SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

But now, as the United States’ war on Iran has set off a global energy crisis, humanity has arrived at a more immediate and critical Coyote moment. The International Monetary Fund (IMF) has issued a report suggesting that continued oil shortages could reduce global economic growth by 2% and raise inflation by 2.3%. Some analysts say the IMF warning is far too weak and that the crisis could trigger a global recession or worse.

Oil is a key ingredient in most consumer products and their packaging; expensive oil therefore translates to price hikes for toys, car parts, electronics, clothing, and more. It powers or is a critical input into essential elements of industrial society, including the food system. And oil moves everything: Global supply chains depend on transportation by truck, rail, ship, and air, and over 90% of transport energy is oil based. That means an extended crisis would likely lead to stagflation, in which the economy is hobbled simultaneously by inflation and slow growth or economic contraction. When prices for food and medicines are eventually impacted, no one will remain unaffected.

America’s status as oil-production king and its cushion of reserves have indeed helped it weather the early stages of the crisis. But the nation won’t be insulated from serious economic damage for long.

However, for the moment, the stock market is hardly signaling imminent economic peril; instead, the Dow Jones is near peak levels. Further, the US, which started the war, seems somewhat spared from its consequences, when compared with many other countries. And oil prices, while higher than before the hostilities, are nowhere near inflation-adjusted historic peaks.

What’s keeping Coyote airborne?

Myanmar, Bangladesh, Slovenia, Sri Lanka, Cambodia, and Vietnam are rationing or restricting the purchasing of fuel. Germany’s Lufthansa airline has cut 20,000 summer flights due to rising fuel costs. The examples could be multiplied: Countries in Asia, Europe, and Africa are already experiencing symptoms of energy scarcity, while Australia faces dire impacts to its agriculture.

But in America, the worst fallout so far is expensive gasoline. Before the first attacks on Tehran in late February, the average price of gas in the US was $2.98 a gallon. It’s now above $4—a political worry for the president and other Republicans, but a price that’s not quite as high as ones motorists faced in the 1970s. US airlines have raised their checked baggage fees in response to higher fuel costs. Yet, otherwise, business hums along more or less as usual. Why have Americans seen so few repercussions?

Two reasons are widely cited. The first is that the US is currently the world’s biggest oil producer and is therefore far less vulnerable to shortages than nations that import most, or all, of their fuel. The second is that the US has the world’s second-largest strategic petroleum reserve (after China), which, in an emergency, can be brought to market to lower prices and avert scarcity.

However, these two pillars of US energy resilience are shaky. First: Even though the United States produces over 13 million barrels of oil per day, it uses almost 20 million barrels. Further, the kinds of oil extracted from American wells are not always the kinds that the nation’s refineries are set up to use. So, oil companies export light crude and import heavier crude to produce the blends of gasoline, diesel, and jet fuel that the US market demands. The result: America is the world’s second-largest oil importer, even though its politicians love to brag about “energy independence.”

Second: Strategic petroleum reserves are only meant to last a relatively brief time. Currently, the US has about 400 million barrels of oil stored in four underground salt caverns along the Gulf of Mexico. That’s 20 days’ worth of total American consumption at current rates. Therefore, the government has limited ability to influence oil prices during a months-long supply crunch.

America’s status as oil-production king and its cushion of reserves have indeed helped it weather the early stages of the crisis. But the nation won’t be insulated from serious economic damage for long.

