SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

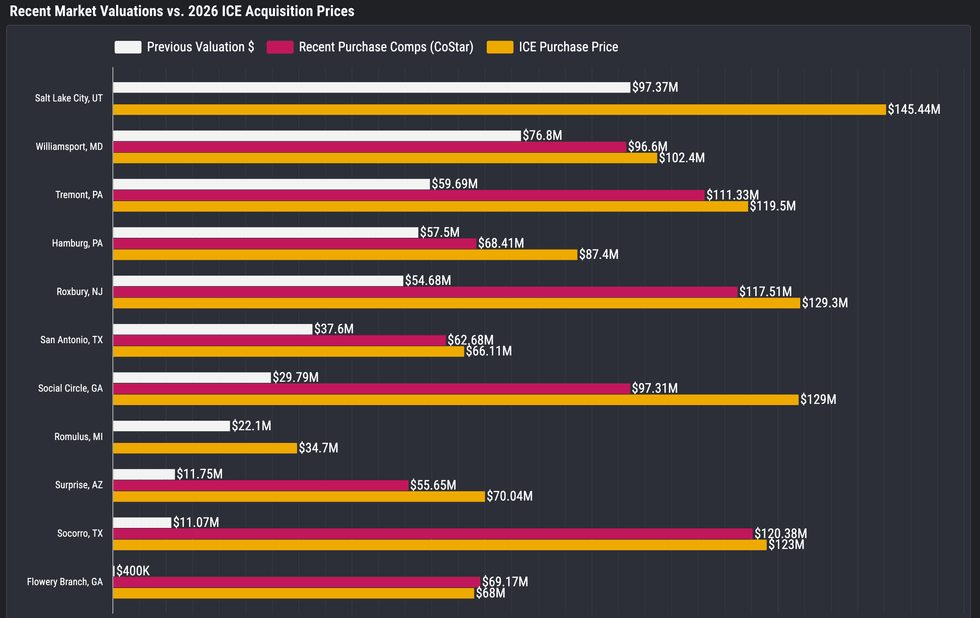

"Folks very close to the White House... were sitting on properties that were causing them losses every year," said a journalist tracking the purchases. "The decision was made to buy them at taxpayer expense."

In what More Perfect Union described as a "new level of corruption" for the Trump administration, an investigation by the progressive news outlet revealed how members of the president's inner circle are cashing in on the Department of Homeland Security's purchase of warehouses for immigrant detention.

It was reported earlier this year that under then-Secretary Kristi Noem, who has since been fired, DHS was planning to spend nearly $40 billion to buy up dozens of warehouses around the US to convert them into makeshift detention camps that could each hold anywhere from 1,000 to 10,000 people arrested as part of President Donald Trump's mass deportation effort.

But when Mae Ryan, a reporter at More Perfect Union, looked into the contracts, she said she "noticed something weird."

"Many of these warehouses had been sitting on the market for years," she explained in a video posted Wednesday. "Now DHS was buying them at a massive markup."

She pointed to one warehouse in Socorro, Texas, recently valued at $11 million, which Immigration and Customs Enforcement (ICE) purchased from the company El Paso Logistics II LLC for $123 million—more than a 1,000% profit.

According to Michael Wriston, an ex-military analyst and investigative journalist who tracked the enormous markups for several of these warehouse purchases for his website Project Salt Box back in March, "across more than a dozen warehouse acquisitions, ICE paid prices that exceeded both prior property valuations and recent market comparables at nearly every site."

For one warehouse in Surprise, Arizona, previously valued at just under $12 million, ICE paid over $70 million. For another in Social Circle, Georgia, valued at about $30 million, the agency paid nearly $130 million.

(Graphic by Project Salt Box)

(Graphic by Project Salt Box)

Many of the warehouses that raked in obscene taxpayer-funded purchases by DHS were owned by financial institutions with deep connections to the Trump administration, Ryan explained.

One warehouse in Roxbury, New Jersey, valued at about $54.6 million in 2025, inexplicably sold to ICE for over $129 million, more than double. Its majority owner was the investment bank Goldman Sachs, where many Trump appointees during his first term—including former Treasury Secretary Steve Mnuchin and Trump financial adviser Gary Cohn—were formerly employed.

ICE paid double for another warehouse in Tremont, Pennsylvania, buying it for nearly $120 million despite a valuation of about $60 million. It was owned by the private capital firm Blue Owl, where at least 33 members of Trump's administration have investments in its funds, including the president himself, who has about $5 million invested in the firm.

Another in Salt Lake City, valued at just $97 million, was purchased by ICE for $145 million, and the agency now plans to convert it into a 10,000-bed facility. It was owned by Deutsche Bank, which has loaned Trump about $2.5 billion over the past two decades.

Wriston told More Perfect Union that the financial payout to Trump allies was top of mind for DHS as it drew up the controversial warehouse plan.

"ICE doesn't necessarily want to be using warehouses," he said. "The plan came from folks very close to the White House who were sitting on properties that were causing them losses every year. And the decision was made to buy them at taxpayer expense."

