SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"Nothing but the power of corporate leaders to rig rules in their favor can explain this double standard."

Millions of people in the United States have little to nothing in retirement savings, a consequence of low-wage jobs that give workers minimal room to stash money away.

Meanwhile, at the end of 2021, the nation's top CEOs held an estimated $9 billion in rapidly growing special retirement accounts that aren't available to their employees—a double standard established by the U.S. tax code.

That double standard is the subject of A Tale of Two Retirements, a new report published Thursday by the Institute for Policy Studies (IPS) and Jobs With Justice. The report says that while "ordinary employees with access to 401(k) plans face strict limits on the amounts they can set aside, tax-free, for their golden years," highly paid executives of major corporations "have unlimited tax-deferred compensation accounts" known as top hat plans.

"The sections of the U.S. tax code related to employer-provided, tax-deferred retirement accounts impose one set of strict rules on ordinary workers and another set of far more flexible rules for corporate top brass," the report notes. "Employees with 401(k) plans face hard caps on the amounts they can set aside in these accounts every year. By contrast, Section 409A of the tax code allows top corporate executives to place unlimited amounts in special 'non-qualified tax-deferred compensation' accounts."

The funds in such plans are only taxed when they are withdrawn, allowing executives to reap the benefits of years of investment returns tax-free.

The new analysis shows that "at more than 20 low-wage employers, executives have sufficient deferred compensation funds to generate monthly retirement checks larger than their workers' median annual pay," pointing specifically to Walmart CEO Doug McMillon (who held over $169 million in his deferred compensation account at the end of last year) and former Home Depot CEO and current board chair Craig Menear (who has nearly $15 million in a deferred compensation account).

Home Depot employees aren't nearly as well-positioned for retirement. According to the researchers behind the new report, 53% of those eligible to participate in Home Depot's 401(k) plan have zero balances. Menear's top hat account balance is "enough to generate a monthly retirement check three times larger than the company’s median worker pay of just $30,100," the report notes.

The executive with the largest top hat account among S&P 500 company heads is Paul Saville, CEO of the homebuilding giant NVR, Inc. At the end of 2022, Saville held $488 million in his deferred compensation account—which could yield $3 million a month in retirement checks for the rest of his life.

"That's 1,513 times as much as a typical American retiree could expect to receive in monthly Social Security and 401(k) benefits," IPS and Jobs With Justice note.

Sarah Anderson, global economy director at IPS and a co-author of the new report, said that "there's no rational argument for allowing wealthy executives to shelter unlimited amounts of compensation from taxes while ordinary workers have strict limits on their annual 401(k) contributions."

"Nothing but the power of corporate leaders to rig rules in their favor can explain this double standard," Anderson argued.

"Perhaps most importantly, we need to expand Social Security, the key pillar for retirement security for most Americans, particularly low- and moderate-income families who receive little to no tax benefits."

For workers under the age of 50, the annual 401(k) contribution limit is $22,500 in 2023—a ceiling that the overwhelming majority of workers with access to a 401(k) won't hit.

"Nationwide, just 35% of working-age adults have tax-deferred 401(k)-type defined contribution plans through their employer and another 13% have defined benefit or cash balance plans. Some 42% of Americans age 56-64 have zero retirement account savings, according to the U.S. Census Bureau," the new report observes. "Americans who are unable to save for retirement need to rely on Social Security, which pays an average monthly benefit of $1,784, as of March 2023."

The report adds that while companies "often match a portion of employee 401(k) contributions," that benefit is "meaningless for the many low-wage workers who cannot afford to set aside any of their wages."

Furthermore, roughly half of U.S. workers in the private sector have no access to an employer-provided retirement plan.

"For decades now, large U.S. corporations have been making workers' retirement futures less secure by abandoning traditional pensions in favor of 401(k) plans," the report points out. "In 1984, more than 30 million Americans had defined benefit pensions through which employers bore the financial risks for their workers' retirement security. By 2020, that number had declined to just 12 million, and private sector workers were approximately 3.5 times as likely to have a defined contribution plan as a traditional pension."

IPS and Jobs With Justice highlight a number of potential policy changes that could help combat the stark and worsening retirement divide between ordinary workers—who are facing a full-fledged retirement income crisis—and executives, including changes to the tax provisions that let rich executives shelter their compensation.

"Perhaps most importantly, we need to expand Social Security, the key pillar for retirement security for most Americans, particularly low- and moderate-income families who receive little to no tax benefits," the report states. "Funding for expansion could come from lifting the wage cap on payroll taxes so that CEOs and other high earners pay roughly the same share of their total income into the Social Security fund as ordinary workers."

Scott Klinger, report co-author and senior equitable development specialist at Jobs With Justice, said that "rather than giving corporate CEOs unfair special retirement tax benefits not available to those they employ, Congress should eliminate the cap on payroll taxes paid by corporate executives so that Social Security benefits can be strengthened, especially for the 40% of American workers for whom Social Security is their sole retirement income."

