SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"Americans understand we're living in a rigged economy," said Sen. Bernie Sanders. "Together, we can and must change that."

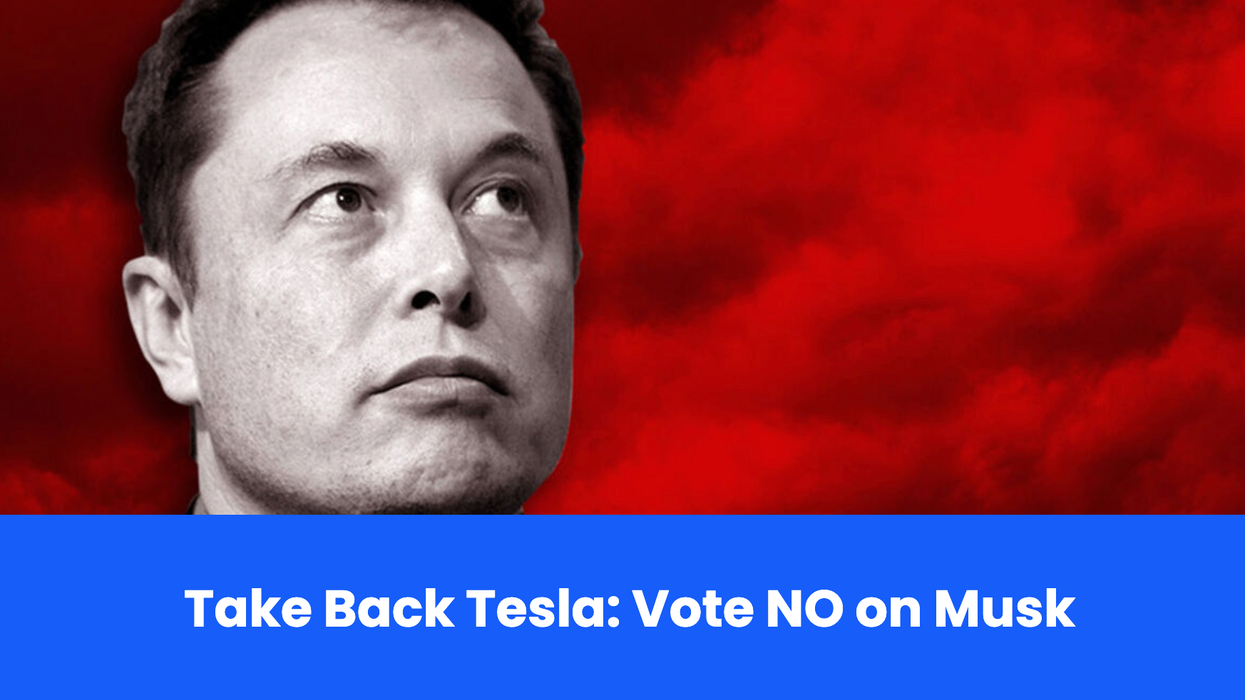

Elon Musk is the world's richest person, with an estimated net worth of nearly $500 billion, but the Tesla CEO could become the world's first trillionaire, thanks to a controversial pay package approved Thursday by the electric vehicle company's shareholders.

Ahead of the vote, a coalition of labor unions and progressive advocacy groups launched the "Take Back Tesla" campaign, urging shareholders to reject the package for its CEO, who spent much of this year spearheading President Donald Trump's so-called Department of Government Efficiency (DOGE), which prompted nationwide protests targeting the company.

Musk's nearly $1 trillion package would be the biggest corporate compensation plan in history if he gets the full amount by boosting share value "eightfold over the next decade" and staying at Tesla for at least that long. It was approved at the company's annual meeting after the billionaire's previous payout, worth $56 billion, was invalidated by a judge.

The approval vote sparked another wave of intense criticism from progressive groups and politicians who opposed it—including on Musk's own social media platform, X.

"Musk, who spent $270 million to get Trump elected, is now in line to become a trillionaire," Sen. Bernie Sanders (I-Vt.) wrote on X. "Meanwhile, 60% of our people are living paycheck to paycheck. Americans understand we're living in a rigged economy. Together, we can and must change that."

The vote came during the longest-ever federal government shutdown, which has sparked court battles over the Supplemental Nutrition Assistance Program. A judge on Thursday ordered the full funding of 42 million low-income Americans' November SNAP benefits, but it is not yet clear whether the Trump administration will comply.

The Sunrise Movement, a youth-led climate group, noted the uncertainty over federal food aid in response to the Tesla vote, saying: "Meanwhile, millions of kids are losing SNAP benefits and healthcare because of Musk's allies in DC. In a country rich enough to have trillionaires, there's no excuse for letting kids go hungry."

Robert Reich, a former labor secretary who's now a professor at the University of California, Berkeley, said: "Remember: Wealth cannot be separated from power. We've seen how the extreme concentration of wealth is distorting our politics, rigging our markets, and granting unprecedented power to a handful of billionaires. Be warned."

In remarks to the Washington Post, another professor warned that other companies could soon follow suit:

Rohan Williamson, professor of finance at Georgetown University, said Musk's argument for commanding such a vast paycheck is largely unique to Tesla—though similar deals may become more prevalent in an age of founder-led startups.

"No matter how you slice it, it's a lot," Williamson said. But the deal seeks to emphasize Musk’s central—even singular—role in the company's rise, and its fate going forward.

"I drove this to where it is and without me it's going to fail," Williamson said, summarizing Musk's argument.

"No CEO is 'worth' $1 trillion. Full stop," the advocacy group Patriotic Millionaires argued Wednesday, ahead of the vote. "We need legislative solutions like the Tax Excessive CEO Pay Act, which would raise taxes on corporations that pay their executives more than 50 times the wages of their workers."

The world's richest man "has wiped billions off of Tesla's share value, trashed the company's reputation, and driven millions of its customers away," one campaigner said, urging shareholders to reject his pay plan.

A coalition of labor unions and progressive advocacy organizations on Tuesday launched the "Take Back Tesla" campaign, urging shareholders of the electric vehicle giant to reject a pay package that could make CEO Elon Musk the world's first trillionaire.

