SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

“Consumers are getting really screwed by all of this,” said one critic.

Political appointees installed by President Donald Trump are overruling career attorneys inside the Department of Justice's Antitrust Division, intervening to weaken or halt investigations into major corporate mergers in a way never seen before, MS NOW reported Thursday.

Three unnamed sources told the outlet "that DOJ staff have privately complained that the Trump administration is essentially deciding not to enforce antitrust laws that are critical to keeping companies from becoming single-source providers and being able to charge enormous sums for their product or service."

According to MS NOW:

The two mergers that DOJ leaders are ramming through include two low-cost Mexican air carriers, Viva Aerobus and Volaris, who announced their plans to merge last year, and the proposed merger of the Italian firm Saipem and UK firm Subsea7, who together control a sizable portion of sales for equipment used for subsea oil operations. Major oil companies, including ExxonMobil, Petrobras and TotalEnergies, have filed formal objections with federal regulators about the latter merger, arguing to antitrust regulators that the combined firms will create a subsea monopoly that will increase costs, delay critical projects and force clients into expensive, long-term contracts.

Experts say the aforementioned mergers are likely to drive up prices US consumers pay for airfare to Mexico and at the gas pump, yet again giving the lie to Trump's "America First" pledge.

Current and former DOJ officials described Trump's interference as without precedent.

“It’s unilateral surrender on antitrust enforcement; it’s absolutely unprecedented,” Bill Baer, the former assistant attorney general for the antitrust division during the Obama administration. “It’s definitely going to hurt consumers. It means prices will go up, concentration is going to increase—and quality often diminishes when you have only a few firms operating in the same market.”

The DOJ Antitrust Division was originally launched more than a century ago during the tail-end of the Progressive Era to combat monopolies and enforce antitrust legislation like the Clayton Antitrust Act and the Gilded Age-era Sherman Act. It was formally created during the Great Depression following weak enforcement of the Sherman and Clayton acts, as the Franklin D. Roosevelt administration viewed concentrated corporate power as a threat not only to consumers but to democracy itself.

While the postwar decades saw relatively aggressive antitrust enforcement by presidents of both major parties, the Reagan administration adopted a much more permissive merger philosophy that laid the groundwork for decades of consolidation across industries that has continued to this day, despite limited antitrust revivals during the Obama and Biden administrations.

Biden-era Federal Trade Commission Chair Lina Khan and DOJ officials pursued a more aggressive antitrust agenda that Trump has been rolling back in favor of deregulation. Critics have pointed out that Trump has sometimes used antitrust mechanisms selectively, targeting certain media or technology companies for political reasons rather than consistently applying a broad anti-monopoly approach.

According to an article published last month in The Wall Street Journal, Stanley Woodward, the senior DOJ official now overseeing antitrust enforcement, has told department lawyers that he favors resolving cases through settlements rather than taking corporations to trial. Some antitrust attorneys interpreted the remarks as a directive to avoid litigation and seek settlements in ongoing and future cases. Critics say Woodward’s posture could weaken the DOJ's ability to challenge monopolistic mergers in favor of fast-tracked settlements.

"He's taking litigation off the table, and you don’t get a settlement absent a litigation threat,” one person with knowledge of Woodward's actions told MS NOW. “I can’t think of an administration in history that would want to run antitrust policy like this.”

“Consumers are getting really screwed by all of this,” the person continued. “We’re talking 10 years of consumer harm that can’t be undone.”

"These megautilities are merely using rising concern about data centers as an excuse to concentrate political and economic power of two giant utilities to maximize financial returns to shareholders," one advocate said.

Seeking to cash in on spiking energy demand from the expansion of artificial intelligence data centers across the US, the Florida energy giant NextEra announced a $67 billion deal on Monday to acquire Virginia's Dominion Energy.

But while the deal is expected to be lucrative for the massive new entity, with national power demands projected to spike perhaps by as much as 25% over the next five years, consumer advocates fear that the proposed merger will be bad for consumers, creating an unaccountable corporate behemoth that will raise costs on ratepayers.

According to Utility Dive, the new entity created by the merger will serve a combined 10 million customers across Florida, Virginia, North Carolina, and South Carolina.

With a market cap of $250 billion, the companies said they'd be the “world’s largest regulated electric utility business by market capitalization and one of the world’s largest energy infrastructure companies.”

But the deal still needs to be approved by federal regulators, a process that will likely pose minimal difficulty given the Trump administration's friendliness toward other corporate megamergers across industries, from media to railroads.

