The Congressional Budget Office (CBO), in its January semi-annual budget review, warned that the slowed growth was the direct result of budget cuts and payroll tax increases. CBO Director Douglas Elmendorf said that the economy was otherwise on track to grow at about 3 percent this year but that the fiscal contraction would shrink the growth rate to just 1.4 percent this fiscal year (October 2012 to September 2013). Growth of around 2 percent is just sufficient to hold the unemployment rate at around an unsatisfactory 8 percent, which produces no pressure to raise wages. But growth of 1.4 percent portends rising joblessness.

(The CBO, which has to answer to both parties, recognizes that budget cutting in the short run slows growth, but then flops around and embraces the conservative view that budget cuts are salutary once the economy reaches full employment. But at the rate that we are deflating the economy, we will never get to full employment.)

Such orthodox economists as Larry Summers of Harvard and Brad DeLong of Berkeley have written that in an economy as sluggish as this one, additional deficit spending would more than pay for itself with higher growth, producing a reduced debt ratio down the road. Josh Bivens of the Economic Policy Institute calculates that in this depressed economy, a $150 billion stimulus outlay that combined general government spending with targeted transfer payments to low-income households "would increase the debt by $71 billion after taking into account revenue and spending feedbacks, but it would also increase GDP by $225 billion, meaning that the debt ratio would actually fall by roughly half a percentage point."

If the austerity cure is intellectually dead, you'd never know it from the broadly shared premise of the continuing debate. Groups like the Peter G. Peterson Foundation, the Committee for a Responsible Federal Budget, Third Way, and Fix the Debt may have been overtaken by economic events, but they have succeeded in defining the fiscal challenge so that nearly everyone--left, right, and center--feels obliged to specify a path to a reduced debt ratio. Responding to the good news that the debt ratio was already roughly stable for the next decade, the austerity groups declared that it was stable at too high a level. On January 31, the Committee for a Responsible Federal Budget put out a statement warning, "Rather than allowing the debt to grow or just barely stabilize the debt, lawmakers must put the debt-to-GDP ratio on a clear downward path. This will require at least $2.2 trillion in new savings between now and 2022, and substantially more over the long run." On February 19, Erskine Bowles and Alan Simpson called for the same additional cut.

This is absurd economics--it would be tantamount to a decade of fiscal cliffs. Yet even President Obama still plays along with the premise that the goal is to get the debt-to-GDP ratio on a downward slope. But surely, if a one-year contraction of $607 billion (the cost of the original "fiscal cliff") is a dangerous precipice, then a $4 trillion cut, nearly seven times that much over a decade, is a fiscal chasm.

Speaking to reporters at the White House on February 5, urging Republicans to delay the sequester while Congress worked out a budget deal, Obama said, "While it's critical for us to cut wasteful spending, we can't just cut our way to prosperity." We can't just cut our way to prosperity. That phrase should be carved into the president's desk. But he added:

The deals that I put forward, the balanced approach of spending cuts and entitlement reform and tax reform that I put forward are still on the table. I've offered sensible reforms to Medicare and other entitlements, and my health-care proposals achieve the same amount of savings by the beginning of the next decade as the reforms that have been proposed by the bipartisan Bowles-Simpson fiscal commission.

More cuts! This is exactly the opposite of what Obama needs to be saying.

Even the center-left Center on Budget and Policy Priorities, which has done heroic work documenting the impact of the cuts, sometimes falls into the same trap of playing the right's game by emphasizing the debt-to-GDP ratio as the test of virtue. In a paper released January 9, the center's Richard Kogan recalculated the numbers and concluded it would take only $1.2 trillion more in budget cuts to stabilize the debt ratio, better than the Obama figures. But why validate that goal at all? Here again, liberals reinforce the mistaken view that the prime goal should be targeting the debt ratio.

As the Greeks have painfully learned over and over again, you can cut spending and raise taxes, and the deficit just keeps growing larger--because you are destroying your economy. The same has been demonstrated for Spain, Portugal, and Britain. Something similar occurred on a more modest scale in the fourth quarter of 2012 right at home.

The White House has been putting out dire warnings about what will occur if the sequester hits. For instance, 70,000 young children will be dropped from Head Start; food-safety inspections will be cut back; 600,000 women and children will lose nutritional benefits; small-business loans will be cut by about $500 million, not to mention massive cuts in defense spending. But the sequester is only a preview of the ten-year deal that the president agreed to in the Budget Control Act of 2011.

Under the act's constraints, domestic social spending will be cut by about $740 billion relative to current program levels. Pell grants, for instance, will be cut by an estimated $50 billion adjusted for inflation and population, meaning that fewer students will be served or the portion of expenses covered will be less.