Musk is already the richest person on the planet, with an estimated net worth of $458-485.9 billion as of Wednesday. His previous 10-year proposal, worth $56 billion, was invalidated by a judge. He's now on an interim plan that has not been approved by shareholders, who are set to vote on the $1 trillion package at the company's annual meeting next month.

Tesla's board unveiled the proposed $1 trillion plan—which would be the biggest corporate compensation package in history—last month. Musk would get the full amount if he boosted share value "eightfold over the next decade" and stayed at Tesla for at least that long. He would own 29% of the company, one of several in which he holds a leadership position.

Top unions, such as the American Federation of Teachers (AFT) and Communications Workers of America (CWA), joined groups including Americans for Financial Reform, Ekō, People's Action Institute, Public Citizen, and Stop the Money Pipeline for the new campaign against "Musk's money grab." As part of it, they launched the website TakeBackTesla.com.

"How shareholders vote on Musk's trillion-dollar pay package and other important Tesla ballot items will likely set the stage for similar attempts by other oligarchs to consolidate their own power."

Several coalition leaders pointed to Musk's recent efforts to get President Donald Trump elected and then help the Republican gut the federal government—which has been shut down for 22 days due to a congressional funding fight—via their so-called Department of Government Efficiency. The billionaire's DOGE activities provoked nationwide protests targeting Tesla.

"In the last 12 months, Elon Musk's attempts to destroy the American government have caused huge damage to the Tesla brand and contributed to a significant decline in the company's sales in multiple key markets," Stop the Money Pipeline's Alex Connon noted, urging shareholders to "reject this insane proposal."

AFT president Randi Weingarten said that "the Tesla board, instead of upholding basic governance standards, wants to green-light an outrageous $1 trillion pay package for a CEO who has spent most of the year engaged in childish political brawls, rather than working to create shareholder value."

"To reward this destructive behavior with an obscene salary is a slap in the face—not only to the federal workers he's fired, but to the retirees whose pensions are invested in Tesla stock," she declared.

Dubbing the proposal "Musk's corporate heist," CWA president Claude Cummings Jr. similarly stressed that "Elon Musk is enriching himself by stealing from the American worker—from our infrastructure dollars for rural broadband to workers' private data from the Department of Labor—and now he wants to steal $1 trillion from our pensions and retirement accounts."

Natalia Renta, Americans for Financial Reform's associate director of corporate governance and power, emphasized that the vote is bigger than Musk. She said that "how shareholders vote on Musk's trillion-dollar pay package and other important Tesla ballot items will likely set the stage for similar attempts by other oligarchs to consolidate their own power."

"This new website allows people to get their voices heard by sending letters to their state financial officer and mutual fund manager (if they have one)," Renta added. State treasurers of Connecticut, Nevada, and New Mexico have already joined mounting calls for shareholders to vote down Musk's compensation package.

Ekō executive director Emma Ruby-Sachs argued that "no CEO is worth a trillion-dollar pay package, but especially not Elon Musk, who has wiped billions off of Tesla's share value, trashed the company's reputation, and driven millions of its customers away. Tesla's shareholders need to show the judgment Musk so clearly lacks, and reject this pay deal."

But there's a solution: The recently introduced Tax Excessive CEO Pay Act would base the CEO-worker pay ratio on five-year averages of the total compensation for a firm’s highest-paid executive and median worker.

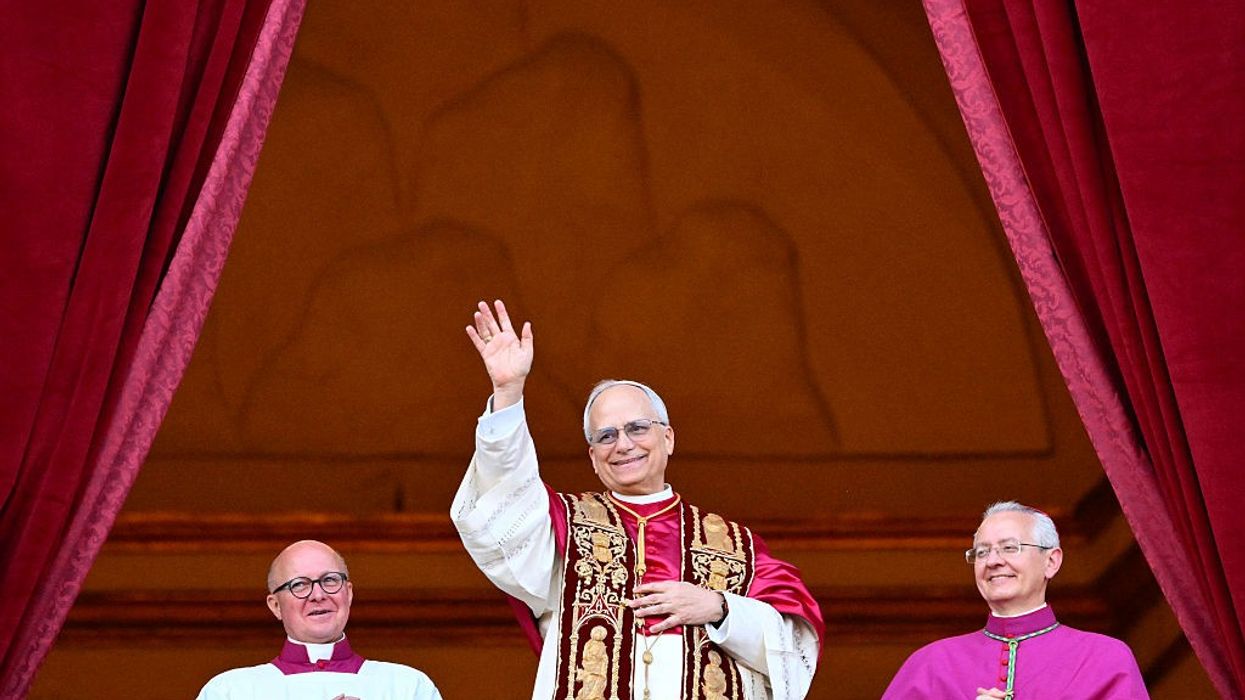

In his first interview since becoming the leader of the Catholic Church, Pope Leo XIV fielded a question about the polarization that is tearing societies apart around the world.