It will also be required to obtain local approvals, including in Virginia, where the recently elected Democratic Gov. Abigail Spanberger has made lowering utility costs and requiring data centers to "pay their fair share" central campaign promises, as massive new projects have been met with furious local backlash around the country.

Tyson Slocum, director of the energy program for the consumer advocacy watchdog Public Citizen, said that "this absurd proposal to merge two massive, well-capitalized utilities should be dead on arrival for state and federal regulators." He added that "household customers have everything to lose and nothing to gain by allowing two behemoths, NextEra and Dominion, to merge."

The company’s combined rate base—the value of assets recognized by regulators when setting rates—are valued at about $138 billion, according to the deal announcement. It said they plan to expand that value by 11% by 2032 with major infrastructure expansions.

Though the company has proposed offering $2.25 billion in credits to customers for two years after the deal closes, consumer advocates fear it is simply meant to ease upfront investment costs, leaving the real rate hikes to show up later once the credits expire.

The group Clean Virginia argued that the proposal needed to be subject “to the most rigorous scrutiny possible," given NextEra's "deeply troubling track record" in Florida.

The company and its subsidiaries in Florida have faced criticism for profiting from a $1.5 billion rate hike on Floridians and for pocketing $1 billion in tax savings without passing it on to consumers.

The company is also renowned for its extensive use of dark money to influence legislators in both parties, as well as Republican Florida Gov. Ron DeSantis, to kill clean energy and other policies that disfavor its business.

David Pomerantz, the executive director of the Energy and Policy Institute, told The New York Times that "a megamonopoly of this size, with the kind of money to buy political influence that NextEra will have, will be nearly impossible to regulate.”

NextEra CEO John Ketchum has said the deal is necessary to accommodate “America’s golden age of power demand.”

“Electricity demand is rising faster than it has in decades,” Ketchum said. “We are bringing NextEra Energy and Dominion Energy together because scale matters more than ever.”

But Slocum called this "a false narrative."

"The merger will do nothing to increase generating capacity, let alone desperately needed renewable generating capacity," he said. "These megautilities are merely using rising concern about data centers as an excuse to concentrate political and economic power of two giant utilities to maximize financial returns to shareholders."

He said federal and state regulators "should reject this outlandish, unnecessary merger as completely contrary to the public interest.“

The heads of the congressional Monopoly-Busters Caucus warned that a future administration could "break up" a merger of United and American Airlines if it is approved by Trump regulators.

The Democratic leaders of the congressional Monopoly-Busters Caucus said Wednesday that a recently floated megamerger of two of the largest airlines in the US—United and American—would be so awful for consumers that it shouldn't even be considered, let alone approved by federal regulators.

"The rumored scheme to merge United and American should never see the light of day," said Reps. Pramila Jayapal (D-Wash.), Chris Deluzio (D-Pa.), Pat Ryan (D-NY), and Angie Craig (D-Minn.). "This disaster of a merger would be illegal, consolidating more than a third of the US airline market, eliminating direct competitors on hundreds of routes across the country, and creating a near-monopoly on flights in many cities."

The House Democrats went on to say that if a United-American merger is formally proposed and approved by President Donald Trump's regulators, a future Democratic administration could break up the resulting airline behemoth.

"In a time when too many Americans just struggle to even go on vacation, much less afford their housing, childcare, and healthcare, these airline executives should not mistake the corruption of this administration as a green light to break the law," the lawmakers said. "They should also remember that there is no statute of limitations on breaking up bad deals."

"In case it is not crystal clear," they added, "that is absolutely a threat to break up this merger should it ever happen."

The lawmakers' statement came a day after Bloomberg reported that United Airlines (UA) CEO Scott Kirby floated the idea of merging his company with American Airlines (AA) "directly" to Trump during a meeting in late February. Kirby also pitched the merger idea to other "senior government officials," the outlet noted, without providing names.

"A combination would create the largest airline on the planet," Bloomberg observed. "As a result, any merger between the two aviation giants would pose serious antitrust concerns and likely face significant backlash from consumers, politicians and rival US airlines."

"That the United CEO raised the idea of a merger with American directly with Donald Trump suggests he thinks he might obtain direct approval from the president for a merger that would otherwise never be permitted.”

Contrary to claims of a "surging MAGA antitrust movement" in the early days of Trump's second White House term, the president's administration has proven friendly to corporate merger efforts, from Paramount-Skydance to UnitedHealth-Amedisys and more. Reuters reported Wednesday that "investment banking fees—earned from advising on mergers and acquisitions and underwriting deals—surged an average of 27% across six major US banks in the first quarter, with record dealmaking a key profit driver."