It's part of a larger pattern of ICE contracts being distributed to companies that have given major financial support to Trump.

According to an investigation in March by OpenSecrets, the GEO Group and CoreCivic, two private prison companies that have collectively received more than $2.8 billion in ICE contracts, each donated $500,000 to Trump's inaugural committee. The GEO Group's employee-funded political action committee contributed $1 million to the pro-Trump super PAC Make America Great Again, Inc. during his reelection campaign in 2024.

The vast majority of those who have been detained during Trump's second term have had no criminal records, despite claims by the administration that they are targeting "the worst of the worst" criminals for deportation.

Those who have been held in ICE detention centers—often without any due process or access to a lawyer—have consistently reported being held in horrendous conditions, denied access to basic food, sanitation, and medical care, and subject to torture and sexual assault by guards.

DHS has reportedly spent only about $1 billion of the more than $38 billion allotted for immigration detention warehouses so far. According to The New York Times, the administration is hoping to build a mass detention system that could stuff these warehouses with over 100,000 detainees at a time across more than 20 facilities.

According to Wriston's running tracker of ICE warehouse sales, at least 13 purchases have been canceled, in many cases due to public backlash. Still, the administration has already purchased enough warehouse space to hold more than 41,500 people at once.

"What we're seeing happen now—I never in a million years envisioned seeing this happen on US soil," Wriston said. "Never. Never once."

The rising costs that small business owners are paying for imports due to President Donald Trump’s trade tariffs, a tax on American consumers and businesses, is roiling mom-and-pop shops across the US.

According to the Pew Research Center, Americans have big trust in small businesses versus big corporations.

Mom-and-pop shops will need that positive vibe and more as they approach the make-or-break year end business season, beginning with Small Business Saturday on November 29. While small business owners can’t compete on prices with larger companies, there are other factors in play such as personal service. Nevertheless, prices of goods and services do matter, so the rising costs that small business owners are paying for imports due to President Donald Trump’s trade tariffs, a tax on American consumers and businesses, is roiling mom-and-pop shops across the US.

On April 2, 2025, Trump announced that he was via tariffs “enacting fair trade policies that will restore our workforce, rebuild our economy, and finally put America First.” According to Small Business Administration Administrator Kelly Loeffler, mom-and-pop shops would reap a bounty of benefits from tariffs on imports from global trading partners: “Small businesses will no longer be crushed by foreign governments and unfair trade deals. Instead, we will put American industry, workers, and strength FIRST.”

How are these claims working out on Main Street? We turn to Fabrice Moschetti, owner of Moschetti Artisan Roasters, in Vallejo, California. Imported coffee he buys from Brazil was tariff-free until the president imposed a baseline “reciprocal tariff” of 10% on imported goods globally, then increased tariffs on Brazilian imports another 40% in July because the government of Brazil was prosecuting its past President Jair Bolsonaro, awaiting a 27-year prison sentence on appeal currently after conviction for planning a military coup against his successor, Brazilian President Luiz Inácio Lula da Silva.

"At this point, we've transitioned from working for profits to working for tariffs. We are just in business to pay off our tariff debt."

It’s been a struggle to find an adequate supply of coffee, according to Moschetti, forcing him to truck it in from cities such as Seattle versus the nearby Port of Oakland. "It's been difficult to tell the mom-and-pop owner-operators who we work with that our prices are increasing 40%," he says.

While Trump recently rolled back the 40% tariffs on coffee imports from Brazil, tariffs on imports from other global trading partners remain in place. Two examples of tariff-price hikes on imports are bags and cups made abroad in China.

Dan Anthony is the executive director of We Pay the Tariffs (WPT), a Washington, DC-based coalition of small businesses. Its aim is to advocate for policies that address the negative impacts of tariffs.

Strength in numbers is a political strategy that confronts the money-power of big banks, corporations, and the wealthy. It’s a strategy that faces enormous obstacles, economically and politically.

Meanwhile, presidential tariffs totaled $120 billion paid on US imports from March to August 2025, according to Anthony. That $120 billion compares with the spending on the National School Lunch Program and related programs for 12 months.

Joann Cartiglia is the owner-operator of The Queen's Treasures in Ticonderoga, New York. Her doll accessories and toy company is struggling with tariff-driven inventory shortages as the make-or-break holiday season approaches, according to Cartiglia. American companies paid $1.2 billion in tariffs on toy imports for the year ending in August 2025, a spike of 22.3% from 0% the past year, according to WPT, based on Census data. Meanwhile, toy imports grew 0.1% between August 2024 and August 2025.

Jared Hendricks is the owner of Village Lighting Co. in West Valley City, Utah. "We're approaching a $1 million in tariffs this year that weren't in the budget,” he says, “weren't in the forecast, and frankly, weren't in the cash flow, so we had to finance that. At this point, we've transitioned from working for profits to working for tariffs. We are just in business to pay off our tariff debt."

