SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

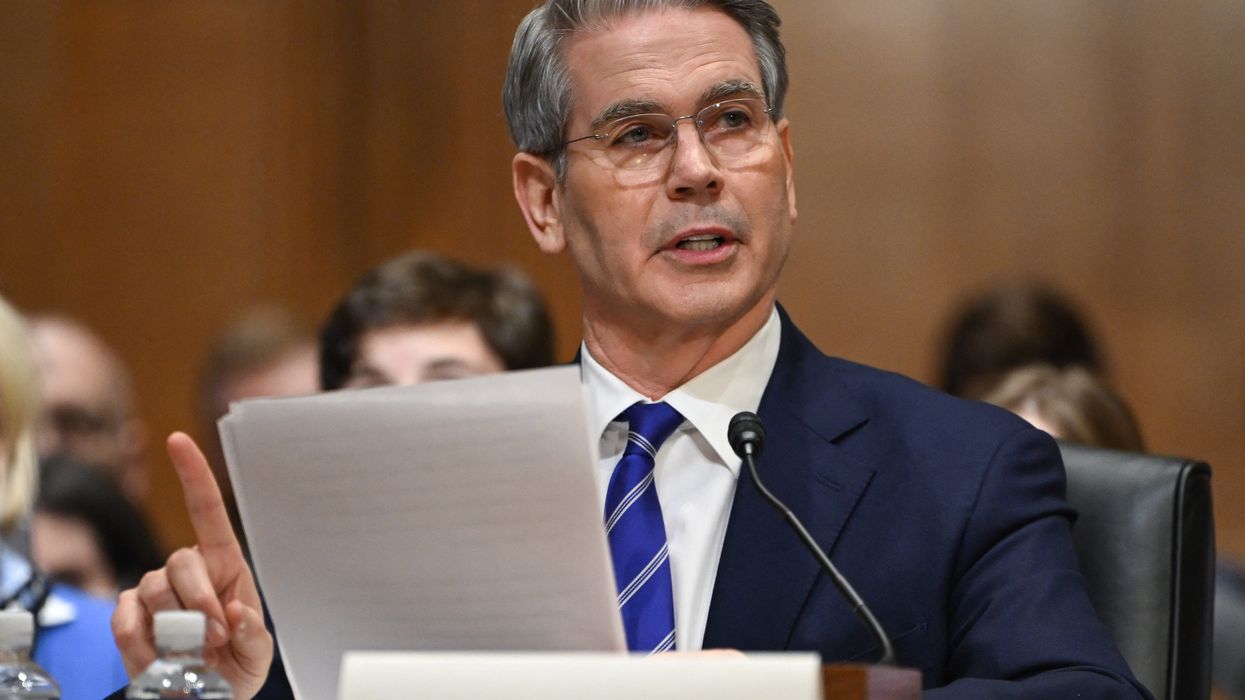

Scott Bessent's "3-3-3" agenda "requires brutal cuts to health and nutrition and higher costs for families at the grocery store," said analysts at the Center for American Progress.

At his confirmation hearing on Thursday, hedge fund manager and U.S. treasury secretary nominee Scott Bessent told the Senate Finance Committee that at the helm of the Treasury Department he would usher in an "economic golden age."

But a report by two policy analysts details how Bessent's signature "3-3-3" plan would only be achievable by gutting programs for some of the nation's most vulnerable households—extending the "golden age" only to wealthy people and corporations for whom the Trump administration plans to slash taxes.

At the Center for American Progress, senior director of economic policy Brendan Duke and senior director of federal budget policy Bobby Kogan completed "the accounting to determine what it would take to achieve" Bessent's 3-3-3 agenda, particularly his plan to cut the federal budget deficit down to 3% of the gross domestic product (GDP). The plan also calls for real GDP growth to reach 3% and the production of 3 million barrels of oil by 2028.