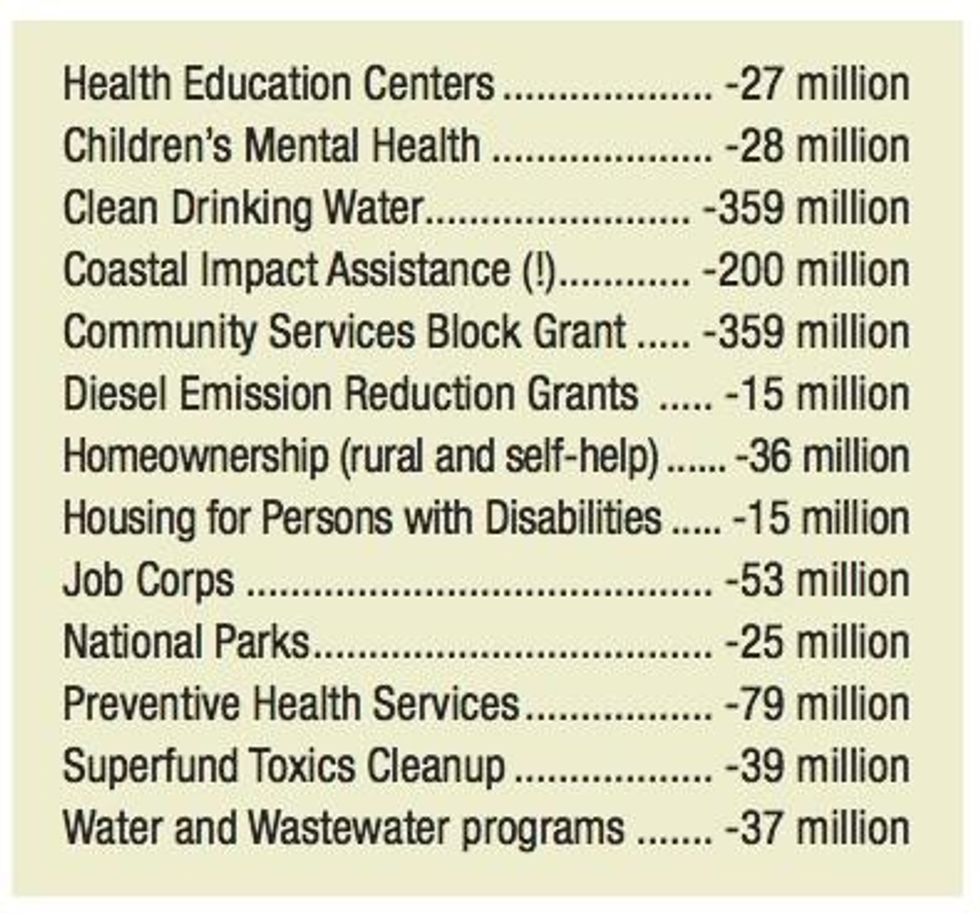

Following the mandate of these caps as well as the president's own commitment to spending cuts, the White House budget for fiscal year 2013 includes $24 billion in domestic reductions. Sample cuts include:

That's just the beginning. Any deal negotiated by House Republicans and the White House, to head off the automatic reductions of the sequester, will impose additional cuts. And we will go through this all over again next year.

Although the New Year's deal averting the fiscal cliff was generally declared a tactical victory for the president, Republicans won on all the details that matter. The original cliff, you'll recall, was the simultaneous sunset of the Bush tax cuts, the end of the two-point temporary reduction in payroll taxes, the spending cuts mandated by the sequester, and the expiration of extended unemployment insurance. President Obama maneuvered Speaker of the House John Boehner into a corner where Republicans were forced to renege on their solemn pledge about not taxing the rich. Obama did not, as some feared, throw Social Security or Medicare into the pot. He seemed to savor his new role as hard bargainer rather than conciliator.

But a closer look suggests how little Obama won. The taxes on the top 1 percent will bring in only about $620 billion in the coming decade, far less than Obama had sought, leaving more money to be taken out of spending later on. The overall deal cuts taxes during the same decade by about $3.6 trillion, some of which is an extension of the Bush income tax cuts to the middle class but much of which is the renewal of business tax preferences. The 2 percent hike in payroll taxes will cost working people close to a trillion dollars of disposable income over a decade. It is a far bigger tax increase in percentage terms than the tax hike on the top 1 percent. The deal was touted as raising taxes only on the rich, but that widely reported description overlooked that payroll taxes are, actually, taxes. Both parties agreed to make further spending cuts into the trillions of dollars, details to be determined later.

Nor did Republicans accept Obama's demand to stop playing games with the debt ceiling once and for all, and the impact of the automatic sequester was delayed by only two months until March 1. So the immediate business before Congress is more spending cuts, with or without the sequester--the only question is how deep. Boehner was right to take the deal. As Pyrrhus, King of Epirus, said in similar circumstances, one more such victory and we are undone.

This story has one other important and underreported element--inflation in the health sector. One budget analyst after another keeps pointing out that the government doesn't have a general deficit problem so much as it has a problem with medical costs. As former Office of Management and Budget Director Peter Orszag, a deficit hawk and big promoter of the Bowles-Simpson Commission, recently wrote in the Financial Times, federal spending on health care is projected to rise from 5.5 percent of GDP today to 12 percent by 2050. During the same period, spending on Social Security is expected to rise only from 5 percent to 6 percent. Take health care out of the equation, and deficits subside without further spending cuts.

Though the rate of health-care inflation has moderated slightly in the past three years, partly because of the weak economy and partly because employers keep cutting back benefits, this is hardly a good solution. Obama's Affordable Care Act will bring coverage to more people, but it made a devil's bargain by not fundamentally changing the structure of the commercial health system, which is what keeps driving up costs. Obama and progressive America will pay dearly for this lapse.

At some point in the next few years, Democrats will either reopen the health debate and move to something like Medicare for All--which will bring far greater efficiency and cost savings to the system--or we will face deepening pressure for spending cuts elsewhere.

The commercialization of the larger health system is devouring the rest of the budget. The solution is neither cuts in other programs, nor the voucherization proposed by the right, nor the incremental cost savings proposed by the center-left. It is a fundamental change in the nature of our health system, and not just of Medicare. Democrats made the wrong choice in backing "Obamacare" rather than true national health insurance and jettisoning even the proposed public option as a way station.

Though too few Democrats will come right out and say it, there is a far better path to both economic recovery and eventual stabilization of the debt ratio. We need to increase public spending in the next few years, using both deficit spending and higher taxes on the wealthy, to get the economy back on a high-growth path. Taxes on the wealthy are better put toward public investment than to deficit reduction. Taxing the rich is far less of a hit to purchasing power than hiking taxes on working families, who spend nearly all of their disposable income. With a program of economic expansion, we can reach a stable long-term debt ratio, but at a higher level of economic output and a more broadly shared prosperity. The goal is economic recovery--and the recovery improves the debt ratio, not the other way around.

Among the economists in this camp are Nobel laureates Paul Krugman and Joseph Stiglitz, as well as Larry Mishel of the Economic Policy Institute, Dean Baker of the Center for Economic and Policy Research, James Galbraith of the University of Texas, and former Biden chief economist Jared Bernstein. In a recent article for the Economic Policy Institute, economists Josh Bivens and Andrew Fieldhouse observed that the "output gap"--the difference between what the economy is producing and what it is capable of producing--is now about a trillion dollars a year. If you cut the budget in such circumstances, you slow growth and get further away from stabilizing the debt ratio. The problem is that these people are not part of the conversation at the White House, which is a dialogue among Obama's top aides, the corporate austerity-mongers, and Republicans, all of whom believe in deficit reduction.