Currently, import prices are rising and small businesses are struggling. Anne Zimmerman is founder and owner of Zimmerman & Co. CPAs Inc. in Cleveland and Cincinnati, Ohio, and cochair of Small Business for America’s Future. The group’s new survey of 1,048 small business owners shows that 74% of them do not think that they will remain open in 2026.

“Congress needs to focus on policies that will actually help us,” Zimmerman says in a statement. “That means extending the Affordable Care Act tax credits so businesses and their employees aren’t hit with massive healthcare cost spikes. The Supreme Court needs to strike down these tariff policies that are crushing small businesses.”

"This is their end goal: the privatization of as much of the U.S. government as possible, enriching the rich and leaving everyone else worse off," warned one progressive.

Elon Musk sparked calls Thursday to fight what one union called an "illegal power grab" after the senior adviser to President Donald Trump and de facto head of the Department of Government Efficiency said that the United States Postal Service and Amtrak, the national passenger rail service, should be privatized.

"I think logically we should privatize anything that can reasonably be privatized," Musk—who is advising Trump on how to eviscerate federal agencies—said while appearing remotely at the Morgan Stanley Technology, Media, and Telecom Conference. "I think we should privatize the post office and Amtrak for example... We should privatize everything we possibly can."

"Basically, something's got to have some chance of going bankrupt, or there's not a good feedback loop for improvement," he opined.

The U.S. Postal Service (USPS) employs more than 600,000 people. Amtrak has more than 21,000 workers.

"Big banks are already drawing up plans for a fire sale of the most profitable parts of our postal network."

Musk called the state of Amtrak "kind of embarrassing" and contrasted the U.S. rail system with the networks of countries including China, where the central government has financed the construction of nearly 30,000 miles (48,200 km) of high-speed lines. The United States has less than 300 miles of high-speed rail.

"Amtrak is a sad situation," Musk asserted. "It's like, if you're coming from another country, please don't use our national rail. It can leave you with a very bad impression of America."

Responding to Musk's remarks, Progressive Mass political director Jonathan Cohn said on social media, "This is their end goal: the privatization of as much of the U.S. government as possible, enriching the rich and leaving everyone else worse off."

Like Musk, Trump has also expressed support for privatizing the USPS, a move recommended by his Office of Management and Budget during his first term. The president also sought to slash Amtrak's funding during his first administration.

Last month, reporting that Trump is seeking to place the USPS under the control of the Commerce Department—which is led by billionaire cryptocurrency banker Howard Lutnick—sparked outrage and allegations of illegality.

"White House sources recently briefed the media that they were planning an illegal power grab of our public Postal Service," the American Postal Workers Union (APWU) said in an email this week responding to ongoing attacks on the USPS. "Such a power grab could allow them to put into action our greatest fear. Stripping our services and selling off our USPS."

"Big banks are already drawing up plans for a fire sale of the most profitable parts of our postal network, raising shipping costs for the public, and leaving taxpayers on the hook to fund the rest," APWU added. "We can't allow this to happen!"

Last month, longtime Postmaster General Louis DeJoy signaled he would step down by asking the United States Postal Service Board of Governors to begin selecting his successor. DeJoy's tenure has been marred by allegations of criminal election obstruction, conflicts of interest, and other corruption. His Delivering for America, a 10-year austerity plan, has been condemned by some critics as a roadmap to privatization.

It's not just the USPS and Amtrak. Key members of the Trump administration and their oligarch allies are pursuing policies and actions opponents argue are ultimately aimed at privatizing a sweeping range of federal agencies and services, from

public education to veterans' healthcare to mortgage lending, Social Security, Medicare, and more.

And the best way to do that is to... fight like hell for the working class.

Kamala Harris must win the former Blue Wall states of Michigan, Pennsylvania, and Wisconsin, which are now up for grabs. And winning those battleground states requires reaching working-class voters who have been economically harmed and left behind by Wall Street’s insatiable greed.

The Harris campaign has not been courting these voters the way you would expect from the party of working people. Instead, she has managed both to kiss up to Wall Street and to allow Trump to appear as the savior of working-class jobs. Those advising her on this strategy are either politically tone deaf or worse, blinded by potential Wall Street employment opportunities after the election.

The Vice-President’s first big gaffe was going to Wall Street for a highly publicized fundraising event saying she “would encourage innovative technologies like AI.” Doesn’t her team understand that Artificial Intelligence is not a term of endearment to working people who fear automation will kill their jobs?

The Harris campaign has not been courting these voters the way you would expect from the party of working people. Instead, she has managed both to kiss up to Wall Street and to allow Trump to appear as the savior of working-class jobs.

Meanwhile, the New York Times reports that behind the scenes her advisors have been moderating her proposals to please Wall Street. (“How Wall St. Is Subtly Shaping the Harris Economic Agenda”.) How is this the party of working people?

Fantasy Finance

The Harris team is suffering from several debilitating illusions. They seem to believe that if Wall Street approves of her economic agenda, it will close the economic-approval ratings gap with Trump. That certainly isn’t the case in the more industrialized states where most working people see Wall Street as the destroyer of jobs.