William McGee, senior fellow for aviation and travel at the American Economic Liberties Project, said Wednesday that "thanks to the federal preemption clause in the 1978 Airline Deregulation Act, states have virtually no airline oversight."

"So effectively the only sheriffs overseeing airlines are [the Department of Transportation] and [Department of Justice]," McGee observed. "Under Trump they've been derelict in policing competition."

"To be clear: A UA-AA merger is absurd," McGee added. "A monolith mega-mega-carrier operating 4 of every 10 domestic flights is so harmful that anyone favoring it doesn't understand airlines. Or is a regulator eager to please a president who 'loves to see big deals.'"

Robert Weissman, co-president of the consumer advocacy group Public Citizen, said in a statement Tuesday that "it would be easy to dismiss the prospect of such a merger passing antitrust scrutiny—except that the Trump Department of Justice seems content to bless dangerously high levels of corporate concentration, so long as administration cronies, allies, or flatterers are in charge of corporate goliath."

"That the United CEO raised the idea of a merger with American directly with Donald Trump," Weissman added, "suggests he thinks he might obtain direct approval from the president for a merger that would otherwise never be permitted.”

"When Democrats win back power we are going to break up these anti-democratic information conglomerates," said Sen. Chris Murphy. "All of them."

Concerns are mounting about the state of the US media landscape now that it looks increasingly likely that Paramount Skydance—a company controlled by the son of billionaire Larry Ellison, a donor to President Donald Trump—will succeed in its bid to acquire Warner Bros. Discovery.

One day after Netflix announced that it was dropping its previously accepted bid to buy Warner, many critics demanded that antitrust laws be invoked to block the Paramount-Warner merger from going through.

Alvaro Bedoya, former commissioner at the Federal Trade Commission, warned that the Ellison family could soon use their control over vast swaths of US media properties to engage in mass censorship, and he pointed to their decisions to cancel Stephen Colbert's program and to refuse to air an interview with Democratic US Senate candidate James Talarico.

"One family is about to control CBS, CNN, HBO, and TikTok," he wrote in a social media post. "They’ll buy [Warner Bros. Discovery] with $24 billion in money from the Saudis, Qatar, and Abu Dhabi. To win over Trump, they canceled Colbert... and blocked Talarico. Much more will follow. Block this rotten deal."

Craig Aaron, co-CEO of Free Press, said the proposed Paramount-Warner merger was "even worse" than the proposed Netflix-Warner merger.

"This deal endangers our democracy by giving a family of pliant billionaires even more control of vast swaths of our news coverage, TV stations, and movie studios," Aaron said. "Allowing more mergers in the already highly concentrated movie business will harm filmmakers and industry workers when Paramount delivers on its promise to make deep cuts to please its Wall Street backers."

Writing in the American Prospect, David Dayen described the Paramount-Warner merger as the "worst-case scenario" that has "echoes of media-political consolidation as we see in dictatorships the world over."

Dayen argued that state governments still had time to block the merger, but warned that they were in a race against time given that Paramount's consultants "are trying to speed run the deal in a matter of weeks."

"The states could challenge the merger even after the feds bless it," Dayen continued, "but by then, Paramount and Warner Bros. would have likely commingled their assets, engaged in layoffs, and made it very difficult to untangle the merger, particularly for judges who are inherently conservative on these matters."

Some Democratic lawmakers are warning that they aren't going to stop fighting the Paramount-Warner merger even if it goes through.

In an interview with Semafor, Sen. Ruben Gallego (R-Ariz.) predicted that the Ellisons would come to regret aggressively buying up US media properties.

"Once we take power, whoever the president is, we’re going to break up your companies," said Gallego. "So all the investment you did to create these mergers are going to be for naught. Your investors are going to be pissed at you, and you’re likely going to end up getting fired as the CEO because you wasted so much money and corrupted yourself in the process."

Sen. Chris Murphy (D-Conn.) echoed Gallego's argument in a social media post.

"Paramount should enjoy its growing news monopoly while they have it," he wrote, "because when Democrats win back power we are going to break up these anti-democratic information conglomerates. All of them."

"Trump’s new antitrust enforcers have demonstrated a willingness to facilitate dealmaking through an uptick in early terminations and settlements," said the American Economic Liberties Project.

Global corporate mergers surged to near-record highs in 2025, driven in part by US President Donald Trump's lax approach to antitrust enforcement.

The Financial Times reported on Friday that global dealmaking in 2025 topped $4 trillion, including 68 mergers worth $10 billion or more, highlighted by Netflix's $72 billion bid to buy Warner Bros. Discovery and a proposed $85 billion mega-merger between railway giants Union Pacific and Norfolk Southern.

