SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

An analysis published in Forbes this week--just ahead of Friday's federal jobs report--challenges the argument from many GOP politicians, including President Donald Trump, that rapidly reopening businesses and loosening restrictions in the midst of the coronavirus pandemic is somehow good for the economy.

The United States continues to lead the world in Covid-19 cases and deaths, with over 4.9 million and at least 160,737, respectively. As the crisis was officially declared a pandemic at the global level in March, and in the absence of serious mitigation actions from the Trump administration or Congress, many U.S. cities and states imposed stay-at-home orders to curb the spread of the virus.

The new analysis from economist and Forbes senior contributor Christian Weller compared states with longer stay-at-home orders and that are gradually reopening--such as Massachusetts, New York, and Washington--with those like Florida, Georgia, and Texas, which have had shorter orders and "aggressively reopened." The latter states have seen spikes in cases and deaths.

Rather than focusing on the health impacts of swiftly reopening, Weller looked at the share of residents missing or deferring rent or mortgage payments, lost earnings, employment, food insufficiency, and expectations about housing costs and future financial losses, based on data from the U.S. Census' Household Pulse Survey and Opportunity Insights' tracktherecovery.org.

The new analysis, which added not only more weeks of data but also information on whether or not people had jobs, "provides more evidence that re-opening quickly and risking public health does not come with economic benefits," Weller explained, highlighting the rent and employment findings.

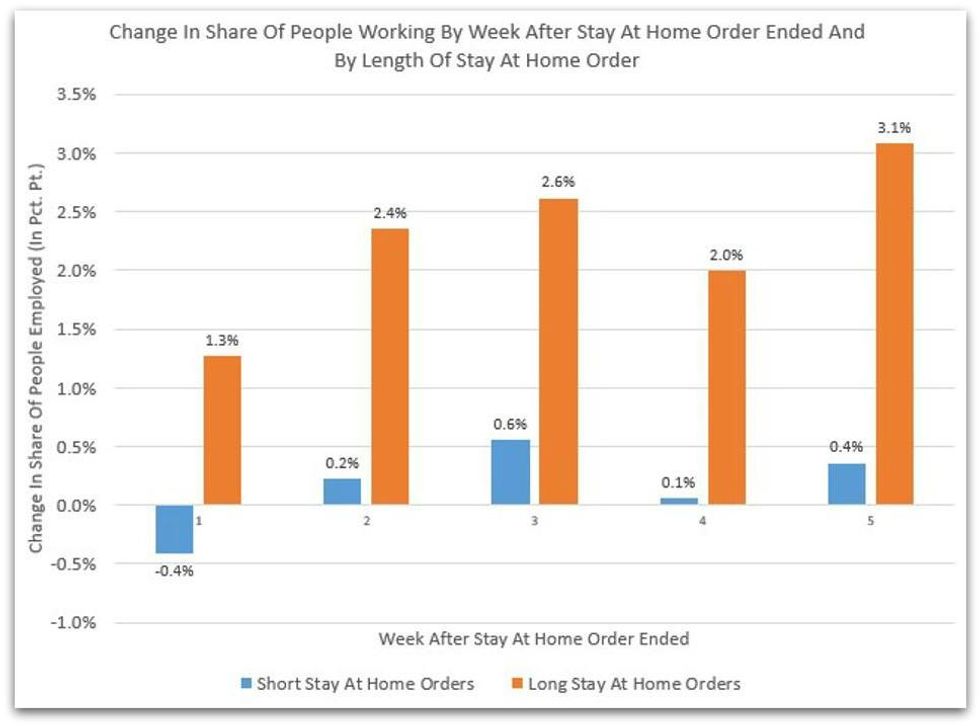

"The additional weeks of data also allow for a somewhat different analysis that illustrates these two different paths after reopening on a week-by-week basis," Weller continued. "All states that had a stay-at-home orders have been open for at least five weeks. The progress for states with cautious health measures versus risky ones looks remarkably different over those five weeks."

