Since taking office in January, President Donald Trump has chosen ex-Goldman Sachs bankers to fill several key positions within his administration. According to a Wall Street Journal analysis published Sunday, it appears that the nation's largest financial institutions are benefiting greatly from having their friends in government.

"The Wall Street bankers against whom Trump ran are making policy now."

--Robert Weismann, Public Citizen"Wall Street regulators have imposed far lower penalties in the first six months of Donald Trump's presidency than they did during the first six months of 2016, a comparable period in the Obama administration," the Journal reported.

Throughout his campaign for the presidency, Trump promised to loosen regulations on big banks by dismantling Dodd-Frank, which was established following the financial crisis of 2008.

But the Journal's report indicates that the Trump team has found another way to ease up on Wall Street: namely, by not levying hefty fines for wrongdoing.

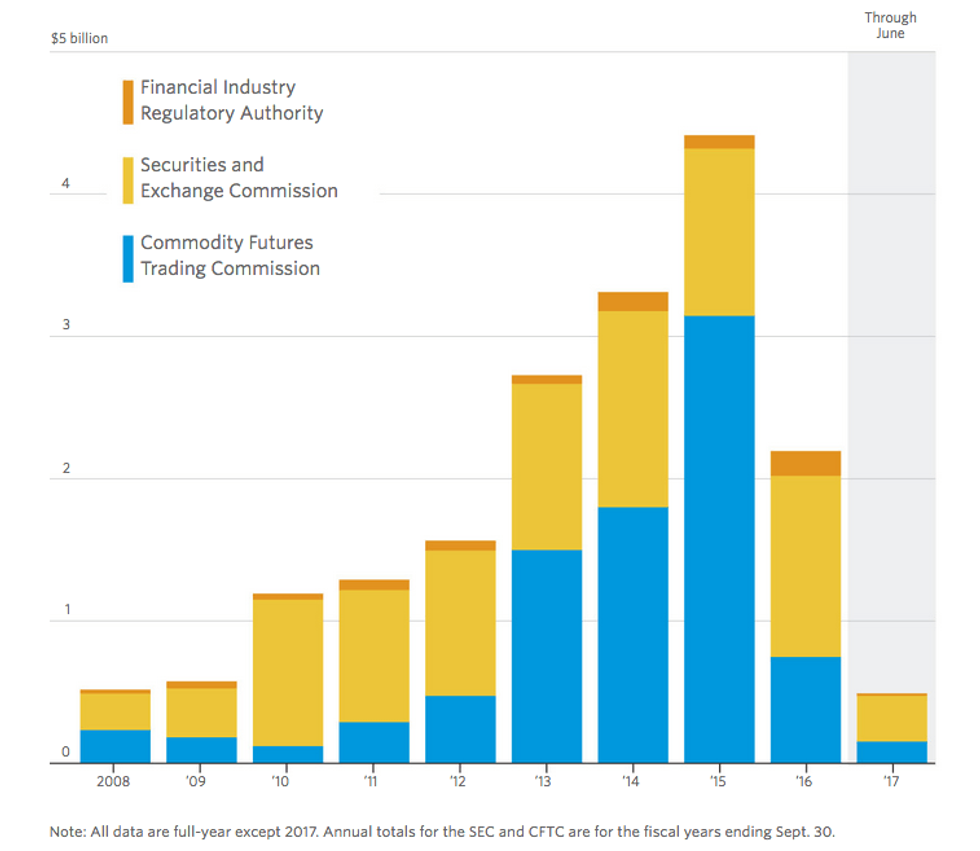

Attributing the rapid drop in fines to the "shift to a business-friendly stance at regulatory agencies," the Journal notes that "[p]enalties levied against firms and individuals by the Securities and Exchange Commission, the Commodity Futures Trading Commission, and the Financial Industry Regulatory Authority in the first half of 2017 were down nearly two-thirds compared with the first half of 2016."

This, the Journal adds, "put[s] regulators on track for the lowest annual level of fines since at least 2010," and Wall Street continues to lobby in favor of lowering this level even further.

Critics have argued that Trump's decision to fill his administration with bankers is conclusive evidence that his populist pro-worker rhetoric was always a sham.

"The Wall Street bankers against whom Trump ran are making policy now," Robert Weissman, president of watchdog group Public Citizen, said back in February.

In response to the Journal's analysis, Gary Rosen, editor of the Journal's Weekend Review, remarked: "You do have to wonder when working-class Trump supporters will start to notice such things."

As Common Dreams has reported, the Trump administration has over the last several weeks taken concrete steps toward relieving Wall Street of even the most basic restrictions and exposing consumers to the potentially devastating consequences. Recent reports indicate that he is now looking to repeal the Volcker rule, which was designed to prevent risky trading and betting.