A significant factor, he said, is the “continuously wider gap between the income levels of the working class and the money that the wealthiest receive.”

Pope Leo appears to be particularly baffled by the Tesla pay package that could turn Elon Musk into the world’s first trillionaire.

“What does that mean and what’s that about?” the Pope asked. “If that is the only thing that has value anymore, then we’re in big trouble.”

We are indeed in big trouble. But we are not without solutions.

Sen. Bernie Sanders (I-Vt.) and Rep. Rashida Tlaib (D-Mich.) are spearheading an effort behind one particularly promising solution: hefty tax hikes on companies with huge gaps between their CEO and median worker pay.

Their recently introduced Tax Excessive CEO Pay Act would base the CEO-worker pay ratio on five-year averages of the total compensation for a firm’s highest-paid executive and median worker. The tax increases would start at 0.5 percentage points on companies with gaps of 50 to 1 and top out at five percentage points on firms that pay their CEO more than 500 times median worker pay.

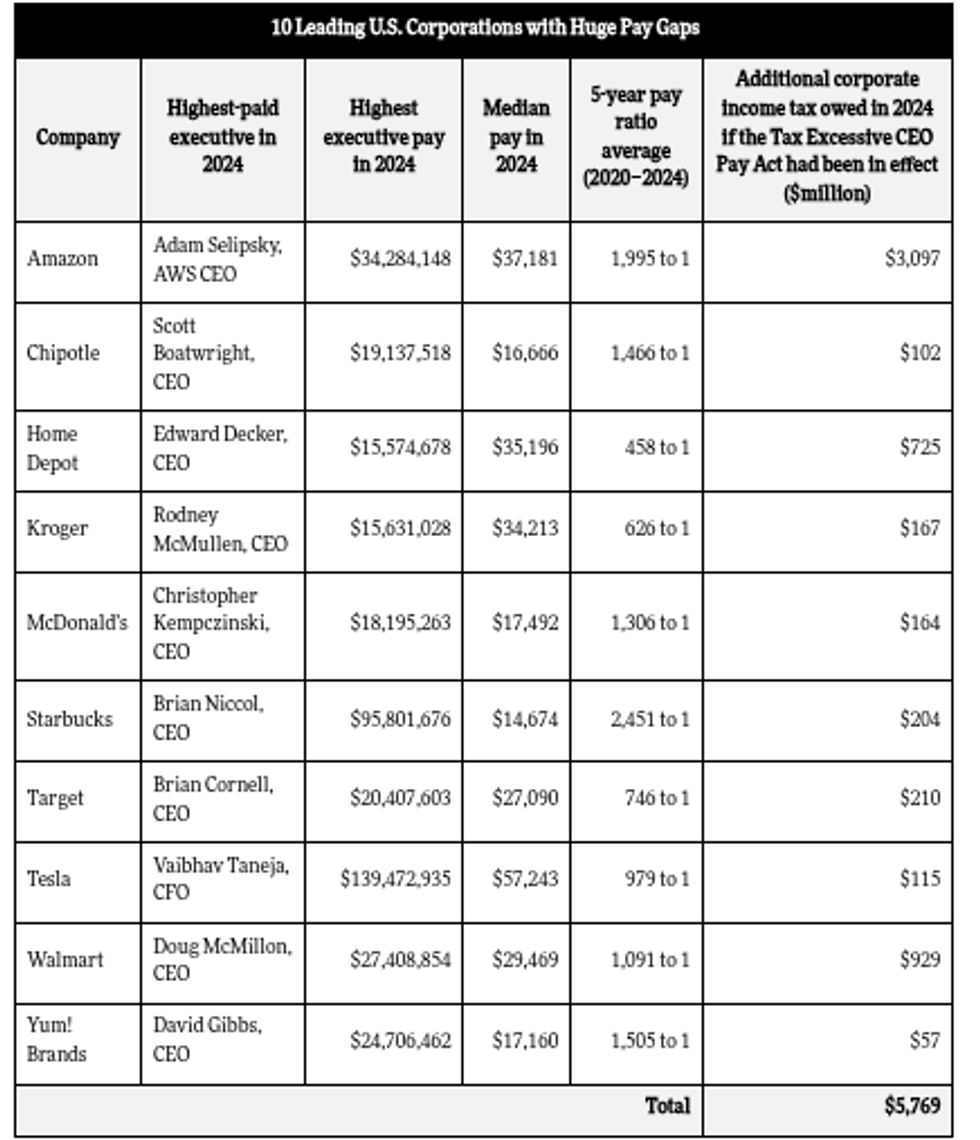

How much might specific companies owe under the bill if they refuse to narrow their gaps? At the Institute for Policy Studies, we ran the numbers on 10 leading US corporations with large pay ratios. We found, for example, that Walmart, with a five-year average pay gap of 1,091 to 1, would have owed as much as $929 million in extra federal taxes in 2024 if this legislation had been in effect.

Amazon, with an even wider gap of 1,995 to 1 and higher profits, would’ve owed as much as an additional $3.1 billion last year.

Source: Institute for Policy Studies analysis of compensation data in proxy statements and US pre-tax income figures from 10-K filings.

Source: Institute for Policy Studies analysis of compensation data in proxy statements and US pre-tax income figures from 10-K filings.

Home Depot would have owed as much as $725 million more in 2024 taxes under this legislation. Like most of these companies, the home improvement giant can’t claim to be short on cash. Over the past six years, they’ve blown nearly $38 billion on stock buybacks, a maneuver that artificially inflates a CEO’s stock-based pay. With the money the firm spent on stock buybacks, Home Depot could’ve given every one of their 470,100 employees six annual $13,423 bonuses.

Sen. Sanders pointed out that if Elon Musk receives the full $975 billion compensation package that Tesla’s board has proposed, Tesla could owe up to $100 billion more in taxes over the next decade under this legislation.

“The Pope is exactly right,” wrote Sanders in a social media post. “No society can survive when one man becomes a trillionaire while the vast majority struggle to just survive—trying to put food on the table, pay rent, and afford healthcare. We can and must do better.”