The plans in President Obama's State of the Union message for rebuilding the middle class will cost money. Universal pre-K alone will require more than $20 billion a year. Unless the president cynically imagines token "demonstration" programs, job training, clean energy, manufacturing policies, and infrastructure will also require public money. Obama suggested in the speech that by closing tax loopholes on the wealthy (no small political lift), we could both find the money for new initiatives and still keep to the trajectory of reduced deficits over a decade. But the demands of the Budget Control Act are so extreme that closing loopholes won't generate new spendable resources unless the president rejects the entire premise of budget austerity--something he explicitly did not do in the State of the Union.

When Obama was on the verge of putting Social Security and Medicare on the chopping block last December, the progressive community, led by the labor movement, got organized. Democrats in Congress made clear to the president that they would vote for no budget deal that included cuts in Social Security and Medicare. The strategy worked, and now the stakes are even higher. Democrats in Congress should now put the president on notice that they will not support any more deflationary budgets, and the broader progressive movement ought to reinforce that politics.

The president has public opinion on his side, and he can use his own eloquence to affirm the common sense of the voters. Most Americans, though they support fiscal discipline as an abstraction, are opposed to cuts in programs that the country needs. According to a recent poll by the Kaiser Foundation, Americans oppose cutting spending on education (67 percent), Social Security (58 percent), or Medicare (58 percent).

Last fall, Hurricane Sandy provided a teachable moment on the need for more public investment. In February, about a million people lost power in the Northeast because of a record blizzard. A sensible country would use the occasion to begin putting power lines underground, creating jobs and saving costs in the long run. But all such policies of infrastructure investment are precluded by the fiscal premise that deficit reduction must take precedence.

Obama needs to do something that doesn't come easily to him. He needs to demolish the previous terms of debate, some of them partly of his own making. He has warned Republicans that if they allow the sequester to destroy a fragile recovery, the burden will be on them. More broadly, he needs to disavow earlier mistaken policies that he embraced, such as the belief that targeting a lower debt ratio as an end in itself will produce a recovery. If he could embolden his thinking on such issues as same-sex marriage and gun control, he owes us no less on the economy. Otherwise, Obama will preside over the worst eight-year economic record of any Democratic president, and the steepest rate of decline in social spending. He will leave an economy even more unequal than the one that he inherited. He needs to find within himself the audacity to restore hope.

Obama's miscalculation began in his first term, with his embrace of the premise that substantial deficit cutting was both politically expected and economically necessary, and his appointment of the 2010 Bowles-Simpson Commission as the expression of that mistaken philosophy. Although the Commission's plan was never carried out, its prestige and Obama's parentage of it locked the president into a deflationary deficit reduction path.

This past week, we've seen how the Republicans took advantage of Obama's self-inflicted wound. With the March 1 deadline looming, the White House assumed that if the president gave enough publicity to the harm of pending automatic cuts, the Republicans would just cave. But the Republican leadership calculated that the ensuing political and economic damage would be worse for Obama, so they hung tough.

Obama also assumed that military cuts would be enough to move Republicans to compromise. But with two wars winding down, most Republicans decided that this year they were deficit hawks more than defense hawks.

The president also played the populist card, calling for tax increase on the wealthy to spare the rest of the country program cuts. But that didn't move the Republicans either.

The Republican leadership also deftly evaded the risk of being blamed for shutting down the government. They offered the Democrats a continuing resolution to allow government to keep operating, but at $85 billion below current spending levels. That shifted the onus to Democrats if they refused to take the deal and Congressional leaders advised the president that they were not prepared to take that risk.

Finally, Republicans took some of the sting--and responsibility--out of the sequester by offering to give Obama new flexibility in how he implemented it, thus making it even more his problem.

Next to come is the long awaited grand bargain of the austerity lobby, in which Republicans agree to close some tax loopholes (which start out grotesquely swollen) and Democrats agree to breach the previously sacrosanct fortresses of Social Security and Medicare.

On all counts, advantage: Republicans.

Long term, colluding in the politics of budget austerity has left Obama with no real capacity to offer the public investment that the economy needs for a robust, broadly-based recovery, and leaves him with the prospect of a weak economy between now and the end of his term--unless he drastically shifts course and repudiates the entire view of the budget and the economy.

Faced with this budget squeeze, Obama has been able to offer only token new initiatives. His State of the Union speech was part lofty aspirations and part depressive fiscal assumptions. He laid out a bold agenda for rebuilding the middle class. But a decade of pending deficit cuts, mandated by the budget deal of 2011 (of which the sequester is the down-payment), renders most of these commitments hollow. There is no money to pay for new initiatives unless Obama radically changes the fiscal assumptions that have become conventional wisdom in both parties.

At stake are not just the programs that progressives care deeply about but also the recovery itself and the success of the Obama presidency. The automated

reductions of the sequester are only the prologue to a decade long drama, in which the economy faces one budget squeeze after another, all but guaranteeing a prolonged slump. Unless Congress repudiates the 2011 Budget Control Act, and President Obama blows up the entire paradigm that produced it, a fragile recovery will be the victim of budgetary masochism.

The 2011 act implemented the received thinking that is still pervasive--the idea that recovery requires us to achieve a particular ratio of public debt to gross domestic product. In line with Bowles--Simpson thinking, it sets budget caps that steadily ratchet down government outlay over a decade. Domestic discretionary spending--everything from Pell grants to Head Start to public health to protection of our coasts--will be cut from about 7 percent of GDP in 1976 to less than 4 percent this year, and just 2.5 percent by 2023, the lowest since Dwight Eisenhower was president.

The economic assumptions behind this logic are backward. The future debt ratio reflects not just the consequence of budget deficits but also the rate of economic growth. In a weak economy, too much deficit cutting raises the ratio of debt to GDP--because it reduces GDP. Yet the austerity lobby mistakenly assumes that a dollar of budget cut equals a dollar of improvement in the debt ratio. Cutting the debt ratio is the wrong target. The right one is getting growth back on track.

