SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

In advance of the House Judiciary Committee holding a hearing on Thursday, July 13, 2023, at 10:00 a.m. ET on "Oversight of the Federal Trade Commission," Revolving Door Project has sent a letter to FTC Chair Lina Khan calling on her to take on the FTC's considerable internal revolving door challenges. In light of recent disclosures that the FTC ethics official judging an ethics complaint from Meta was herself a Meta shareholder and that recent FTC career officials are being scooped up by various BigTech firms, Khan must prioritize strengthening ethics at the FTC.

In the face of supplier driven inflation and a wave of anti-consumer scams across the economy, now more than ever Americans required an FTC that is beyond reproach ethically. The FTC's our public servants must spend each day protecting American consumers and workers, rather than preserving their stock portfolios or dreaming of a lucrative job helping current or would be monopolists undermine antitrust law.

Revolving Door Project's letter can be found here.

Additionally relevant past Revolving Door Project work can be found here.

The Revolving Door Project (RDP) scrutinizes executive branch appointees to ensure they use their office to serve the broad public interest, rather than to entrench corporate power or seek personal advancement.

"Only a select few in the top tax bracket are benefiting from this, and the majority of you ain’t in it," said former Rep. Marjorie Taylor Greene.

Observers are once again raising concerns about insider trading on Wednesday after a trader took a colossal crude oil short position just over an hour before a US-Iran peace deal was reported to be on the horizon, causing prices to fall.

The Kobeissi Letter, a financial newsletter, reported on X that at 3:40 am on Wednesday, "nearly 10,000 contracts worth of crude oil shorts were taken without any major news."

This was equivalent to $920 million in notional value, which the letter described as "an unusually large trade" so early in the morning. But it would soon pay off.

At 4:50 am, just 70 minutes later, Axios published an exclusive scoop by Middle East reporter Barak Ravid that the White House believed the US and Iran were on the verge of agreeing to a one-page "memorandum of understanding" to end the war, which included more nuclear negotiations, one of the key sticking points for US President Donald Trump.

By 7:00 am, just over two hours after Axios dropped its report, oil prices had fallen by 12%, allowing the savvy investor to make $125 million in a matter of hours, which led to accusations that it was yet another example of "epic insider trading" by those in the know about Trump's plans.

Prices have since rebounded by about 8% after Iran announced the creation of the new "Persian Gulf Strait Authority," to mediate the passage of ships through the Strait of Hormuz on its terms.

The Trump administration has already been deluged with accusations that its members are using insider information to take advantage of financial markets and prediction market apps.

Last month, an active-duty US special forces soldier was indicted by the Department of Justice after he made about $400,000 betting on Polymarket that Venezuelan President Nicolás Maduro would be removed from power, a bet he allegedly placed using classified information about an operation he himself was involved with.

More bettors collected around $1 million in profits from bets on the specific timing of Trump's war with Iran in late February. The Financial Times also reported a surge of more than $580 million in oil futures trading right before Trump announced a pause in strikes on Iran's energy facilities in March.

Of course, Wednesday's bet theoretically could have been made without the aid of insider information.

The new peace framework is the latest in what has seemed to be an endless pattern over the past several weeks in which US officials tell media outlets that a peace agreement is on the horizon, causing oil prices to dip, only for it to collapse later in the week, often with Trump issuing hostile threats or making new demands.

It has become such a familiar story that some have speculated that the announcement of productive ceasefire talks is deliberately choreographed to calm oil markets and bring down prices, which have become a growing problem for Trump among voters.

But as The Economic Times explained, the bet placed Wednesday morning likely "is not a routine hedge" or "a portfolio rebalancing move."

"At that hour, in that size," it said, "a crude oil short of that magnitude is a deliberate, high-conviction directional bet."

Former Rep. Marjorie Taylor Greene (R-Ga.), a one-time Trump cheerleader who's become one of his leading critics, suggested Trump's erratic approach to negotiating an end to the war was just a tool used by him and his allies to profit.

"When is everyone going to start realizing that the on-again, off-again war/peace rhetoric is really just insider trading? And sprinkle in some murder," Greene wrote on social media. "Only a select few in the top tax bracket are benefiting from this, and the majority of you ain’t in it."

Democrats in Congress have urged the Securities and Exchange Commission (SEC) to investigate what Sen. Chris Murphy (D-Conn.) suggested could be "mind-blowing corruption" by the White House, not only related to Trump's wars, but also to his tariff regime, which has caused similar market chaos that bettors have been able to capitalize on with fortuitously timed wagers.

But critics have described profiting from the machinations of a war that has killed more than 1,700 civilians as particularly grotesque.

"This has to stop," said Fox News commentator Jessica Tarlov. "Lives on the line so they can insider trade!"

"Reckless actions on the economy and the expensive fallout from the war in Iran has made it harder for working families to purchase a car and has left millions more feeling major pocket pain at the pump," one researcher said.