“Working people are sick and tired of corporate greed,” Rep. Tlaib added in a press release. “It’s disgraceful that corporations continue to rake in record profits by exploiting the labor of their workers. Every worker deserves a living wage and human dignity on the job.”

Additional original co-sponsors of the Tax Excessive CEO Pay Act include: Sens. Elizabeth Warren (D-Mass.), Chris Van Hollen (D-Md.), Peter Welch (D-Vt.), Ed Markey (D-Mass.), and 22 members of the House of Representatives.

Polling suggests that Americans across the political spectrum would support the bill. One 2024 survey, for instance, found that 80% of likely voters favor a tax hike on corporations that pay their CEOs more than 50 times more than what they pay their median employees. Large majorities in every political group gave the idea the thumbs up, including 89% of Democrats, 77% of Independents, and 71% of Republicans.

In these hyperpolarized times, Americans of diverse backgrounds, faiths, and political perspectives seem to share enormous common ground on at least one problem facing our nation: the extreme economic divides within our country’s largest corporations.

"At a time of record-breaking income and wealth inequality, we must demand that the wealthiest people and most profitable corporations in America finally pay their fair share of taxes," said Sen. Bernie Sanders.

With the world's richest person, Tesla CEO and Republican megadonor Elon Musk, on the cusp of becoming the first trillionaire on the planet, two leading progressive lawmakers are calling on Congress to pass a bill to "rein in the obscene salaries of America's top executives."

Sen. Bernie Sanders (I-Vt.) and Rep. Rashida Tlaib (D-Mich.) on Monday introduced the Tax Excessive CEO Pay Act with the aim of raising taxes on companies that pay their executives more than 50 times their workers' wages.

The legislation would impose penalties starting at 0.5 percentage points for companies with CEO-to-worker pay ratios between 50-to-1 and 100-to-1. Firms where executives make more than 500 times their workers' pay would be forced to pay the highest rate.

The bill would also require the US Treasury Department to crack down on tax avoidance, including schemes that disguise pay disparities by outsourcing jobs to contractors.

Sanders said that exorbitant CEO pay and massive pay gaps at corporations are intolerable "while 60% of Americans live paycheck to paycheck and millions work longer hours for lower wages."

"It is unacceptable that the CEOs of the largest low-wage corporations make more than 630 times what their average workers make," said the senator, who has been criss-crossing the country this year with his Fighting Oligarchy Tour, galvanizing people in red and blue districts against wealth inequality, political corruption, and corporate power.

"This is not only morally obscene, but also insane economic policy," said Sanders. "At a time of record-breaking income and wealth inequality, we must demand that the wealthiest people and most profitable corporations in America finally pay their fair share of taxes and treat all employees with the respect and dignity they deserve. That’s precisely what this legislation begins to do."

The proposal would raise an estimated $150 billion over a decade if tech giants, Wall Street firms, and other large corporations continue their current compensation patterns, and Sanders and Tlaib noted that the largest companies in the US would have paid billions of dollars more in taxes last year had the legislation been in effect.

JPMorgan Chase would have paid $2.38 billion in taxes, while Google would have paid $2.16 billion and Walmart would have paid $929 million.

With 62% of Republican voters and 75% of Democrats supporting a cap on CEO pay relative to worker salaries, the legislation would likely be well received by Americans across the political spectrum—but Republican lawmakers have shown little to no interest in confronting the pay gap, ensuring fair wages for workers, or reining in excessive executive compensation.

With the current CEO-employee pay gap, CEOs at the 350 largest publicly owned firms make 290 times more than the average pay of a typical worker at their companies, with the gap much larger at some corporations.

The median Walmart worker made $29,469 in 2024, while CEO Doug McMillon took home $27.4 million—a 930-to-1 gap.

The median Starbucks worker would have to work for more than 6,000 years to earn the pay CEO Brian Niccol took home in 2024.

"Working people are sick and tired of corporate greed," said Tlaib. “It’s disgraceful that corporations continue to rake in record profits by exploiting the labor of their workers. Every worker deserves a living wage and human dignity on the job."

"It’s time," she added, "to make the rich pay their fair share.”

Tlaib and Sanders introduced the legislation as Pope Leo spoke out against exorbitant CEO pay in his first interview since taking the helm of the Catholic Church, reserving particular condemnation for Musk, for whom the Tesla board proposed a $1 trillion pay package if he grows the company by eightfold over the next decade.

“CEOs that 60 years ago might have been making four to six times more than what the workers are receiving... it’s [now] 600 times more than the average workers are receiving,” the pope told the Catholic outlet Crux.

“Yesterday, the news that Elon Musk is going to be the first trillionaire in the world: What does that mean and what’s that about?" he added. "If that is the only thing that has value anymore, then we’re in big trouble.”

Sanders said Monday that the pope "is exactly right."

"No society can survive when one man becomes a trillionaire while the vast majority struggle to just survive—trying to put food on the table, pay rent, and afford healthcare," said Sanders. "We can and must do better."

The report found that seven of America's biggest healthcare companies have collectively dodged $34 billion in taxes as a result of Trump's 2017 tax law while making patient care worse.

President Donald Trump's tax policies have allowed the healthcare industry to rake in "sick profits" by avoiding tens of billions of dollars in taxes and lowering the quality of care for patients, according to a report out Wednesday.

The report, by the advocacy groups Americans for Tax Fairness and Community Catalyst, found that "seven of America's biggest healthcare corporations have dodged over $34 billion in collective taxes since the enactment of the 2017 Trump-GOP tax law that Republicans recently succeeded in extending."

The study examined four health insurance companies—Centene, Cigna, Elevance (formerly Anthem), and Humana; two for-profit hospital chains—HCA Holdings and Universal Health Services; and the CVS Healthcare pharmacy conglomerate.

It found that these companies' average profits increased by 75%, from around $21 billion before the tax bill to about $35 billion afterward, and yet their federal tax rate was about the same.