After calling for budget cuts totaling $4 trillion over a decade, the president now says that thanks to cuts already extracted, we only need another $1.5 trillion--budget cutting at a rate more than 50 percent larger than the sequester that has everyone so alarmed. Economically, that figure is still too deflationary. Politically, it just whets the conservative appetite. What we face is not a single decisive showdown but ongoing retrench warfare. With the centenary of World War I coming next year, the analogy is uncomfortably apt.

No matter what deficit reductions the president eventually accepts for this year, Republicans will be pressing for further cuts in fiscal year 2014 and fiscal year 2015 and on into the next decade.To all but the most dogmatic, the right has already lost the debate on the economics. As New York Times columnist Paul Krugman recently observed, the austerity lobby keeps crying wolf about the impact of deficits upon borrowing costs, but interest rates have stayed low. Europe continues to demonstrate the folly of belt-tightening as a strategy of recovery. And the federal deficit is already coming down of its own accord as the economy fitfully returns to life. The debt ratio is now roughly stable in the range of 70 percent to 80 percent of GDP. Several mainstream figures as moderate as former Federal Reserve Vice Chair Alan Blinder, International Monetary Fund Chief Economist Olivier Blanchard, and Financial Times columnist Martin Wolf have all written recently that austerity only breeds more austerity. Even Federal Reserve Chair Ben Bernanke has come close to declaring that the economy needs more fiscal stimulus, not less.

As if to put an exclamation point on these views, the economy shrank by a tenth of 1 percent in the last quarter of 2012, because of a reduction in federal spending. The Pentagon, prudently deferring outlays in anticipation of a possible January 1 sequester, cut spending in the fourth quarter by 22 percent. The Congressional Budget Office (CBO), in its January semi-annual budget review, warned that the slowed growth was the direct result of budget cuts and payroll tax increases. CBO Director Douglas Elmendorf said that the economy was otherwise on track to grow at about 3 percent this year but that the fiscal contraction would shrink the growth rate to just 1.4 percent this fiscal year (October 2012 to September 2013). Growth of around 2 percent is just sufficient to hold the unemployment rate at around an unsatisfactory 8 percent, which produces no pressure to raise wages. But growth of 1.4 percent portends rising joblessness.

(The CBO, which has to answer to both parties, recognizes that budget cutting in the short run slows growth, but then flops around and embraces the conservative view that budget cuts are salutary once the economy reaches full employment. But at the rate that we are deflating the economy, we will never get to full employment.)

Such orthodox economists as Larry Summers of Harvard and Brad DeLong of Berkeley have written that in an economy as sluggish as this one, additional deficit spending would more than pay for itself with higher growth, producing a reduced debt ratio down the road. Josh Bivens of the Economic Policy Institute calculates that in this depressed economy, a $150 billion stimulus outlay that combined general government spending with targeted transfer payments to low-income households "would increase the debt by $71 billion after taking into account revenue and spending feedbacks, but it would also increase GDP by $225 billion, meaning that the debt ratio would actually fall by roughly half a percentage point."

If the austerity cure is intellectually dead, you'd never know it from the broadly shared premise of the continuing debate. Groups like the Peter G. Peterson Foundation, the Committee for a Responsible Federal Budget, Third Way, and Fix the Debt may have been overtaken by economic events, but they have succeeded in defining the fiscal challenge so that nearly everyone--left, right, and center--feels obliged to specify a path to a reduced debt ratio. Responding to the good news that the debt ratio was already roughly stable for the next decade, the austerity groups declared that it was stable at too high a level. On January 31, the Committee for a Responsible Federal Budget put out a statement warning, "Rather than allowing the debt to grow or just barely stabilize the debt, lawmakers must put the debt-to-GDP ratio on a clear downward path. This will require at least $2.2 trillion in new savings between now and 2022, and substantially more over the long run." On February 19, Erskine Bowles and Alan Simpson called for the same additional cut.

This is absurd economics--it would be tantamount to a decade of fiscal cliffs. Yet even President Obama still plays along with the premise that the goal is to get the debt-to-GDP ratio on a downward slope. But surely, if a one-year contraction of $607 billion (the cost of the original "fiscal cliff") is a dangerous precipice, then a $4 trillion cut, nearly seven times that much over a decade, is a fiscal chasm.

Speaking to reporters at the White House on February 5, urging Republicans to delay the sequester while Congress worked out a budget deal, Obama said, "While it's critical for us to cut wasteful spending, we can't just cut our way to prosperity." We can't just cut our way to prosperity. That phrase should be carved into the president's desk. But he added:

The deals that I put forward, the balanced approach of spending cuts and entitlement reform and tax reform that I put forward are still on the table. I've offered sensible reforms to Medicare and other entitlements, and my health-care proposals achieve the same amount of savings by the beginning of the next decade as the reforms that have been proposed by the bipartisan Bowles-Simpson fiscal commission.

More cuts! This is exactly the opposite of what Obama needs to be saying.

Even the center-left Center on Budget and Policy Priorities, which has done heroic work documenting the impact of the cuts, sometimes falls into the same trap of playing the right's game by emphasizing the debt-to-GDP ratio as the test of virtue. In a paper released January 9, the center's Richard Kogan recalculated the numbers and concluded it would take only $1.2 trillion more in budget cuts to stabilize the debt ratio, better than the Obama figures. But why validate that goal at all? Here again, liberals reinforce the mistaken view that the prime goal should be targeting the debt ratio.

As the Greeks have painfully learned over and over again, you can cut spending and raise taxes, and the deficit just keeps growing larger--because you are destroying your economy. The same has been demonstrated for Spain, Portugal, and Britain. Something similar occurred on a more modest scale in the fourth quarter of 2012 right at home.

The White House has been putting out dire warnings about what will occur if the sequester hits. For instance, 70,000 young children will be dropped from Head Start; food-safety inspections will be cut back; 600,000 women and children will lose nutritional benefits; small-business loans will be cut by about $500 million, not to mention massive cuts in defense spending. But the sequester is only a preview of the ten-year deal that the president agreed to in the Budget Control Act of 2011.