While reducing the budget deficit and simultaneously protecting programs American families rely on is a "laudable goal," wrote Duke and Kogan, Bessent has "explicitly stated that extending the expiring 2017 tax cuts is a priority, and he would likely rule out tax increases on the wealthy to pay for them"—suggesting that the Treasury nominee's 3-3-3 agenda would require new taxes on imported goods and "massive cuts to anti-poverty programs."

The Congressional Budget Office has projected that the budget deficit will represent 5.8% of the nation's GDP in 2028.

"The president-elect is stacking his cabinet with one goal in mind: more tax breaks for his billionaire boys club and major corporations."

With Bessent proposing an extension of the 2017 tax cuts—which are projected to grow the budget deficit by about $4 trillion over a decade—the elimination of Inflation Reduction Act energy investments, and a pause on nondefense discretionary spending increases, said Duke and Kogan, Bessent's plan would "actually increase the projected 2028 budget deficit from 5.8 to 6.0% of GDP, or $1 trillion above the 3% target.

Without any cuts to Medicare and Social Security—which Trump has said he would exempt from cuts—or defense spending, says the analysis, Bessent's deficit target would require both:

"The combination of policies that would deliver the deficit reduction proposed in Bessent's 3-3-3 economic plan would raise taxes on low- and middle-income families and gut healthcare, nutrition assistance, and veterans' programs while still cutting taxes for the wealthy," wrote Duke and Kogan. "Such a plan would hike families' costs both because broad-based tariffs would increase prices and because Americans would have to pay more for healthcare and food due to cuts to federal programs that help lower the cost of living."

With families across the U.S. facing "brutal cuts to health and nutrition" and higher prices at the grocery store under Bessent's plan, said Duke, the wealthiest households would still get "a net tax cut."

At The Washington Post, columnist Catherine Rampell wrote that "the magnitude of cuts required to make Bessent's arithmetic work is breathtaking."

"If you add up all the tax-cut promises Trump made during his campaign, the budget hole swells to almost $10 trillion," wrote Rampell. "To compensate, government programs would have to shrink by two-thirds. Alternatively, Trump could raise taxes on the middle class. Pick your poison."

On social media, government watchdog Accountable.US denounced Bessent's defense of Trump's tax cuts—under which "the top 1% saw benefits nearly three times larger than families in the bottom 60%"—and of the president-elect's proposed tariffs, which leading economists say would "reignite" inflation.

"Scott Bessent's nomination isn't about helping American families," said the group. "It's about lining the pockets of the ultra-wealthy and doubling down on policies that hurt the middle class."

Meanwhile, critics of Bessent on Thursday pointed to new reporting from Politico that Senate Democrats have accused the Treasury nominee of dodging $910,182 in Medicare taxes for income he made through his hedge fund from 2021-23. A memo circulated by Democrats stated that Bessent argued that as a "limited partner" in his fund, he was not liable for taxes on certain income.

Sen. Ron Wyden (D-Ore.) addressed the memo at Bessent's hearing, saying: "Like a number of Wall Street fund managers, Mr. Bessent makes use of a tricky legal maneuver to opt out of paying into Medicare."

"The billionaire hedge fund manager Trump handpicked to oversee a massive tax giveaway for the ultra-wealthy doesn't pay his own taxes," said Lindsay Owens, executive director of Groundwork Collaborative. "It's almost too on the nose. The president-elect is stacking his cabinet with one goal in mind: more tax breaks for his billionaire boys club and major corporations."

Creating a sane healthcare system will depend on building a massive common movement to free our economy from Wall Street’s wealth extraction.

The United States health care system—more costly than any on earth—will become ever more so as Wall Street increasingly extracts money from it.

Private equity funds own approximately 9% of all private hospitals and 30% of all proprietary for-profit hospitals, including 34% that serve rural populations. They’ve also bought up nursing homes and doctors’ practices and are investing more year by year. The net impact? Medical costs to the government and to patients have gone up while patients have suffered more adverse medical results, according to two current studies.

The Journal of the American Medical Association (JAMA) recently published a paper which found:

Private equity acquisition was associated with increased hospital-acquired adverse events, including falls and central line–associated bloodstream infections, along with a larger but less statistically precise increase in surgical site infections.