After Recode on Friday revealed an internal document from last year warns that "if we continue business as usual, Amazon will deplete the available labor supply in the U.S. network by 2024," critics of the online retail giant's labor practices renewed calls for improvement.

"I guess treating people like they're expendable has consequences, who knew?"

Journalist Jason Del Rey's reporting on the "looming labor crisis" comes as the company is under fire for battling its workers' organizing efforts, including the historic victory of the Amazon Labor Union at a Staten Island facility earlier this year.

"This is crazy. Amazon burns through workers so fast there might be none left soon," tweeted New York City organizer and writer Joshua Potash, adding that he "can't imagine how anyone defends a system that treats people like expendable parts like this."

Retired journalist Laura Keeney said that "if you need to better understand how Amazon burns through workers, here you go. I guess treating people like they're expendable has consequences, who knew?"

California Labor Federation's Lorena Gonzalez Fletcher told Amazon that "maybe it's time to improve working conditions and allow your workers to unionize."

"It turns out that low wages and unsafe working conditions are [Amazon's] biggest labor problem, not unions," declared Doug Bloch, political director for Teamsters Joint Council 7. "Gee, aren't those the problems that workers join together in unions to fix?"

Longtime labor reporter Steven Greenhouse similarly suggested that "IF AMAZON LETS ITS WAREHOUSES UNIONIZE, they could become far less grueling places to work and worker turnover could decline greatly."

Pointing out that "workers have long warned Amazon that its 'churn and burn' would cause the company to 'run out of workers,'" Jobs with Justice also said that "maybe if Amazon stopped fighting workers organizing unions, they could build a safer, healthier workplace and this would be less of a problem."

According to Del Rey--who noted that an Amazon spokesperson didn't deny the report's findings but declined to comment--the company "was expected to exhaust its entire available labor pool in the Phoenix, Arizona, metro area by the end of 2021, and in the Inland Empire region of California, roughly 60 miles east of Los Angeles, by the end of 2022."

"The internal research also identified the regions surrounding Memphis, Tennessee, and Wilmington, Delaware, as areas where Amazon was on the cusp of exhausting local warehouse labor availability," he continued, highlighting the accuracy of the company's models for staffing shortages ahead of Amazon Prime Day shopping event in June 2021.

Amazon's own data shows that its attrition rate was 123% in 2019 and 159% in 2020, which are high figures compared with the federal government's estimates for those two years in the U.S. transportation and warehouse sectors (46% and 59%) and retail (58% and 70%).

The document "provides a rare glimpse into the staffing challenges" faced by a company whose employees "have long complained of stresses unique to Amazon's workplace, from the pace and repetition of the labor to the unrelenting computerized surveillance of workers' every move to comparatively high injury rates," Del Rey wrote. "The leaked internal findings also serve as a cautionary tale for other employers who seek to emulate the Amazon Way of management."

The journalist asserted that the report "reads like an attempted wake-up call" and outlined the projected impacts of some solutions it offers, including raising wages, changing termination or retention policies, improving the hiring process, choosing new warehouse locations in areas with significant labor pools, and increasing automation.

Noting that Amazon's new CEO, Andy Jassy, has claimed the company is "not close to being done in how we improve the lives of our employees," Del Rey concluded that "as the internal report shows, doing so should no longer be optional for Amazon; it's an imperative."

Progressives hailed Friday's unionization vote by employees at an Amazon warehouse in New York City as a historic victory for workers across the United States and an inspiring call to action for others seeking to organize.

"This is the catalyst for the revolution."

In what's being described as a "tremendous upset" of "David versus Goliath" proportions, employees at Amazon's JFK8 warehouse in Staten Island--led by fired worker Chris Smalls--defeated a multimillion-dollar union-busting effort by one of the world's largest and most powerful corporations and voted to form the Amazon Labor Union (ALU).

"It's official," ALU tweeted after the vote. "Amazon Labor Union is the first Amazon union in U.S. history. Power to the people!"

"This is the catalyst for the revolution," Smalls, the ALU organizer and president, said while celebrating the vote.

Erica Smiley, executive director of the labor advocacy group Jobs With Justice, said in a statement that "this triumphant union victory over Amazon represents a watershed moment in the labor movement."

"Amazon finally got what it deserved today after the trillion-dollar company ignored the demands for safer working conditions in 2020 from its workers exposed to Covid and retaliated against Christian Smalls and others who led a walkout," she said.

Smiley added that "the closeness of the election in Bessemer, Alabama"--where Amazon employees are also fighting to form a union--"is a further indication of the genuine sea-change for all Amazon workers and workers everywhere."

Varshini Prakash, executive director of the youth-led climate group Sunrise Movement, cheered Friday's "win for workers across America," while hailing "worker victories at giant corporations like Amazon and Starbucks" as "part of a growing wave of activism that is paving the way for a more just economy."

