SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

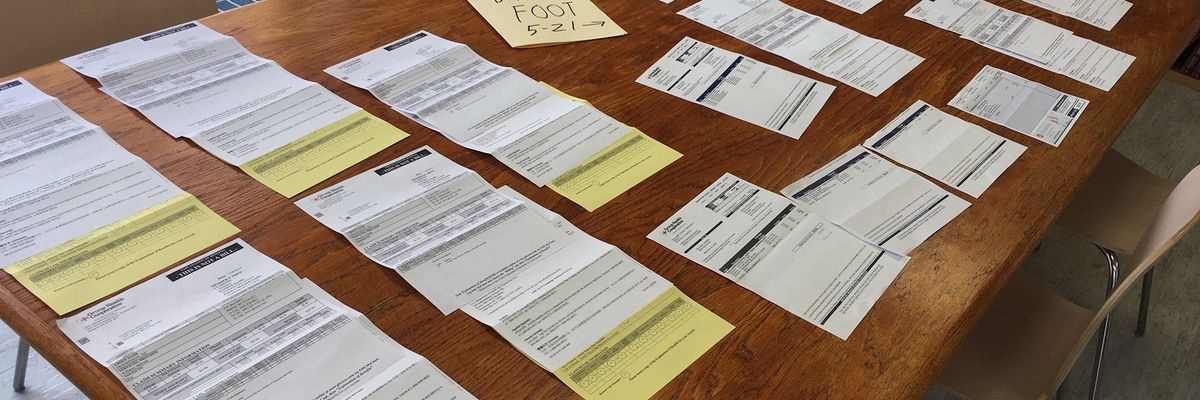

Don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't. (Photo: The Progressive)

The other day, the health maintenance organization of which I am a "member" sent me five separate envelopes each containing three sheets of paper. These purported to be "An Explanation of Benefits," with huge letters at the top proclaiming, "THIS IS NOT A BILL."

All five of these mailings were from two visits to the same department in the same clinic on the same day, July 10; only the top page differed. One said I would be charged $29.90 for "Diagnostic Labor"; a second listed a charge of $34.45 for "Diagnostic Labor"; a third said I would soon be asked to pay $57.85 for "Diagnostic Labor"; a fourth listed costs of $43.55 and $78 for "Diagnostic Labor"; and a fifth delivered the news that I would owe $113.10 for "Diagnostic Radio," whatever that is. (For that sum, I could get Sirius XM radio's "Mostly Music" option for an entire year.)

The total, which none of these forms provided, was $356.85. The two visits, minutes apart, were for some diagnostic tests related to my Type 2 diabetes and an x-ray of my right foot, which I managed to break while hiking on vacation. I knew it the moment it happened, but initially tried to ignore it, in part because I knew my health insurance would cover next to nothing. But when the pain didn't go away, I went in for a visit, nine days after the break.

I was charged $371 for that initial visit, on May 30, which also included a test to determine the cause of an unrelated rash. The physician's assistant I saw referred me to a foot and ankle specialist at UW Health, a separate provider, for two visits and one set of X-rays, at a cost of more than $500. Oh, and there was a $50 copay for each visit.

The reason all of these costs are my responsibility and not my insurer's is that my insurance plan has a $3,000 deductible. For this coverage my employer, The Progressive, pays $879.24 a month, or $10,550.88 a year. My dental insurance is a separate expense.

I've been thinking about this as I watch the moderate Democrats who would be President stoke public fears about how some of the more ambitious plans for reforming the nation's health care system would mean, as former Vice President Joe Biden darkly put it during the July 31 candidate debate, "You will lose your employer-based insurance."

Colorado Senator Michael Bennet made this sound more foreboding: The plan backed by Senators Bernie Sanders, Elizabeth Warren, and Kamala Harris, he warned, would make employer-based health coverage in this country "illegal."

Apparently, some Democratic contenders--all of whom likely have vastly superior health coverage than the average voter--believe that a broad swath of the American public JUST LOVES employer-provided health care and the dizzying array of deductibles, co-pays, exclusions, humiliations, and rationing of care that comes with it.

But, personally, I don't know anyone who feels that way. Most people I know hate their employee-based coverage, and for good reason.

Take Group Health Cooperative, which in my household is known as Group Health Uncooperative. While GHC has no qualms about brazenly indulging in bureaucratic waste--for instance, by sending five separate letters for various services performed by the same clinic on the same day--in other respects it seems quite intently focused on the bottom line.

For instance, GHC will bill you for a separate visit if you use your free annual physical to raise a specific health issue requiring separate attention--like if I have waited until my next physical to bring up my broken foot. As GHC explains on its website, an annual physical and an office visit are two completely different things that can, on occasion, both happen during the same appointment. "If this is the case," the site says, "your provider will submit a charge for both a preventive physical and an office visit."