This should not come as a surprise. Private equity firms in general operate as follows: They raise funds from investors to purchase enterprises using as much borrowed money as possible. That debt does not fall on the private equity firm or its investors, however. Instead, all of it is placed on the books of the purchased entity. If a private equity firm borrows money and buys up a nursing home or hospital chain, the debt goes on the books of these healthcare facilities in what is called a leveraged buyout.

To service the debt, the enterprise’s management, directed by their private equity ownership, must reduce costs, and increase its cash flow. The first and easiest way to reduce costs is by reducing the number of staff and by decreasing services. Of course, the quality of care then suffers. Meanwhile, the private equity firm charges the company fees in order to secure its own profits.

With so much taxpayer money sloshing around in the system, hedge funds also are cashing in.

An even larger study of private equity and health was completed this summer and published in the British Medical Journal (BMJ). After reviewing 1,778 studies it concluded that after private equity firms purchased healthcare facilities, health outcomes deteriorated, costs to patients or payers increased, and overall quality declined.

One former executive at a private equity firm that owns an assisted-living facility near Boulder, Colorado, candidly described why the firm was refusing to hire and retain high-quality caregivers: “Their position was: We are trying to increase our profitability. Care is an ancillary part of the conversation.”

Congress passed the Medicare Advantage program in 2003. Its proponents claimed it would encourage competition and greater efficiency in the provision of health insurance for seniors. At the time, privatization was all the rage as the Democratic and Republican parties competed to please Wall Street donors. It was argued that Medicare, which was actually much more efficient than private insurance companies, needed the iron fist of profit-making to improve its services. These new private plans were permitted to compete with Medicare Part C (Medigap) supplemental insurance.

In 2007, 19% of Medicare recipients enrolled in Medicare Advantage plans. By 2023 enrollment had risen to 51%. These heavily marketed plans are attractive because many don’t charge additional monthly premiums, and they often include dental, vision, and hearing coverage, which Medicare does not. And in some plans, other perks get thrown in, like gym memberships and preloaded over-the-counter debit cards for use in pharmacies for health items.

How is it possible for Medical Advantage to do all this and still make a profit?

According to a report by the Physicians for a National Health Program, it’s very simple—they overcharge the government, that is we, the taxpayers, “by a minimum of $88 billion per year.” The report says it could be as much as $140 billion.

In addition to inflating their bills to the government, these HMO plans don’t pay doctors outside of their networks, deny or slow needed coverage to patients, and delay legitimate payments. As Dr. Kenneth Williams, CEO of Alliance HealthCare, said of Medicare Advantage plans, “They don’t want to reimburse for anything — deny, deny, deny. They are taking over Medicare and they are taking advantage of elderly patients.”

With so much taxpayer money sloshing around in the system, hedge funds also are cashing in. They have bought large quantities of stock in the healthcare companies that are milking the government through their Medicare Advantage programs. They then insist that these healthcare companies initiate stock buybacks, inflating the price of their stock and the financial return to the hedge funds. Stock buybacks are a simple way to transfer corporate money to the largest stock-sellers.

(A stock buyback is when a corporation repurchases its own stock. The stock price invariably goes up because the company’s earnings are spread over a smaller number of shares. Until they were deregulated in 1982, stock buybacks were essentially outlawed because they were considered a form of stock price manipulation.)

United Healthcare, for example, is the largest player in the Medicare Advantage market, accounting for 29% of all enrollments in 2023. It also has handsomely rewarded its hedge fund stock-sellers to the tune of $45 billion in stock buybacks since 2007, with a third of that coming since March 2020. Cigna, another big Medicare Advantage player, just announced a $10 billion stock buyback.

These repurchases are also extremely lucrative for United Healthcare’s top executives, who receive most of their compensation through stock incentives. CEO Andrew Witty, for example, hauled in $20.9 million in 2022 compensation, of which $16.4 million came from stock and stock option awards.

Those of us fighting for Medicare for All have much in common with every worker who is losing his or her job as a result of leveraged buyouts and stock buybacks.