Although the second figure included in the report focuses only on the share of people working each week after local orders ended, "the same pattern emerges for other indicators," he noted. "A little over month after opening up, states that aggressively forged ahead and put their people's lives at risk got an economic whimper rather than a bang."

The Forbes report served as an update to a similar July 20 piece that Weller, a Center for American Progress senior fellow and professor of public policy at the University of Massachusetts Boston, co-authored with Ryan Zamarripa, CAP's associate director of economic policy. The key takeaways from the data, Weller wrote for Forbes, are clear.

"There is no way around it: getting the economy back on track means controlling the pandemic. There are no short cuts. Putting people's lives at risk and wishing the virus away are not going to produce a magic economic recovery," the economist argued.

"The second lesson from the data is that no state is an island. All state economies are connected with each other," he added. "No single state can forge its own path out of the pandemic. Because controlling the pandemic first is essential, it is then also clear that the federal government needs to develop, implement, and sustain a national strategy to fight the pandemic. It also needs to lead on combating the economic fallout from the pandemic."

Specifically, Weller called on Congress and the White House to urgently pursue "targeted, large, and sustained fiscal interventions" such as expanded unemployment benefits and paid leave policies, more stimulus payments, and financial assistance for struggling businesses as well as state and local governments.

Federal policymakers, he argued, "need to act soon and stop treating protecting the public's health and seeding an economic recovery as conflicting goals."

Despite such demands and the desperate levels of need for relief throughout the country, White House officials and Democratic leaders on Friday failed to strike a deal on another congressional recovery package, Politico reported. Treasury Secretary Steven Mnuchin and White House Chief of Staff Mark Meadows said they would urge Trump to move forward with some related executive orders.

The "last-ditch meeting" on the deal followed the Labor Department's morning release of the July jobs reports. As the Associated Press noted, the report revealed the U.S. added 1.8 million jobs last month, "a pullback from the gains of May and June and evidence that the resurgent coronavirus has weakened hiring and the economic rebound."

The new jobs report, according to Glassdoor economist Daniel Zhao, "exposes cracks in efforts to reopen as employers struggle to deal with resurgent outbreaks around the country" and "increases the pressure on policymakers to extend financial relief to avoid the slowdown from turning into a full-blown double-dip recession."

Echoing Weller's argument in Forbes, Zhao said that "the slowdown in the rate of recovery amid a worsening pandemic shows that a sustainable return to economic normal is hinged on first addressing the public health crisis."

"Today's jobs report comes at a critical juncture," he continued. "Not only is it the first jobs report to capture the impact of the resurgent pandemic on American workers, it also coincides with congressional negotiations on financial relief for many millions of Americans."

"And with less than three months until the election," Zhao added, "attention on the coming jobs reports will likely heighten."

An analysis published in Forbes this week--just ahead of Friday's federal jobs report--challenges the argument from many GOP politicians, including President Donald Trump, that rapidly reopening businesses and loosening restrictions in the midst of the coronavirus pandemic is somehow good for the economy.

The United States continues to lead the world in Covid-19 cases and deaths, with over 4.9 million and at least 160,737, respectively. As the crisis was officially declared a pandemic at the global level in March, and in the absence of serious mitigation actions from the Trump administration or Congress, many U.S. cities and states imposed stay-at-home orders to curb the spread of the virus.

The new analysis from economist and Forbes senior contributor Christian Weller compared states with longer stay-at-home orders and that are gradually reopening--such as Massachusetts, New York, and Washington--with those like Florida, Georgia, and Texas, which have had shorter orders and "aggressively reopened." The latter states have seen spikes in cases and deaths.

Rather than focusing on the health impacts of swiftly reopening, Weller looked at the share of residents missing or deferring rent or mortgage payments, lost earnings, employment, food insufficiency, and expectations about housing costs and future financial losses, based on data from the U.S. Census' Household Pulse Survey and Opportunity Insights' tracktherecovery.org.

