SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

"It's a struggle. Especially with everything else being inflated in the country," said one US Army vet, "you know, with groceries, gas... I'm like, what the hell?"

Just as President Donald Trump and Republicans in Congress were warned would happen, close to 100,000 US veterans are currently behind on their mortgage payments or are in the process of foreclosure as a result of the White House's decision to shut down a Department of Veterans Affairs program that helped people with VA-backed home loans when they were behind on their monthly payments.

As NPR reported Thursday, more than 10,000 have already lost their homes, nearly a year after the Trump administration abruptly did away with the VA Servicing Purchase (VASP) program.

The program was rolled out during the Biden administration, after the VA ended a pandemic-era assistance program that had allowed VA home loan borrowers to gradually pay back mortgage payments that they had needed to skip.

Under VASP, the VA purchases home loans that were in default from mortgage services and then modified the loans.

In March 2025, a representative from the Mortgage Bankers Association told the House Veterans Affairs Committee that widespread foreclosures would result if the VASP program—which Republicans in Congress said had been created by former President Joe Biden for "political purposes... to undercut the VA Home Loan program—was not protected.

Despite the warning, the VASP program was halted two months later.

Nearly a year after the program's end, the VA is still developing a replacement to help veterans—many of whom are struggling to afford essentials just like the majority of other Americans as the cost of living crisis intensifies with rising fuel prices due to Trump's war on Iran.

Sources in the mortgage industry told NPR that many of the vets who have lost their homes so far had enough disability benefits or other income to avoid foreclosure, had the VASP program remained in operation.

NPR interviewed Leann Ledford, whose husband, a Marine veteran who served in Afghanistan, has a brain injury, experiences seizures, and suffers post-traumatic stress disorder. The family is one of tens of thousands who learned in October 2022 that the Biden administration had ended the earlier pandemic-era program and that they would have to pay a year's worth of back payments in one lump sum.

The Ledfords were also one of many veteran families who were unable to enroll in VASP before Trump abruptly shut it down.

Ledford told NPR that with her husband's $3,971 monthly disability check, they could have afforded mortgage payments under the VASP program.

Army veteran Jon Henry was also unable to enroll in VASP before it was shut down, and was forced to take a modified loan with payments that are $380 more per month than his original mortgage.

"It's a struggle," Henry told NPR. "Especially with everything else being inflated in the country, you know, with groceries, gas … I'm like, what the hell?"

NPR's reporting led Sen. Tammy Duckworth (D-Ill.), an Iraq War veteran, to denounced Trump as "the most anti-veteran president in history."

When Trump's new VA home loan assistance program is up and running—which isn't expected to happen for several more months, veterans will be able to move their missed payments to the back of their loan term. But in the current draft of the plan, reported NPR, "the VA is telling mortgage companies that if a new, modified loan at a higher interest rate only raises a veteran's monthly payment by up to 15%, they must place vets into that more costly loan."

"So a veteran with a $2,000 monthly mortgage payment could still be pushed into a modified loan that raises their payment by up to $300 a month. And they wouldn't be given the option of moving their missed payments to the back of their loan and keeping their original, lower-cost mortgage," reported the outlet.

Pete Mills of the Mortgage Bankers Association told the VA last month that under Trump's plan, "as drafted, veterans will continue to have worse options than similarly situated non-veterans."

"Buying a home has never been less affordable. Trump has made it worse."

With mortgage rates climbing and the median income a family needs to afford a home ballooning by nearly 50% in just the past five years, the advocacy group Groundwork Collaborative on Wednesday called on the federal government to take targeted, concrete actions to reverse the affordability crisis that President Donald Trump's policies are only making worse.

Groundwork's senior adviser for economic policy, Emily DiVito, joined former deputy director of the National Economic Council Bharat Ramamurti to release a report titled Unraveling the Mortgage Maze: How Government Can Make Homeownership More Affordable for American Families. The paper emphasizes that "at a time when American families are struggling with a severe housing affordability crisis, relief for overburdened consumers requires the federal government to reshape and strengthen its role in the mortgage financing system."

Because interest rates have been elevated since 2022, homeowners are "locked in" to their existing mortgages, with many young families feeling stuck in their "starter homes" even as they outgrow them. In addition to the impact on families, the "lock-in effect" is suppressing turnover, reducing supply, and contributing to more expensive houses.

Those consequences "ripple across generations and regions," wrote DiVito and Ramamurti in the report. "Today, younger families disproportionately confront a market in which suitable homes are scarce, mobility is costly, and the financial advantages once associated with homeownership are increasingly out of reach."

While the federal government intervened during the Great Depression and established new housing agencies and mortgage financing programs, homebuyers now have to contend with a "hybrid" system, with the government providing liquidity for financial firms and consumers relying on private loan services, lenders, and brokers to find an affordable mortgage and navigate the purchasing process.

Reducing home prices was part of the platform Trump campaigned on, but as with his tariffs' impact on grocery prices and the effect on electricity bills that his aggressive push for artificial intelligence expansion is having, the president's proposals would make the housing affordability crisis worse, DiVito and Ramamurti explained.

Trump and his Federal Housing Finance Agency (FHFA) director, Bill Pulte, "impulsively introduced a 50-year mortgage proposal in early November 2025 that would lower a family’s monthly payment on a median-priced home by less than $120, while saddling homeowners with higher interest rates and a slower path to equity," reads the report.