A look at the pharmaceutical industry shows where all this is heading. Between 2012 and 2021, fourteen of the largest publicly traded pharmaceutical companies spent $747 billion on stock buybacks and dividends, more than the $660 billion they spent on research and development, according to a report by economists William Lazonick and Öner Tulum. Little wonder that drug prices are astronomically high in the U.S.

And so, the gravy train is loaded and rolling, delivering our tax dollars via Medicare Advantage reimbursements to companies like United Healthcare and Big Pharma, which pass it on to Wall Street private equity firms and hedge funds.

In researching my book, Wall Street’s War on Workers, we found that private equity firms and hedge funds are undermining the working class through leveraged buyouts and stock buybacks. When private equity moves in, mass layoffs (just like healthcare staff cuts and shortages) almost always follow so that the companies can service their debt and private equity can extract profits. When hedge funds insist on stock repurchases, mass layoffs are used to free up cash in order to buy back their shares. As a result, between 1996 and today, we estimate that more than 30 million workers have gone through mass layoffs.

Meanwhile, stock buybacks have metastasized throughout the economy. In 1982, before deregulation, only about 2% of all corporate profits went to stock buybacks. Today, it is nearly 70%.

Those of us fighting for Medicare for All, therefore, have much in common with every worker who is losing his or her job as a result of leveraged buyouts and stock buybacks. Every fight to stop a mass layoff is a fight against the same Wall Street forces that are attacking Medicare and trying to privatize it. Creating a sane healthcare system, therefore, will depend on building a massive common movement to free our economy from Wall Street’s wealth extraction.

To take the wind out of Medicare Advantage and Wall Street’s rapacious sail through our healthcare system, we don’t need more studies. It’s time to outlaw leveraged buyouts and stock buybacks.

Stock buybacks have become the main goal in life for corporate executives and activist stock sellers. And this sickness is spreading.

The institution casting a broad shadow over the UAW strike against the Big Three automakers is Wall Street. GM workers and those of us who have longed for the production of high-quality and affordable electric cars to combat global warming could not have invented a more damning story than the reality of how the financiers fleeced us.

The story starts back in 2008, when the auto industry was going bankrupt due to the financial crisis that Wall Street’s reckless gambling had caused. Six million workers lost their jobs in six months through no fault of their own. Motor vehicle sales fell by nearly 40 percent and as bankruptcies loomed, another three million more auto industry jobs were at risk.

The federal government intervened with a massive bailout, eventually loaning the companies more than $81 billion. To reorganize the industry, the government wanted more financial expertise. So where did it turn? To Wall Street! The financial foxes were hired to overhaul the hen house.

The UAW strike is illuminating a type of financial insanity that has gripped our economy.

To lead 1990s Presidential Task Force on the Auto Industry, the Obama administration recruited Steve Rattner, a Wall Street investment banker, whose net worth was $188 million. (A year later, we learned a bit how Rattner became so wealthy. He was charged by the Security and Exchange Commission in a pay-to-play scheme to obtain investments from New York’s largest pension fund and was forced to pay a $10 million fine.)

Rattner, dubbed the Car Czar by the media, recruited a 37-year-old Wall Street “turn around” expert, Harry J. Wilson, to guide GM to solvency. Wilson joined the federal task force, he claimed, out of a lofty sense of noblesse oblige. As he wrote to Rattner, “I have a very deep interest in public service, particularly given the good fortune I have enjoyed in my own life…” Wilson’s good fortune continued to follow him to GM. At taxpayer expense he would learn everything there was to learn about GM and then use it to fleece the company a few years later.

The bailout’s net cost to US taxpayers was $11. 2 billion, while autoworkers absorbed $11 billion in reduced labor costs. In exchange for the survival of their jobs, workers were saddled with a bitter decade-long wage freeze, the elimination of long-held cost-of-living adjustments, and reduced wages and benefits for new hires. This led to a 19.3 percent loss of real wages (after accounting for inflation) from 2008 to 2022). The UAW’s current request for a sizable wage increase is to make up for more than a decade of lost ground.