Our Revolution, the progressive political action group spun out of Sen. Bernie Sanders' (I-Vt.) 2016 presidential campaign, called the results of the vote "a massive victory" and "an inspiration for working-class people across the U.S."

Dennis Hogan, who rose to prominence organizing a graduate students' union at Brown University, tweeted: "Doubtless there will be many takes on the Amazon Labor Union's historic and little-anticipated victory in the election today. But I think a lot of it boils down to this: for everyone in the labor movement, it's time to dramatically rethink what we imagine is possible."

"There's probably never been a better time to take big risks and win," he added. "Who knows how long this window of militancy and possibility will last. Months? Years? Impossible to say. But if you're not making big moves now you risk missing it."

Eric Blanc, an assistant professor of labor studies at Rutgers University and author of Red State Revolt: The Teachers' Strike Wave and Working-Class Politics, tweeted that "the iron is hot--unions urgently need to seize the moment for new organizing."

Some labor advocates reported increased interest from workers seeing to form their own unions.

Others, including numerous Democratic U.S. lawmakers, called on Congress to pass the Protect the Right to Organize (PRO) Act, legislation whose provisions include penalties for employers who engage in union-busting activity.

"Fantastic news," Rep. Ro Khanna (D-Calif.) tweeted about the ALU vote. "Now let's get the PRO Act to [President Joe Biden's] desk to protect the right of all workers to organize."

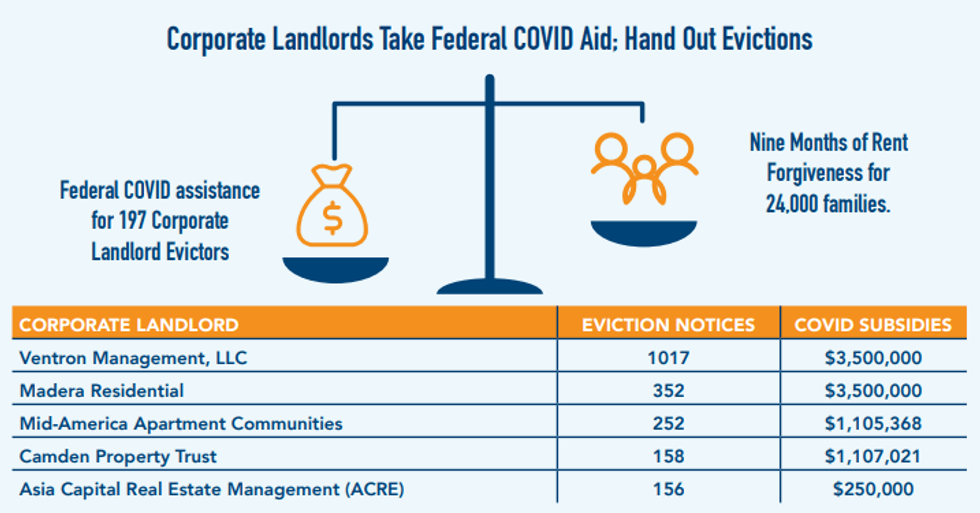

Nearly 200 corporate landlords received $320 million in federal pandemic-related assistance only to turn around and file more than 5,380 evictions between mid-March and mid-October of last year, recklessly displacing thousands of impoverished Americans in the midst of a public health and economic emergency.

"By subsidizing corporate landlords through PPP loans, tax breaks, and sweetheart deals, Congress was subsidizing the spread of Covid."

--Job With Justice

That's according to Taxpayer Subsidized Evictions: Corporate Landlords Pocket Federal Sweetheart Deals, Subsidies, and Tax Breaks While Evicting Struggling Families, a new report (pdf) published Tuesday by the Jobs With Justice Education Fund and the Private Equity Stakeholder Project.

Although corporate landlords have benefited from public subsidies and favorable tax laws for years, the report details how these actors--under crisis conditions--were able to capitalize on a novel form of financial aid, specifically loans from the Paycheck Protection Program (PPP), part of the $2 trillion CARES Act passed by Congress in late March 2020.

Even as they received millions of dollars in taxpayer-funded support, corporate landlords continued to kick thousands of tenants to the curb despite the recommendations of public health officials who urged people to shelter-in-place to slow the spread of the virus.

The report's data were drawn from public records in 25 counties across Arizona, Florida, Georgia, Tennessee, and Texas, meaning that the number of renters evicted by corporate landlords throughout the U.S. is almost certainly higher. Some of the top offenders are depicted in the table below:

Previous studies have shown that corporate landlords are more likely than "mom-n-pop" landlords to evict tenants, and yet that did not prompt legislators to make allocation of public aid dependent on commitments to halt displacement.