The US alone accounted for $2.3 trillion worth of mergers and acquisitions, which the Financial Times said highlighted the Trump administration's role in green-lighting corporate consolidation.

"Top dealmakers said that the Trump administration’s push to loosen regulation had encouraged companies to explore tie-ups that they might otherwise have been hesitant to pursue," the Financial Times explained.

Andrew Nussbaum, co-chair of the executive committee at law firm Wachtell, Lipton, Rosen & Katz, told the Financial Times that corporate leaders "see a willingness of the regulators to engage in constructive dialogue" under the second Trump administration, which has given them "a willingness to take on regulatory risk for transactions that are strategic."

The American Economic Liberties Project has also taken note of the Trump administration's role in shepherding through big mergers, and created a Trump Merger Boom tracker earlier this year to document the massive wave of corporate consolidation.

In its analysis of the administration's lax approach to antitrust enforcement, the American Economic Liberties Project said that "Trump’s new antitrust enforcers have demonstrated a willingness to facilitate dealmaking through an uptick in early terminations and settlements."

"Despite pro-enforcement rhetoric early on from Trump’s heads of the FTC and DOJ Antitrust Division," the American Economic Liberties Project added, "it’s becoming increasingly clear that agency leadership is having trouble making their decisions in a vacuum—with a quiet tide of deals granted to companies that have been friendly to the White House."

"The threat of this merger in any form is an alarming escalation in a consolidation crisis that threatens the entire entertainment industry, the public it serves, and—potentially—the First Amendment itself," warned actress Jane Fonda.

Netflix announced a deal Friday to acquire Warner Bros. Discovery’s film studio and streaming business for $83 billion, a merger that—if approved by the Trump administration—would create a media behemoth that critics say threatens industry competition, higher costs for consumers, the rights of entertainment workers, and democracy.

Netflix, the largest streaming company in the world, and Warner Bros. Discovery (WBD), owner of the third-largest streaming platform HBO Max, unveiled the proposed agreement after a closely watched bidding war that included Paramount Skydance, the company that the Trump administration reportedly favored to acquire WBD. Paramount is owned by David Ellison, the son of billionaire Republican megadonor Larry Ellison—a close ally of President Donald Trump.

David Ellison reportedly met with Trump administration officials on Thursday to "press his case" against Netflix's pending acquisition of WBD. An unnamed senior official told CNBC on Friday that the Trump administration is treating the Netflix-WBD deal with "heavy skepticism."

While some expressed relief that Paramount appears—at least for now—to have lost the bid for Warner Bros., antitrust advocates argued such a view overlooks the much broader and more serious threat of corporate consolidation.

"Does anyone think Netflix won’t do what Trump wants to get their deal through?" asked Matt Stoller, director of research at the American Economic Liberties Project. "The threat to democracy isn’t the Ellisons, it’s media consolidation."

The American Prospect's David Dayen expressed a similar sentiment, writing on social media: "Keeping WBD out of Paramount's hands is good. Putting it in Netflix's is still unlawful consolidation though. This is the #1 streamer merging with #3. State enforcers should speak up."

"If we don’t speak now, we may have no industry—and no democracy—left to defend."

In a newsletter post following news of the merger agreement, Stoller argued the Netflix-WBD deal is plainly illegal under the Clayton Antitrust Act and "a recipe for monopolization."

"The ideal scenario now is a trial that puts the secrets of Hollywood executives and financiers on display, and crushes the financiers who think mergers are the only move in business," Stoller wrote. "Then Hollywood can get back to the business of making good TV shows and movies."

Sen. Elizabeth Warren (D-Mass.) said that "this deal looks like an anti-monopoly nightmare."

"A Netflix-Warner Bros. would create one massive media giant with control of close to half of the streaming market," said Warren. "It could force you into higher prices, fewer choices over what and how you watch, and may put American workers at risk."

"Under Donald Trump, the antitrust review process has also become a cesspool of political favoritism and corruption," the senator continued. "The Justice Department must enforce our nation’s anti-monopoly laws fairly and transparently—not use the Warner Bros. deal review to invite influence-peddling and bribery."

Ahead of the announcement, major figures in the entertainment industry sounded alarm over the possibility of a Netflix takeover of WBD. In a letter to members of Congress on Thursday, a group of film producers warned that Neflix would "effectively hold a noose around the theatrical marketplace" if it acquired WBD.

The Writers’ Guild of America, which represents film and TV writers, has said it would oppose WBD merging with any "major studio or streamer," warning it "would be a disaster for writers, for consumers, and for competition."