Under the act's constraints, domestic social spending will be cut by about $740 billion relative to current program levels. Pell grants, for instance, will be cut by an estimated $50 billion adjusted for inflation and population, meaning that fewer students will be served or the portion of expenses covered will be less.

Following the mandate of these caps as well as the president's own commitment to spending cuts, the White House budget for fiscal year 2013 includes $24 billion in domestic reductions. Sample cuts include:

That's just the beginning. Any deal negotiated by House Republicans and the White House, to head off the automatic reductions of the sequester, will impose additional cuts. And we will go through this all over again next year.

Although the New Year's deal averting the fiscal cliff was generally declared a tactical victory for the president, Republicans won on all the details that matter. The original cliff, you'll recall, was the simultaneous sunset of the Bush tax cuts, the end of the two-point temporary reduction in payroll taxes, the spending cuts mandated by the sequester, and the expiration of extended unemployment insurance. President Obama maneuvered Speaker of the House John Boehner into a corner where Republicans were forced to renege on their solemn pledge about not taxing the rich. Obama did not, as some feared, throw Social Security or Medicare into the pot. He seemed to savor his new role as hard bargainer rather than conciliator.

But a closer look suggests how little Obama won. The taxes on the top 1 percent will bring in only about $620 billion in the coming decade, far less than Obama had sought, leaving more money to be taken out of spending later on. The overall deal cuts taxes during the same decade by about $3.6 trillion, some of which is an extension of the Bush income tax cuts to the middle class but much of which is the renewal of business tax preferences. The 2 percent hike in payroll taxes will cost working people close to a trillion dollars of disposable income over a decade. It is a far bigger tax increase in percentage terms than the tax hike on the top 1 percent. The deal was touted as raising taxes only on the rich, but that widely reported description overlooked that payroll taxes are, actually, taxes. Both parties agreed to make further spending cuts into the trillions of dollars, details to be determined later.

Nor did Republicans accept Obama's demand to stop playing games with the debt ceiling once and for all, and the impact of the automatic sequester was delayed by only two months until March 1. So the immediate business before Congress is more spending cuts, with or without the sequester--the only question is how deep. Boehner was right to take the deal. As Pyrrhus, King of Epirus, said in similar circumstances, one more such victory and we are undone.

This story has one other important and underreported element--inflation in the health sector. One budget analyst after another keeps pointing out that the government doesn't have a general deficit problem so much as it has a problem with medical costs. As former Office of Management and Budget Director Peter Orszag, a deficit hawk and big promoter of the Bowles-Simpson Commission, recently wrote in the Financial Times, federal spending on health care is projected to rise from 5.5 percent of GDP today to 12 percent by 2050. During the same period, spending on Social Security is expected to rise only from 5 percent to 6 percent. Take health care out of the equation, and deficits subside without further spending cuts.

Though the rate of health-care inflation has moderated slightly in the past three years, partly because of the weak economy and partly because employers keep cutting back benefits, this is hardly a good solution. Obama's Affordable Care Act will bring coverage to more people, but it made a devil's bargain by not fundamentally changing the structure of the commercial health system, which is what keeps driving up costs. Obama and progressive America will pay dearly for this lapse.

At some point in the next few years, Democrats will either reopen the health debate and move to something like Medicare for All--which will bring far greater efficiency and cost savings to the system--or we will face deepening pressure for spending cuts elsewhere.

The commercialization of the larger health system is devouring the rest of the budget. The solution is neither cuts in other programs, nor the voucherization proposed by the right, nor the incremental cost savings proposed by the center-left. It is a fundamental change in the nature of our health system, and not just of Medicare. Democrats made the wrong choice in backing "Obamacare" rather than true national health insurance and jettisoning even the proposed public option as a way station.

Though too few Democrats will come right out and say it, there is a far better path to both economic recovery and eventual stabilization of the debt ratio. We need to increase public spending in the next few years, using both deficit spending and higher taxes on the wealthy, to get the economy back on a high-growth path. Taxes on the wealthy are better put toward public investment than to deficit reduction. Taxing the rich is far less of a hit to purchasing power than hiking taxes on working families, who spend nearly all of their disposable income. With a program of economic expansion, we can reach a stable long-term debt ratio, but at a higher level of economic output and a more broadly shared prosperity. The goal is economic recovery--and the recovery improves the debt ratio, not the other way around.

Among the economists in this camp are Nobel laureates Paul Krugman and Joseph Stiglitz, as well as Larry Mishel of the Economic Policy Institute, Dean Baker of the Center for Economic and Policy Research, James Galbraith of the University of Texas, and former Biden chief economist Jared Bernstein. In a recent article for the Economic Policy Institute, economists Josh Bivens and Andrew Fieldhouse observed that the "output gap"--the difference between what the economy is producing and what it is capable of producing--is now about a trillion dollars a year. If you cut the budget in such circumstances, you slow growth and get further away from stabilizing the debt ratio. The problem is that these people are not part of the conversation at the White House, which is a dialogue among Obama's top aides, the corporate austerity-mongers, and Republicans, all of whom believe in deficit reduction.

The plans in President Obama's State of the Union message for rebuilding the middle class will cost money. Universal pre-K alone will require more than $20 billion a year. Unless the president cynically imagines token "demonstration" programs, job training, clean energy, manufacturing policies, and infrastructure will also require public money. Obama suggested in the speech that by closing tax loopholes on the wealthy (no small political lift), we could both find the money for new initiatives and still keep to the trajectory of reduced deficits over a decade. But the demands of the Budget Control Act are so extreme that closing loopholes won't generate new spendable resources unless the president rejects the entire premise of budget austerity--something he explicitly did not do in the State of the Union.

When Obama was on the verge of putting Social Security and Medicare on the chopping block last December, the progressive community, led by the labor movement, got organized. Democrats in Congress made clear to the president that they would vote for no budget deal that included cuts in Social Security and Medicare. The strategy worked, and now the stakes are even higher. Democrats in Congress should now put the president on notice that they will not support any more deflationary budgets, and the broader progressive movement ought to reinforce that politics.