While corporate landlords took advantage of no-strings-attached coronavirus relief that did not mandate a corresponding pause in eviction filings, the report notes how much more effectively housing security, and thus public health, could have been improved had the government provided rental assistance directly to tenants instead of routing the subsidies through private, profit-maximizing housing entities.

According to the report:

The $320 million of Covid subsidies handed out to corporate landlords would have been enough to cover 219,550 months of rent at the nation's median rent ($1,463). The corporate landlord Covid stimulus subsidies would have been enough to pay the nine months of rent (since the pandemic started) for 24,394 families.

Jobs With Justice compared the taxpayer-funded support of eviction-prone landlords to the public bailouts of climate-destroying fossil fuel corporations--something the Trump administration also implemented in its pandemic response--both of which have deadly consequences.

Recent studies have confirmed that evictions are a matter of life-and-death. As Common Dreams reported last November, researchers found that between the onset of the pandemic in mid-March and the implementation of a national eviction moratorium in early September, the premature lifting of statewide protections in the spring and summer caused more than 433,000 excess Covid-19 infections and 10,700 excess deaths.

"Giving 'Covid relief' to those most likely to evict is like giving money to stop climate change to oil barons--it makes the problem worse," the group tweeted. "By subsidizing corporate landlords through PPP loans, tax breaks, and sweetheart deals, Congress was subsidizing the spread of Covid."

President-elect Joe Biden and Congress, soon controlled by Democrats, "must immediately end the policy of handing out public 'Covid relief' to the corporate landlords who are making Covid worse," said Jobs With Justice.

"They must stop funding these evictors," the group added, "and start getting relief to tenants."

The coronavirus relief package passed by Congress in December extended the CDC's nationwide eviction moratorium through the end of January 2021, temporarily boosted unemployment insurance benefits, and distributed $25 billion in emergency rental assistance. While they called this legislation helpful, the report authors noted that these measures are insufficient considering the scale of the problem and "merely push a mounting crisis down the road."

"To prevent this housing catastrophe," the authors continued, lawmakers should further extend eviction and foreclosure moratoriums and cancel rents that have accumulated as a result of the coronavirus crisis, with landlord compensation coming from the federal government.

"In addition to Congress and the White House establishing new relief and protection programs to keep families in their homes as the pandemic deepens this winter and into the spring, corporate landlords also have an important role to play," the authors noted.

Corporate landlords--already having benefited from public support--can chip in by "forgiving accrued rents for Covid affected families, and immediately suspending eviction filings," the report stated.

Toiling amid a pandemic and a callous response from corporate America and the federal government that is exposing millions to deadly hazards and deepening poverty, workers across the country are rising up, planning hundreds of strikes and sickouts for International Workers' Day on May 1.

May Day actions throughout the United States will include worker strikes, car caravan protests, rent strikes, and a host of social media onslaughts urging work stoppages, and boycotts of major corporations that are failing to fairly pay and protect their workers amid the pandemic.

At a time when worker organizing could be stifled by physical distancing rules and the Trump administration's disabling of the National Labor Relations Board, workers are walking off the job in massive coordinated walk-outs and sick-outs targeting major employers such as Amazon, Whole Foods, Target, Walmart, FedEx, and Instacart, demanding hazard pay, personal protective equipment and other basic protections.

May Day actions throughout the United States will include worker strikes, car caravan protests, rent strikes, and a host of social media onslaughts urging work stoppages, and boycotts of major corporations that are failing to fairly pay and protect their workers amid the pandemic, activists say. Activists are also pressuring for rent and debt relief, and a "People's Bailout" demanding a more equitable stimulus and economic recovery plan that prioritizes workers.

Long overworked and underpaid, warehouse and food industry workers (including grocery clerks, meatpackers, and farmworkers) are now deemed "essential"--responsible for hazardous jobs at the epicenter of the Covid-19 storm. Yet while some unionized workers have secured hazard pay and protective gear, millions of these workers on the pandemic's front lines remain in or near poverty and without adequate healthcare or safety protections. Now they're striking back, shining a spotlight on the struggles of low-wage workers laboring amid viral hazards while corporations like Amazon and Instacart report booming business and profits.

Even as unemployment skyrockets above 20% (with an astounding 30 million new claims since the beginning of March), Amazon alone is raking in $11,000 per second and its shares are rising, the Guardian reports. The company's CEO Jeff Bezos, meanwhile, has seen his personal fortune bloat to $138 billion amid the pandemic.

Protesting unsafe conditions and lack of hazard pay for many employees, Target Workers Unite is waging a mass sickout of the retail chain's workers, stating, "We want to shut down industry across the board and pushback with large numbers against the right-wing groups that want to risk our lives by reopening the economy."

On its website, the group describes "atrocious" foot traffic in stores, "putting us at needless risk when greater safety measures are required to ensure social distancing. Workers nor guests have been required to wear masks...Our maximum capacity of guests have been set too high."