The administration is also working to privatize government-sponsored entities, which would raise mortgage rates and restrict credit "while generating huge windfalls for hedge funds and billionaires."

No other detailed proposals have been released by the White House for reducing costs for homebuyers, according to DiVito and Ramamurti.

The report offers four proposals that would provide families with "material relief":

Without congressional action, says the report, the Trump administration could lower the rate at which the mortgage insurance premium (MIP) is charged to borrowers—a step the federal government has taken before, as recently as 2023 when it saved an average of $453 annually for 1.1 million borrowers.

The government could also shorten the lifetime of MIP payments by requiring automatic termination earlier than currently required:

If a borrower puts down less than 10% on government-backed loans, the MIP will be assessed for the lifetime of the loan or until the borrower can refinance. If a borrower puts down more than 10%, MIP payments are automatically canceled after 11 years. [Private mortgage insurance] on the other hand, is supposed to be canceled automatically at 78% [loan-to-value], and borrowers can request early cancellation at 80%. However, many borrowers report that servicers fail to terminate their payments when they hit the threshold. Policymakers can amend Section 4902 of the Homeowners Protection Act (12 U.S. Code § 4902) to enable earlier cancellation of PMI, which is enforced by the [Consumer Financial Protection Bureau].

Policymakers can also expand offerings for mobile mortgages, "an underutilized home loan product that could deliver thousands in cost savings to homeowners each year." Allowing buyers to assume the existing rate of a seller or bring their current rate with them to their new home would alleviate the lock-in effect, "freeing up existing housing supply and making it easier for families to move affordably and when they want—no matter the interest rate environment."

Mobilizing a mobile mortgage could save a family up to $5,078 annually, and with Baby Boomers owning 28% of the nation's largest homes, "more affordable and flexible mortgage financing could free up millions of existing homes for younger buyers or large families," wrote DiVito and Ramamurti.

Government-provided direct loans at the cost of borrowing is named in the report as "the most direct role" the Trump administration could take in the mortgage market.

"Doing so would extend the benefits of the government’s cheaper financing directly to consumers," reads the report. "To ensure that the program targets the low- and middle-income homeowners who are most likely to need and benefit from cheaper financing, awards could be pegged to the median purchase price of single-family homes in any given area. Income and credit thresholds could also be established, as they already are for government-backed mortgages, to allow for more efficient underwriting."

Policymakers could also create a centralized online platform listing all mortgage lenders' terms, fees, eligibility requirements, and customer service information, bringing "closely held industry information out of the shadows, [and] equipping consumers with the knowledge necessary to navigate the mortgage market successfully."

The CFPB found that 30% of borrowers do not comparison-shop for their mortgage and more than 75% apply for a mortgage at just one lender—costing the average homebuyer about $300 per year.

Making a centralized database available to borrowers would stop lenders from colluding on mortgage rates as Wells Fargo, Rocket Mortgage, and JPMorgan Chase have been accused of doing in a recent class action lawsuit.

"By leveraging the government’s unique financing power and regulatory authority to craft a mortgage system that is simpler, less costly, and more responsive to households’ needs," wrote DiVito and Ramamurti, "millions of families who feel buying a home is out of reach may finally be able to achieve and maintain homeownership."

We too have a little bird trying to call our attention to a major problem. That bird is the insurance industry with its army of actuaries.

As the cost of insuring our houses escalates around the United States and the world, it appears that property insurance is acting like a canary in a coal mine.

Canaries used to be taken into coal mines because they served as an early warning system if dangerous gases were building up. Since the canaries were more sensitive to these gases than people, they protected the miners from life-threatening conditions. When the canary dropped dead, the miners could still get out.

Like the canaries, the actuaries who interpret data for insurance companies are more sensitive than most individual people to changes going on in the world. Actuaries earn big salaries because the financial health of their employers depends on them.

Things have already gotten so bad that the National Academies of Sciences, Engineering, and Medicine (NASEM) recently sponsored a webinar panel discussion: "Extreme Weather Events and Insurance: Households, Homeowners, and Risk." (This link will take you to a video of the event.)

Any coal miner who refused to evacuate a mine when the mine’s canary keeled over—perhaps saying, “I don’t believe there is any real danger here”—would not have been long for this world.

The panelists were located in the United States (Washington, DC and Madison, Wisconsin) and England (London and Cambridge). Climate changes are not limited to the United States, nor is awareness that we need to do something about them if we can.

The panelists were not grinding particular political axes. They were discussing the measured fact that an increasing number of extreme weather events are destroying valuable property—housing, commercial buildings, streets, bridges, etc.—requiring insurance company payouts to policyholders.

These insurance payouts must be financed by the premiums charged to people who are insuring their property. As damages increase, the premiums also have to increase. Although premiums may be regulated by state regulators, if they do not allow the needed increases insurance companies will pull out of doing business in that state.

As insurance companies pull out, it may become more and more difficult—perhaps even impossible—for people to insure their houses. But if a house cannot be insured, banks won’t finance a mortgage on it, and if it cannot be financed the owner may be unable to sell it.

