A volunteer with Forgotten Harvest loads food into a vehicle at a mobile pantry April 14, 2020 in Detroit, Michigan. The organization distributes food throughout the metro area, which has seen an uptick in demand due to the Covid-19 pandemic. (Photo: Gregory Shamus/Getty Images)

The Biden Rescue Plan Is Neither Risky Nor a Distraction From Structural Issues

The risks of going too-big are trivial. The risks of going too-small are large—letting the unemployment shock from Covid-19 linger for years.

Economist Larry Summers raised fears today that the Biden administration's economic rescue plan might go too far, leading to economic overheating or squandering political and economic space for long-run reforms down the road. Neither of these fears are very compelling.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions.

On the first-the danger of economic overheating-there's not much more to add to what I and several others have already said on this: The U.S. economy has run far too-cool for decades, and this has stunted growth and deprived millions of potential job opportunities and tens of millions of potential opportunities for faster pay raises. Frequently, those worried about overheating cite current estimates from the Congressional Budget Office (CBO) of the "output gap"--the gap between income generated in today's economy and what could be generated (or potential output) if there was no downward pressure on spending by households, businesses, and governments (aggregate demand). These current CBO estimates look relatively small compared to the Biden rescue plan's fiscal support. But, these current estimates are almost certainly too-small. To provide just one piece of evidence--these estimates suggest that the economy was running above potential output in 2019 before Covid-19 struck. But there was no evidence of overheating that year--price inflation was tame and wage growth actually decelerated.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions. If this happens, and if the unemployment rate falls far beneath what it was in the pre-Covid period and stays below this for a few years, this will be an affirmatively good thing, not something to fear.