Sen. Elizabeth Warren (D-Mass.) has argued--echoing consumer advocacy groups--that such moves, if successful, would "make it easier for big banks to cheat their customers and spark another financial meltdown."

Since taking office in January, President Donald Trump has chosen ex-Goldman Sachs bankers to fill several key positions within his administration. According to a Wall Street Journal analysis published Sunday, it appears that the nation's largest financial institutions are benefiting greatly from having their friends in government.

"The Wall Street bankers against whom Trump ran are making policy now."

--Robert Weismann, Public Citizen"Wall Street regulators have imposed far lower penalties in the first six months of Donald Trump's presidency than they did during the first six months of 2016, a comparable period in the Obama administration," the Journal reported.

Throughout his campaign for the presidency, Trump promised to loosen regulations on big banks by dismantling Dodd-Frank, which was established following the financial crisis of 2008.

But the Journal's report indicates that the Trump team has found another way to ease up on Wall Street: namely, by not levying hefty fines for wrongdoing.

Attributing the rapid drop in fines to the "shift to a business-friendly stance at regulatory agencies," the Journal notes that "[p]enalties levied against firms and individuals by the Securities and Exchange Commission, the Commodity Futures Trading Commission, and the Financial Industry Regulatory Authority in the first half of 2017 were down nearly two-thirds compared with the first half of 2016."

This, the Journal adds, "put[s] regulators on track for the lowest annual level of fines since at least 2010," and Wall Street continues to lobby in favor of lowering this level even further.

Critics have argued that Trump's decision to fill his administration with bankers is conclusive evidence that his populist pro-worker rhetoric was always a sham.

"The Wall Street bankers against whom Trump ran are making policy now," Robert Weissman, president of watchdog group Public Citizen, said back in February.

In response to the Journal's analysis, Gary Rosen, editor of the Journal's Weekend Review, remarked: "You do have to wonder when working-class Trump supporters will start to notice such things."

As Common Dreams has reported, the Trump administration has over the last several weeks taken concrete steps toward relieving Wall Street of even the most basic restrictions and exposing consumers to the potentially devastating consequences. Recent reports indicate that he is now looking to repeal the Volcker rule, which was designed to prevent risky trading and betting.

Sen. Elizabeth Warren (D-Mass.) has argued--echoing consumer advocacy groups--that such moves, if successful, would "make it easier for big banks to cheat their customers and spark another financial meltdown."

Since taking office in January, President Donald Trump has chosen ex-Goldman Sachs bankers to fill several key positions within his administration. According to a Wall Street Journal analysis published Sunday, it appears that the nation's largest financial institutions are benefiting greatly from having their friends in government.

"The Wall Street bankers against whom Trump ran are making policy now."

--Robert Weismann, Public Citizen"Wall Street regulators have imposed far lower penalties in the first six months of Donald Trump's presidency than they did during the first six months of 2016, a comparable period in the Obama administration," the Journal reported.

Throughout his campaign for the presidency, Trump promised to loosen regulations on big banks by dismantling Dodd-Frank, which was established following the financial crisis of 2008.

But the Journal's report indicates that the Trump team has found another way to ease up on Wall Street: namely, by not levying hefty fines for wrongdoing.

Attributing the rapid drop in fines to the "shift to a business-friendly stance at regulatory agencies," the Journal notes that "[p]enalties levied against firms and individuals by the Securities and Exchange Commission, the Commodity Futures Trading Commission, and the Financial Industry Regulatory Authority in the first half of 2017 were down nearly two-thirds compared with the first half of 2016."

This, the Journal adds, "put[s] regulators on track for the lowest annual level of fines since at least 2010," and Wall Street continues to lobby in favor of lowering this level even further.

Critics have argued that Trump's decision to fill his administration with bankers is conclusive evidence that his populist pro-worker rhetoric was always a sham.

"The Wall Street bankers against whom Trump ran are making policy now," Robert Weissman, president of watchdog group Public Citizen, said back in February.

In response to the Journal's analysis, Gary Rosen, editor of the Journal's Weekend Review, remarked: "You do have to wonder when working-class Trump supporters will start to notice such things."

As Common Dreams has reported, the Trump administration has over the last several weeks taken concrete steps toward relieving Wall Street of even the most basic restrictions and exposing consumers to the potentially devastating consequences. Recent reports indicate that he is now looking to repeal the Volcker rule, which was designed to prevent risky trading and betting.

Sen. Elizabeth Warren (D-Mass.) has argued--echoing consumer advocacy groups--that such moves, if successful, would "make it easier for big banks to cheat their customers and spark another financial meltdown."