The HMO feels it isn't fair for people to use their free annual physical to take care of things they could be paying for. How fair is it that members don't have even a single day each year where they can bring up a health problem without being charged?

The good news is that Group Health Cooperative members can feel out their providers as to whether raising a health issue during an annual physical that may entail a separate charge. If money is tight, it may be that the last person you'd want to tell about a nagging health issue is your doctor.

I don't want to single out Group Health Cooperative as an especially bad provider; they may very well be better than most. But my experience as a customer--er, member--is that the quality of coverage leaves much to be desired. I think many other people who get their health coverage through an employer feel the same way.

The discussion among Democrats over exactly how to reform health care is legitimate, just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

My life coverage has always come through employers--first my dad's, then places I have worked. With the possible exception of 1986, the year my son was born, I am reasonably certain that my insurer has never paid out as much in benefits in any given year as it has charged in premiums. My lifelong record of generally good health has been an unmitigated boon for them. Kind of makes me want to get cancer.

Everyone whose life intersects with the U.S. health-care industry knows that much of the "care" provided isn't care at all but machinations related to billing. It's shitty coverage that just keeps getting shittier. I have liked most of my doctors but would love to see the organizations they work for be put out of business. Maybe they would, too.

In fact, a recent poll found that 55 percent of voters back a Medicare-for-All system that would diminish the role of private insurers if they are able to retain access to their preferred providers. And at least one-third of insured Americans report difficulty affording premiums, deductibles, and drugs.

Yet politicians including Joe Biden still think they can gin up mass fear over the prospect of leaving behind predatory insurers in favor of a system that costs less and works better. At the July 31 debate, New York City Mayor Bill de Blasio pushed back.

"The folks I talk to about health insurance say that their health insurance isn't working for them," de Blasio said. "There's tens of millions of Americans who don't even have health insurance, tens of millions more who have health insurance they can barely make work because of the co-pays, the deductibles, the premiums, the out-of-pocket expenses."

Harris also put in a bad word for the health care status quo, saying, "I have met so many Americans who stick to a job that they do not like, where they are not prospering simply because they need the health care that that employer provides. It's time that we separate employers from the kind of health care people get."

The disagreement among Democrats over exactly how to reform health care is legitimate. It's worth weighing whether a complete and immediate changeover is as feasible as a plan that would allow people to try out a public option and see how they like it. I personally favor a complete and immediate changeover, at least as an aspirational starting point, but there is nothing wrong with having this discussion.

Just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

More good news: My broken foot healed. The treatment consisted of wearing good boots.

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

The other day, the health maintenance organization of which I am a "member" sent me five separate envelopes each containing three sheets of paper. These purported to be "An Explanation of Benefits," with huge letters at the top proclaiming, "THIS IS NOT A BILL."

All five of these mailings were from two visits to the same department in the same clinic on the same day, July 10; only the top page differed. One said I would be charged $29.90 for "Diagnostic Labor"; a second listed a charge of $34.45 for "Diagnostic Labor"; a third said I would soon be asked to pay $57.85 for "Diagnostic Labor"; a fourth listed costs of $43.55 and $78 for "Diagnostic Labor"; and a fifth delivered the news that I would owe $113.10 for "Diagnostic Radio," whatever that is. (For that sum, I could get Sirius XM radio's "Mostly Music" option for an entire year.)

The total, which none of these forms provided, was $356.85. The two visits, minutes apart, were for some diagnostic tests related to my Type 2 diabetes and an x-ray of my right foot, which I managed to break while hiking on vacation. I knew it the moment it happened, but initially tried to ignore it, in part because I knew my health insurance would cover next to nothing. But when the pain didn't go away, I went in for a visit, nine days after the break.

I was charged $371 for that initial visit, on May 30, which also included a test to determine the cause of an unrelated rash. The physician's assistant I saw referred me to a foot and ankle specialist at UW Health, a separate provider, for two visits and one set of X-rays, at a cost of more than $500. Oh, and there was a $50 copay for each visit.

The reason all of these costs are my responsibility and not my insurer's is that my insurance plan has a $3,000 deductible. For this coverage my employer, The Progressive, pays $879.24 a month, or $10,550.88 a year. My dental insurance is a separate expense.

I've been thinking about this as I watch the moderate Democrats who would be President stoke public fears about how some of the more ambitious plans for reforming the nation's health care system would mean, as former Vice President Joe Biden darkly put it during the July 31 candidate debate, "You will lose your employer-based insurance."