Whole Worker, a movement of Whole Foods workers pushing for unionization, plans a mass "sickout" for what is also being called #EssentialWorkersDay. Workers at the non-union corporate chain, which is owned by billionaire Bezos, are demanding guaranteed paid leave for employees who self-quarantine, reinstating healthcare coverage for part-time and seasonal workers, and the immediate shutdown of any store where a worker tests positive for Covid-19. According to organizers, 254 Whole Foods workers have tested positive for the virus nationwide, and two have died.

Gig economy workers for Instacart, the app-propelled tech corporation that dispatches "shoppers" for customers, will wage their second work stoppage in a month, after a March 30 strike demanding hazard pay, paid sick leave and safety protections. Despite Instacart's booming business amid the Covid-19 pandemic, "Most workers STILL haven't been able to order, let alone receive, proper PPE," according to the Gig Workers Collective.

This week, dozens of workers at an Amazon fulfillment center warehouse in Tracy, CA walked off the job after learning that a co-worker who had tested positive for Covid-19 had died. One employee told a local television station, "We are short handed now working extra hard, and I'm questioning what I'm still doing here honestly...I'm actually nervous now and wondering if it's even worth coming."

Citing a "lack of response from this government in terms of PPE and mandatory [safety] standards," the AFL-CIO will be supporting and "uplifting" striking workers at Amazon, Target, Instacart and elsewhere who are "risking their lives every day on the job," said spokesperson Kalina Newman. "While our affiliates who work with retail workers, UFCW and RWDSU, aren't helping organize the May Day strikes, they may uplift them. At the end of the day, we support workers who are standing up for their rights."

In an email, Newman elaborated that the AFL-CIO is encouraging union members "to contact their congressperson stressing that the coronavirus relief packages approved so far leave many working families behind, including hardworking immigrants who provide essential services."

Since the pandemic began, union workers at Safeway, Stop & Shop and Kroger's have won hazard pay and protective equipment guarantees, Newman added, following pressure from the United Food and Commercial Workers.

Other prominent labor groups are backing the May Day strike actions. Jobs With Justice "is supporting worker walkouts across the country, from Amazon workers to Instacart drivers," and will be "standing in solidarity with workers who are walking off the job and demanding safer working conditions," organizing director Nafisah Ula said in an email.

A range of other groups, including the Democratic Socialists of America and new grassroots initiatives like Coronastrike will also be backing up the workers on May Day. Launched by Occupy Wall Street alumni, Coronastrike aims to "amplify the efforts and voices of those striking," says organizer Yolian Ogbu, a 20-year-old climate justice activist.

"We're frustrated by the inaction by these corporations," Ogbu adds. "There is all this pent-up energy, and we're asking people to put it somewhere. People are desperate."

According to Fight for 15, the nationwide coalition for a $15 federal minimum wage, fast food workers have already been striking for fair wages and safety protections as they attempt to survive low-wage work and exposure to Covid-19. Since the pandemic began, fast food workers have walked off the job in Los Angeles, Oakland, Chicago, Memphis, Miami, St. Louis and other major cities, demanding personal protective equipment, hazard pay and paid sick leave.

In early April, hundreds of workers from more than 50 fast-food restaurants across California--including McDonald's, Taco Bell, Burger King and Domino's--walked out of work to demand better pay and safety protections, Vice reported. This week, Arby's workers in Morris, Illinois, walked out in the middle of their shift to protest conditions and climbed into their with windows festooned with big posters stating, "We don't want to die for fries," and "Hazard pay and PPE now!" They are demanding $3 per hour in added hazard pay and say the corporation has not provided masks or any other protective gear.

Since March, there have already reportedly been at least 140 documented wildcat strikes across the country.

As the Covid-19 pandemic intensifies and exposes America's inequalities, workers, so long stifled and embattled, are showing renewed force.

The U.S. Supreme Court will hear the opening arguments on Monday in a case that workers and labor leaders fear could deliver a serious blow to public sector unions.

In Janus vs. AFSCME, the court will reconsider its 1977 decision stating that public employees who choose not to join unions can still be required to pay partial union dues, to help fund unions' collective bargaining negotiations, which hold benefits for all workers.

While AFSCME is the union that represents state and municipal workers, supporters fear that a decision in favor of Mark Janus--the individual plaintiff backed by a network of billionaires, corporate interests and right-wing ideologues determined to undermine organized workers--would threaten labor in all sectors across the country. As Andrew Hanna and Caitlin Emma wrote at Politico on Sunday:

The financial blow dealt by a Janus victory would far exceed the loss of nonmember fees, thanks to what economists call a "free rider" problem. Unions are compelled by law to represent all workers within a collective-bargaining unit--not just dues-paying union members. If workers are permitted to quit the union and still benefit from collective bargaining agreements without paying non-member fees, union non-membership will become much more attractive.