The president has public opinion on his side, and he can use his own eloquence to affirm the common sense of the voters. Most Americans, though they support fiscal discipline as an abstraction, are opposed to cuts in programs that the country needs. According to a recent poll by the Kaiser Foundation, Americans oppose cutting spending on education (67 percent), Social Security (58 percent), or Medicare (58 percent).

Last fall, Hurricane Sandy provided a teachable moment on the need for more public investment. In February, about a million people lost power in the Northeast because of a record blizzard. A sensible country would use the occasion to begin putting power lines underground, creating jobs and saving costs in the long run. But all such policies of infrastructure investment are precluded by the fiscal premise that deficit reduction must take precedence.

Obama needs to do something that doesn't come easily to him. He needs to demolish the previous terms of debate, some of them partly of his own making. He has warned Republicans that if they allow the sequester to destroy a fragile recovery, the burden will be on them. More broadly, he needs to disavow earlier mistaken policies that he embraced, such as the belief that targeting a lower debt ratio as an end in itself will produce a recovery. If he could embolden his thinking on such issues as same-sex marriage and gun control, he owes us no less on the economy. Otherwise, Obama will preside over the worst eight-year economic record of any Democratic president, and the steepest rate of decline in social spending. He will leave an economy even more unequal than the one that he inherited. He needs to find within himself the audacity to restore hope.

Obama's miscalculation began in his first term, with his embrace of the premise that substantial deficit cutting was both politically expected and economically necessary, and his appointment of the 2010 Bowles-Simpson Commission as the expression of that mistaken philosophy. Although the Commission's plan was never carried out, its prestige and Obama's parentage of it locked the president into a deflationary deficit reduction path.

This past week, we've seen how the Republicans took advantage of Obama's self-inflicted wound. With the March 1 deadline looming, the White House assumed that if the president gave enough publicity to the harm of pending automatic cuts, the Republicans would just cave. But the Republican leadership calculated that the ensuing political and economic damage would be worse for Obama, so they hung tough.

Obama also assumed that military cuts would be enough to move Republicans to compromise. But with two wars winding down, most Republicans decided that this year they were deficit hawks more than defense hawks.

The president also played the populist card, calling for tax increase on the wealthy to spare the rest of the country program cuts. But that didn't move the Republicans either.

The Republican leadership also deftly evaded the risk of being blamed for shutting down the government. They offered the Democrats a continuing resolution to allow government to keep operating, but at $85 billion below current spending levels. That shifted the onus to Democrats if they refused to take the deal and Congressional leaders advised the president that they were not prepared to take that risk.

Finally, Republicans took some of the sting--and responsibility--out of the sequester by offering to give Obama new flexibility in how he implemented it, thus making it even more his problem.

Next to come is the long awaited grand bargain of the austerity lobby, in which Republicans agree to close some tax loopholes (which start out grotesquely swollen) and Democrats agree to breach the previously sacrosanct fortresses of Social Security and Medicare.

On all counts, advantage: Republicans.

Long term, colluding in the politics of budget austerity has left Obama with no real capacity to offer the public investment that the economy needs for a robust, broadly-based recovery, and leaves him with the prospect of a weak economy between now and the end of his term--unless he drastically shifts course and repudiates the entire view of the budget and the economy.

Faced with this budget squeeze, Obama has been able to offer only token new initiatives. His State of the Union speech was part lofty aspirations and part depressive fiscal assumptions. He laid out a bold agenda for rebuilding the middle class. But a decade of pending deficit cuts, mandated by the budget deal of 2011 (of which the sequester is the down-payment), renders most of these commitments hollow. There is no money to pay for new initiatives unless Obama radically changes the fiscal assumptions that have become conventional wisdom in both parties.

At stake are not just the programs that progressives care deeply about but also the recovery itself and the success of the Obama presidency. The automated

reductions of the sequester are only the prologue to a decade long drama, in which the economy faces one budget squeeze after another, all but guaranteeing a prolonged slump. Unless Congress repudiates the 2011 Budget Control Act, and President Obama blows up the entire paradigm that produced it, a fragile recovery will be the victim of budgetary masochism.

The 2011 act implemented the received thinking that is still pervasive--the idea that recovery requires us to achieve a particular ratio of public debt to gross domestic product. In line with Bowles--Simpson thinking, it sets budget caps that steadily ratchet down government outlay over a decade. Domestic discretionary spending--everything from Pell grants to Head Start to public health to protection of our coasts--will be cut from about 7 percent of GDP in 1976 to less than 4 percent this year, and just 2.5 percent by 2023, the lowest since Dwight Eisenhower was president.

The economic assumptions behind this logic are backward. The future debt ratio reflects not just the consequence of budget deficits but also the rate of economic growth. In a weak economy, too much deficit cutting raises the ratio of debt to GDP--because it reduces GDP. Yet the austerity lobby mistakenly assumes that a dollar of budget cut equals a dollar of improvement in the debt ratio. Cutting the debt ratio is the wrong target. The right one is getting growth back on track.

After calling for budget cuts totaling $4 trillion over a decade, the president now says that thanks to cuts already extracted, we only need another $1.5 trillion--budget cutting at a rate more than 50 percent larger than the sequester that has everyone so alarmed. Economically, that figure is still too deflationary. Politically, it just whets the conservative appetite. What we face is not a single decisive showdown but ongoing retrench warfare. With the centenary of World War I coming next year, the analogy is uncomfortably apt.

No matter what deficit reductions the president eventually accepts for this year, Republicans will be pressing for further cuts in fiscal year 2014 and fiscal year 2015 and on into the next decade.To all but the most dogmatic, the right has already lost the debate on the economics. As New York Times columnist Paul Krugman recently observed, the austerity lobby keeps crying wolf about the impact of deficits upon borrowing costs, but interest rates have stayed low. Europe continues to demonstrate the folly of belt-tightening as a strategy of recovery. And the federal deficit is already coming down of its own accord as the economy fitfully returns to life. The debt ratio is now roughly stable in the range of 70 percent to 80 percent of GDP. Several mainstream figures as moderate as former Federal Reserve Vice Chair Alan Blinder, International Monetary Fund Chief Economist Olivier Blanchard, and Financial Times columnist Martin Wolf have all written recently that austerity only breeds more austerity. Even Federal Reserve Chair Ben Bernanke has come close to declaring that the economy needs more fiscal stimulus, not less.