For many people, their home is their primary investment, and they cannot afford to live in it if they cannot insure it. If it burned down or was otherwise destroyed, they would be wiped out financially. But if they cannot sell it, then the homeowner is a real pickle.

Disrupted housing markets can produce disastrous results for a country’s economy in general, as we Americans discovered during the recession beginning around 2008.

The impact of a world that is heating up is not being felt as much in the United States as in many other countries in Europe, Africa, and Asia which are suffering from unusually long bouts of very hot weather, flooding downpours alternating with extreme droughts, forest fires, etc. Some island nations may be literally wiped out as melting icebergs and glaciers increase sea level, putting them underwater.

But enough extreme weather events are already occurring in the United States that the insurance companies must make major increases in their prices.

Any coal miner who refused to evacuate a mine when the mine’s canary keeled over—perhaps saying, “I don’t believe there is any real danger here”—would not have been long for this world.

Americans who continue to politicize discussion of global warming—either denying its existence, its extent, its speed, or its seriousness—will be like that coal miner. We too have a little bird trying to call our attention to a major problem. That bird is the insurance industry with its army of actuaries. We ignore that warning at our own risk, and at the risk of our children and grandchildren.

The basic story here is that in order to give donors in the financial industry still more money, Trump is planning to privatize a perfectly well-functioning public system for securitizing mortgages.

In Washington no bad idea stays dead long. Therefore it should not be surprising that U.S. President Donald Trump is planning to move forward with plans to privatize Fannie Mae and Freddie Mac, the mortgage giants that have been in government conservatorship for almost two decades.

As with many of the moves undertaken by Trump, it is not clear what problem this is meant to solve. For the period they have been in conservatorship, Fannie and Freddie have been securitizing mortgages at a low cost and have not faced any substantial management problems.

There is of course one problem that privatizing Fannie and Freddie would solve. This is yet one more way that the financial industry can run up some profits and high pay for top executives at the expense of the rest of us.

The Congressional Budget Office calculated that having private institutions, rather than Fannie and Freddie in their current form, would add roughly 20 basis points, 0.2% to the cost of securitizing mortgages. With around $1 trillion in mortgages being securitized each year, that comes to $2 billion annually. That is not huge in the context of the federal budget (0.03%), but it is four times the annual appropriation for the Corporation for Public Broadcasting that got Trump so upset.

Trump is giving a green light to his finance buddies to find every more creative ways to rip off businesses and ordinary people.

And in the case of privatizing Fannie and Freddie, we literally get nothing for it except a less efficient mechanism for securitizing mortgages. This is similar to the plans for privatizing Social Security. We have an extremely efficient public system, but many people in the Trump administration see the opportunity to make trillions of dollars in fees by turning it into a private system.

As with a privatized Social Security system, we would also be exposing ourselves to needless risk by privatizing Fannie and Freddie. The basic problem is that we would be allowing a private corporation to operate with a government guarantee against losses. This guarantee gives a private securitizer an enormous incentive to securitize bad mortgages in order to increase volume and make more profits. That was the story of the housing bubble and the subsequent collapse and financial crisis in 2008-09.

If a private securitizer is carefully regulated, it can limit the risk of reckless lending. But does anyone believe that the Trump administration is going to have careful regulation of the financial industry?

The basic story here is that in order to give donors in the financial industry still more money, Trump is planning to privatize a perfectly well-functioning public system for securitizing mortgages. This move will almost certainly increase the cost of mortgages for homebuyers, the only question is by how much. And it raises the risk for future financial crises and government bailouts.

Making the financial sector less efficient in order to hand money to contributors is very much front and center in the Trump administration. This is the same story with his decision to promote crypto currency, which is making Trump and his friends tens of billions of dollars; as opposed to letting the Federal Reserve Board issue a digital currency, which would save us tens of billions in bank and credit card fees.

The evisceration of the Consumer Financial Protection Bureau follows the same pattern. Trump is giving a green light to his finance buddies to find every more creative ways to rip off businesses and ordinary people.

That’s how we should understand the drive to privatize Fannie and Freddie. How could anyone oppose it?

"The president promised to lower costs on day one, and by that standard, he's broken that promise and has made choices that will cost families thousands of dollars a year," said one policy expert recently.

The Trump administration has made its desire for Americans to expand their families well known, but a new survey out Monday details how a growing number of people are postponing such major life decisions—including having children, buying a home, or expanding their education—due to the economic anxiety created by President Donald Trump's policies.

The Harris poll was conducted on behalf of The Guardian between April 24-26, in the wake of the news that the White House was considering multiple ways to encourage people to have more children. The proposals being floated by "pronatalist" advisers include a $5,000 "baby bonus" that the administration would offer to people when they have a new baby—which would cover less than half of the average annual cost of childcare in the United States.

The survey suggested that the proposal was not enticing to would-be parents in the U.S., with 65% of people who had previously planned to have a child in 2025 reporting they were now holding off on the decision. Thirty-three percent said they were not comfortable expanding their families in the current economy, and 32% said they were unable to afford having a child.

Trump has imposed and rolled back various tariffs several times since taking office; the White House announced Monday that reciprocal tariffs with China were being paused for 90 days while the two countries try to work out a trade deal. Tariffs on Canadian and Mexican goods are partially in effect, and the administration has also imposed tariffs on aluminum and steel imports, cars, and car parts.