This was primarily due to the 2017 law's slashing of the corporate tax rate from 35% to 21%, a change that was cheered on by the healthcare industry and continued with this year's GOP tax legislation. The legislation also loosened many tax loopholes and made it easier to move profits to offshore tax shelters.

The report found that Cigna, for instance, saved an estimated $181 million in taxes on the $2.5 billion it held in offshore accounts before the law took effect.

The law's supporters, including those in the healthcare industry, argued that lowering corporate taxes would allow companies to increase wages and provide better services to patients. But the report found that "healthcare corporations failed to use their tax savings to lower costs for customers or meaningfully boost worker pay."

Instead, they used those windfalls primarily to increase shareholder payouts through stock buybacks and dividends and to give fat bonuses to their top executives.

Stock buybacks increased by 42% after the law passed, with Centene purchasing an astonishing average of 20 times more of its own shares in the years following its enactment than in the years before. During the first seven years of the law, dividends for shareholders increased by 133% to an average of $5.6 billion.

Pay for the seven companies' half-dozen top executives increased by a combined $100 million, 42%, on average. This is compared to the $14,000 pay increase that the average employee at these companies received over the same period, which is a much more modest increase of 24%.

And contrary to claims that lower taxes would allow companies to improve coverage or patient care, the opposite has occurred.

While data is scarce, the rate of denied insurance claims is believed to have risen since the law went into effect.

The four major insurers' Medicare Advantage plans were found to frequently deny claims improperly. In the case of Centene, 93% of its denials for prior authorizations were overturned once patients appealed them, which indicates that they may have been improper. The others were not much better: 86% of Cigna's denials were overturned, along with 71% for Elevance/Anthem, and 65% for Humana.

The report said that such high rates of denials being overturned raise "questions about whether Medicare Advantage plans are complying with their coverage obligations or just reflexively saying 'no' in the hopes there will be no appeal."

Salespeople for the Cigna-owned company EviCore, which insurers hire to review claims, have even boasted that they help companies reduce their costs by increasing denials by 15%, part of a model that ProPublica has called the "denials for dollars business." Their investigation in 2024 found that insurers have used EviCore to evaluate whether to pay for coverage for over 100 million people.

And while paying tens of millions to their executives, both HCA and Universal Health Services—which each saved around $5.5 billion from Trump's tax law—have been repeatedly accused of overbilling patients while treating them in horrendous conditions.

"Congress should demand both more in tax revenue and better patient care from these highly profitable corporations," Americans for Tax Fairness said in a statement. "Healthcare corporation profitability should not come before quality of patient care. In healthcare, more than almost any other industry, the search for ever higher earnings threatens the wellbeing and lives of the American people."

"At a time when many American workers are struggling with high costs for groceries and housing, the nation's largest low-wage employers are fixated on making their overpaid CEOs even richer," said the author of a new report.

Detailing the widening gap between outrageously high CEO compensation and the median wages of employees at some of the world's largest and most profitable companies, a progressive think tank on Thursday warned executives will continue to enrich themselves at the expense of their lowest-paid workers unless policies are adopted to curb such corporate greed.

"Across the political spectrum, Americans are fed up with overpaid CEOs," said Sarah Anderson, program director at the Institute for Policy Studies (IPS) and author of a new report out Thursday. "Policymakers should take long overdue action to push Corporate America in a more equitable direction."

The report, Executive Excess 2025, finds that absent federal policies forcing corporations to rein in their spending on stock buybacks and exorbitant CEO pay packages, the average CEO-to-worker pay gap widened by 12.9% last year at what IPS calls the "Low-Wage 100"—the 100 S&P 500 companies with the lowest median worker pay.

The average gap between executive and worker pay now stands at 632-to-1 at these firms, up from 560-to-1 in 2023.

Between 2019-24, the average CEO at a Low-Wage 100 company saw their pay rise 34.7%, unadjusted for inflation, while the average median worker pay rose just 16.3%.

CEO compensation increased by 22.6% over the time period, far outpacing inflation. Meanwhile, wage hikes by these same companies didn't even match inflation, including for warehouse workers at software company Aptiv, where the CEO-to-worker pay gap was 2,072-to-1 last year, or cashiers at Ross Stores, where the gap was 1,770-to-1.

"We can curb this runaway source of inequality by taxing corporate greed."

Aptiv CEO Kevin Clark was paid $18.8 million last year while the median worker at the firm made just $9,052. Ross Stores' pay ratio was similar, with CEO Barbara Rentler taking home $17 million compared to the company's median worker, who made just $9,602.

Starbucks, which has made headlines in recent years both for its store employees' fight to unionize across the United States and for its executives' illegal union-busting tactics, had far-and-away the largest gap between CEO and median worker pay in 2024, with CEO Brian Niccol taking home $95.8 million and the median employee earning just $14,674.

That makes the wage gap 6,666-to-1 at the coffee chain.

A petition organized last year by Starbucks Workers United, which has unionized at hundreds of stores since a landmark victory in Buffalo, New York in 2021, warned Niccol that the cost of living across the US "is skyrocketing while you continue to make millions" and the employees "who actually make your Starbucks run can't make ends meet."

IPS said the petition reflected its report's main finding: "At a time when many American workers are struggling with high costs for groceries and housing, the nation's largest low-wage employers are fixated on making their overpaid CEOs even richer."

Contributing to the growing wage gap at the Low-Wage 100 is the companies' focus on stock buybacks, in which firms buy back their own shares to "artificially inflate executive stock-based pay and siphon resources out of worker wages and productive long-term investments."

The 100 companies spent $644 billion on stock buybacks from 2019-24, according to IPS, with home improvement giant Lowe's ranking as the "stock buy back leader," spending $46.6 billion buying its own shares over the past six years.

"That sum could've instead covered the cost of giving each of the firm's 273,000 global employees an annual $28,456 bonus for six years," reads the report. "In 2024, Lowe's CEO Marvin Ellison enjoyed total compensation of $20.2 million, which is 659 times the retailer's $30,606 median annual worker pay."

Anderson said the report highlights "how America's largest low-wage employers are funneling profits into their CEOs' pockets—at the expense of both their workers and their companies' long-term growth."