"Merger after merger in the media industry has harmed workers, diminished competition and free speech, and wasted hundreds of billions of dollars better invested in organic growth," the union said in a recent statement.

Jane Fonda, the renowned actress and activist, wrote Thursday that "the threat of this merger in any form is an alarming escalation in a consolidation crisis that threatens the entire entertainment industry, the public it serves, and—potentially—the First Amendment itself."

"Consolidation at this scale would be catastrophic for an industry built on free expression, for the creative workers who power it, and for consumers who depend on a free, independent media ecosystem to understand the world," Fonda wrote. "It will mean fewer jobs, fewer opportunities to sell work, fewer creative risks, fewer news sources, and far less diversity in the stories Americans get to hear."

"If we don’t speak now, we may have no industry—and no democracy—left to defend," she added.

Roger Alford, who was fired over his objections to a corrupt tech merger last month, said MAGA lobbyists and DOJ officials are "determined to exert and expand their influence and enrich themselves."

An antitrust lawyer fired from the US Department of Justice last month accused Attorney General Pam Bondi's underlings on Monday of giving MAGA-aligned corporate lobbyists the ability to "rule" over antitrust enforcement.

Roger Alford, formerly the deputy assistant attorney general in the DOJ's antitrust division, was ousted in July, reportedly for "insubordination" after he objected to the involvement of politically connected lobbyists in the $14 billion merger between Hewlett-Packard Enterprise (HPE) and Juniper Networks.

The DOJ had sued in January to block the merger, arguing that HPE's acquisition of Juniper would unlawfully stifle competition, raise prices for consumers, and harm innovation, since the two entities control over 70% of the wi-fi relied on by large companies, hospitals, universities, and other entities.

But that suit was resolved in June in what the Capitol Forum described as a "highly unusual settlement" in which Bondi's chief of staff, Chad Mizelle, overruled the DOJ's antitrust chief, Assistant Attorney General Gail Slater, to allow the deal to settle.

At the time, left-wing consumer advocates, like Nidhi Hegde, executive director of the American Economic Liberties Project, argued that the deal was "a corrupt and politically rigged merger settlement," which came after political operatives tied to Trump lobbied on behalf of the company.

Despite still describing himself as a staunch MAGA loyalist, Alford likewise feels that the settlement was a "scandal."

In a speech delivered Monday at the Technology Policy Institute in Aspen, Colorado, he said senior DOJ officials "perverted justice and acted inconsistently with the rule of law" by allowing "corrupt lobbyists" to hijack the process.

According to disclosures from HPE, it hired multiple top Trump allies as lobbyists to advocate for the merger. These included MAGA influencer Mike Davis—a right-wing critic of Big Tech and a notorious legal operative responsible for many of Trump's judicial nominations—and Arthur Schwartz, a close adviser and confidante to Donald Trump, Jr. and JD Vance.

According to reporting from the conservative writer Sohrab Ahmari in UnHerd last month, which cites one unnamed senior official, the DOJ's merger settlement was the product of "boozy backroom meetings between company lawyers and lobbyists, on one hand, and officials from elsewhere in the Department of Justice, on the other."

As Ahmari explained:

"Boozy backroom deal" here isn't a figure of speech, by the way. It captures what literally took place, according to the former official, who described a meeting between government officials and lobbyists that took place at one of Washington's "private city clubs" over cocktails.

In an essay for UnHerd adapted from his speech, Alford berated these "MAGA-in-name-only lobbyists and the DOJ officials enabling them," who he said are "determined to exert and expand their influence and enrich themselves as long as their friends are in power."

The current DOJ, Alford continued, has allowed for the "rule of lobbyists" to supplant the "rule of law." While he says this was not true of those idealists serving with him in the antitrust division—including his embattled former boss, Slater—he says that others in the DOJ showed "special solicitude" to lobbyists they perceived to be on the "same MAGA team."

"Too often in the current DOJ," he said, "meetings are accepted and decisions are made depending upon whether the request or information comes from a MAGA friend. Aware of this injustice, companies are hiring lawyers and influence-peddlers to bolster their MAGA credentials and pervert traditional law enforcement."

Alford makes a distinction between these corrupt officials and those he calls "genuine MAGA reformers" who "strive to remain true to President Trump's populist message that resonated with working-class Americans."

While he does not group Bondi in with the officials he deems corrupt, he does blame her for having "delegated authority to figures—such as her chief of staff, Chad Mizelle, and Associate Attorney General-Designee Stanley Woodward—who don't share her commitment to a single tier of justice for all."