From a financial perspective, the bailout was a success. GM, after losing $38.5 billion in 2008-09, earned $16.7 billion in 2010. By 2014, GM had $29.5 billion in cash on hand, a tidy sum with which to enter the budding competitive race against new firms like Tesla to produce affordable electric vehicles.

But from Harry J. Wilson’s perspective, the GM hen house had far too many eggs. After returning to Wall Street from public service, he set his sights on GM’s cash.

First, Wilson purchased 30,000 GM shares worth about $1.1 million at the time. His goal was to press GM to conduct a stock buyback as soon as possible. (A stock buyback in effect moves cash from the corporation to stock-sellers. By reducing the number of outstanding shares, it drives up the price of each share so that Harry and other large financial entities can cash out quickly and with sizable profits.)

He then cut a deal with billionaire David Tepper, whose Appaloosa hedge fund owned $300 million in GM stock. Wilson also worked out arrangements with several other hedge funds, including Taconic Capital, which owned another $120 million worth of GM shares. In each arrangement, Wilson would receive a performance fee and a share of the profits should he succeed in forcing a GM stock buyback. The hedge fund group also agreed to cover up to $1 million of expenses incurred by Wilson over the next year.

Wilson then pushed GM to commit to an $8 billion stock buyback. When GM announced buybacks shortly thereafter Wilson and his Wall Street backers did even better than expected. GM went on to announce a $5 billion in buybacks in March 2015, another $4 billion later that year, and another $5 billion in 2017.

The business of American business is to create stock buybacks for top executives and for looting investors.

So, while Tesla was straining to sell 50,000 electric cars in 2015, GM was busily opening up a new ultra-luxury production line of stock buybacks that enriched Harry J Wilson and his Wall Street compatriots, and GM executives who were compensated with stock incentives. In the last 12 years, GM has spent $21 billion on stock buybacks rather than additional investments in greener vehicles. Not coincidently, in 2022 GM sold 39,096 electric cars, while Tesla produced 32 times more ( 1.31 million).

GM CEO Mary Barra has reaped an average of $41.8 million a year for the past four years in total compensation. “My compensation,” she said, “92 percent of it is based on the performance of the company,” She means that 92 percent of her income comes from stock incentives. The “performance of the company” is measured for compensation purposes by its stock price, which she is able to manipulate and raise through stock buybacks. The more GM engages in stock buybacks the higher the price of their shares, and therefore, the higher the pay of those executives who are paid with stock incentives tied to the price of the stock.

The strike is shining a bright light on a type of financial insanity that has gripped our economy. Stock buybacks have become the main goal in life for corporate executives and activist stock-sellers like Harry J. Wilson and his hedge fund raiders. Their looting adds nothing of value to their companies, yet this sickness is spreading. In 1982 only 2 percent of corporate profits were used for stock buybacks. Now, nearly 70 percent of all corporate profits go to stock buybacks instead of research and development, environmental controls, and worker health and safety. And certainly not to provide job security nor livable wages. Increasingly the business of American business is not to make things and provide services, but instead to create stock buybacks to benefit top executives and looting stock-sellers.

Hopefully, the UAW strike will move us one step closer to outlawing any and all stock buybacks.

The only win if Canadian Pacific acquires Kansas City Southern is for freight rail's hedge fund investors, who are squeezing operating cash out of these railroads at the expense of workers, community safety, and the overall economy.

On March 15th, the Surface Transportation Board (STB)—the federal agency that regulates the U.S. freight rail industry—gave final approval to the acquisition of Kansas City Southern by Canadian Pacific. Approving this merger between America's sixth- and seventh-largest railroads was a dire mistake, which will have enormous economic and social costs that resound for decades.

In a nation committed to a competitive market, in a sector that's already as consolidated as American freight rail, it's important to evaluate mergers very carefully, because once big companies absorb smaller ones, it becomes impossible to pull them apart again. And as economics researcher Eric Peinert of the American Economic Liberties Project puts it, "Nothing in the history of rail consolidation suggests this particular merger is a good idea."