IPS pointed to "three particularly promising areas for CEO pay policy reform," including:

Congress should pass the Curtailing Executive Overcompensation (CEO) Act, which would apply an excise tax to companies with CEO-to-worker pay ratios exceeding 50-to-1, or the Tax Excessive CEO Pay Act, said the group.

"A May 2024 survey suggests that such taxes would be enormously popular," reads the report. "Overall, 80% of likely voters favor a tax hike on corporations that pay their CEOs over 50 or more times more than what they pay their median employees. Large majorities in every political group support this approach: some 89% of Democrats, 77% of independents, and 71% of Republicans. In swing states, 83% of likely voters give this proposal a thumbs up."

Other legislation, the Stock Buyback Accountability Act, would quadruple the 1% federal excise tax currently in effect for stock buybacks, and would have raised $6.3 billion from the Low-Wage 100 if it had been in effect in 2023 and 2024—enough to cover the cost of 327,218 public housing units each year for two years.

"We can curb this runaway source of inequality," said IPS, "by taxing corporate greed."

The CEO of Starbucks made 6,666 times as much as the company's median employee, all while the company crushes workers' efforts to unionize.

The staggering inequality between bosses and workers only continued to grow last year, according to a new report from the AFL-CIO on executive pay.

The union's latest "Executive Paywatch" report, which uses data from the Securities and Exchange Commission (SEC) to track the pay disparities between CEOs and the employees that work for them, found that the average S&P 500 executive made an eye-popping 285 times more than their median worker did, up from a 268-to-1 ratio in 2023.

CEOs received a $1.4 million raise last year, the data shows, bringing their average yearly compensation up to $18.9 million, a 7% increase. The median worker, meanwhile, made just $49,500, marking just a 3% increase from the year before.

In order to make the same amount as their boss made in a single year, the report noted that the typical employee would need to have begun working in 1740—"Before the AMERICAN REVOLUTION," the union noted on X.

By far the widest disparity was at Starbucks, where CEO Brian Niccol—who took over the company last year—brought home 6,666 times as much as his median employee.

In 2024, while the average Starbucks employee took home less than $15,000, Niccol received a compensation package, primarily made up of company stock, worth nearly $98 million.

For more than three years, Starbucks has waged what New York Times columnist Megan Stack called a "dirty war" against its employees' attempts to unionize.

The company has fired union organizers and pro-union workers, cut their hours to deny them healthcare coverage, shut down unionized stores, and subjected employees to aggressive anti-union "captive audience" meetings.

The Economic Policy Institute estimates that Starbucks has likely had more complaints of illegal union-busting filed against it than any other company in the National Labor Relations Board's 90-year history.

In response to the AFL-CIO's new report, the X account for Starbucks Workers United wrote: "When Starbucks and CEO Brian Niccol tries to tell us they can't afford fair union contracts... remember this."

Starbucks is merely the most glaring example of the inequality highlighted in the report: Coca-Cola, General Electric, Ross Stores, Yum! Brands, Chipotle, and many other flagship American companies paid their CEOs more than 1,000 times as much as their median workers.

These disparities are projected to get even larger following the passage of President Donald Trump's recent budget legislation, which guts social safety net programs like Medicaid and food stamps in order to pay for gigantic new tax breaks for corporations and the wealthiest Americans.

It has been described by some economic analysts as the "largest transfer of wealth in history."

According to a study by the University of Pennsylvania, the incomes of the top 0.1% wealthiest households will increase by more than $83,000 on average by 2033, while the incomes of the poorest 40% will decline.

"Corporate CEOs are raking in millions, and now they'll get another kickback from President Trump's tax cut gift and anti-worker agenda," said Fred Redmond, secretary-treasurer of the AFL-CIO.

The average marginal tax rate paid by these executives, the report found, will decrease by nearly $500,000 a year. In all, the CEOs in the report will be able to avoid paying an extra $738 million in income taxes thanks to the bill.

That lost tax revenue, the report found, could have paid for Medicaid healthcare coverage for more than 80,000 people, SNAP food assistance for over 300,000, or school lunches for more than 900,000 students.

The report notes that many of the CEOs and companies that are expected to profit royally from the bill gave large donations to Trump's inauguration, including Amazon's Jeff Bezos, Coinbase's Brian Armstrong, Google's Sundar Pichai, and Meta's Mark Zuckerberg.

"Is it any wonder," asked former Labor Secretary Robert Reich, "so many people think the system is rigged?"

"This isn't a glitch in the system—it's the system working exactly as designed, funneling wealth ever upwards while millions of working people struggle to afford rent, food, and healthcare."

As people worldwide filled the streets Thursday to celebrate International Workers' Day and mobilize against attacks on the working class, a new analysis showed that average global CEO pay has surged 50% since 2019—56 times more than the pay of ordinary employees.

The Oxfam International analysis examined figures from nearly 2,000 corporations across 35 countries where CEOs were paid more than $1 million on average last year, including bonuses and stock options. Across those companies, the average pay of chief executives reached $4.3 million in 2024, up from $2.9 million just five years ago.

By contrast, average worker pay in those 35 nations rose just 0.9% between 2019 and 2024.

"Year after year, we see the same grotesque spectacle: CEO pay explodes while workers' wages barely budge," said Amitabh Behar, Oxfam's executive director. "This isn't a glitch in the system—it's the system working exactly as designed, funneling wealth ever upwards while millions of working people struggle to afford rent, food, and healthcare."

According to Oxfam, global billionaires "pocketed on average $206 billion in new wealth over the last year," or $23,500 an hour. That's more than the average annual income globally—$21,000—in 2023.

To begin redressing global economic inequality, Oxfam called for top marginal tax rates of at least 75% on the highest earners and wage increases to ensure worker pay keeps up with inflation.

"It's time to end the billionaire coup against democracy and put people and planet first."

Luc Triangle, general secretary of the International Trade Union Confederation, said in a statement that the "outrageous pay inequality between CEOs and workers confirms that we lack democracy where it is needed most: at work."

"Around the world, workers are being denied the basics of life while corporations pocket record profits, dodge taxes, and lobby to evade responsibility," Triangle added. "Workers are demanding a New Social Contract that works for them—not the billionaires undermining democracy. Fair taxation, strong public services, living wages, and a just transition are not radical demands—they are the foundation of a just society."