There also is no lost love there for the big banks that are too big to fail and get bailed out whenever they rape and pillage the economy into disaster. If you ask the average worker in the Midwest to pick the one word that they associate with Wall Street, nearly all will say “greed.”

The Harris team clearly believes that we live in a win-win economy—that when Wall Street does well, we all do well. They seem oblivious to the ways in which Wall Street’s leveraged buyouts and stock buybacks have robbed millions of working people of their livelihoods.

These workers are not stupid. When a private equity company buys up the facility where they work, they know layoffs are coming to service the new debt load. When a company pours corporate funds into buying back their own stock to artificially boost the stock price, they know that layoffs will be used to pay for shoveling all this money to the richest stock owners and executives. (Please see Wall Street’s War on Workers for all the gory details.)

Blowing Off the John Deere Workers

The Harris team, however, has the perfect chance to show that they understand how important it is for the government to save jobs from rapacious corporations. The opportunity came when John Deere announced that it would send 1,000 jobs to Mexico, crying competitive pressure while in 2023 earning $10 billion in profits, paying its CEO $26.7 million, and conducting $12.2 billion in stock buybacks.

Donald Trump saw a big opening and called for a 200 percent tariff on Deere’s imports if it shipped those jobs to Mexico. That threat, idle or not, certainly caught the attention of the workers who were about to see their jobs evaporate. And it certainly resonated with economically precarious workers all through the industrial heartland who could care less about whether tariffs are good or bad macroeconomic policy.

What did the Harris team do? Exactly the wrong thing. It wheeled out Mark Cuban, the celebrity billionaire owner of the Dallas Mavericks, to attack the tariff as “insanity…ridiculously bad and destructive,” on macroeconomic grounds Not a word said by Cuban or the Harris campaign about those 1,000 jobs that are about to be destroyed. That shows “ridiculously bad and destructive” political campaigning.

I’m starting to wonder about the smarts of the Harris advisors. They seem willfully oblivious to the fact that Trump’s 2017 intervention to save jobs at the Carrier air conditioning company in Indiana was wildly popular among voters of all political persuasions. Guess what? Having the government step in to save your job is what people want the government to do. Why can’t Harris say she will do the same?

I’ve been begging, pleading, jumping up and down to get the Harris campaign to say she will stop corporations from taking our tax dollars, pouring it into stock buybacks, and then laying off millions of workers each year. The proposal is really simple. Add this one sentence to every federal contract:

“No taxpayer money in the form of federal grants, contracts, and purchases, shall go to corporations that layoff taxpayers and conduct stock buybacks.”

But my message is not penetrating the dense Democratic Party ecosystem distorted by Wall Street’s cash and future lucrative job opportunities.

The Harris campaign clearly believes they are doing more than enough to attract working people in the key battleground states, and that it is wiser to placate rather than offend Wall Street.

I sure hope they are right and, come election night, that my analysis is dead wrong.

Big banks like Chase have repeatedly targeted communities, taxpayers, and even our schools with predatory debt. It's time to fight back.

Chicago’s school year kicked off amid a looming budget crisis that jeopardizes stability for both students and teachers. At the heart of the issue is a silent killer of public education: predatory bank loans, particularly from JPMorgan Chase.

During a bargaining session with the Chicago Teachers Union (CTU), I urged Chicago Public Schools (CPS) to stop allowing big banks to hold Chicago students hostage. Instead of delaying contract negotiations with teachers and risking program cuts that harm students, CPS and state officials should take legal action to recover the funds lost due to these toxic bank deals.

CPS has a deficit projection of over half a billion dollars, perpetuated by the several hundred million dollars in predatory loans from banks like JPMorgan Chase taken out nearly a decade ago. These loans have strangled CPS finances and prevented the district from providing the high-quality education Chicago's children deserve.

Predatory loans are a familiar problem for families in Chicago and around the country. These risky loans are hawked as a short-term solution to fill a gap in finances–with a steep interest rate buried in the fine print that balloons over time.

Chicago Public Schools should hold banks like Chase accountable for the harm they’ve caused Chicago’s schoolchildren.

Chase has repeatedly targeted communities, taxpayers, and even our schools with predatory debt. Chase and its predecessor banks pushed Black and brown Chicagoans into the predatory subprime mortgages that caused the 2008 financial crisis, leading to a tsunami of foreclosures that resulted in a massive loss of household wealth in communities of color.

And nearly 10 years ago, Chase closed a predatory deal with CPS that has haunted our finances ever since.

CPS was already reeling from drastic cuts to special education services in 2016, prompted by the immediate payment of $234 million in termination fees for bad deals they entered into a decade prior. An unfair school funding formula forced 50 schools to shutter three years earlier and continued to destabilize the same South and West side neighborhoods.

A twin set of threats were on the horizon: a potential takeover of schools by Governor Bruce Rauner, a Republican who was hellbent on making Illinois more like Texas, and a threat by Mayor Rahm Emanuel to lay off 6,000 teachers to close a budget gap caused by structural underfunding.