Allowing these two railroads to merge is likely to reduce competition in the industry, leading to higher shipping prices, reduced service, and job cuts. It will impair the ability of small businesses to operate. It will lead to increased safety risks and have environmental impacts on the communities where rail traffic will increase. And as cost-cutting pressure from railroads' predatory hedge fund investors continues to mount, it will likely contribute to even more aggressive cuts in service than we have seen over the past five years.

The STB knew all that. They got 2,000 public comments about the merger, from industry experts, researchers, lawmakers, and the general public—hundreds of them laying out reasons why it shouldn't get the green light. On behalf of people across America, U.S. Senators and Representatives weighed in with their concerns, which the STB ignored.

"Cost-cutting demanded by the industry's hedge-fund investors—while generating a cash windfall for them personally—has resulted in safety compromises that risk the lives of employees and the well-being of the densely settled communities freight railroads pass through..."

The most obvious risks are to the competitive marketplace, with both rail customers and rail workers paying the biggest price. Sen. Elizabeth Warren (D-Mass.) called for the merger application to be denied outright on antimonopoly grounds. As Rep. Katie Porter (D-Calif.) put it, as America's Class I freight railroads have dwindled from 33 to just seven, "lack of competition has allowed railroads to gut capacity, capture and extort businesses, fire thousands of workers, and threaten the integrity of America's freight transport network and supply chains – all while extracting monopoly profits."

For American businesses, precision scheduled railroading (PSR), the approach these giant railroads are taking to providing as little service as they can get away with and doing it as cheaply as possible, has meant less frequent, less reliable, and more expensive shipping options. And for the freight rail workforce, it's meant job cuts of 28% across the industry with onerous contract terms and more dangerous working conditions for those who remain.

In the wake of the hazardous Norfolk Southern derailment at East Palestine, Ohio and a string of other high-profile derailments earlier this year, industry-watchers of all stripes have noted that cost-cutting demanded by the industry's hedge-fund investors—while generating a cash windfall for them personally—has resulted in safety compromises that risk the lives of employees and the well-being of the densely settled communities freight railroads pass through, like the Chicago suburbs.

According to employees, extreme schedule pressures under PSR push workers to their physical limits, leaving them with as little as 60 seconds to conduct railcar safety inspections. And due to investor pressure to save money by running fewer, longer trains, it's more and more frequent to see trains as long (150 cars) as the one that derailed in Ohio. Sarah Feinberg, former head of the Federal Railroad Administration (FRA), says that even trains as short as 80 cars can pose size risks.

The American Economic Liberties Project describes the hyper-consolidated U.S. freight rail giants as operating under a "financially extractive business model," which makes but money for the railroads' hedge fund investors at great cost to the public welfare. And Peinert says yet another merger will make things even worse. "This deal sets the stage for future disasters like East Palestine, and will likely lead to even further railroad staffing cuts, even higher cargo loads, and other profit-driven safety shortcuts."

Despite the recent statement by STB chair Martin Oberman that this merger "will be an improvement for all citizens in terms of safety and the environment," their own environmental impact study found that the opposite would be the case in numerous communities along busy rail routes: the merger will increase hazardous cargo transportation along 141 of the 178 rail segments, totaling 5,800 miles of track in 16 states. And even basic public services like Metra passenger rail service—a critical economic engine for the 10-million-population three-state Chicago metro area, which operates on Canadian Pacific tracks, competing with freight services—are at risk. Along some of those track segments, freight traffic is projected to triple, with much of the new cargo slated to include hazardous materials.

In response to the market consolidation concerns raised by merger opponents, the STB has imposed some conditions. They will require that interchanges within other railroads be kept open, that a process be provided for challenging rate increases, and that the companies provide data so the STB can monitor compliance. But as Sen. Warren noted, these measures are insufficient. That's especially true given that there's already evidence that Canadian Pacific and Kansas City Southern may have been violating antitrust law against collusion, by sitting down together at a luxury hotel in Florida to plan the future of the company in early February, even before the merger was approved.