As Americans on Wednesday continued to face the economic fallout of President Donald Trump's war on Iran, a gallon of gasoline cost $4.536, the average transaction price for a new vehicle was $49,275, and a pair of progressive groups published a report detailing "how surging auto loan debt is hurting households."

"The costs of purchasing and financing a car have been going up for years," noted Protect Borrowers senior fellow Tara Mikkilineni, who co-authored the report, "When The Wheels Come Off," with other experts from her organization and The Century Foundation.

"Unfortunately, the Trump administration's reckless actions on the economy and the expensive fallout from the war in Iran has made it harder for working families to purchase a car and has left millions more feeling major pocket pain at the pump," Mikkilineni said. "For millions of working families, a car is not a luxury, it is an essential economic lifeline. Working families deserve relief and they deserve to have a government that is watching out for them, not allowing lenders and auto dealers to rake in record profits at their expense."

Mikkilineni's team found that "in recent years, aggregate total auto debt has reached $1.68 trillion, a 37% jump since early 2018, and now comprises the largest volume of outstanding loan debt ever recorded. At the end of 2025, nearly 86 million Americans—roughly 28% of consumers—have outstanding auto loan or lease debt. Residents in states where driving is most necessary, such as Texas, Alaska, Louisiana, and Florida, are struggling with the highest levels of auto debt."

"Borrowers carrying auto loans see significantly higher and faster credit card balance growth—regardless of income level—suggesting that auto debt cascades into broader financial pressure," according to the report. Specifically, "between early 2018 and late 2025, credit card balances for middle-income borrowers with auto debt surged by 31%, while those without auto loans saw a notably lower growth of 17%. Borrowers with extended-length auto loans are carrying monthly balances on their credit cards that are 190% of (that is, nearly twice) their monthly income."

"At the end of 2025, the average origination balance for an auto loan reached $33,519, an amount $10,000 higher than the average in 2018, due to massive increases in the price of even the most basic cars and a shortage of 'affordable' car models," the publication explains. "Borrowers are also facing higher interest rates. Today, the average annual percentage rate (APR) for auto loans is nearly 10%, up from 7.5% in 2018."

Financially vulnerable borrowers are being hit particularly hard by current conditions. The researchers found that for those with the most limited access to credit, "the average APR is up to 18.7%, which means a six-year loan on a $30,000 car will cost $20,000 in interest alone. Furthermore, Black, Hispanic, and American Indian and Alaska Native borrowers face higher interest rates than their white and Asian counterparts."

NEW from @cnbc.com: Auto debt is crushing families. Our new report with @borrowerjustice.bsky.social shows that 86 million Americans owe a staggering $1.68 trillion in auto loan debt, with auto debt now reaching the highest level ever recorded. www.cnbc.com/2026/05/06/c...

[image or embed]

— The Century Foundation (@tcfdotorg.bsky.social) May 6, 2026 at 10:24 AM

Affordable vehicles are also harder to find these days. Sean Tucker, a managing editor at Kelley Blue Book, told CNBC that "in 2017, [automakers] built 36 models priced at $25,000 or under... Today? Four."

Tucker said that a "record" share of new cars—over 43%—are now bought by households with incomes of at least $150,000. According to him, "Automakers are serving that market."

Angela Hanks, another report co-author and chief of policy programs at The Century Foundation, stressed that "for the overwhelming majority of working families, a car is a necessity—yet purchasing a car has become a financial trap, eating up more of people's paychecks than ever before."

With so many US communities lacking quality public transit, some US families in need of a vehicle turn to loans with longer terms. The report points out that "for these borrowers, even after taking on these riskier products with additional lifetime costs, auto loan payments are still nearly 20% of their monthly income, meaning nearly $1 out of every $5 they earn will go toward car payments over the seven years of their loan."

Hanks highlighted that "while families drown" from costly, extended-term loans, "the Trump administration is refunding big businesses for the tariffs that consumers paid, with interest."

The Trump administration last month launched a portal designed to facilitate refunds for around $166 billion in tariffs that the US Supreme Court struck down as unconstitutional, but only businesses that directly paid the import taxes are eligible, even though companies largely passed on the cost hikes to consumers.

Meanwhile, the president responded to the high court's decision by imposing temporary import taxes, and his administration is pursuing "plan B," holding hearings required to impose tariffs under Section 301 of the Trade Act of 1974, a different legal authority than the one Trump used last year.

The new report concludes by calling on US policymakers to act: "Amidst the growing affordability crisis, Americans deserve urgent action to bring down costs and rein in profiteering from the dealers and lenders who have been allowed to get away with nickel-and-diming working families for far too long."

"Is this supposed to be a brag?" said Democratic US Rep. Mark Pocan.