"Some progressives may blanche at Alford's praise for [US President Donald] Trump's populist messaging, and insistence that it has been subverted by top DOJ officials selling out to lobbyists," writes David Dayen in the American Prospect.

But Dayen notes that Alford's audience is not progressives and that he is instead "attempting to reach the president and his inner circle by playing on Trump's demand for total loyalty."

The merger between HPE and Juniper can still be stopped under the Tunney Act, which requires it to be reviewed by a federal judge to determine whether settlements brought in federal "antitrust" cases are in the "public interest."

While the Capital Forum says this process is typically a "rubber stamp," they wrote that "given the settlement's atypical substance and process, plus third parties who may be motivated to intervene and a judge who may be inclined to approach the review skeptically, what's normally a quick judicial signoff could turn into a fraught process with wide-reaching implications."

"Indeed, the court should block the HPE-Juniper merger," Alford said. "If you knew what I know, you would hope so, too."

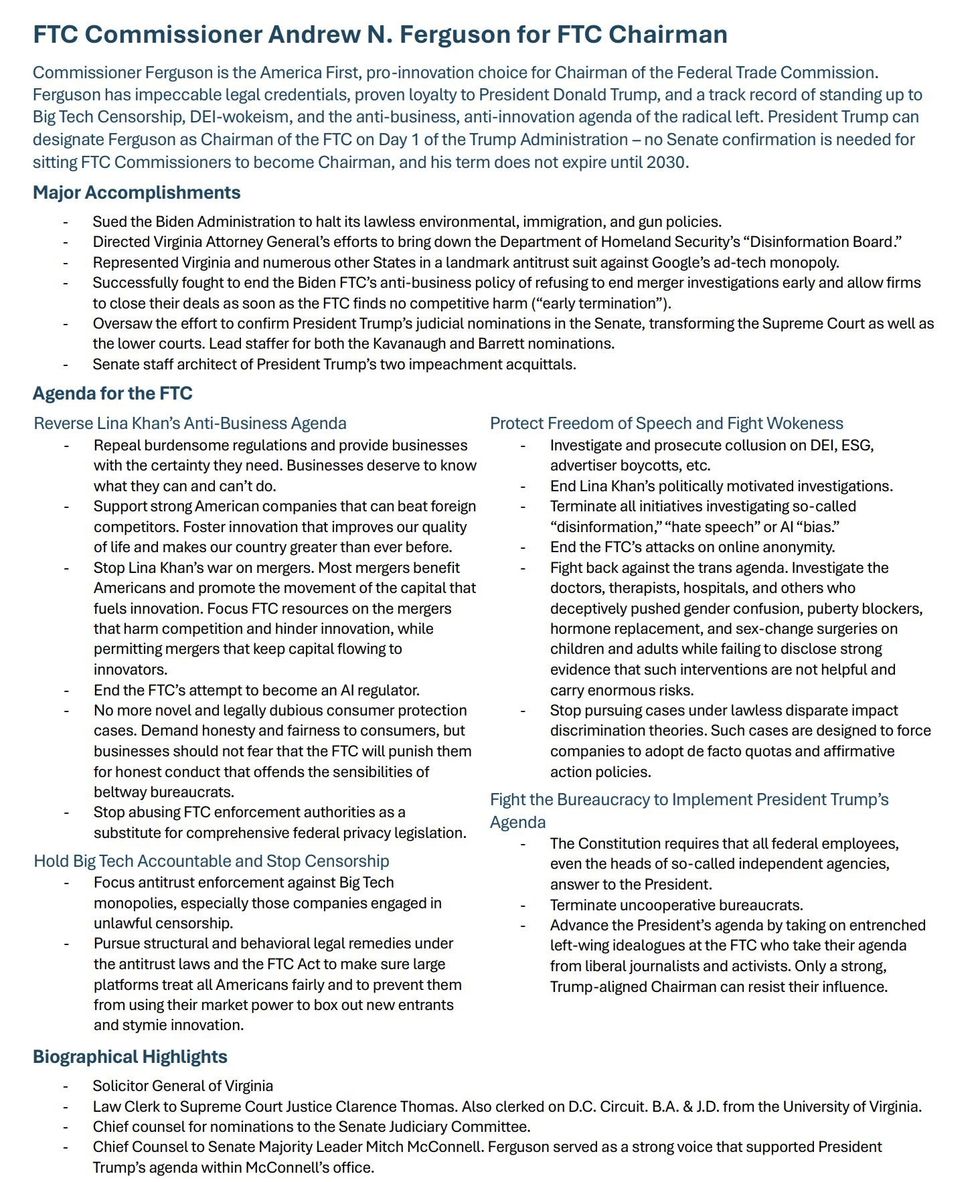

"Andrew Ferguson is a corporate shill who opposes banning noncompetes, opposes banning junk fees, and opposes enforcing the Anti-Merger Act," said one antitrust attorney.