Cutting routes, service, and workers may be good for profits, but it's bad for American competitiveness, for workers, for industry, and for public safety and quality of life. The only win here is for freight rail's hedge fund investors, who are squeezing operating cash out of these railroads—cash they used to use to pay employees, fund service, and finance safety improvements—and taking it to the bank.

Puerto Rico says it will default on its debt on Monday, escalating the economic crisis on the island that sees no sign of stopping in the face of exploitative hedge funds.

The commonwealth is expected to miss its upcoming $422 million bond payment for its Government Development Bank. The default comes after U.S. Congress failed to act to help the island territory last week, in a decision that followed a concerted lobbying push by hedge funds angling to profit off its debt crisis.

As the International Business Times reports:

Over the last few years, hedge funds and mutual funds have bought up large tranches of Puerto Rico's bonds at cut-rate prices, hoping the island will pay back its debts in full, thereby giving those financial interests a big payout. That gamble, however, has relied in part on the bet that the island will make draconian cuts to social services and worker pensions and use the savings to pay back 100 cents on the dollar to its Wall Street creditors -- a bet, in other words, that Congress will prevent the island from simply erasing some of its debt through the kind of bankruptcy protections that are afforded U.S. cities.

To that end, federal lobbying records show that major banks, bond insurers and hedge funds spent millions last year to try to shape bankruptcy proposals for the island. Two so-called dark money groups linked to the billionaire Koch brothers and Republican strategist Karl Rove are also working to influence the debate over Puerto Rico's debt.

"Faced with the inability to meet the demands of our creditors and the needs of our people, I had to make a choice," Puerto Rico Governor Alejandro Garcia Padilla said during a televised speech on Sunday. "I decided that essential services for the 3.5 million American citizens in Puerto Rico came first."

The Sunlight Foundation reported earlier this month that one of the dark-money groups behind the lobbying push, the Center for Individual Freedom (CFIF), purchased at least $200,000 in ads around Washington, D.C., to influence lawmakers away from passing legislation that would ease the island's debt burden. The Koch-backed American Future Fund also placed ads with Politico and the Wall Street Journal that attacked Garcia Padilla.

Congress continued to drag its feet on legislation that could have eased some of Puerto Rico's debt burden despite efforts by economic justice groups like Jubilee USA, which organized a call-in day of action urging constituents to ask their representatives in the House to pass the Puerto Rico Oversight, Management, and Economic Stability Act (PROMESA), which would have allowed the commonwealth to restructure its debt.

"There are no budget cuts or tax hikes that can solve this crisis," said Jubilee USA executive director Eric LeCompte. "Debt restructuring is a necessity before we can see any economic growth."

The $422 million is only a small chunk of the island's $70 billion debt burden. Its human impact has been enormous, fueling a poverty rate of nearly 45 percent, tens of thousands of public employee layoffs, tax hikes, and widespread school closures. As a result, Puerto Rico is seeing its largest exodus in 50 years, its population dropping nine percent from 2000 to 2015.

Puerto Rico's next payment is due in July. As LeCompte said on Monday, "Congress could have prevented the May default. With even greater consequences around a July default, Congress needs to act quickly."

"Puerto Rico needs to bring its debt back to payable levels," he said. "Any solution must respect the rights of the creditors, Puerto Rico's government and the needs of the island's people. We remain concerned how this fiscal crisis is impacting the poor and vulnerable. 57 percent of Puerto Rico's kids live in poverty. The most important cost to be concerned about is the human cost of this crisis."

For more than 80 days, about 35 parents and children have been camping out in front of their neighborhood school in the U.S. Territory of Puerto Rico.

The Commonwealth government closed the Jose Melendez de Manati school along with more than 150 others over the last 5 years.

But the community is refusing to let them loot it.

They hope to force lawmakers to reopen the facility.

Department of Education officials have been repeatedly turned away by protesters holding placards with slogans like "This is my school and I want to defend it," and "There is no triumph without struggle, there is no struggle without sacrifice!"

Officials haven't even been able to shut off the water or electricity or even set foot inside the building.