The U.S. economy contracted in the first quarter, with the gross domestic produce declining at an annual rate of 0.3% after having climbed by 2.4% in the final quarter of 2024.

For Americans, the tariffs have meant higher prices for items like toys, children's clothes, household tools, and washing machines.

As Common Dreams reported last week, despite Trump's proposal of a "baby bonus," Groundwork Collaborative executive director Lindsay Owens has termed the tariffs a "baby tax"—directly causing essentials like strollers, high chairs, and cribs to cost more.

"The president promised to lower costs on day one, and by that standard, he's broken that promise and has made choices that will cost families thousands of dollars a year," said Groundwork Collaborative fellow Michael Negron told a U.S. House committee last week.

Nearly 80% of people surveyed said they've experienced higher grocery prices since Trump took office—despite the fact that he explicitly promised his presidency would swiftly bring about a lower cost of living—and 60% said they noticed their monthly bills going up.

The Harris poll found that 66% of people are now putting off making large purchases like cars or home appliances under Trump's economy, and three-quarters of those who had previously been hoping to buy a home are postponing that purchase.

Mortgage rates are currently 6.7%—more than double what they were four years ago.

CNN reported last month that although interest rates on home loans have been falling, "President Donald Trump's scattered approach to tariffs and an escalating trade war with China has injected volatility into the stock market, and resulted in a sell-off in U.S. bonds last week."

Sixty-eight percent of Millennial and Gen Z renters—those in their 20s, 30s, and early 40s—said they had a goal of buying a home, compared to 29% of older renters, suggesting that the major life decisions of younger Americans are being most affected by the Trump administration.

The Harris poll also asked respondents if they believed the economy is worsening, and found a partisan divide: 33% of Republicans said yes compared to 73% of Democratic voters who agreed.

But among Independents—44% of whom supported Trump in the 2024 election, according to a post-election survey—64% agreed with the majority of Democrats about the economy's trajectory.

Nearly a third of respondents said they believe Trump's tariffs will cause the most harm to their household finances, despite the president's claims that the tariffs will "make America wealthy again."

During his testimony last week, Negron said that higher prices on essential goods and services "are the types of things that you would expect to hear when you look at what experts have said, that [tariffs are] going cost anywhere from $4,500 to $5,000 more for the average household once they're fully in effect."

"When you look at the promises to lower prices," he said, "the administration is not living up to them."

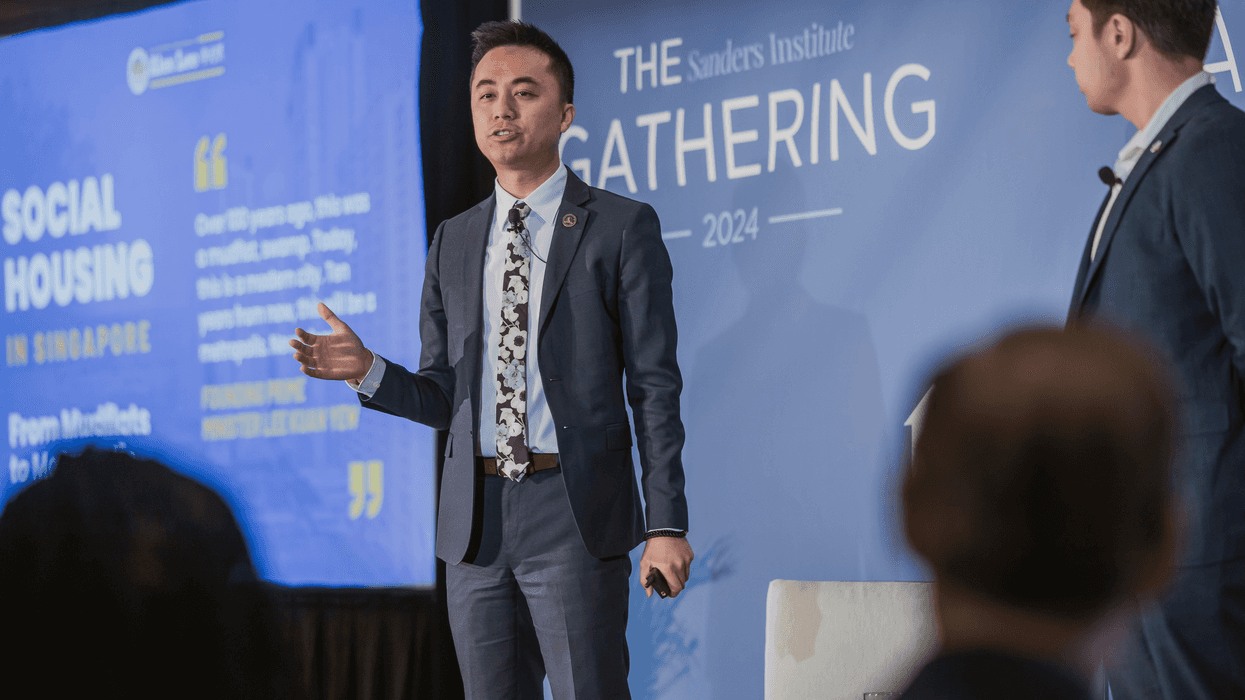

The housing crisis is threatening to make the American dream impossible. What’s needed is the will and investment necessary to bring social housing—publicly developed homes for residents of mixed incomes—to California.