"It's time to end the billionaire coup against democracy and put people and planet first," he added.

In addition to spotlighting the growing chasm between CEO and worker pay, the Oxfam analysis warned that the global working class "is now facing a new threat" in the form of U.S. President Donald Trump's tariff regime. The humanitarian group argued that "these policies pose significant risks for workers worldwide, including job losses and rising costs for basic goods that would stoke extreme inequality everywhere."

"For so many workers worldwide, President Trump's reckless use of tariffs means a push from one cruel order to another: from the frying pan of destructive neoliberal trade policy to the fire of weaponized tariffs," said Behar. "These policies will not only hurt working families in the U.S., but especially harm workers trying to escape poverty in some of the world's poorest countries."

Corporate CEO paychecks continuing to go gangbusters while the corporations these execs run are—at best—just treading water.

Every day’s headlines now seem to bombard us with ever more outrageous Trumpian antics. Who could have possibly imagined, for instance, that a president of the United States would turn the White House lawn into a Tesla auto showroom?

But these antics actually do serve a useful social and political purpose—for President Donald Trump’s fellow deep pockets and the corporations they run. Trump’s kleptocratic arrogance and audacity have shoved the institutionalized thievery of Corporate America’s ever-grasping top execs off into the shadows.

Those shadows could hardly be more welcome. American corporate executive compensation, as the business journal Fortune has just detailed, is now “surging amid a roaring bonus rebound.”

Heads CEOs win, in other words, tails they never lose.

One example: Tyson Foods CEO Donnie King has seen his annual executive rewards leap from $13 million in 2023 to $22.7 million in 2024. To keep King smiling, Tyson’s board of directors has also extended his CEO contract into 2027 and guaranteed him “a post-employment perk that includes 75 hours of personal use of the company jet as long as he sticks around on the board.”

And what in the way of wonders has Tyson’s King been working to earn all this? Not much, concludes a new Compensation Advisory Partners analysis. Anyone who had $100 invested in Tyson shares at the end of fiscal 2019 today holds a nest egg worth just $80.54. Tyson’s most typical workers aren’t doing particularly well either. They took home $43,417 in 2024, 525 times less than the annual compensation that CEO Donnie King pocketed.

Over at Moderna, Big Pharma’s newest big kid on the corporate block, chief exec Stéphane Bancel saw his 2024 annual pay jump 16.4% over his 2023 compensation despite a 53% drop in Moderna’s annual revenue.

Back in 2022, at Covid-19’s height, Bancel personally collected over $392 million exercising stacks of the stock options he had been sitting upon. Between that year’s start and 2024’s close, Moderna shares plummeted from just under $254 each to under $42.

Moderna’s transition to our post-Covid world, the Moderna board acknowledges, has been “more complex than anticipated.” That complexity, the board apparently believes, in no way justifies denying Bancel his rightful place among Big Pharma’s top-earning CEOs. Bancel’s near $20-million 2024 payday is keeping him well within hailing distance of all his Big Pharma peers.

How can corporate CEO paychecks be continuing to go gangbusters while the corporations these execs run are—at best—just treading water? Lauren Peek, a partner at Compensation Advisory Partners and a co-author of the firm’s latest CEO pay analysis, has an explanation.

Corporate board compensation committees, Peek observes, want to keep their top execs adequately incentivized. These board panels simply cannot bear the sight of their CEOs getting down in the dumps. So what do these panels do? They exclude from their final CEO pay decisions any negative economic factors that CEOs can’t directly determine. But these same corporate panels never take into account unexpected positive economic factors that their CEOs had no hand in creating.

Heads CEOs win, in other words, tails they never lose.

Among those winners: Disney chief exec Robert Iger. His 2024 total pay jumped to $41 million, up nearly $10 million from his 2023 compensation. Disney’s total shareholder return, over that same year, didn’t even reach halfway up the total return that Disney’s peer companies recorded.

Disney hardly rates as an outlier among the 50 major publicly traded corporations that the recently released Compensation Advisory Partners report puts under the microscope. The median revenue growth of these 50 firms dropped to 1.6% in 2024, less than half their 2023 rate. Their earnings remained virtually flat as well. But their CEO compensation climbed an average 9%.

“With financial performance largely flat across these early Fortune 500 filers,” notes an HR Grapevine analysis of the Compensation Advisory Partners findings, “board-level decisions to maintain or raise executive bonuses may prompt further scrutiny from investors and stakeholders alike.”

“For ‘shop-floor’ employees,” adds the HR Grapevine, “news of CEO wage hikes despite average financial performances will undoubtedly prompt a good deal of rumination about their own levels of compensation.”

Equilar, an information services firm specializing in corporate pay, has also been busy analyzing the latest trends in CEO remuneration. Equilar’s latest look at corner-office compensation has found that median CEO pay within the corporations that make up the Equilar 500 jumped up from $12 million in 2020 to $16.5 million last year.

CEO-worker pay gaps have increased even more significantly. At the median Equilar 500 corporation, CEOs pocketed 186.5 times the pay of their most typical workers in 2020 and 306 times that pay in 2024. At America’s larger corporations—those companies sitting at the 75th percentile of the Equilar 500—CEOs made 307.5 times their typical worker pay in 2020 and last year collected 527 times more.

A key driver of this ever-widening CEO-worker pay gap? The sinking compensation going to typical corporate workers, as Equilar’s Joyce Chen concluded last week in an analysis for the Harvard Law School Forum on Corporate Governance. These median workers took home $66,321 in 2020, but just $57,299 last year.

But top execs aren’t just shortchanging workers at pay-time. They’re also pressuring those workers to squeeze and defraud clients and customers at every opportunity, as former Wells Fargo bank manager and investigator Kieran Cuadras has just vividly detailed.

Nearly a decade ago, Cuadras relates, a mammoth phony accounts scandal at Wells Fargo led to fines totaling $20 million against the bank’s then-CEO John Stumpf. But those fines, she points out, hardly made a dent in the estimated $130 million that Stumpf “walked away with in compensation when he resigned.”