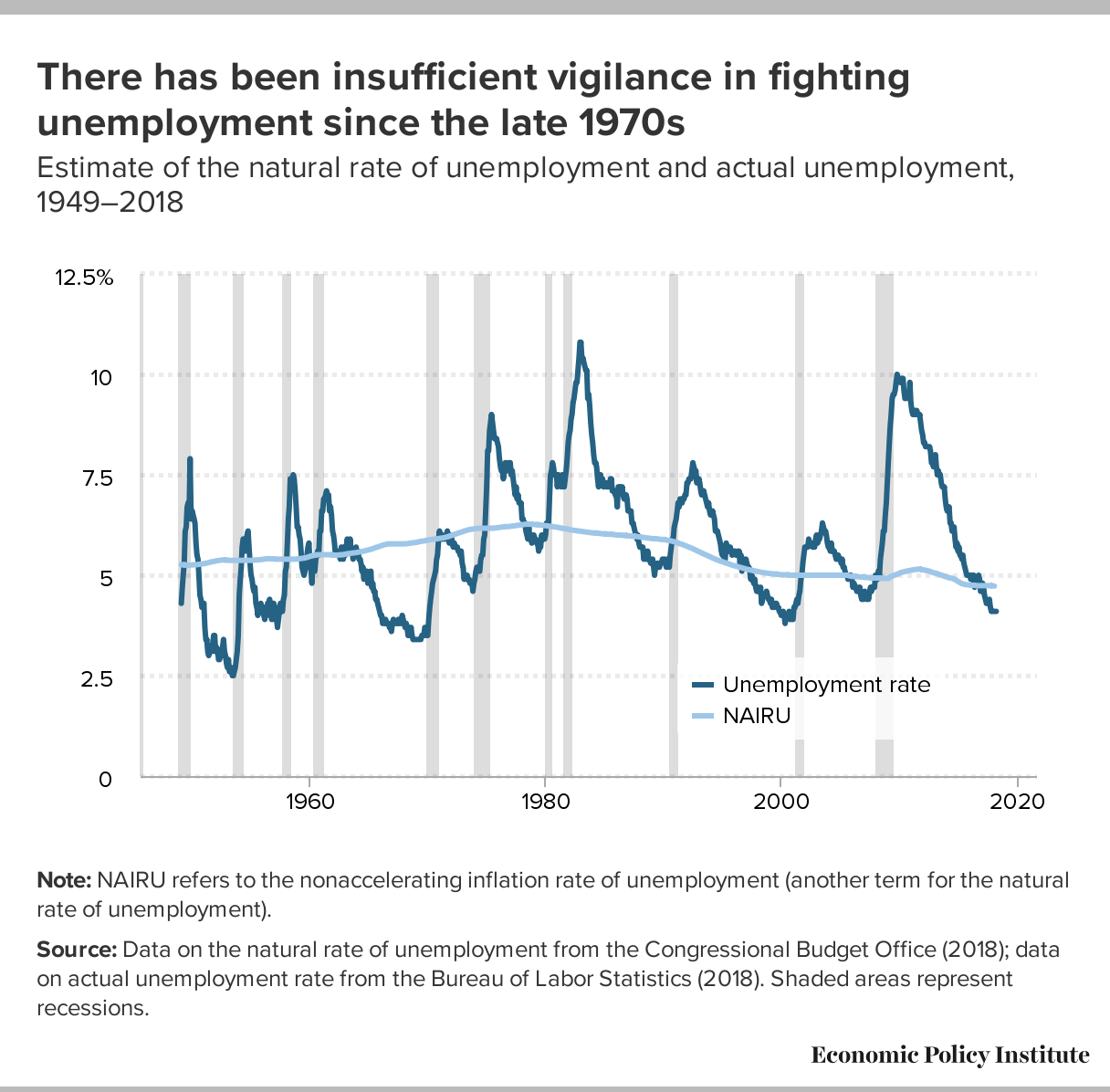

To be really clear about this--the unemployment can fall quite a ways beneath estimates of the so-called "natural rate" (or, the lowest rate of unemployment thought to be consistent with stable inflation in the long-run) for extended periods of time without disaster striking--look at the years before 1979 on this chart--we spent lots of time beneath the natural rate and had substantially faster growth (and more equal growth) than we've had since.

{kind=link}

In decades past, it was taken as near-gospel among macroeconomic policymakers that their main concern should be keeping inflationary pressures in check. After an episode of high inflation in the 1970s, some of these policymakers adopted an implicit strategy of "opportunistic disinflation." The idea was not to affirmatively engineer recessions per se, but, following each recession the subsequent recovery in the unemployment rate was cut a bit short before it reached its previous low, hence putting consistent downward pressure on inflation (including wage inflation). This decades-long period of keeping labor markets softer than they needed to be to keep inflation stable (and instead targeting downward pressure on inflation) had huge costs. These soft labor markets were as important as any other factor in explaining the anemic wage growth faced by typical workers in those years and in the rise of wage inequality.

The Biden plan is essentially the reverse of opportunistic disinflation--it's opportunistic go-for-growth. Yes, there are several factors arguing that the economy could be well-poised to return unemployment to non-crisis levels relatively soon even without quite as big a plan. But, so what? Why not do even better than that? As many have pointed out, the risks of going too-big are trivial--a period of inflation that the Federal Reserve is well-equipped to neutralize. The risks of going too-small are large--letting the unemployment shock from Covid-19 linger for years.

The second worry expressed by Summers is a pure political calculation--that the Biden administration has a fixed lump-of-political-capital and spending too much on pure relief and recovery measures (when a smaller package will do) leaves too little available for pressing long-run issues yet to be addressed (think climate measures, green investment, care investments, etc.). He's clearly right that it would be a terrible thing if political miscalculations early in Biden's term led to less movement on these important issues. But, it also seems like a key way to build public confidence in the federal government's ability to do big things skillfully is to quickly smother the virus and engineer a rapid return to low unemployment.

Finally, I'll just note that when criticizing the Biden rescue plan, critics really do need to decide whether or not the $1,400 checks included in it are a problem because they make the plan "too big" and likely to cause overheating, or are a problem because they will "just be saved." If the checks are saved, then the economy will not overheat.

An Urgent Message From Our Co-Founder

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

Economist Larry Summers raised fears today that the Biden administration's economic rescue plan might go too far, leading to economic overheating or squandering political and economic space for long-run reforms down the road. Neither of these fears are very compelling.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions.

On the first-the danger of economic overheating-there's not much more to add to what I and several others have already said on this: The U.S. economy has run far too-cool for decades, and this has stunted growth and deprived millions of potential job opportunities and tens of millions of potential opportunities for faster pay raises. Frequently, those worried about overheating cite current estimates from the Congressional Budget Office (CBO) of the "output gap"--the gap between income generated in today's economy and what could be generated (or potential output) if there was no downward pressure on spending by households, businesses, and governments (aggregate demand). These current CBO estimates look relatively small compared to the Biden rescue plan's fiscal support. But, these current estimates are almost certainly too-small. To provide just one piece of evidence--these estimates suggest that the economy was running above potential output in 2019 before Covid-19 struck. But there was no evidence of overheating that year--price inflation was tame and wage growth actually decelerated.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions. If this happens, and if the unemployment rate falls far beneath what it was in the pre-Covid period and stays below this for a few years, this will be an affirmatively good thing, not something to fear.

To be really clear about this--the unemployment can fall quite a ways beneath estimates of the so-called "natural rate" (or, the lowest rate of unemployment thought to be consistent with stable inflation in the long-run) for extended periods of time without disaster striking--look at the years before 1979 on this chart--we spent lots of time beneath the natural rate and had substantially faster growth (and more equal growth) than we've had since.

In decades past, it was taken as near-gospel among macroeconomic policymakers that their main concern should be keeping inflationary pressures in check. After an episode of high inflation in the 1970s, some of these policymakers adopted an implicit strategy of "opportunistic disinflation." The idea was not to affirmatively engineer recessions per se, but, following each recession the subsequent recovery in the unemployment rate was cut a bit short before it reached its previous low, hence putting consistent downward pressure on inflation (including wage inflation). This decades-long period of keeping labor markets softer than they needed to be to keep inflation stable (and instead targeting downward pressure on inflation) had huge costs. These soft labor markets were as important as any other factor in explaining the anemic wage growth faced by typical workers in those years and in the rise of wage inequality.