California is the epicenter of the national housing shortage. Over half of California renters—and four in ten mortgaged homeowners—are cost-burdened, which means they pay more than 30% of their income on housing. And I am one of them.

Yet of the 120 members of the California State Legislature, I’m one of the only five renters.

In the Bay Area district I represent, home prices average roughly $1.5 million and modest apartments rent for over $2,000 per month. It’s impossible for most working people to afford to buy a home in my district. Too many of my friends and family have been priced out of the communities we grew up in.

To address this urgent crisis, I have tirelessly pursued a policy that has successfully ended housing shortages in jurisdictions around the world: social housing.

Social housing is the public development of housing for residents of mixed incomes. I have introduced the California Social Housing Act every year since I took office. I fought to become Chair of the Select Committee on Social Housing, and I’ve participated in delegations to Vienna, Austria, and Singapore to study their social housing systems.

As that dream becomes impossible for so many Americans, there remains one tool that has realized that dream for millions of people around the world.

Vienna and Singapore have important lessons for us on how social housing can actualize housing as a human right.

In both cities, social housing emerged from crisis. After a crushing defeat in World War I, Vienna saw the collapse of its monarchy and extremely overcrowded living conditions. Singapore experienced destruction during World War II and emerged from both Japanese and British colonization with a severe housing shortage. Squatter settlements were devastated by fire in 1961, leaving about 16,000 people homeless. Today, the two governments are identified with opposite ends of the political spectrum—left-leaning Vienna compared to the more right-leaning Singapore—but both housed their populations through social housing.

- YouTubewww.youtube.com

In Singapore, the Housing and Development Board builds 99-year leasehold flats that it sells to citizens. It has built so many units that roughly 80% of Singapore’s population live in them. Nine out of ten of these residents own their homes. Homeowners have the right to resell them, rent them out, and pass them to their heirs. These condos appreciate in value over time, enabling them to generate wealth. Only citizens and permanent residents may buy these flats, so no private equity firms, corporations, or speculators can game this system.

Vienna—sometimes referred to as the “Renters’ Utopia”—builds social housing for rent with indefinite leases that tenants never need to renew and can even pass down to their children. Over 60 percent of its residents live in social housing. As in Singapore, most residents qualify for social housing under the high income cap that encompasses 75% of the Viennese population. This income limit only applies when the tenant moves in. Without constant eligibility screenings, tenants may remain even if they make more money in the future, enabling socioeconomic integration of social housing neighborhoods. Residents pay about a third less rent than their counterparts in other major European capitals. Even private sector renters enjoy strong tenant protections.

While Singapore and Vienna offer different social housing models, both governments prioritize creating housing for the public good. The foundation of their policies are the finances, land banking powers, and expertise to build housing as a human right.

The result? Both are consistently ranked as the most livable cities in the world.

California today is well positioned to implement what Vienna and Singapore undertook in the past century. What’s needed here is the political will to bring social housing to our state. We can’t afford to wait.

The harsh reality is that California has roughly 30% of all people experiencing homelessness in the nation. The Golden State must build at least 2.5 million more homes by 2030 to end the current shortage. But California built just 85,000 housing units annually from 2018 to 2022.

California today is well positioned to implement what Vienna and Singapore undertook in the past century. What’s needed here is the political will to bring social housing to our state. We can’t afford to wait.

Today’s social housing proposals avoid the mistakes of the past by creating socioeconomically integrated, financially self-sustaining housing. And momentum is building nationwide. In 2023, my social housing bill was approved with two-thirds majorities in both houses of the California Legislature, but was vetoed. In 2023, Seattle voters approved a ballot measure to create a social housing developer. The state of Hawaii has passed legislation to develop social housing. Montgomery County, Maryland, is at the forefront of creating publicly developed, mixed-income housing through the Housing Opportunities Commission. The Commission serves roughly 17,500 renter households and owns more than 9,000 rental units.

Earlier this year, British Columbia, Canada, announced a CAD $4.95 billion (USD $3.67 billion) social housing initiative. Called BC Builds, the plan is to build 8,000 to 10,000 homes over the next five years, which could be the world’s largest new social housing program in decades.

The American dream has long been centered on having your own home. As that dream becomes impossible for so many Americans, there remains one tool that has realized that dream for millions of people around the world.

Let’s learn from our global peers and embrace social housing as a proven tool to solve our housing crisis.

Building a movement to stop Wall Street’s insatiable greed starts with labor unions, like the United Auto Workers, that have shown the willingness to take on corporate power, not only to protect their own members, but also to enhance the working class as a whole.

Purchasing a home is usually the only pathway for the working class to accumulate a bit of wealth. Today, working-class home-buying is increasingly out of reach. Housing rent inflation also remains stubbornly high, further squeezing working people, as well as causing the Federal Reserve to fret about why inflation isn’t falling faster.

While economists hunt for technical explanations, they ignore the ways in which Wall Street has come to dominate the housing market to the detriment of working people. The real story is about how our two major political parties have sold out to financialized capitalism.