The new analysis, which added not only more weeks of data but also information on whether or not people had jobs, "provides more evidence that re-opening quickly and risking public health does not come with economic benefits," Weller explained, highlighting the rent and employment findings.

"The additional weeks of data also allow for a somewhat different analysis that illustrates these two different paths after reopening on a week-by-week basis," Weller continued. "All states that had a stay-at-home orders have been open for at least five weeks. The progress for states with cautious health measures versus risky ones looks remarkably different over those five weeks."

Although the second figure included in the report focuses only on the share of people working each week after local orders ended, "the same pattern emerges for other indicators," he noted. "A little over month after opening up, states that aggressively forged ahead and put their people's lives at risk got an economic whimper rather than a bang."

The Forbes report served as an update to a similar July 20 piece that Weller, a Center for American Progress senior fellow and professor of public policy at the University of Massachusetts Boston, co-authored with Ryan Zamarripa, CAP's associate director of economic policy. The key takeaways from the data, Weller wrote for Forbes, are clear.

"There is no way around it: getting the economy back on track means controlling the pandemic. There are no short cuts. Putting people's lives at risk and wishing the virus away are not going to produce a magic economic recovery," the economist argued.

"The second lesson from the data is that no state is an island. All state economies are connected with each other," he added. "No single state can forge its own path out of the pandemic. Because controlling the pandemic first is essential, it is then also clear that the federal government needs to develop, implement, and sustain a national strategy to fight the pandemic. It also needs to lead on combating the economic fallout from the pandemic."

Specifically, Weller called on Congress and the White House to urgently pursue "targeted, large, and sustained fiscal interventions" such as expanded unemployment benefits and paid leave policies, more stimulus payments, and financial assistance for struggling businesses as well as state and local governments.

Federal policymakers, he argued, "need to act soon and stop treating protecting the public's health and seeding an economic recovery as conflicting goals."

Despite such demands and the desperate levels of need for relief throughout the country, White House officials and Democratic leaders on Friday failed to strike a deal on another congressional recovery package, Politico reported. Treasury Secretary Steven Mnuchin and White House Chief of Staff Mark Meadows said they would urge Trump to move forward with some related executive orders.

The "last-ditch meeting" on the deal followed the Labor Department's morning release of the July jobs reports. As the Associated Press noted, the report revealed the U.S. added 1.8 million jobs last month, "a pullback from the gains of May and June and evidence that the resurgent coronavirus has weakened hiring and the economic rebound."

The new jobs report, according to Glassdoor economist Daniel Zhao, "exposes cracks in efforts to reopen as employers struggle to deal with resurgent outbreaks around the country" and "increases the pressure on policymakers to extend financial relief to avoid the slowdown from turning into a full-blown double-dip recession."

Echoing Weller's argument in Forbes, Zhao said that "the slowdown in the rate of recovery amid a worsening pandemic shows that a sustainable return to economic normal is hinged on first addressing the public health crisis."

"Today's jobs report comes at a critical juncture," he continued. "Not only is it the first jobs report to capture the impact of the resurgent pandemic on American workers, it also coincides with congressional negotiations on financial relief for many millions of Americans."

"And with less than three months until the election," Zhao added, "attention on the coming jobs reports will likely heighten."

An analysis published in Forbes this week--just ahead of Friday's federal jobs report--challenges the argument from many GOP politicians, including President Donald Trump, that rapidly reopening businesses and loosening restrictions in the midst of the coronavirus pandemic is somehow good for the economy.

The United States continues to lead the world in Covid-19 cases and deaths, with over 4.9 million and at least 160,737, respectively. As the crisis was officially declared a pandemic at the global level in March, and in the absence of serious mitigation actions from the Trump administration or Congress, many U.S. cities and states imposed stay-at-home orders to curb the spread of the virus.