President-elect Donald Trump's pick to lead the Federal Trade Commission vowed in his job pitch to end current chair Lina Khan's "war on mergers," a signal to an eager corporate America that the incoming administration intends to be far more lax on antitrust enforcement.

Andrew Ferguson was initially nominated by President Joe Biden to serve as a Republican commissioner on the bipartisan FTC, and his elevation to chair of the commission will not require Senate confirmation.

In a one-page document obtained by Punchbowl, Ferguson—who previously worked as chief counsel to Sen. Mitch McConnell (R-Ky.)—pitched himself to Trump's team as the "pro-innovation choice" with "impeccable legal credentials" and "proven loyalty" to the president-elect.

Ferguson's top agenda priority, according to the document, is to "reverse Lina Khan's anti-business agenda" by rolling back "burdensome regulations," stopping her "war on mergers," halting the agency's "attempt to become an AI regulator," and ditching "novel and legally dubious consumer protection cases."

Trump announced Ferguson as the incoming administration's FTC chair as judges in Oregon and Washington state

blocked the proposed merger of Kroger and Albertsons, decisions that one antitrust advocate called a "fantastic culmination of the FTC's work to protect consumers and workers."

According to a recent

report by the American Economic Liberties Project, the Biden administration "brought to trial four times as many billion-dollar merger challenges as Trump-Pence or Obama-Biden enforcers did," thanks to "strong leaders at the FTC" and the Justice Department's Antitrust Division.

In a letter to Ferguson following Trump's announcement on Tuesday, FTC Commissioners Alvaro Bedoya and Rebecca Kelly Slaughter wrote that the document obtained and published by Punchbowl "raises questions" about his priorities at the agency mainly "because of what is not in it."

"Americans pay more for healthcare than anyone else in the developed world, yet they die younger," they wrote. "Medical bills bankrupt people. In fact, this is the main reason Americans go bankrupt. But the document does not mention the cost of healthcare or prescription medicine."

"If there was one takeaway from the election, it was that groceries are too expensive. So is gas," the commissioners continued. "Yet the document does not mention groceries, gas, or the cost of living. While you have said we're entering the 'most pro-worker administration in history,' the document does not mention labor, either. Americans are losing billions of dollars to fraud. Fraudsters are so brazen that they impersonate sitting FTC commissioners to steal money from retirees. The word 'fraud' does not appear in the document."

"The document does propose allowing more mergers, firing civil servants, and fighting something called 'the trans agenda,'" they added. "Is all of that more important than the cost of healthcare and groceries and gasoline? Or fighting fraud?"

As an FTC commissioner, Ferguson voted against rules banning anti-worker noncompete agreements and making it easier for consumers to cancel subscriptions. Ferguson was also the only FTC member to oppose an expansion of a rule to protect consumers from tech support scams that disproportionately impact older Americans.

"Andrew Ferguson is a corporate shill who opposes banning noncompetes, opposes banning junk fees, and opposes enforcing the Anti-Merger Act," said Basel Musharbash, principal attorney at Antimonopoly Counsel. "Appointing him to chair the FTC is an affront to the antitrust laws and a gift to the oligarchs and monopolies bleeding this country dry."

One corporate CEO welcomed the Republican's victory as "an opportunity for consolidation."

Wall Street is "foaming at the mouth," as one leading business magazine put it, at the prospect of a corporate merger frenzy following Republican Donald Trump's victory in the 2024 presidential election—a win that's set to spell the end of antitrust champion Lina Khan's popular tenure at the helm of the Federal Trade Commission.

Trump's second administration, which is likely to be stacked with billionaires and corporate-friendly officials, is expected to take aim at merger and acquisition guidelines issued last year by Khan's FTC and the U.S. Department of Justice after decades of relentless corporate consolidation.

David Kostin, chief U.S. equity strategist at the Wall Street behemoth Goldman Sachs, predicted in a note published Wednesday that under Trump's incoming administration, "the regulatory posture of the Federal Trade Commission and the Department of Justice Antitrust Division that during the past four years challenged many proposed business combinations will likely be more relaxed."

That more relaxed posture, according to Kostin, could result in a 20% increase in merger activity in just the first year of Trump's second term.

Raul Gutierrez, the head of mergers and acquisitions at the investment banking firm Truist Securities, echoed Kostin's assessment, telling Bloomberg that "you should be able to see larger transactions move forward" under the incoming Trump administration.