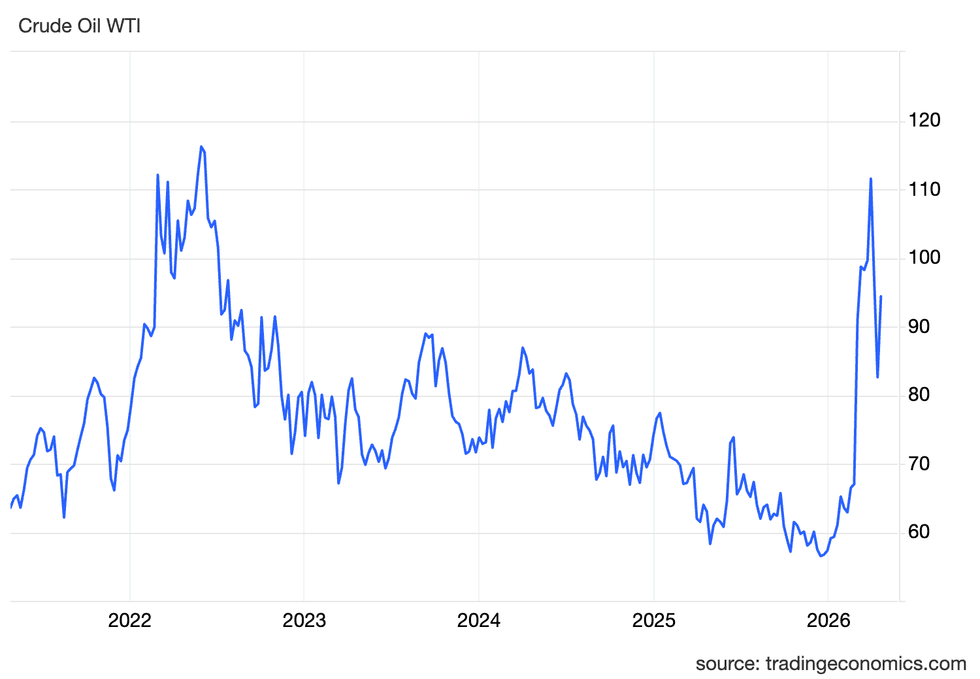

Oil has been trading at roughly $100 a barrel since the start of hostilities, a price somewhat lower than ones seen in June and July 2022 when Russia invaded Ukraine. The closure of the Strait of Hormuz would intuitively seem a much graver threat to world oil supplies. Given that a fifth of the world’s petroleum flow is now unavailable, why haven’t prices shot even higher?

WTI Crude Oil Prices are shown from 2021-2026. (Graphic via Trading Economics)

WTI Crude Oil Prices are shown from 2021-2026. (Graphic via Trading Economics)

One factor is the so-called TACO trade. US President Donald Trump has repeatedly shown the tendency to make threats and then back away; hence the meme “Trump Always Chickens Out” (TACO). The term “TACO trade” gained currency during 2025, when the president announced steep tariffs, then canceled or moderated them, ostensibly to leave time for negotiations but also perhaps in response to negative impacts those announcements had on stock prices (stock market activity appears to influence Donald Trump’s behavior more than most other factors). Savvy stock traders learned that if, instead of taking Trump’s most belligerent threats seriously, they bet against price dips, they could make more money.

We’re all dancing somewhere off the end of history’s biggest cliff, sensing that something isn’t quite right but blaming that sensation on people whose politics we disagree with.

The TACO trade has also followed Trump’s recent statements about the Iran War. When he said, in a late-night Truth Social post, that “a whole civilization will die tonight, never to be brought back again” if a deal to reopen the Strait of Hormuz was not immediately reached, many oil traders sat tight, assuming Trump would renege on his threat. He did. If Trump’s backdowns happen on a Tuesday, as on April 21, the internet explodes with “TACO Tuesday” comments.

However, the longer the crisis drags on, the harder real shortages will bite oil-importing economies worldwide. And there are reasons to expect the impasse between the US and Iran to continue. Trump’s instinct is to bully and bluster, but every time he attacks Iran or threatens to do so, oil prices rise (despite the muting effect of the TACO trade) and the stock market dips. Both trends are political kryptonite. However, it would be even worse politically for Trump if he were to accede to a long-term Iranian peace deal that looks like a defeat for America. So, the standoff persists, with the Strait of Hormuz blocked, 20% of world oil supplies offline, and the global economy held hostage.

The strait has been closed for over two months. Analysts say that if it remains shut to tanker traffic for months longer, oil prices could soar to $200, which would almost surely send the global economy into contraction.

An acute Wile E. Coyote moment is also happening in global stock markets. Many people (including most investors) tend to think of stock prices as a barometer of the overall soundness of the economy. Others disagree, pointing out that stock prices just measure future profit expectations of listed companies, not current employment or wages, much less the health of the biosphere. Further, stock ownership is highly concentrated, so market booms often benefit only the wealthy. Nevertheless, the opinions of the rich tend to be amplified throughout society, so even many non-investors watch the Dow Jones and S&P 500. And, despite the Iran war and resulting higher oil prices, and despite warnings from experts about rising fertilizer costs and the possibility of global food shortages, the Dow seems to be doing just fine. The major market indexes dipped significantly between late February and late March but have recovered since then and are once again near record highs.

The market’s resilience is puzzling for another reason as well. Most investment action during the past couple of years has centered on artificial intelligence (AI). Nvidia, which makes computer chips for AI, is now the world’s most valuable company by market capitalization, even though the AI industry is struggling to be profitable. Many analysts say that AI is a classic financial bubble—and a historically big one.