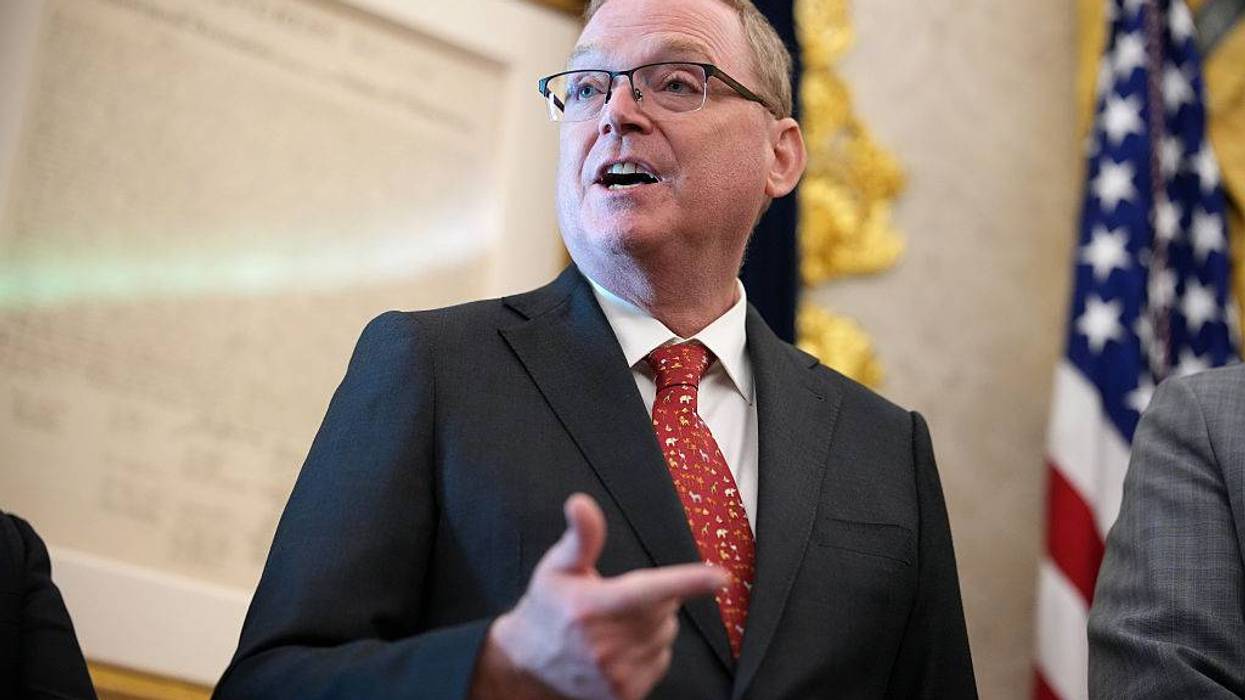

National Economic Council Director Kevin Hassett on Wednesday tried to put a rosy spin on President Donald Trump's economy by highlighting the large credit card bills being racked up by US consumers.

During an interview on Fox Business, Hassett cited credit card spending as a purported sign of strength in the economy as a whole.

"I had the head of one of the Big Five banks in my office yesterday, going through credit card data," he said. "Credit card spending is through the roof! They're spending more on gasoline, but they're spending more on everything else too."

Hassett on American consumers: "Credit card spending is through the roof. They're spending more on gasoline, but they're spending more on everything else too." pic.twitter.com/zayCSaxhwr

— Aaron Rupar (@atrupar) May 6, 2026

The price of oil has been surging since Trump launched an illegal war with Iran in late February, and on Wednesday the average price for a gallon of gasoline in the US topped $4.50, a high not seen since 2022 in the wake of Russia's invasion of Ukraine.

As the Iran crisis persists, economists project that the price of energy will be reflected in increases in other consumer goods, most notably food.

Given this, many critics were astonished that Hassett decided to brag about consumer credit card spending as a way to reassure Americans concerned about the economy.

"Working-class Americans are maxing out their credit cards to pay for groceries and gas," wrote House Minority Leader Hakeem Jeffries (D-NY). "The Trump Cartel thinks this is something to celebrate. Shameful."

Hassett's claims about credit card spending also earned a swift rebuke from Warren Gunnels, staff director for Sen. Bernie Sanders (I-Vt.).

"Americans are putting more stuff on credit cards because they don’t have enough money to pay for the skyrocketing cost of virtually everything," Gunnels wrote. "Trump promised to put a 10% cap on credit card interest rates. Instead, the average credit card interest rate today is 22%. Obscene."

Fred Wellman, a Democratic candidate for the US House of Representatives in Missouri, could not hide his disgust at Hassett's performance.

"He’s smiling," Wellman observed. "He's celebrating that we are all maxing out our credit cards because they have torched the economy. He’s not smiling for working people. He’s happy for the corporations and billionaires. It's good for them. We can all die poor. This is why I'm running for Congress."

Rep. Mark Pocan (D-Wis.) expressed bewilderment at Hassett's argument.

"Is this supposed to be a brag?" Pocan asked.

Jon Favreau, former speechwriter for President Barack Obama and current co-host of Pod Save America, found Hassett's messaging so tone-deaf that "we must consider the possibility that Kevin Hassett is secretly working for the Democrats."

The Democratic House Majority Political Action Committee had a response similar to Favreau's, recommending that the GOP make Hassett "the spokesperson for the entire Republican Party."