Wells Fargo’s current CEO, Charles Scharf, appears to be doing his best to follow in Stumpf’s footsteps. Scharf’s gutted risk and complaint departments are cutting corners “to create the illusion of fewer complaints.” The reality: Those departments are closing complaint cases prematurely. In 2024, these and other sneaky moves helped Scharf pocket a sweet $31.2 million .

Our nation’s political leaders, says Wells Fargo employee and customer advocate Kieran Cuadras, need “to step up and do something about a CEO pay system that rewards executives with obscenely large paychecks for practices that harm workers and the broader economy.”

Where to start that stepping up? Lawmakers ought to be levying new taxes on corporations “with huge gaps between their CEO and worker pay,” Cuadras posits, and increasing an already existing tax on stock buybacks.

Moves like these, she astutely sums up, “would encourage companies to focus on long-term prosperity and stability rather than simply making wealthy executives and shareholders even richer.”

Major insurers are denying legitimate claims following extreme weather events while underwriting fossil fuels and lining their CEOs’ pocketbooks.

Do you know that you’re in good hands with Allstate? Or how about State Farm? Do you know that, like a good neighbor, State Farm is there? Of course you do. Insurance companies have been blasting slogans like these at us for years now. In 2022 alone, Allstate spent $617 million on advertising. State Farm spent an even more whopping $1.05 billion.

But if insurance giants like State Farm truly rated as our “good neighbors,” they’d be behaving—in real life—quite a bit differently than their award-winning advertising suggests.

In hurricane-plagued Florida, for instance, State Farm last year denied 46.4% of homeowner claims, refusals that directly impacted over 76,000 households.

Another reform approach might more quickly catch the attention of top insurance industry boards of directors: tying an insurance company’s tax rate to the ratio between that company’s CEO pay and the paychecks of the firm’s workers.

“Property insurers who deny legitimate claims,” notes Martin Weiss, the founder of the nation’s only independent insurer rating agency, “are sending the implicit message, ‘If you don’t like it, sue us.’”

To add injury to that insult, Weiss adds, Florida Gov. Ron DeSantis had just before last year signed into law new legislation that makes policyholder lawsuits against insurers “far more difficult.”

For recently retired State Farm CEO Michael Tipsord, insurance industry lobbying victories along that Florida line have helped him pocket some stunning personal rewards. Tipsord pulled down $24.4 million in compensation two years ago, almost $4 million more than his industry’s second-highest 2022 CEO pay total. Tipsord had pocketed even more, $24.5 million, in 2021.

“CEOs are living high on the hog while increasing insurance premiums for people living paycheck to paycheck,” the Consumer Federation of America’s Michael DeLong charged last October. “Insurers are telling regulators that ordinary consumers have to pay much more for auto and home insurance because the companies are struggling with inflation and climate change, but they are quietly handing CEOs gigantic bonuses.”

Overall, DeLong’s Consumer Federation reports, the chief execs at America’s ten largest personal insurance lines collected over a quarter-billion dollars in CEO compensation for their services in 2021 and 2022.

If we really had a “good neighbor” at State Farm—or any other insurance giant—those companies wouldn’t have been spending recent years denying relief to the victims of climate change. They would have been insisting instead that lawmakers crack down on the fossil-fuel corporate giants doing so much to foul our planet.

Top insurers did make an early feint in that direction over a half-century ago. Way back in 1973, notes Peter Bosshard, the global coordinator of the U.S.-based Insure Our Future campaign, “the insurance industry first warned about climate risks.” But that warning, in the years to come, wouldn’t stop insurers from “underwriting and investing in the expansion of fossil fuels.”

Giant insurance companies that actually took climate science seriously, Bosshard observes, would have been “suing fossil fuel companies, to make polluters pay for the growing costs of climate disasters and keep insurance affordable for climate-affected communities.”

Insurers haven’t been doing any of that.

”Insurers talk a lot about their climate commitments and supporting their clients through the energy transition, but this is plain greenwashing,” charges Ariel Le Bourdonnec, a Reclaim Finance insurance activist. “They are still profiting from providing cover that allows companies to develop new fossil fuel projects. Insurers could be a force for change, but instead they are undermining climate action.”

Other critics are emphasizing that insurance industry execs have gone beyond “greenwashing” to “bluelining,” as Lilith Fellowes-Granda, a Center for American Progress associate director, points out. These execs are increasing prices and withdrawing services “from regions they perceive to be at high environmental risk.” These moves typically hit hardest on the “communities most vulnerable to the effects of climate change.”

Climate activists are advocating for a variety of policy changes to reverse these dynamics, everything from making sure property insurers must share the risks they cover to ensuring underserved communities access to affordable insurance.

Another reform approach might more quickly catch the attention of top insurance industry boards of directors: tying an insurance company’s tax rate to the ratio between that company’s CEO pay and the paychecks of the firm’s workers.

Inside the insurance industry, as in every other major U.S. economic sector, that ratio between CEO and worker has soared over recent decades.

In 2023, the chief executive at Chubb Ltd., Evan Greenberg, took home $27.7 million, enough to make him that year’s top-paid American property and casualty insurer. Those millions added up to 452 times more than the annual pay of the typical Chubb employee. In 2022, Greenberg pocketed a mere 346 times his company’s typical employee pay.

Back in 1965, the Economic Policy Institute noted last month in its latest annual CEO pay report, the top execs at major U.S. corporations only averaged 21 times what typical American workers earned. Nearly a quarter-century later, in 1989, CEOs were still only averaging 61 times worker pay.

How could we restore greater equity to corporate compensation and, at the same time, give top corporate executives an incentive to care about more than simply maximizing their own personal compensation? Lawmakers at the state and federal levels have over recent years advanced dozens of proposals that tie corporate tax rates to the size of the gap between top executive and worker pay.

In all these proposals, the higher a corporation’s CEO-worker pay ratio, the higher that corporation’s tax rate.

The Institute for Policy Studies has compiled an exhaustive guide to these CEO-worker pay gap proposals. Maybe the winds of Hurricane Milton will help give these moves the momentum they need to turn into law—and give top execs a reason to care about something more than the size of their own personal pay.