The school district desperately needed funds to pay for projects like lead abatement. Rather than face a takeover or mass layoffs, they decided to issue bonds in order to pay the termination fee. But because CPS’s credit rating had been downgraded to “junk” just a few months prior, financial giants like Chase and Nuveen exploited the opportunity.

Banks purchased the bonds from CPS at a lowball price but then sold them to other investors just months later for a much higher payoff. Over a span of two months, Chase bank made a 9.5% profit on $150 million in bonds through this arbitrage scheme, an annualized profit of 82%. This calls into question whether Chase met its legal obligation to give CPS a fair price for the bonds. Our schools are still impacted by these bad deals, paying $200 million annually for loans taken out during this moment of crisis.

CPS was also the victim of toxic interest rate swaps deals that cost the district, Chicago, and the state of Illinois hundreds of millions of dollars in the early 2000s. Banks had marketed swaps as a way for cash-strapped governments to save money, but they were laden with hidden risks that materialized as a result of the 2008 financial crisis, causing payments to skyrocket and costing taxpayers a fortune.

As with Chicago’s parking meter and Skyway deals, future generations of taxpayers were stuck holding the bag. From 2012 to 2016, the City of Chicago handed over $145 million to Chase Bank alone to terminate these toxic swaps.

CPS should hold banks like Chase accountable for the harm they’ve caused Chicago’s schoolchildren. There is strong reason to believe the banks that trapped CPS into these predatory deals violated their legal responsibilities to the district. While the district has improved its financial health since 2016, recovering the millions lost to predatory lending would help build on their progress.

Decades of underfunding and predatory banking have swallowed the district’s reserves. Now, faced with a federal reduction that could slash funding by $800 per student, the district has reached an inflection point: Will CPS hold banks accountable and fund the programs, resources, and staff that students deserve—or will they make cuts that set kids back?

Our institutions—from the White House to the university president, from the bank CEO to the labor leader, from the newspaper editor to the religious leader—need to be willing to show some ability to change.

There’s no question that the rate of climate anxiety is growing—how could it not be, on a world where fires and floods are increasingly commonplace? And once your house has flooded—well, the next rainstorm, or even the next forecast, is going to bring back too many memories.

But I’ve found that a fair number of people, especially younger ones, are feeling really desperate anxiety even before they’ve had a traumatic experience, to the point where, for instance, they don’t want to have children of their own. My guess is that this has as much to do with the sense that they’ve been abandoned by the leading institutions—political and economic—of our societies, who can’t bring themselves to acknowledge the scale of this emergency or break old practices.

I’ve been thinking all week at my anger at America’s big banks, the companies that represent the capital in capitalism—as I explained last week, they’ve now backed away even from their very scant climate commitments, fearful it might cost them a bit at the margins. And this week the Biden administration let it be known it was going to relax the timetable for getting rid of internal combustion engines, because of combined pressure from the auto companies and the auto workers union.

I remember debating a wind power opponent at Dartmouth years ago; when he was done making his case that no one should have to look at these “monstrosities,” the first question from a student was: “Could you please explain how you managed to get your head so far up your butt?”

I have no more sympathy for the car companies than the banks—they’ve opposed every regulation anyone has ever proposed, at least as far back as seat belts. And I have lots of sympathy for the UAW—they deserved and needed a new contract, which is why many of us tried to play at least a tiny part in helping their successful fall strike. They fret that moving too fast could cost jobs, which is a real worry. But moving too slow has a huge cost too, on a planet that has just come through its hottest year in the last 125,000: Passenger vehicles contribute almost a third of America’s carbon emissions. In a world that understood the climate crisis as an emergency, UAW president Shawn Fain, and the car company CEOs, and the Biden administration would be out on the stump together, doing everything they could to get people to buy EVs.

No need to single out the UAW, especially since they’re doing their best to undercut the Trump campaign (he’d love to make electric cars, which he insists grind to a halt after 15 minutes of driving, a centerpiece of his campaign). After all, we could say the same thing about all those universities that have fought fossil fuel divestment because it’s easier just to keep investing as you have in the past, or those insurance companies that continue to underwrite new pipelines even as their data show the inexorable rise in climate damage, or those longtime residents of cities and suburbs who oppose denser housing in their communities even though it’s clearly a key part of both cutting emissions and letting the next generation have an affordable place to live. If you’re a young person you could look at them all and think: They don’t want even relatively small changes, and in the process they’re guaranteeing that absolutely everything will change for us.

I think older people underestimate how often their resistance to change is read as disregard for the future. I remember debating a wind power opponent at Dartmouth years ago; when he was done making his case that no one should have to look at these “monstrosities,” the first question from a student was: “Could you please explain how you managed to get your head so far up your butt?” There are occasions when I despair that the motto of my beloved Vermont, oldest state in the union, should be “change anything you want once I’m dead.”