As if to put an exclamation point on these views, the economy shrank by a tenth of 1 percent in the last quarter of 2012, because of a reduction in federal spending. The Pentagon, prudently deferring outlays in anticipation of a possible January 1 sequester, cut spending in the fourth quarter by 22 percent. The Congressional Budget Office (CBO), in its January semi-annual budget review, warned that the slowed growth was the direct result of budget cuts and payroll tax increases. CBO Director Douglas Elmendorf said that the economy was otherwise on track to grow at about 3 percent this year but that the fiscal contraction would shrink the growth rate to just 1.4 percent this fiscal year (October 2012 to September 2013). Growth of around 2 percent is just sufficient to hold the unemployment rate at around an unsatisfactory 8 percent, which produces no pressure to raise wages. But growth of 1.4 percent portends rising joblessness.

(The CBO, which has to answer to both parties, recognizes that budget cutting in the short run slows growth, but then flops around and embraces the conservative view that budget cuts are salutary once the economy reaches full employment. But at the rate that we are deflating the economy, we will never get to full employment.)

Such orthodox economists as Larry Summers of Harvard and Brad DeLong of Berkeley have written that in an economy as sluggish as this one, additional deficit spending would more than pay for itself with higher growth, producing a reduced debt ratio down the road. Josh Bivens of the Economic Policy Institute calculates that in this depressed economy, a $150 billion stimulus outlay that combined general government spending with targeted transfer payments to low-income households "would increase the debt by $71 billion after taking into account revenue and spending feedbacks, but it would also increase GDP by $225 billion, meaning that the debt ratio would actually fall by roughly half a percentage point."

If the austerity cure is intellectually dead, you'd never know it from the broadly shared premise of the continuing debate. Groups like the Peter G. Peterson Foundation, the Committee for a Responsible Federal Budget, Third Way, and Fix the Debt may have been overtaken by economic events, but they have succeeded in defining the fiscal challenge so that nearly everyone--left, right, and center--feels obliged to specify a path to a reduced debt ratio. Responding to the good news that the debt ratio was already roughly stable for the next decade, the austerity groups declared that it was stable at too high a level. On January 31, the Committee for a Responsible Federal Budget put out a statement warning, "Rather than allowing the debt to grow or just barely stabilize the debt, lawmakers must put the debt-to-GDP ratio on a clear downward path. This will require at least $2.2 trillion in new savings between now and 2022, and substantially more over the long run." On February 19, Erskine Bowles and Alan Simpson called for the same additional cut.

This is absurd economics--it would be tantamount to a decade of fiscal cliffs. Yet even President Obama still plays along with the premise that the goal is to get the debt-to-GDP ratio on a downward slope. But surely, if a one-year contraction of $607 billion (the cost of the original "fiscal cliff") is a dangerous precipice, then a $4 trillion cut, nearly seven times that much over a decade, is a fiscal chasm.

Speaking to reporters at the White House on February 5, urging Republicans to delay the sequester while Congress worked out a budget deal, Obama said, "While it's critical for us to cut wasteful spending, we can't just cut our way to prosperity." We can't just cut our way to prosperity. That phrase should be carved into the president's desk. But he added:

The deals that I put forward, the balanced approach of spending cuts and entitlement reform and tax reform that I put forward are still on the table. I've offered sensible reforms to Medicare and other entitlements, and my health-care proposals achieve the same amount of savings by the beginning of the next decade as the reforms that have been proposed by the bipartisan Bowles-Simpson fiscal commission.

More cuts! This is exactly the opposite of what Obama needs to be saying.

Even the center-left Center on Budget and Policy Priorities, which has done heroic work documenting the impact of the cuts, sometimes falls into the same trap of playing the right's game by emphasizing the debt-to-GDP ratio as the test of virtue. In a paper released January 9, the center's Richard Kogan recalculated the numbers and concluded it would take only $1.2 trillion more in budget cuts to stabilize the debt ratio, better than the Obama figures. But why validate that goal at all? Here again, liberals reinforce the mistaken view that the prime goal should be targeting the debt ratio.

As the Greeks have painfully learned over and over again, you can cut spending and raise taxes, and the deficit just keeps growing larger--because you are destroying your economy. The same has been demonstrated for Spain, Portugal, and Britain. Something similar occurred on a more modest scale in the fourth quarter of 2012 right at home.

The White House has been putting out dire warnings about what will occur if the sequester hits. For instance, 70,000 young children will be dropped from Head Start; food-safety inspections will be cut back; 600,000 women and children will lose nutritional benefits; small-business loans will be cut by about $500 million, not to mention massive cuts in defense spending. But the sequester is only a preview of the ten-year deal that the president agreed to in the Budget Control Act of 2011.

Under the act's constraints, domestic social spending will be cut by about $740 billion relative to current program levels. Pell grants, for instance, will be cut by an estimated $50 billion adjusted for inflation and population, meaning that fewer students will be served or the portion of expenses covered will be less.

Following the mandate of these caps as well as the president's own commitment to spending cuts, the White House budget for fiscal year 2013 includes $24 billion in domestic reductions. Sample cuts include:

That's just the beginning. Any deal negotiated by House Republicans and the White House, to head off the automatic reductions of the sequester, will impose additional cuts. And we will go through this all over again next year.

Although the New Year's deal averting the fiscal cliff was generally declared a tactical victory for the president, Republicans won on all the details that matter. The original cliff, you'll recall, was the simultaneous sunset of the Bush tax cuts, the end of the two-point temporary reduction in payroll taxes, the spending cuts mandated by the sequester, and the expiration of extended unemployment insurance. President Obama maneuvered Speaker of the House John Boehner into a corner where Republicans were forced to renege on their solemn pledge about not taxing the rich. Obama did not, as some feared, throw Social Security or Medicare into the pot. He seemed to savor his new role as hard bargainer rather than conciliator.