So, are investors stupid, or what? A more nuanced take might be that they exhibit herd mentality, and that they tend to chase short-term profits, hoping to sell shares just before prices plunge.

Here’s another factor. According to some analysts, the markets are simply high on cash. Governments created enormous amounts of money to stanch problems created by the Global Financial Crisis of 2008 and the Covid-19 epidemic, and much of that money eventually found its way to investors. When the US federal government racks up giant fiscal deficits, it is creating new money, much of which winds up inflating bubbles.

In short, the market runs on investor sentiment, which is now detached from both consumer sentiment and business prospects—as well as from long-term biophysical reality.

But sooner or later, reality imposes itself.

In the cartoon, it’s not until Coyote looks down that he realizes his predicament. This sudden awareness triggers his fall.

Of course, in the real world, temporary ignorance can’t cancel gravity. Actual coyotes don’t hover until they glance groundward. However, the human economy can do something like that—because it’s a hybrid of a real-world component comprised of energy and material flows (which ultimately depend on nature), and an imaginary-world component comprised of money, prices, hype, and speculation. This hybrid semi-reality can run up ecological deficits and undermine the conditions of life for future generations while still maintaining affluence and entertainment for hundreds of millions of mostly clueless people. For now.

It’s our bigger, longer-playing Coyote moments to which we should be paying most attention—climate change, resource depletion, chemical pollution, and the disappearance of wild nature. Markets and prices are of little help in shifting our awareness in that direction: Cutting down an old-growth forest for timber can result in corporate profits and a bump in GDP, but the human and environmental impacts that will linger for generations don’t figure into this quarter’s P&L reports. We’re all dancing somewhere off the end of history’s biggest cliff, sensing that something isn’t quite right but blaming that sensation on people whose politics we disagree with. We do anything we can to avoid looking down.

Returning to the main subject of this article: Will oil prices skyrocket? Will Trump continue to TACO? Will the economy crater? Or will the US and Iran reach a deal and open the strait, so that normalcy can resume? Your guess is as good as anyone’s. But if you’re starting to have nagging worries, you’re not crazy and you’re not alone. Do something. Plant a vegetable garden. Talk to your neighbors about sharing tools and skills. Examine your oil dependency and see how you can reduce it. Imagine how your life might look if the economy were smaller, not bigger, and start making adjustments. Most of all, focus on building community with those around you.

"The largest individual gainer Wednesday was Tesla Inc. CEO Elon Musk, who added $36 billion to his fortune as the EV manufacturer's stock jumped 23%, followed by Meta Platforms Inc.'s Mark Zuckerberg, who gained almost $26 billion," Bloomberg reported. "Nvidia Corp.'s Jensen Huang saw his wealth rise $15.5 billion as the chipmaker's shares rebounded 19%, nearly offsetting its 13% decline in the week to Tuesday's close."

Though the stock market gave up some of the massive gains on Thursday amid continued uncertainty about Trump's tariffs, the rapid billionaire wealth surge amplified concerns about possible market manipulation and insider trading ahead of the president's announcement of a 90-day pause. Trump publicly encouraged people to buy stock just hours before announcing the pause.

"Is there any doubt in anyone's mind they were tipped off?" The Tennessee Holler, a progressive news outlet, wrote on social media. "They are laughing at us all."

In the days leading up to the president's partial tariff pause, some of his billionaire supporters publicly criticized his approach as their wealth took a hit amid the trade war-induced market sell-off.

According to Bloomberg, the 500 richest people in the world saw their collective wealth fall by $208 billion the day after Trump announced the sweeping tariffs last week. The Wall Street Journal reported Thursday that Treasury Secretary Scott Bessent was "flooded with worried calls from Wall Street over the weekend and felt strongly he had to persuade Trump that a pause was needed."

The partial tariff pause came a day before the Republican-controlled House passed a budget blueprint that paves the way for another round of tax cuts that would primarily benefit the wealthiest Americans.

"These tariffs are not designed to solve an actual trade or economic challenge," Sen. Ron Wyden (D-Ore.), the top Democrat on the Senate Finance Committee, said Thursday. "They're designed to soak typical workers with higher taxes in order to help pay for handouts to the top."

"They're focused on yet more handouts to billionaires and corporations," Wyden added, "and everybody else is going to be on the hook to pay for them."