A global study in The Lancet a couple of years ago attempted to quantify this sense of what the authors called “betrayal.” The researchers found deep-seated climate anxiety around the planet. Read the findings just to let them sink in:

A large proportion of children and young people around the world report emotional distress and a wide range of painful, complex emotions (sad, afraid, angry, powerless, helpless, guilty, ashamed, despair, hurt, grief, and depressed). Similarly, large numbers report experiencing some functional impact and have pessimistic beliefs about the future (people have failed to care for the planet; the future is frightening; humanity is doomed; they won’t have access to the same opportunities their parents had; things they value will be destroyed; security is threatened; and they are hesitant to have children). These results reinforce findings of earlier empirical research and expand on previous findings by showing the extensive, global nature of this distress, as well as its impact on functioning. Climate distress is clearly evident both in countries that are already experiencing extensive physical impacts of climate change, such as the Philippines, a nation that is highly vulnerable to coastal flooding and typhoons. It is also evident in countries where the direct impacts are still less severe, such as the U.K., where populations are relatively protected from extreme weather events.

And they also found that that feeling of abandonment was a huge part of the problem:

Distress appears to be greater when young people believe that government response is inadequate, which leads us to argue that the failure of governments to adequately reduce, prevent, or mitigate climate change is contributing to psychological distress, moral injury, and injustice.

Such high levels of distress, functional impact, and feelings of betrayal will negatively affect the mental health of children and young people. Climate anxiety might not constitute a mental illness, but the realities of climate change alongside governmental failures to act are chronic, long-term, and potentially inescapable stressors. These factors are likely to increase the risk of developing mental health problems, particularly in more vulnerable individuals such as children and young people, who often face multiple life stressors without having the power to reduce, prevent, or avoid such stressors.

Humans are remarkable creatures. Though we can, uniquely, worry about the future, we can also, uniquely, feel the kind of solidarity and support that lets us carry on even amidst great travail. But isolation, lack of connection—they crack us.

Our institutions—from the White House to the university president, from the bank CEO to the labor leader, from the newspaper editor to the religious leader—need to be willing to show some ability to change in the face of an emergency. We’re not even talking huge sacrifice—the difference between making EVs and making old-school SUVs, or investing in a fossil-free index fund, or ending loans to oil companies, is not existential to any of the parties involved. They are small hits indeed compared with the hits that are headed our way if the planet keeps heating. And the willingness to change would not only help us weather this crisis physically—it would also help us weather it emotionally.

We only get one life. The thought that young people are having to live theirs under this shadow—damaged by the climate crisis even before its fully hit them—should give all of us real pause. There’s a generational theft underway: of water and ice and coral, but also of security and ease.

"We bet it was super easy for Patrick McHenry and Andy Barr to decide their position on predatory overdraft fees, since all they did is copy and paste whatever Big Banks said."

A pair of Republican lawmakers on the House Financial Services Committee issued a statement last week criticizing a new Consumer Financial Protection Bureau proposal aimed at cracking down on predatory overdraft fees, claiming the rule would harm consumers.

But they didn't mention that parts of their criticism of the rule precisely mirrored the talking points of the Consumer Bankers Association (CBA), a lobbying group that represents financial institutions that rake in huge profits by hitting their customers with often unexpected overdraft charges. The group's membership list includes JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo as well as smaller banks from around the country.

Rep. Patrick McHenry (R-N.C.), the chair of the House Financial Services Committee, and Rep. Andy Barr (R-Ky.) said in their statement that the CFPB's rule reflects "the Biden administration's attempts to mandate one-size-fits-all consumer financial products and services."

"We urge the CFPB to withdraw this misguided proposal that harms the very consumers the agency was created to protect," the GOP lawmakers added.

As Politico's Caitlin Oprysko pointed out late Tuesday, McHenry and Barr's response bears a close resemblance to language used by CBA president Lindsey Johnson, who warned the consumer agency's "misguided proposal" and "one-size-fits-all approach" could "undo years of progress" that banks have purportedly made in reforming their overdraft policies.

"Shilling for their financial industry megadonors has become so involuntary and routine that they're now literally copying and pasting talking points from banking lobbyists."

The similarities between the Republican lawmakers' response to the rule and CBA talking points become more glaring further down in McHenry and Barr's statement, which says that "consumers must proactively opt-in to use overdraft services."

Oprysko observed that the CBA uses the same exact wording on a website it launched earlier this month in opposition to the CFPB's overdraft rule, which the agency estimates could save U.S. consumers more than $3.5 billion in fees per year.

"Consumers must proactively opt-in to use overdraft services," the website reads, adding that "consumers can discontinue overdraft services at any time."

McHenry and Barr similarly say that consumers "can discontinue these services at any time." The lawmakers and CBA also "both highlight the same 2023 survey finding about consumer sentiment toward overdraft services and the same quote from a Biden administration financial regulator," Oprysko noted.

A spokesperson for CBA told Politico that the lobbying organization did not coordinate with McHenry or Barr on their responses to the rule but that "we like their message and agree with it." A Barr spokesperson told the outlet that the responses were so similar because the CFPB's proposal is "clearly problematic."

Liz Zelnick, director of the Economic Security and Corporate Power program at the progressive watchdog group Accountable.US, said in a statement Wednesday that "for Chairman McHenry and Rep. Barr, shilling for their financial industry megadonors has become so involuntary and routine that they're now literally copying and pasting talking points from banking lobbyists and trying to pass it off as their own."