Wealthy conservative donors including the Bradley Foundation and the Koch brothers have contributed to the "right to work" cause represented by Janus for decades. The National Right to Work Foundation and the Illinois Policy Institute, which represent the plaintiff, have received hundreds of thousands of dollars in donations from the groups.

Public sector unions and labor advocates including the National Education Association (NEA), Jobs with Justice, and AFSCME rallied in front of the Supreme Court on Monday, keeping up the momentum started by protests in cities across the country on Saturday's Working People's Day of Action.

Using the rallying call, "Unrig the system," leaders including Sarita Gupta of Jobs with Justice spoke out at the Supreme Court against the corporate power behind efforts to weaken unions.

"This case is a culmination of years of attacks on working people," Gupta told the crowd. "It's an assault by wealthy elites on our freedom to create better lives and sustainable futures for our families. Greedy billionaires, divisive extremists, and the corrupt politicians who do their bidding are rigging the rules in their favor in an attempt to gain more power. And we're not going to let that happen."

A ruling in the Janus case is expected by June.

Hundreds of thousands of immigrants and allies are expected to strike and protest on Monday, taking part in what organizers are hoping will be the largest national strike since the May Day demonstrations of 2006.

"I definitely think this is going to be one of the biggest May Day marches," Kent Wong, executive director of the UCLA Labor Center, told The Nation, which noted that "[t]he turbulent Trump era and draconian attacks on immigrant communities all but guarantee a bigger and more passionate turnout than usual this year."

"This Day Without Immigrants is the first step in a series of strikes and boycotts that will change the conversation on immigration in the United States," said Maria Fernanda Cabello, the May 1st campaign coordinator with Movimiento Cosecha.

"We believe that when the country recognizes it depends on immigrant labor to function, we will win permanent protection from deportation for the 11 million undocumented immigrants; the right to travel freely to visit our loved ones abroad; and the right to be treated with dignity and respect," she said. "After years of broken promises, raids, driving in fear of being pulled over, not being able to bury our loved ones, Trump is just the final straw."

Still, while the nationwide campaign is focused on immigrant rights, workers everywhere are being urged to participate given the Trump administration's blatant disdain for labor protections and ordinary Americans.

"We are sick and tired of a political and economic system that prioritizes corporate profits over the basic needs of our communities," Jobs With Justice says in its call-to-action. "We know that the change we need won't come from President [Donald] Trump, his corporate cabinet, or billionaire-backed politicians in Congress."

"The only way to take action against our rigged economy is by coming together and working to raise wages and working standards for all of us," the labor advocacy group continued. "While some of us were born here and others came here to escape hardships and build a new life, we share many of the same struggles. We've seen corporations attack our rights to join together and negotiate for a fair return on our work, and right-wing threats against us and our families regularly used to force us to remain silent. But we will remain quiet no more."

Furthermore, progressive advocacy groups are framing May Day as a chance to highlight the intersectional nature of key movements, including those pursuing labor rights, climate action, and racial justice. Already, dozens of climate groups have pledged their support for striking workers.

And Mother Jones reports that on Monday, "a coalition of nearly 40 advocacy groups, is holding actions across the nation related to workers' rights, police brutality and incarceration, immigrants' rights, environmental justice, indigenous sovereignty, and LGBT issues--and more broadly railing against a Trump agenda organizers say puts them all at risk."

The effort, organized under the banner "Beyond the Moment," recognizes that "it's going to take all of our movements in order to fight and win right now," Patrisse Cullors, a co-founder of one of the Black Lives Matter groups involved, told Mother Jones.

Fight for $15 has a "How to Strike" guide and The Nation has a run-down of some of the bigger rallies and actions slated for Monday.

Find a full list of events here, and follow online under the hashtags #MayDay; #undiasininmigrantes; or #beyondthemoment:

Labor unions and workers' rights advocates are pressuring President Donald Trump to drop his nominee for Labor Secretary, Andy Puzder, over the fast-food CEO's recent admission that he had hired an undocumented immigrant as a housekeeper.

The AFL-CIO, the nation's largest labor union, penned a letter (pdf) to Trump--signed by 128 progressive organizations, including the Service Employees International Union (SEIU), Jobs With Justice, and the NAACP--calling on him to ditch Puzder and pick "a suitable nominee who shows proper respect for working people and our nation's employment laws."

Puzder on Monday admitted that he had also failed to pay taxes on his housekeeper while she was in his employ, although he claimed he did not know of her immigration status at the time. He said he later fired her and has since paid back what he owed--but opponents say that's reason enough to drop him.

Indeed, they say, Puzder only repaid his taxes when his nomination was imminent.

"Mr. Puzder is an experienced attorney and a CEO of a major fast-food chain, so he cannot plausibly claim ignorance of his legal obligations as an employer," the letter reads. "We already have ample cause to doubt Mr. Puzder's fitness for the job as Secretary of Labor, and this latest news confirms our view that he should not be confirmed."