The Biden plan is essentially the reverse of opportunistic disinflation--it's opportunistic go-for-growth. Yes, there are several factors arguing that the economy could be well-poised to return unemployment to non-crisis levels relatively soon even without quite as big a plan. But, so what? Why not do even better than that? As many have pointed out, the risks of going too-big are trivial--a period of inflation that the Federal Reserve is well-equipped to neutralize. The risks of going too-small are large--letting the unemployment shock from Covid-19 linger for years.

The second worry expressed by Summers is a pure political calculation--that the Biden administration has a fixed lump-of-political-capital and spending too much on pure relief and recovery measures (when a smaller package will do) leaves too little available for pressing long-run issues yet to be addressed (think climate measures, green investment, care investments, etc.). He's clearly right that it would be a terrible thing if political miscalculations early in Biden's term led to less movement on these important issues. But, it also seems like a key way to build public confidence in the federal government's ability to do big things skillfully is to quickly smother the virus and engineer a rapid return to low unemployment.

Finally, I'll just note that when criticizing the Biden rescue plan, critics really do need to decide whether or not the $1,400 checks included in it are a problem because they make the plan "too big" and likely to cause overheating, or are a problem because they will "just be saved." If the checks are saved, then the economy will not overheat.

Economist Larry Summers raised fears today that the Biden administration's economic rescue plan might go too far, leading to economic overheating or squandering political and economic space for long-run reforms down the road. Neither of these fears are very compelling.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions.

On the first-the danger of economic overheating-there's not much more to add to what I and several others have already said on this: The U.S. economy has run far too-cool for decades, and this has stunted growth and deprived millions of potential job opportunities and tens of millions of potential opportunities for faster pay raises. Frequently, those worried about overheating cite current estimates from the Congressional Budget Office (CBO) of the "output gap"--the gap between income generated in today's economy and what could be generated (or potential output) if there was no downward pressure on spending by households, businesses, and governments (aggregate demand). These current CBO estimates look relatively small compared to the Biden rescue plan's fiscal support. But, these current estimates are almost certainly too-small. To provide just one piece of evidence--these estimates suggest that the economy was running above potential output in 2019 before Covid-19 struck. But there was no evidence of overheating that year--price inflation was tame and wage growth actually decelerated.

If the vaccines take hold and there is a significant relaxation of social distancing measures in the coming year, the economic relief we've provided so far through this crisis and the Biden plan could combine to see the economy spring to life and generate a recovery far faster than what we've seen in the past few recessions. If this happens, and if the unemployment rate falls far beneath what it was in the pre-Covid period and stays below this for a few years, this will be an affirmatively good thing, not something to fear.

To be really clear about this--the unemployment can fall quite a ways beneath estimates of the so-called "natural rate" (or, the lowest rate of unemployment thought to be consistent with stable inflation in the long-run) for extended periods of time without disaster striking--look at the years before 1979 on this chart--we spent lots of time beneath the natural rate and had substantially faster growth (and more equal growth) than we've had since.

In decades past, it was taken as near-gospel among macroeconomic policymakers that their main concern should be keeping inflationary pressures in check. After an episode of high inflation in the 1970s, some of these policymakers adopted an implicit strategy of "opportunistic disinflation." The idea was not to affirmatively engineer recessions per se, but, following each recession the subsequent recovery in the unemployment rate was cut a bit short before it reached its previous low, hence putting consistent downward pressure on inflation (including wage inflation). This decades-long period of keeping labor markets softer than they needed to be to keep inflation stable (and instead targeting downward pressure on inflation) had huge costs. These soft labor markets were as important as any other factor in explaining the anemic wage growth faced by typical workers in those years and in the rise of wage inequality.

The Biden plan is essentially the reverse of opportunistic disinflation--it's opportunistic go-for-growth. Yes, there are several factors arguing that the economy could be well-poised to return unemployment to non-crisis levels relatively soon even without quite as big a plan. But, so what? Why not do even better than that? As many have pointed out, the risks of going too-big are trivial--a period of inflation that the Federal Reserve is well-equipped to neutralize. The risks of going too-small are large--letting the unemployment shock from Covid-19 linger for years.

The second worry expressed by Summers is a pure political calculation--that the Biden administration has a fixed lump-of-political-capital and spending too much on pure relief and recovery measures (when a smaller package will do) leaves too little available for pressing long-run issues yet to be addressed (think climate measures, green investment, care investments, etc.). He's clearly right that it would be a terrible thing if political miscalculations early in Biden's term led to less movement on these important issues. But, it also seems like a key way to build public confidence in the federal government's ability to do big things skillfully is to quickly smother the virus and engineer a rapid return to low unemployment.

Finally, I'll just note that when criticizing the Biden rescue plan, critics really do need to decide whether or not the $1,400 checks included in it are a problem because they make the plan "too big" and likely to cause overheating, or are a problem because they will "just be saved." If the checks are saved, then the economy will not overheat.