SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

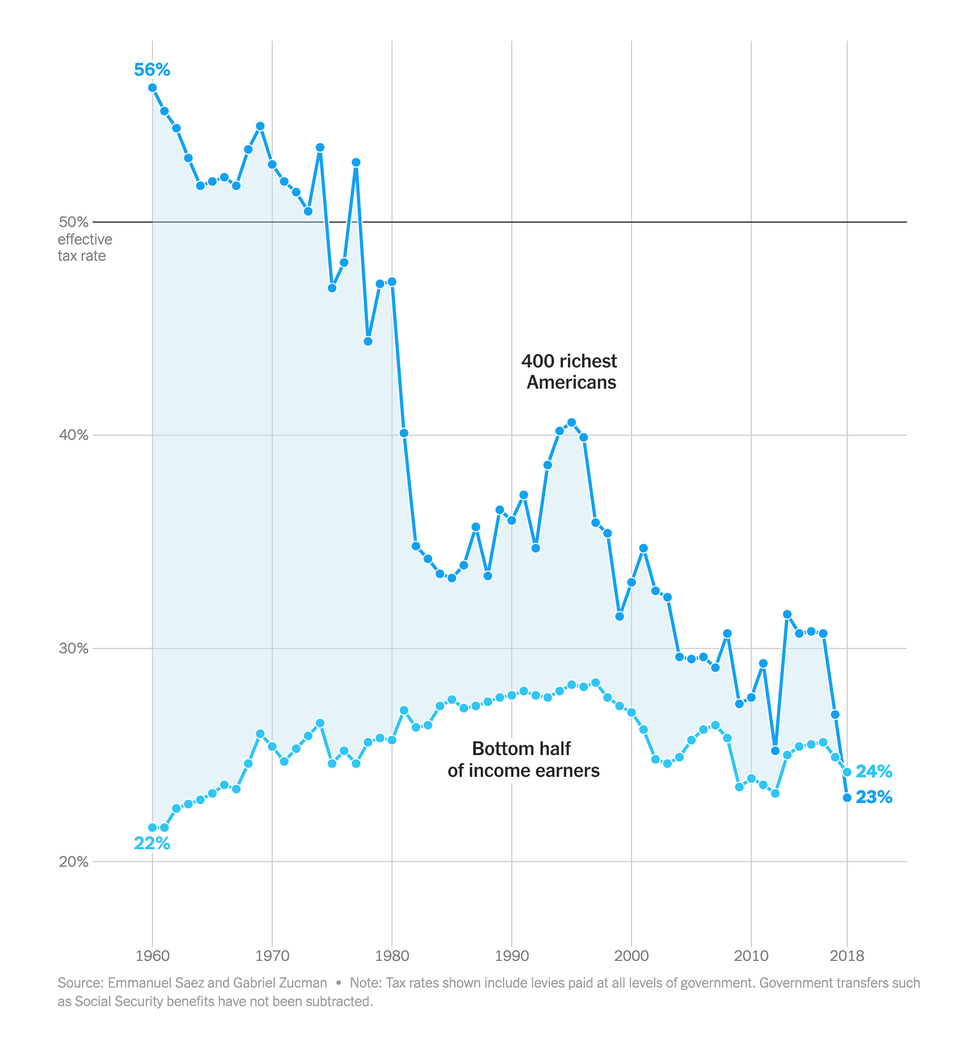

Stock gains aren't currently taxed in the U.S. until the underlying asset is sold, leaving billionaires like Amazon founder Jeff Bezos and Tesla CEO Elon Musk—a pair frequently competing to be the single richest man on the planet—with very little taxable income.

"But they can still make eye-popping purchases by borrowing against their assets," Zucman noted. "Mr. Musk, for example, used his shares in Tesla as collateral to rustle up around $13 billion in tax-free loans to put toward his acquisition of Twitter."

To begin reversing the decades-long trend of surging inequality that has weakened democratic institutions and undermined critical programs such as Social Security, Zucman made the case for a minimum tax on billionaires in the U.S. and around the world.

"The idea that billionaires should pay a minimum amount of income tax is not a radical idea," Zucman wrote Friday. "What is radical is continuing to allow the wealthiest people in the world to pay a smaller percentage in income tax than nearly everybody else. In liberal democracies, a wave of political sentiment is building, focused on rooting out the inequality that corrodes societies. A coordinated minimum tax on the super-rich will not fix capitalism. But it is a necessary first step."

Responding to those who claim a minimum tax would be impractical because "wealth is difficult to value," Zucman wrote that "this fear is overblown."

"According to my research, about 60% of U.S. billionaires' wealth is in stocks of publicly traded companies," the economist observed. "The rest is mostly ownership stakes in private businesses, which can be assigned a monetary value by looking at how the market values similar firms."

Since 2018, the final year examined in Zucman's analysis, the wealth of global billionaires has continued to explode while worker pay has been largely stagnant. As of last month, there were a record 2,781 billionaires worldwide with combined assets of $14.2 trillion.

The U.S. has more billionaires than any other country, with 813 individuals worth a combined $5.7 trillion.

"The ultra-wealthy are paying less in taxes than the bottom half of income earners. That's absurd!" Rakeen Mabud, chief economist at the Groundwork Collaborative, wrote in response to Zucman's analysis. "We've got to raise taxes on the wealthy and large corporations. Enough with the wealth hoarding. It's past time for us to take back what's ours."

U.S. Sen. Sheldon Whitehouse (D-R.I.), chair of the Senate Budget Committee, called the figures assembled by Zucman "disgraceful" and said that "not only can we fix this, we can make Social Security and Medicare safe and sound as far as the eye can see."