The new analysis from economist and Forbes senior contributor Christian Weller compared states with longer stay-at-home orders and that are gradually reopening--such as Massachusetts, New York, and Washington--with those like Florida, Georgia, and Texas, which have had shorter orders and "aggressively reopened." The latter states have seen spikes in cases and deaths.

Rather than focusing on the health impacts of swiftly reopening, Weller looked at the share of residents missing or deferring rent or mortgage payments, lost earnings, employment, food insufficiency, and expectations about housing costs and future financial losses, based on data from the U.S. Census' Household Pulse Survey and Opportunity Insights' tracktherecovery.org.

The new analysis, which added not only more weeks of data but also information on whether or not people had jobs, "provides more evidence that re-opening quickly and risking public health does not come with economic benefits," Weller explained, highlighting the rent and employment findings.

"The additional weeks of data also allow for a somewhat different analysis that illustrates these two different paths after reopening on a week-by-week basis," Weller continued. "All states that had a stay-at-home orders have been open for at least five weeks. The progress for states with cautious health measures versus risky ones looks remarkably different over those five weeks."

Although the second figure included in the report focuses only on the share of people working each week after local orders ended, "the same pattern emerges for other indicators," he noted. "A little over month after opening up, states that aggressively forged ahead and put their people's lives at risk got an economic whimper rather than a bang."

The Forbes report served as an update to a similar July 20 piece that Weller, a Center for American Progress senior fellow and professor of public policy at the University of Massachusetts Boston, co-authored with Ryan Zamarripa, CAP's associate director of economic policy. The key takeaways from the data, Weller wrote for Forbes, are clear.

"There is no way around it: getting the economy back on track means controlling the pandemic. There are no short cuts. Putting people's lives at risk and wishing the virus away are not going to produce a magic economic recovery," the economist argued.

"The second lesson from the data is that no state is an island. All state economies are connected with each other," he added. "No single state can forge its own path out of the pandemic. Because controlling the pandemic first is essential, it is then also clear that the federal government needs to develop, implement, and sustain a national strategy to fight the pandemic. It also needs to lead on combating the economic fallout from the pandemic."

Specifically, Weller called on Congress and the White House to urgently pursue "targeted, large, and sustained fiscal interventions" such as expanded unemployment benefits and paid leave policies, more stimulus payments, and financial assistance for struggling businesses as well as state and local governments.

Federal policymakers, he argued, "need to act soon and stop treating protecting the public's health and seeding an economic recovery as conflicting goals."

Despite such demands and the desperate levels of need for relief throughout the country, White House officials and Democratic leaders on Friday failed to strike a deal on another congressional recovery package, Politico reported. Treasury Secretary Steven Mnuchin and White House Chief of Staff Mark Meadows said they would urge Trump to move forward with some related executive orders.

The "last-ditch meeting" on the deal followed the Labor Department's morning release of the July jobs reports. As the Associated Press noted, the report revealed the U.S. added 1.8 million jobs last month, "a pullback from the gains of May and June and evidence that the resurgent coronavirus has weakened hiring and the economic rebound."

The new jobs report, according to Glassdoor economist Daniel Zhao, "exposes cracks in efforts to reopen as employers struggle to deal with resurgent outbreaks around the country" and "increases the pressure on policymakers to extend financial relief to avoid the slowdown from turning into a full-blown double-dip recession."

Echoing Weller's argument in Forbes, Zhao said that "the slowdown in the rate of recovery amid a worsening pandemic shows that a sustainable return to economic normal is hinged on first addressing the public health crisis."

"Today's jobs report comes at a critical juncture," he continued. "Not only is it the first jobs report to capture the impact of the resurgent pandemic on American workers, it also coincides with congressional negotiations on financial relief for many millions of Americans."

"And with less than three months until the election," Zhao added, "attention on the coming jobs reports will likely heighten."