In 2008 Wall Street crashed the housing market, by profiting wildly from unregulated artificial mortgage-backed bonds. When that house of cards collapsed, they were bailed out with our tax dollars. Then, Wall Street rushed in to buy up housing assets on the cheap, turning them into rentals and profiting yet again from the very mess it had created. And now the working class is being squeezed out of the homeowner market and paying more and more for rentals.

It wasn’t always this way. Following the crash of 1929, caused by massive financial malfeasance, the New Deal ushered in a strong regulatory regime to control the inherent greed of the banking and securities businesses. For 25 years after those stiff regulations went into effect, the standard of living for the working class steadily increased and there were no Wall Street implosions.

The real story is about how our two major political parties have sold out to financialized capitalism.

Those regulations held until the Reagan and Clinton administrations removed many of the guard rails intended to constrain the ability of financiers to manipulate and threaten our economy. Financial recklessness and greed once again were given free rein. By 2008, Wall Street had thoroughly crashed the economy, leading to six million jobs lost in a matter of months.

I gave the crash a good look in my book, The Looting of America. The machinations of Wall Street in the early part of this century involving the housing market were beyond belief. Freed from all serious oversight, large banks and financial firms believed they had engineered a financial miracle – taking all the risk out of high-risk mortgages. They created artificial investment products that the trusted credit rating agencies assured us were as good as gold. Rated AAA, they said.

Sub-prime mortgage-backed securities, built repeatedly upon the same risky mortgages, promised big safe profits, and sold like hot cakes. When those risky mortgages inevitably failed, so did the supposedly safe securities, and the whole system crumbled.

Incredibly, at the same time, some of the richest Wall Streeters created financial products designed to fail, so that they could bet against them. They made billions!

This is the type of garbage that led to the 1929 crash and the Great Depression. In 2008 it was called the Great Recession. Economic devastation, fueled by unregulated banks and securities firms, happened again.

The damage done was so great that the government used taxpayer money to bail out the financial bandits, fearing that if they didn’t the whole economy would collapse into another Great Depression. None of the financial criminals went to jail. Very few suffered serious financial harm. But with the collapse of the housing market millions of homeowners were left with underwater mortgages. The only bailout for them was bankruptcy and ruination.

The country was angry, and this disaster created the perfect opportunity to reregulate Wall Street so that it served the American people, not the other way around.

President Obama, in 2009, understood the public fury aimed at the high salaries that the financial titans had the gall to award themselves even as they were accepting taxpayer support. The CEOs argued that they still needed to pay top dollar for executives during the bailout because, “We’re competing for talent on an international market.”

Obama warned, “Be careful how you make those statements, gentlemen. The public isn’t buying it.” Then he made a telling concession: “My administration is the only thing between you and the pitchforks.”

Obama never channeled the popular anger to bring Wall Street to heel. Instead, that fury energized the Tea Party, which turned the attacks away from Wall Street and towards the government itself. That was the fury Trump rode to power.

Meanwhile, the banks grew larger, richer, and more concentrated than ever. Today the top five banks own more banking assets they had before the 2008 crash. More worrisome yet is that hedge funds and private equity companies, which are far less regulated than banks, now hold more than $25 trillion in assets, making them larger than all of commercial banking.

Due to Wall Street’s financial implosion and the mortgage crisis, housing prices collapsed after the 2008 crash. Big money institutions rushed in and bought up as much housing as possible. No regulator, no political party, no movement stopped them from exploiting the crisis Wall Street itself had created.

Smack in the middle of the financial crisis in New York City, private equity companies had the chutzpah to buy thousands of apartment buildings, hoping to jack up stabilized rents as soon as tenants moved out. To move things along, these new owners applied a bit of pressure. “Tenants have been sued repeatedly for unpaid rent that has already been received by the landlords; they have been sent false notices of rent bills, lease terminations and non-renewals; and they have been accused of illegal sublets,” reported Gretchen Morgenson in the New York Times.

Now, after 15 years of Wall Street housing purchases, regular home buyers are getting squeezed out of the market. About 20 percent of all home purchases in the third quarter of 2022 went to corporations that owned more than 100 properties, with half of the Wall Street buyers owning more than 1,000. If you need a mortgage to buy a home you are likely to lose out to the big boys.

“They are, by definition, cash buyers. They don’t have mortgages; they don’t have contingencies; they’ve got briefcases full of cash, ready to go,” reports CoreLogic data.

In the Bradfield Farms subdivision in Charlotte, North Carolina, in 2021-22, fifty percent of the homes were bought by investors with cash and turned into rentals, according to an investigation by the New York Times. And we wonder why it’s so hard for young working people to purchase a home.

After fifteen years of abuse, politicians are finally taking notice. Two Democratic legislators from North Carolina, Jeff Jackson and Alma Adams, recently introduced the American Neighborhoods Protection Act, which would require a corporate owner of more than 75 single-family homes to pay an annual $10,000 fee per home into a trust fund to help family buyers with down-payments. But, in the divided Congress, this bill isn’t going anywhere.

Why wasn’t it presented, one wonders, when the Democrats were in full control? Maybe because if it was pushed forward, Democrats would have to choose between placating Wall Street or defending working-class homebuyers. Hmm, which way do you think they would go?

It is time to wake up to what Wall Street is doing to us.

But we shouldn’t just be angry at the politicians who have coddled Wall Street for 40 years in exchange for campaign contributions (and lucrative financial jobs after leaving public office). We need to look at ourselves and our collective organizations.