Colorado Senator Michael Bennet made this sound more foreboding: The plan backed by Senators Bernie Sanders, Elizabeth Warren, and Kamala Harris, he warned, would make employer-based health coverage in this country "illegal."

Apparently, some Democratic contenders--all of whom likely have vastly superior health coverage than the average voter--believe that a broad swath of the American public JUST LOVES employer-provided health care and the dizzying array of deductibles, co-pays, exclusions, humiliations, and rationing of care that comes with it.

But, personally, I don't know anyone who feels that way. Most people I know hate their employee-based coverage, and for good reason.

Take Group Health Cooperative, which in my household is known as Group Health Uncooperative. While GHC has no qualms about brazenly indulging in bureaucratic waste--for instance, by sending five separate letters for various services performed by the same clinic on the same day--in other respects it seems quite intently focused on the bottom line.

For instance, GHC will bill you for a separate visit if you use your free annual physical to raise a specific health issue requiring separate attention--like if I have waited until my next physical to bring up my broken foot. As GHC explains on its website, an annual physical and an office visit are two completely different things that can, on occasion, both happen during the same appointment. "If this is the case," the site says, "your provider will submit a charge for both a preventive physical and an office visit."

The HMO feels it isn't fair for people to use their free annual physical to take care of things they could be paying for. How fair is it that members don't have even a single day each year where they can bring up a health problem without being charged?

The good news is that Group Health Cooperative members can feel out their providers as to whether raising a health issue during an annual physical that may entail a separate charge. If money is tight, it may be that the last person you'd want to tell about a nagging health issue is your doctor.

I don't want to single out Group Health Cooperative as an especially bad provider; they may very well be better than most. But my experience as a customer--er, member--is that the quality of coverage leaves much to be desired. I think many other people who get their health coverage through an employer feel the same way.

The discussion among Democrats over exactly how to reform health care is legitimate, just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

My life coverage has always come through employers--first my dad's, then places I have worked. With the possible exception of 1986, the year my son was born, I am reasonably certain that my insurer has never paid out as much in benefits in any given year as it has charged in premiums. My lifelong record of generally good health has been an unmitigated boon for them. Kind of makes me want to get cancer.

Everyone whose life intersects with the U.S. health-care industry knows that much of the "care" provided isn't care at all but machinations related to billing. It's shitty coverage that just keeps getting shittier. I have liked most of my doctors but would love to see the organizations they work for be put out of business. Maybe they would, too.

In fact, a recent poll found that 55 percent of voters back a Medicare-for-All system that would diminish the role of private insurers if they are able to retain access to their preferred providers. And at least one-third of insured Americans report difficulty affording premiums, deductibles, and drugs.

Yet politicians including Joe Biden still think they can gin up mass fear over the prospect of leaving behind predatory insurers in favor of a system that costs less and works better. At the July 31 debate, New York City Mayor Bill de Blasio pushed back.

"The folks I talk to about health insurance say that their health insurance isn't working for them," de Blasio said. "There's tens of millions of Americans who don't even have health insurance, tens of millions more who have health insurance they can barely make work because of the co-pays, the deductibles, the premiums, the out-of-pocket expenses."

Harris also put in a bad word for the health care status quo, saying, "I have met so many Americans who stick to a job that they do not like, where they are not prospering simply because they need the health care that that employer provides. It's time that we separate employers from the kind of health care people get."

The disagreement among Democrats over exactly how to reform health care is legitimate. It's worth weighing whether a complete and immediate changeover is as feasible as a plan that would allow people to try out a public option and see how they like it. I personally favor a complete and immediate changeover, at least as an aspirational starting point, but there is nothing wrong with having this discussion.

Just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

More good news: My broken foot healed. The treatment consisted of wearing good boots.

The other day, the health maintenance organization of which I am a "member" sent me five separate envelopes each containing three sheets of paper. These purported to be "An Explanation of Benefits," with huge letters at the top proclaiming, "THIS IS NOT A BILL."

All five of these mailings were from two visits to the same department in the same clinic on the same day, July 10; only the top page differed. One said I would be charged $29.90 for "Diagnostic Labor"; a second listed a charge of $34.45 for "Diagnostic Labor"; a third said I would soon be asked to pay $57.85 for "Diagnostic Labor"; a fourth listed costs of $43.55 and $78 for "Diagnostic Labor"; and a fifth delivered the news that I would owe $113.10 for "Diagnostic Radio," whatever that is. (For that sum, I could get Sirius XM radio's "Mostly Music" option for an entire year.)

The total, which none of these forms provided, was $356.85. The two visits, minutes apart, were for some diagnostic tests related to my Type 2 diabetes and an x-ray of my right foot, which I managed to break while hiking on vacation. I knew it the moment it happened, but initially tried to ignore it, in part because I knew my health insurance would cover next to nothing. But when the pain didn't go away, I went in for a visit, nine days after the break.