The teachers union - the Federacion de Maestros de Puerto Rico (FMPR) - has called for a mass demonstration of parents, students and teachers on Sunday, Aug. 23. Protesters in the capital of San Juan will begin a march at 1 p.m. from Plaza Colon to La Fortaleza (the Governor's residence).

The Jose Melendez de Manati school, for instance, served students 92% of whom live in poverty.

Now that the building has been closed, parents say they can't afford the cost to transport their children to a new school miles away. And those schools that remain open have been forced to make drastic cuts to remain functional. Class sizes have ballooned to 35 students or more. Amenities like arts, music, health and physical education have typically been slashed.

Why?

The island territory is besieged by vulture capitalists encouraging damaging rewrites to the tax code while buying and selling Puerto Rican debt.

Hundreds of American private equity moguls and entrepreneurs are using the Commonwealth as a tax haven.

Since 2012, U.S. citizens who live on the island for at least 183 days a year pay minimal or no taxes, and unlike those living in Singapore or Bermuda, they get to keep their U.S. passports. After all, they're still living in the territorial U.S. These individuals pay no local or federal capital gains taxes and no local taxes on dividend interest for 20 years. Even someone working for a mainland company who resides on the island is exempt from paying U.S. federal taxes on his salary.

Worldwide, American companies keep 60 percent of their cash overseas and untaxed. That's about $1.7 trillion annually.

Microsoft, for instance, routes its domestic operations through Puerto Rican holdings to reduce taxes on its profits to 1.02 percent - a huge savings from the U.S. corporate tax rate of 35 percent! Over three years, Microsoft saved $4.5 billion in taxes on goods sold in the U.S. alone. That's a savings of $4 million a day!

Meanwhile, these corporate tax savings equal much less revenue for government entities - both inside and outside of Puerto Rico - to use for public goods such as schooling.

Public schools get their funding from tax revenues. Less tax money means less money to pay for children's educations. As the Puerto Rican government borrowed in an attempt to shore up budget deficits, the economy tanked.

But have no fear! In swooped Hedge Funds to buy up that debt and sell it for a profit.

When this still wasn't enough to prop up a system suffering from years of neglect, the Hedge Fund managers demanded more school closures, firing more teachers, etc.

Of course, this is only one interpretation of events.

If you ask Wall Street moguls, they'll blame the situation on declining student enrollment. And they have a point.

Some 450,000 people have left the island in the last decade as the economy suffered an 8-year depression.

There were 423,000 students in the Puerto Rican school system in 2013. That's expected to drop to 317,000 by 2020.

But is this the cause of the island's problems or a symptom?

Unfortunately, things look to get much worse before they'll get any better.

The government warns it may be out of money to pay its bills by as early as 2016. Over the next five years, it may have to close nearly 600 more schools - almost half of the remaining facilities!

Right on cue, Senate President Eduardo Bhatia is proposing corporate education reform methods to justify these draconian measures. This includes privatizing the school system, tying teacher evaluations to standardized test scores and increasing test-based accountability.

"Our interest is to promote transparency and flow of data through the implementation of a standardized measurement and accountability system for all agencies," Bhatia said, adding that the methodology has been successful in such cities as Chicago.

Despite such overwhelming opposition, protesters are taking the fight to the capitol. "Tax the Rich!" is a popular slogan on signs for Sunday's march.

"The foreign companies that pay no taxes or a less amount to evade paying their due in contributions - impose a tax on them now!"

This is just a beginning, she adds. Stronger actions will be coming.

In the meantime, those brave parents and children still refuse to give up their shuttered school.

They dream of a day when that empty building once again rings with the laughter of students and the instruction of teachers.

In a country being used by the wealthy to increase their already swollen bank statements, is that really so much to ask?

You can show your solidarity with these Puerto Rican protestors by spreading the word through social media. Post a picture of yourself with a sign saying you're with them in their fight. Tweet the Commonwealth Secretary of Education @Rafaelroman6. Use the hashtags #EducacionEnPR #SOSdocente.