In 2008, Wall Street was on its knees begging for support. The financial barons were at their weakest point since the Great Depression. To extract serious financial reforms, we needed a mass movement that united labor unions with the many community and environmental groups around the country. It didn’t happen.

It is time to wake up to what Wall Street is doing to us. Not only did it crash the economy in 2008. Not only does it now control more and more of the housing market, but it is also destroying the lives of working people through mass layoffs. As Wall Street gorges itself on stock buybacks, (another result of deregulation in 1982), 30 million of us have lost our jobs in mass layoffs, jobs often sacrificed as corporations pay for those buybacks Wall Street demanded. (Please see Wall Street’s War on Workers for more about this.)

Building a movement to stop Wall Street’s insatiable greed starts with labor unions, like the United Auto Workers, that have shown the willingness to take on corporate power, not only to protect their own members, but also to enhance the working class as a whole.

A new movement could be built around leaders like UAW president Shawn Fain, who recently said: “Billionaires, in my opinion, don’t have a right to exist.”

That the anger and energy of indignation is still out there, waiting to coalesce and aim at taming Wall Street’s insatiable greed. We should join with Fain and other progressives to mobilize and harness it now.

Sooner would be much better than waiting for the next crash.

Bankruptcy was designed so people could start over, but these days, the only ones starting over are those with enough political clout to shape bankruptcy laws to their liking.

Within days of a nearly $150 million judgment against former New York Mayor Rudy Giuliani for defaming Ruby Freeman and Shaye Moss, the election workers Giuliani falsely claimed stole the 2020 election in Georgia for President Joe Biden, Giuliani filed for bankruptcy.

He thereby shielded himself from having to surrender his assets to fulfill the judgment, at least in the near term.

The long term may be quite long. Freeman and Moss may not see a penny of that judgment for many years, and when they do, it’s likely to be far less than $150 million.

The prevailing myth that America has a “free market” existing outside and apart from government prevents us from understanding that the very rules by which the market runs—including the basic one about what to do when someone can’t or won’t pay what they owe—are made by lawmakers.

One of the most basic of all questions in a market economy is what to do when someone can’t pay what they owe. The U.S. Constitution (Article I, Section 8, Clause 4) authorizes Congress to enact “uniform Laws on the subject of Bankruptcies throughout the United States.”

Congress has done so repeatedly. In the last few decades, Congress’ changes have reflected the demands of the wealthy, giant corporations, and Wall Street banks, which have made it harder for average people to declare bankruptcy but easier for themselves to do it.

Many people are too broke to go bankrupt. Filing for bankruptcy costs money, as does hiring an attorney (which is the best way to make sure you actually get debt relief). Because attorney fees, like other debts, are wiped out in a bankruptcy, most bankruptcy lawyers require clients to pay in full before filing.

In an economy where nearly half of adults say that if they were hit with an emergency expense of $400, they wouldn’t have the cash on hand to cover it, large numbers of people simply can’t afford those upfront costs.

The 2005 bankruptcy bill pushed by Wall Street worsened the problem. To prevent people from cheating their lenders, the bill put new burdens on debtors and their lawyers. The extent of such abuses was questionable, but the new requirements have driven up attorney fees nationwide by about 50%. The result? Even fewer filings.

Bankruptcy was designed so people could start over. But these days, the only ones starting over are those with enough political clout to shape bankruptcy laws to their liking, and enough money to hire bankruptcy lawyers to use those laws to their full advantage.

On the opening day of Trump Plaza in Atlantic City in 1984, Donald Trump stood in a dark topcoat on the casino floor celebrating his new investment as the “finest building in the city and possibly the nation.”

Thirty years later, after the Trump Plaza folded, Trump was on Twitter praising himself for his “great timing” in getting out of the investment. He got a giant tax write-off, too.

But some 1,000 of his former employees were left holding the bag—without jobs, and with homes worth a fraction of what they paid for them. They couldn’t declare bankruptcy. Chapter 13 of the bankruptcy code—whose drafting was largely the work of the financial industry—prevents homeowners from declaring bankruptcy on mortgage loans for their primary residence.

The Granddaddy of all failures to repay occurred in September 2008 when Lehman Brothers went into the largest bankruptcy in history, with more than $691 billion of assets and far more in liabilities.

Some commentators (including yours truly) urged that the rest of Wall Street should be forced to grapple with their problems in bankruptcy, too.

But Lehman’s bankruptcy so shook the street that Henry Paulson Jr., George W. Bush’s outgoing secretary of the treasury (and, before that, head of Goldman Sachs), persuaded Congress to authorize several hundred billion dollars of funding to protect the other big banks from going bankrupt.

Paulson didn’t explicitly state that big banks were too big to fail. They were, rather, too big to be reorganized under bankruptcy—which would, in Paulson’s view, have threatened the entire financial system.

The real burden of Wall Street’s near meltdown fell on homeowners. As home prices plummeted, many found themselves owing more on their mortgages than their homes were worth and unable to refinance.

Some members of Congress tried to amend the bankruptcy law so distressed homeowners could use bankruptcy, which would have helped prevent the banks from foreclosing on their homes. But the financial industry (among the largest donors to both parties) claimed this would greatly increase the cost of home loans (no convincing evidence showed this to be the case), and the bill died.