I was charged $371 for that initial visit, on May 30, which also included a test to determine the cause of an unrelated rash. The physician's assistant I saw referred me to a foot and ankle specialist at UW Health, a separate provider, for two visits and one set of X-rays, at a cost of more than $500. Oh, and there was a $50 copay for each visit.

The reason all of these costs are my responsibility and not my insurer's is that my insurance plan has a $3,000 deductible. For this coverage my employer, The Progressive, pays $879.24 a month, or $10,550.88 a year. My dental insurance is a separate expense.

I've been thinking about this as I watch the moderate Democrats who would be President stoke public fears about how some of the more ambitious plans for reforming the nation's health care system would mean, as former Vice President Joe Biden darkly put it during the July 31 candidate debate, "You will lose your employer-based insurance."

Colorado Senator Michael Bennet made this sound more foreboding: The plan backed by Senators Bernie Sanders, Elizabeth Warren, and Kamala Harris, he warned, would make employer-based health coverage in this country "illegal."

Apparently, some Democratic contenders--all of whom likely have vastly superior health coverage than the average voter--believe that a broad swath of the American public JUST LOVES employer-provided health care and the dizzying array of deductibles, co-pays, exclusions, humiliations, and rationing of care that comes with it.

But, personally, I don't know anyone who feels that way. Most people I know hate their employee-based coverage, and for good reason.

Take Group Health Cooperative, which in my household is known as Group Health Uncooperative. While GHC has no qualms about brazenly indulging in bureaucratic waste--for instance, by sending five separate letters for various services performed by the same clinic on the same day--in other respects it seems quite intently focused on the bottom line.

For instance, GHC will bill you for a separate visit if you use your free annual physical to raise a specific health issue requiring separate attention--like if I have waited until my next physical to bring up my broken foot. As GHC explains on its website, an annual physical and an office visit are two completely different things that can, on occasion, both happen during the same appointment. "If this is the case," the site says, "your provider will submit a charge for both a preventive physical and an office visit."

The HMO feels it isn't fair for people to use their free annual physical to take care of things they could be paying for. How fair is it that members don't have even a single day each year where they can bring up a health problem without being charged?

The good news is that Group Health Cooperative members can feel out their providers as to whether raising a health issue during an annual physical that may entail a separate charge. If money is tight, it may be that the last person you'd want to tell about a nagging health issue is your doctor.

I don't want to single out Group Health Cooperative as an especially bad provider; they may very well be better than most. But my experience as a customer--er, member--is that the quality of coverage leaves much to be desired. I think many other people who get their health coverage through an employer feel the same way.

The discussion among Democrats over exactly how to reform health care is legitimate, just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

My life coverage has always come through employers--first my dad's, then places I have worked. With the possible exception of 1986, the year my son was born, I am reasonably certain that my insurer has never paid out as much in benefits in any given year as it has charged in premiums. My lifelong record of generally good health has been an unmitigated boon for them. Kind of makes me want to get cancer.

Everyone whose life intersects with the U.S. health-care industry knows that much of the "care" provided isn't care at all but machinations related to billing. It's shitty coverage that just keeps getting shittier. I have liked most of my doctors but would love to see the organizations they work for be put out of business. Maybe they would, too.

In fact, a recent poll found that 55 percent of voters back a Medicare-for-All system that would diminish the role of private insurers if they are able to retain access to their preferred providers. And at least one-third of insured Americans report difficulty affording premiums, deductibles, and drugs.

Yet politicians including Joe Biden still think they can gin up mass fear over the prospect of leaving behind predatory insurers in favor of a system that costs less and works better. At the July 31 debate, New York City Mayor Bill de Blasio pushed back.

"The folks I talk to about health insurance say that their health insurance isn't working for them," de Blasio said. "There's tens of millions of Americans who don't even have health insurance, tens of millions more who have health insurance they can barely make work because of the co-pays, the deductibles, the premiums, the out-of-pocket expenses."

Harris also put in a bad word for the health care status quo, saying, "I have met so many Americans who stick to a job that they do not like, where they are not prospering simply because they need the health care that that employer provides. It's time that we separate employers from the kind of health care people get."

The disagreement among Democrats over exactly how to reform health care is legitimate. It's worth weighing whether a complete and immediate changeover is as feasible as a plan that would allow people to try out a public option and see how they like it. I personally favor a complete and immediate changeover, at least as an aspirational starting point, but there is nothing wrong with having this discussion.

Just don't pretend that most Americans have warm fuzzies for their employer-based health insurance plans. They don't.

More good news: My broken foot healed. The treatment consisted of wearing good boots.