"If he cannot be trusted to follow even one of the most basic laws of employment in his own home, there is no way we can expect him to enforce the crucial laws the Department of Labor oversees on behalf of working people," it states.

Senate Minority Leader Chuck Schumer (D-N.Y.) likewise called for Trump to withdraw Puzder's nomination, calling him "one of the most anti-worker nominees to any cabinet position, and probably the most anti-worker to the Department of Labor ever."

Watch below:

The letter comes just before large-scale protests against Puzder's nomination are scheduled to launch nationwide. The actions, organized by the workers' rights collective Fight for $15, will take place Monday, days before his confirmation hearing, which was rescheduled for the fifth time this week and is now set to take place February 16.

Puzder is the CEO of CKE Restaurants, which operates Hardee's and Carl's Jr., among other chains. Workers from several of Puzder's restaurants in January filed 33 complaints with state and federal agencies alleging wage theft, sexual harassment, and retaliation against organizing. His record continues to be a major rallying point for opponents.

"Andy Puzder is unfit to be Labor Secretary--period," said Angel Gallegos, a Carl's Jr. cashier from Los Angeles, California. "We're stepping up our fight to demand that Puzder withdraw his nomination, and if he won't, then the U.S. Senate should reject him. Working families need a real Labor Secretary who will fight for ordinary people, not powerful corporations."

Doreatha Hines, a Hardee's cashier from Orlando, Florida, said, "By picking Puzder, Donald Trump has shown that instead of taking on the rigged economy, he wants to rig it up even more."

"If Trump is going to be a president for the fast-food corporations instead of for the fast-food workers he is going to be on the wrong side of history," Hines said. "And one thing is for sure, whether Puzder's nomination is confirmed, denied or withdrawn: we won't back down for one minute in our demands for $15 an hour and union rights for all working Americans."

In February, 15 students who had attended Corinthian Colleges Inc. launched the nation's first student debt strike. The students declared that they would no longer repay their loans on the grounds that Corinthian -- a network of for-profit schools including Everest, Heald and WyoTech -- had used fraudulent marketing and recruitment practices and that the credits and degrees they earned were worthless. Soon the Corinthian 15 became the Corinthian 100, and the 200. Groups such as the American Federation of Teachers and Jobs With Justice endorsed their cause.

In February, 15 students who had attended Corinthian Colleges Inc. launched the nation's first student debt strike. The students declared that they would no longer repay their loans on the grounds that Corinthian -- a network of for-profit schools including Everest, Heald and WyoTech -- had used fraudulent marketing and recruitment practices and that the credits and degrees they earned were worthless. Soon the Corinthian 15 became the Corinthian 100, and the 200. Groups such as the American Federation of Teachers and Jobs With Justice endorsed their cause.

Corinthian filed for bankruptcy in May, and the Department of Education has now announced a plan to cancel the debt of some former Corinthian students.

This is a significant victory for the strikers. It shows that the tactic of debt refusal, when strategically deployed, can get results. But the department hasn't done nearly as much as it could, or should, to set things right.

When Education Secretary Arne Duncan revealed the debt relief plan, he blasted schools such as Corinthian for bringing "the ethics of payday lending into higher education." These schools, Duncan said, "prey on the most vulnerable students and leave them with debt that they too often can't repay." Indeed, a third of Corinthian students came from families that earned less than $10,000 per year.

A close look at the fine print, however, reveals that Duncan and his staff are presenting a stopgap measure as a meaningful solution. Instead of issuing a blanket discharge to all former Corinthian students, the department offers a byzantine process that will likely leave out many students.

Most students will have to apply individually, and be required to submit transcripts and other documents that may be hard to come by because their campuses have shut down or been sold. They must also spell out what parts of a state law Corinthian violated in their particular case. These students are not lawyers, and they should not be required to do the job of a federal agency with a fleet of attorneys on staff.

The government makes an obscene profit from the student loan program -- an estimated $110 billion over the next decade... Why not divert some ... to make scammed students whole?Students, already drowning in debt, will soon find themselves tied up in red tape, and that's only if they know the relief program exists in the first place. The Education Department has announced no plans to alert students about their options, even though it acknowledged to the New York Times that in past cases of college closures, only 6% of students have typically asked for debt cancellation.

It's clear from the long trail of allegations against Corinthian that it was a "bad actor," a term federal officials used in a meeting with strikers and organizers. The state of California has been investigating the company since at least 2007, when a last-minute settlement stopped an impending lawsuit. Since then, dozens of state and federal authorities have investigated Corinthian. The federal Consumer Financial Protection Bureau sued the company in 2014, accusing it of operating a predatory lending scheme.

But the Education Department is largely to blame for the problem of unscrupulous, for-profit schools. For decades, the government has funded billions of dollars in grants, loans and GI Bill benefits to students at these institutions. A 2012 Senate Committee found that 86% of the revenue at 15 of these publicly traded schools came from taxpayers. Corinthian alone got $1.4 billion a year -- much of which flowed to conservative think tanks and public relations firms, according to investigative reporter Lee Fang.