"But what's more unethical is that McHenry and Barr continue to claim consumers should be grateful for hidden and excessive overdraft fees when their only real purpose is to pad profits for big banks and credit unions," said Zelnick. "McHenry and Barr can appease bank CEOs and lobbyists all they want by parroting industry misinformation, but they should at least be honest that they're doing it at the expense of consumers, not to their benefit. The fact remains, the Biden administration crackdown on excessive overdraft penalties like a $42 charge on a gallon of milk will directly benefit consumers by lowering their costs."

According to the CFPB, around 23 million U.S. households pay overdraft fees every year, often getting hit with $35 charges even though overdrafts are typically less than $26.

The agency said in a statement last week that its rule would "close an outdated loophole that exempts overdraft lending services from longstanding provisions of the Truth in Lending Act and other consumer financial protection laws." The rule would apply to banks with more than $10 billion in assets.

The proposed rule garnered enthusiastic praise from consumer advocacy organizations.

Kimberly Fountain, consumer field manager at Americans for Financial Reform, said that "curbing abusive overdraft fees will help stop Wall Street from padding its bottom line with the hard-earned money of millions of families in the United States."

"Overdraft fees are not so much a useful service as they are a lucrative profit center underwritten by the most economically vulnerable consumers," Fountain added.

"It is business as usual for most banks and investors who continue to support fossil fuel developers without any restrictions, despite their high-profile commitments to carbon neutrality."

Top banks in the United States and around the world have made a show of embracing net-zero emissions pledges, portraying themselves as allies in the fight against the global climate emergency.

But a new analysis published Tuesday by a group of NGOs makes clear that the world's leading financial institutions—including major Wall Street banks such as Citigroup, JPMorgan Chase, and Bank of America—are still pumping money into fossil fuel expansion, bolstering the industry that is primarily responsible for worsening climate chaos.

According to the report, 56 of the largest banks in the Net-Zero Banking Alliance (NZBA)—a coalition convened by the United Nations—have provided nearly $270 billion in the form of loans and underwriting to more than 100 "major fossil fuel expanders," from Saudi Aramco to ExxonMobil to Shell.

Additionally, 58 of the biggest members of the Net-Zero Asset Managers (NZAM) initiative—including the investment behemoths BlackRock and Vanguard—held at least $847 billion worth of stocks and bonds in more than 200 large fossil fuel developers as of September.

Both the NZBA and the NZAM are under the umbrella of the Glasgow Financial Alliance for Net-Zero (GFANZ), a campaign launched in 2021 with the goal of expanding "the number of net zero-committed financial institutions." Climate advocates have long argued that net-zero pledges are fundamentally inadequate to the task of stopping runaway warming.

"The science is very clear: we need to stop developing new coal, oil, and gas projects as soon as possible if we want to meet our climate goals and avoid a worst-case scenario," said Lucie Pinson, the executive director and founder of the watchdog group Reclaim Finance. "Yet, it is business as usual for most banks and investors who continue to support fossil fuel developers without any restrictions, despite their high-profile commitments to carbon neutrality."

"Their greenwashing is all the more damaging as it casts doubt on the sincerity of all net-zero commitments and undermines the efforts of those who are truly acting for the climate," Pinson added.

The groups found that the U.S.-based Wall Street giants Citigroup, JPMorgan Chase, Bank of America, Morgan Stanley, and Wells Fargo provided nearly $90 billion in total financing for fossil fuel expansion between the dates they joined the NZBA and August 2022.

Citigroup, which touts its net-zero commitments on its website, led the pack with $30.5 billion in fossil fuel financing from April 2021 to August 2022.

"The U.S. financial sector cannot be taken seriously on climate change until it stops investing in new fossil fuel projects," said Adele Shraiman, a representative for the Sierra Club's Fossil-Free Finance campaign. "We need an urgent transition to a green economy and the financial sector must help deliver that."

Overall, according to the new report, "229 of the world's largest fossil fuel developers received finance from the 161 GFANZ members covered... which will support them to develop new coal power plants, mines, ports, and other infrastructure, as well as new oil and gas fields and pipelines and LNG terminals."

"These new fossil fuel projects are incompatible with the objective of limiting global warming to 1.5°C, as confirmed in the latest International Energy Agency's World Energy Outlook published in October 2022," the report states. "They will lock in greenhouse gas emissions for decades, despite the adoption of decarbonization targets by some GFANZ members."

Paddy McCully, a senior analyst at Reclaim Finance, said in a statement that "GFANZ members are acting as climate arsonists."

"They've pledged to achieve net-zero but are continuing to pour hundreds of billions of dollars into fossil fuel developers," said McCully. "GFANZ and its member alliances will only be credible once they up their game and insist that their members help bring a rapid end to the era of coal, oil, and fossil gas expansion."

The Republican threatened to divest from financial institutions including JPMorgan Chase and Citigroup—widely accused of failing to meet even modest climate goals—under a state law banning "energy company boycotts."