But a closer look suggests how little Obama won. The taxes on the top 1 percent will bring in only about $620 billion in the coming decade, far less than Obama had sought, leaving more money to be taken out of spending later on. The overall deal cuts taxes during the same decade by about $3.6 trillion, some of which is an extension of the Bush income tax cuts to the middle class but much of which is the renewal of business tax preferences. The 2 percent hike in payroll taxes will cost working people close to a trillion dollars of disposable income over a decade. It is a far bigger tax increase in percentage terms than the tax hike on the top 1 percent. The deal was touted as raising taxes only on the rich, but that widely reported description overlooked that payroll taxes are, actually, taxes. Both parties agreed to make further spending cuts into the trillions of dollars, details to be determined later.

Nor did Republicans accept Obama's demand to stop playing games with the debt ceiling once and for all, and the impact of the automatic sequester was delayed by only two months until March 1. So the immediate business before Congress is more spending cuts, with or without the sequester--the only question is how deep. Boehner was right to take the deal. As Pyrrhus, King of Epirus, said in similar circumstances, one more such victory and we are undone.

This story has one other important and underreported element--inflation in the health sector. One budget analyst after another keeps pointing out that the government doesn't have a general deficit problem so much as it has a problem with medical costs. As former Office of Management and Budget Director Peter Orszag, a deficit hawk and big promoter of the Bowles-Simpson Commission, recently wrote in the Financial Times, federal spending on health care is projected to rise from 5.5 percent of GDP today to 12 percent by 2050. During the same period, spending on Social Security is expected to rise only from 5 percent to 6 percent. Take health care out of the equation, and deficits subside without further spending cuts.

Though the rate of health-care inflation has moderated slightly in the past three years, partly because of the weak economy and partly because employers keep cutting back benefits, this is hardly a good solution. Obama's Affordable Care Act will bring coverage to more people, but it made a devil's bargain by not fundamentally changing the structure of the commercial health system, which is what keeps driving up costs. Obama and progressive America will pay dearly for this lapse.

At some point in the next few years, Democrats will either reopen the health debate and move to something like Medicare for All--which will bring far greater efficiency and cost savings to the system--or we will face deepening pressure for spending cuts elsewhere.

The commercialization of the larger health system is devouring the rest of the budget. The solution is neither cuts in other programs, nor the voucherization proposed by the right, nor the incremental cost savings proposed by the center-left. It is a fundamental change in the nature of our health system, and not just of Medicare. Democrats made the wrong choice in backing "Obamacare" rather than true national health insurance and jettisoning even the proposed public option as a way station.

Though too few Democrats will come right out and say it, there is a far better path to both economic recovery and eventual stabilization of the debt ratio. We need to increase public spending in the next few years, using both deficit spending and higher taxes on the wealthy, to get the economy back on a high-growth path. Taxes on the wealthy are better put toward public investment than to deficit reduction. Taxing the rich is far less of a hit to purchasing power than hiking taxes on working families, who spend nearly all of their disposable income. With a program of economic expansion, we can reach a stable long-term debt ratio, but at a higher level of economic output and a more broadly shared prosperity. The goal is economic recovery--and the recovery improves the debt ratio, not the other way around.

Among the economists in this camp are Nobel laureates Paul Krugman and Joseph Stiglitz, as well as Larry Mishel of the Economic Policy Institute, Dean Baker of the Center for Economic and Policy Research, James Galbraith of the University of Texas, and former Biden chief economist Jared Bernstein. In a recent article for the Economic Policy Institute, economists Josh Bivens and Andrew Fieldhouse observed that the "output gap"--the difference between what the economy is producing and what it is capable of producing--is now about a trillion dollars a year. If you cut the budget in such circumstances, you slow growth and get further away from stabilizing the debt ratio. The problem is that these people are not part of the conversation at the White House, which is a dialogue among Obama's top aides, the corporate austerity-mongers, and Republicans, all of whom believe in deficit reduction.

The plans in President Obama's State of the Union message for rebuilding the middle class will cost money. Universal pre-K alone will require more than $20 billion a year. Unless the president cynically imagines token "demonstration" programs, job training, clean energy, manufacturing policies, and infrastructure will also require public money. Obama suggested in the speech that by closing tax loopholes on the wealthy (no small political lift), we could both find the money for new initiatives and still keep to the trajectory of reduced deficits over a decade. But the demands of the Budget Control Act are so extreme that closing loopholes won't generate new spendable resources unless the president rejects the entire premise of budget austerity--something he explicitly did not do in the State of the Union.

When Obama was on the verge of putting Social Security and Medicare on the chopping block last December, the progressive community, led by the labor movement, got organized. Democrats in Congress made clear to the president that they would vote for no budget deal that included cuts in Social Security and Medicare. The strategy worked, and now the stakes are even higher. Democrats in Congress should now put the president on notice that they will not support any more deflationary budgets, and the broader progressive movement ought to reinforce that politics.

The president has public opinion on his side, and he can use his own eloquence to affirm the common sense of the voters. Most Americans, though they support fiscal discipline as an abstraction, are opposed to cuts in programs that the country needs. According to a recent poll by the Kaiser Foundation, Americans oppose cutting spending on education (67 percent), Social Security (58 percent), or Medicare (58 percent).

Last fall, Hurricane Sandy provided a teachable moment on the need for more public investment. In February, about a million people lost power in the Northeast because of a record blizzard. A sensible country would use the occasion to begin putting power lines underground, creating jobs and saving costs in the long run. But all such policies of infrastructure investment are precluded by the fiscal premise that deficit reduction must take precedence.

Obama needs to do something that doesn't come easily to him. He needs to demolish the previous terms of debate, some of them partly of his own making. He has warned Republicans that if they allow the sequester to destroy a fragile recovery, the burden will be on them. More broadly, he needs to disavow earlier mistaken policies that he embraced, such as the belief that targeting a lower debt ratio as an end in itself will produce a recovery. If he could embolden his thinking on such issues as same-sex marriage and gun control, he owes us no less on the economy. Otherwise, Obama will preside over the worst eight-year economic record of any Democratic president, and the steepest rate of decline in social spending. He will leave an economy even more unequal than the one that he inherited. He needs to find within himself the audacity to restore hope.