In 2014, the Education Department accused Everest College of lying to students about job placement rates and briefly cut off federal funding to Corinthian. After the company said it could not survive even a few weeks without the public money, the Education Department continued funding Corinthian while the network sought a buyer.

The Education Department is aware that its actions in this case will set a precedent. There are other for-profit colleges that are teetering on the brink of collapse. The Securities and Exchange Commission, for instance, recently announced it was investigating ITT Tech for fraud. And in May, the Art Institutes announced it would shut down more than a dozen campuses.

It's clear that the Department of Education does not want to be in the position of having to cancel potentially millions of student loans. But anything less would be morally unacceptable. The government makes an obscene profit from the student loan program -- an estimated $110 billion over the next decade. That may be justifiable when students actually receive an education, but not when they're defrauded. Why not divert some of the $110 billion to make scammed students whole?

According to attorneys at the National Consumer Law Center, the Education Department has the legal power to issue a broad cancellation of Corinthian loans. Reaching into its own coffers to erase the debts of the hundreds of thousands of former Corinthian students is both lawful and the right thing to do.

A few weeks ago, people working at McDonald's filed several complaints that detailed the dangerous accidents and severe burns they've suffered while on the job, citing company management's policies to work quickly without protective gear or training. Of course, the injuries that the complainants describe were preventable, but it would require McDonald's and its franchisees to treat employees as human beings worth protecting.

A few weeks ago, people working at McDonald's filed several complaints that detailed the dangerous accidents and severe burns they've suffered while on the job, citing company management's policies to work quickly without protective gear or training. Of course, the injuries that the complainants describe were preventable, but it would require McDonald's and its franchisees to treat employees as human beings worth protecting. Their scars are more painful reminders of how giant corporations are burning low-wage workers and our communities.

The pressure-cooking job conditions people working at McDonald's described are not unique to the Golden Arches. I've met men and women from all walks of life who are working fast and furiously and with little reward. For far too long, we've allowed profitable corporations to ignore the basic well-being and needs of everyday Americans. Even as the cost of living goes up, wealthy CEOs have been hell-bent on keeping wages down, pocketing almost everything their employees produce for the company. This leaves our friends and neighbors who work for these incredibly profitable corporations living on the brink.

But this week, fast-food workers are going on strike to protest unsafe jobs and unfair pay. This time, they will be joined by Walmart associates and other retail employees, as well as caregivers, adjunct professors, and others who have had enough of working and still not being able to make ends meet. On April 15, they're using their collective voice to demand a better economic system - one that provides families with decent jobs and a starting wage of $15 an hour.

Yes, I said $15 an hour. Not $9, and not $10. These strikes were started by fast-food cooks and cashiers, but the movement has grown, and the response has been quite telling. Recently, Walmart, McDonald's, Target and The Gap have all responded to workers' demands, announcing moves to increase wages and some benefits for some of their workforce. Unfortunately, these minor wage hikes won't put enough money in people's pockets to pay the bills and take care of their families.

And when jobs don't pay enough, workers turn to critical public assistance in order to meet their basic needs. A new study from the Labor Center at the University of California Berkeley finds that states are spending $25 billion per year on public assistance programs provided to working families. If you have a job, you shouldn't need to rely on public assistance. But the people who help you pick out shoes or an outfit for your kids can't access enough hours to even cover their rent. The workers taking care of our grandparents don't even get overtime pay. And there are adjunct professors at some of our country's largest educational institutions who are living in their cars.

Even if you haven't experienced working in a minimum wage job, you should join together with the men and women taking on these profitable corporations. Certainly, these companies can afford to create jobs that pay people enough to actually live on, but nearly two-thirds of American households earn less money today than they did in 2002, despite the fact that corporate profits are at an all-time high. Moreover, you're the one bearing the costs of these low-wage jobs, because these employers offset wages and benefits onto taxpayers in the form of public assistance. So even if you never stop at a Wendy's or Taco Bell drive-thru, or you won't set foot in a Walmart, you're still picking up the tab for these companies' cheap labor.

Thankfully, there are several legislative initiatives emerging to hold CEOs of major corporations accountable for refusing to pay family-sustaining wages, denying basic benefits, and shifting their responsibilities onto taxpayers. For example, in Connecticut, a proposal for a Low-Wage Employer Fee would fine large companies that pay employees less than $15 per hour. The money recovered from the fee would fund critical early childhood education and healthcare services for low-income families, many of whom work for these big corporations.

Policies such as this one aim to level the playing field--to help right the dangerous imbalance in our economy and ensure that if you do well in America, you do right by America. If we don't stand up with those who are protesting this week, greedy corporations are going to continue to burn all of us, employees and taxpayers alike. But if we stand up together, we are heard. We are taken seriously. We make change happen.