Subsequently, more than 5 million people lost their homes.

Another group of debtors who can’t use bankruptcy to renegotiate their loans are former students laden with student debt.

Student loans are now about 10% of all debt in the United States, second only to mortgages and higher than auto loans and credit card debt. But the bankruptcy code doesn’t allow student debts to be worked out under its protection.

If graduates don’t meet their payments, the law allows lenders to garnish their paychecks. If they are still behind on student loan payments by the time they retire, lenders can even garnish their Social Security checks.

The only way graduates can reduce their student debt burdens—according to a provision enacted at the behest of the student loan industry—is to prove that repayment would impose an “undue hardship” on them and their dependents.

This is a stricter standard than bankruptcy courts apply to gamblers trying to reduce their gambling debts.

For years, Purdue Pharma, the maker of the prescription painkiller OxyContin, was entangled in civil lawsuits seeking to hold it accountable for its role in the spiraling opioid crisis.

A major settlement reached last year seemed to end thousands of those cases. It exempted members of the billionaire Sackler family, which once controlled the company, from all civil lawsuits in exchange for billions of dollars toward fighting the epidemic (although aware of OxyContin’s risk for abuse, members of the family had continued to aggressively market it).

Under the deal, the Sacklers do not have to personally declare bankruptcy and are insulated from liability even without the consent of all of those who could potentially sue them. (The Supreme Court has taken up the case.)

The prevailing myth that America has a “free market” existing outside and apart from government prevents us from understanding that the very rules by which the market runs—including the basic one about what to do when someone can’t or won’t pay what they owe—are made by lawmakers.

The real question is whose interests those lawmakers are pursuing. Are they working for the vast majority of Americans, or are they beholden to those at the top? The recent history of bankruptcy—right up to Rudy Giuliani’s use of it last week—provides a clear answer.

To act today, based on the fierce urgency of now, we must make the investments to eliminate racial disparities within one generation.

It’s now been 60 years since the March on Washington for Jobs and Freedom—and the Reverend Martin Luther King, Jr.’s “I Have a Dream” speech.

At the rally, Dr. King famously proclaimed that all people, Black as well as white, have a “promissory note” from their government guaranteeing “the inalienable rights of life, liberty, and the pursuit of happiness.” He lamented that “America has defaulted on this promissory note” to Black citizens.

Six decades later, despite incremental progress on some fronts, the check has still come back marked “insufficient funds.” But with enough political will, we can clear it quickly. That’s the conclusion of our new report, Still a Dream: Over 500 Years to Black Economic Equality.

For many important economic indicators, the pace of progress has been so incremental that it would still take centuries for Black Americans to reach parity with whites.

There are important signs of progress to mark. The unthinkably high rate of Black poverty has diminished since King’s time, falling from 51% in 1963 to 20% by 2021. But with 1 in 5 Black Americans still living in poverty—and 1 in 12 whites—it’s hardly a moment to pop the champagne bottle.

Other positive indicators include a sharp increase in Black high school attainment over the last 60 years and a significant decline in Black unemployment. For many important economic indicators, however, the pace of progress has been so incremental that it would still take centuries for Black Americans to reach parity with whites.

For example, the Black-white income gap has barely narrowed at all. In 1967, African Americans earned 58 cents for every dollar earned by whites. By 2021, that had risen to just 62 cents on the dollar. At this rate of progress, it would take Black households 513 years to reach income parity with their white counterparts.

Progress in narrowing the racial wealth divide has been even slower. In 1962, Blacks had 12 cents of wealth for every dollar of white wealth. By 2019, the last year of comprehensive data, Blacks had just 18 cents for every dollar of white wealth. At this pace, it would take 780 years for Black wealth to equal white wealth.

There has been essentially no progress in narrowing the gap between white and Black rates of homeownership, another key indicator of wealth and well-being. Sixty years later, there remains roughly a 30 percentage point gap, with 44% of Black households owning a home compared with 74% of whites.

In part, our country’s failure to bridge the racial economic divide reflects the growing inequality in our society overall.

During the last 40 years, America has experienced extreme levels of income and wealth inequality, with most gains flowing into the hands of the wealthiest—and mostly white—1%. This has contributed to the stalling of progress toward racial equity, along with government withdrawal from investments such as affordable housing.

What could put us back on track? Without a doubt, the persistent Black-white divide requires racially targeted commitments to individual asset-building and other forms of reparations.

But other programs—including full employment, a government jobs program, universal healthcare, and a massive commitment to homeownership—would reduce racial inequality and lift up all those suffering from 40 years of stagnant wages, regardless of their race.

Many of these investments could be paid for by wealth taxes aimed at reducing dynastic concentrations of wealth and power, among other efforts to get the very wealthy to pay their fair share in our unequal country.

At the Lincoln Memorial 60 years ago, King exclaimed: “We have come to this hallowed spot to remind America of the fierce urgency of now. This is no time to engage in the luxury of cooling off or to take the tranquilizing drug of gradualism.”

Taking over half a millennium to close our racial economic divide is gradualism in the extreme.

To act today, based on the fierce urgency of now, we must make the investments to eliminate racial disparities within one generation.

Sixty years after bouncing the check, it is time to fulfill America’s promise with a bold response.