"Some of these had been put on hold given the current antitrust stance," said Gutierrez, "and I think you'll see a greater willingness to test agencies out once the administration takes over."

Khan's term officially expired in late September, but she's expected to stay on at the FTC until Trump is inaugurated in January and chooses a replacement. While Vice President-elect JD Vance has praised Khan, "Trump and his allies are likely to get rid of anyone associated with the Biden administration's antitrust battles with the big Silicon Valley tech companies," The New York Times reported earlier this week.

Tesla CEO Elon Musk, who pumped upward of $118 million into Trump reelection efforts, wrote days before the November 5 election that Khan "will be fired soon."

According to the FTC's latest data, the Biden administration brought a record number of merger enforcement actions in fiscal year 2022. A recent analysis by the American Economic Liberties Project found that the Biden administration "brought to trial four times as many billion-dollar merger challenges as Trump-Pence or Obama-Biden enforcers did."

Under Khan's leadership, the FTC has taken legal action against some of the most powerful companies in the world, including Amazon and Microsoft.

But Trump's election victory has sparked hopes on Wall Street that aggressive merger enforcement could soon end.

"We think that under a Trump administration, deal approvals will speed up markedly and the process will be more clearly delineated," Mark Fitzgibbon, managing director of the banking company Piper Sandler, wrote in a research note.

David Zaslav, the CEO of Warner Bros. Discovery, hailed Trump's victory as "an opportunity for consolidation."

Kroger, a company that is currently locked in a legal battle with the Khan-led FTC over its attempt to acquire competitor Albertsons, saw its stock price jump in the wake of Trump's election victory, with investors anticipating "a more lax environment for corporate mergers" under the Republican, Barron's reported.

Axios reported Friday that "the $35 billion credit card merger of Capital One and Discover will be a bellwether for how Trump's antitrust crew views the M&A environment."

"Shares of each company rose 15% after his election," the outlet observed, adding that shares of the airline companies Frontier and Spirit also surged in a "sign their previous attempt at a merger could be revived."

"Americans are paying the price for Big Oil's greed and are still struggling to keep up with gas prices higher than pre-pandemic levels."

U.S. Congressman Ro Khanna and Senate Majority Leader Chuck Schumer on Wednesday led dozens of congressional colleagues in urging federal regulators to investigate the recent historic surge in oil and gas industry consolidation.

In a bicameral letter to Federal Trade Commission (FTC) Chair Lina Khan, the lawmakers took aim at what analysts say is the biggest-ever wave of Big Oil mergers and acquisitions (M&A), which totaled a staggering $190 billion last year, including $144 billion worth of industry consolidation in the fourth quarter alone.

"Contrary to disinformation spread by industry groups, these deals are not about efficiency, international competitiveness, or lowering costs; they are designed to pump more profits out of Americans' pockets—plain and simple," the letter led by Khanna (D-Calif.) and Schumer (D-N.Y.) states. "Fossil fuel companies have overwhelmingly identified investor pressure as the reason to keep prices high so they can continue to benefit from record profits. Americans are paying the price for Big Oil's greed and are still struggling to keep up with gas prices higher than pre-pandemic levels."

The lawmakers urged the FTC to "consider all harms that past and future mergers present to American consumers" and "oppose any acquisitions it determines to be in violation of antitrust law."

The FTC is currently investigating last year's megamergers involving Chevron and Hess, ExxonMobil and Pioneer, and Occidental Petroleum and CrownRock.

"Oil and gas is undergoing a historic consolidation wave comparable to what occurred in the late 1990s and early 2000s giving rise to the modern supermajors," Andrew Dittmar, a senior vice president at the analytics firm Enverus, said earlier this year. "After a decade of lowered investment in exploration and with the major U.S. shale plays largely defined, M&A has become the preferred tool to replace declining reserves and secure longevity in these companies' profitable upstream businesses."

The lawmakers' letter warns that "if a small group of dominant firms is allowed to control this industry, American consumers and industry competition will only suffer."

"Therefore, we urge the FTC to extend its current investigations, open inquiries into these new deals, and take all appropriate actions to protect competition in this industry," the letter adds. "Lax enforcement during the last generation, such as allowing Exxon and Mobil to merge, resulted in market manipulation, unstable supply, and price hikes for Americans. We must avoid similar mistakes going forward."

The letter is backed by advocacy groups including Food & Water Watch, Public Citizen, Friends of the Earth, Center for Biological Diversity, Indigenous Environmental Network, Greenpeace USA, Zero Hour, and Sierra Club.