Kentucky's Republican treasurer on Tuesday threatened to divest from 11 financial institutions—including major fossil fuel investors—that she falsely claimed were "engaged in energy company boycotts" in violation of commonwealth law.

"When companies boycott fossil fuels, they intentionally choke off the lifeblood of capital to Kentucky's signature industries," Treasurer Allison Ball said in a statement. "Traditional energy sources fuel our Kentucky economy, provide much-needed jobs, and warm our homes. Kentucky must not allow our signature industries to be irreparably damaged based upon the ideological whims of a select few."

In the same statement, Ball's office said that "all listed financial companies must stop engaging in the energy company boycott to avoid becoming subject to divestment."

Last year, Kentucky's Republican-dominated Legislature passed, and Democratic Gov. Andy Beshear signed into law, S.B. 205, which takes aim at environmental, social, and governance (ESG) investing, a set of criteria that include companies' policies for addressing the climate emergency.

Republicans have derided ESG as "woke" investing. Numerous GOP-led states have divested billions of dollars from targeted investment firms—even when doing so harms them financially.

Ball's list includes BlackRock—one of the world's largest investors in fossil fuels and deforestation—as well as institutions such as JPMorgan Chase and Citigroup, which also rank among the top fossil fuel industry financiers, according to Bloomberg. Climate campaigners have criticized many of the financial institutions on Ball's list for failing to meet even the modest climate goals they've set for themselves.

"The fact is that we are among the largest financers of the U.S. traditional and renewable energy industries, including in Kentucky, where we serve some of its largest energy companies and utilities," JPMorgan Chase spokesperson Trish Wexler told Bloomberg. "We believe our business practices are in line with Kentucky law, and we are hopeful a deeper look at these facts would lead to reconsideration."

BlackRock spokesperson Christopher Van Es told Bloomberg that "on behalf of our clients, we have invested approximately $276 billion in energy companies globally. BlackRock does not boycott energy companies and will continue to be investors across the energy sector."

Ball's office gave state agencies 30 days to say whether they hold investments in any of the listed financial institutions, and 90 days to "cease boycotting energy companies in order to avoid divestment."

"Treasurer Ball has long been a national leader in the fight against harmful ESG schemes which hurt our economy, threaten our national security, and prioritize political goals above financial returns," the treasurer's office said. "The compilation of this list is the latest in a series of her efforts to oppose this dangerous practice."

As the U.S. Federal Reserve on Wednesday raised interest rates--the fourth consecutive 0.75% increase and the sixth hike of the year--progressives stressed that Fed policy boosts the likelihood of a global recession and disproportionately harms low-income workers and other marginalized people.

"Working people should not be the target of lowering inflation, it should be corporations that are earning record profits."

Fed Chair Jerome Powell explained that the move was necessary to ease inflation, which has hit a 40-year-high due to factors including corporate profiteering, Russia's invasion of Ukraine, and the climate emergency.

"We've always said it was going to be difficult," he said, "but to the extent rates have to go higher and stay higher for longer it becomes harder to see the path" to avoiding recession.

"I would say the path has narrowed over the course of the last year," Powell added.

Progressive economists and activists refuted the Fed's approach.

Accountable.US spokesperson Liz Zelnick noted in a statement that "a chorus of economic experts have warned hiking interest rates again is a recipe for millions of Americans receiving pink slips, yet the Fed has decided to triple down on what is not working."

"Throughout the pandemic, the Fed should have been acting as stewards of the fragile economic recovery but instead have prioritized demands from big banks, hedge funds, and other Wall Street special interests at the great expense of average working families," she contended.

"If excessive interest rate hikes hasten the arrival of an otherwise avoidable recession, will the Fed take responsibility," added Zelnick, "or try to pass the buck as they keep making matters worse?"

AFL-CIO president Liz Shuler said the Fed's latest rate hike "will have a direct and harmful impact on working people and our families" and "will not address the underlying causes of inflation."

"The Fed seems determined to raise interest rates, though it openly admits those rates could ruin our current economy as unemployment remains low and people are able to find jobs," she continued. "A recession would instead cause companies to hire fewer people, making it harder for young workers, workers of color, and others who have greater barriers finding jobs, and put downward pressure on the wages of all working people who will bear the brunt of an overactive monetary policy."

"Working people should not be the target of lowering inflation," Schuler added, "it should be corporations that are earning record profits."

Anticipating Wednesday's rate hike, Groundwork Collaborative chief economist Rakeen Mabud argued Tuesday that the move is a "misguided policy with catastrophic outcomes for the millions around the country who are already struggling to make ends meet."

"The Fed's rate-hiking frenzy is doing everything but lowering prices," she said. "Wage growth is slowing and mortgage rates are the highest in 20 years. If Powell wants to be taken seriously as a responsible steward of the economy, he should think twice before raising rates again."

Progressive former U.S. Labor Secretary Robert Reich tweeted: "Memo to the Fed: Interest rate hikes aren't working because inflation is being driven by corporations using it as cover to price gouge the people."