SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Winter is coming and with it a very likely economic contraction in 2023. Its roots lie beyond just the pandemic's effects on the economy. To be sure, Covid acted as a catalyst exposing much deeper structural deficiencies related to a highly unequal distribution of wealth along class lines, state capture by huge MNCs and financial interests, and the waning influence of organized labor over the last 40 or more years. The weaknesses in the globalization of supply chains and "just in time" production were on full display as soon as supply bottlenecks manifested during the shutdowns. Compounding this is the war in Ukraine that is making itself felt in both energy and food markets. Finally, climate change is disrupting global food markets in every country on earth in the form of droughts, hurricanes, and other extreme weather events.

If inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future.

The losers are a familiar lot: workers and the Global South. The tools through which the punishments are doled out should also be familiar to students of economic history. The dictums of "central bank independence" and of balanced budgets summarize well both the monetary and fiscal approaches acolytes of the Washington Consensus adhere to in times of economic crisis. But, as the most basic student of history can point out, these two policy precepts are responsible for more suffering than relief. The so-called "independence" of central banks is much more about its freedom from democratic rule than its neutrality between capital and labor. And just a cursory review of different international balance of payment crises reveals the true costs of balanced budgets.

When focusing on the current state of both the domestic and global economy, signs of a looming crisis abound. Layoffs are coming amidst business leaders' concerns over weak growth in the next year. Tech employees are being hit particularly hard: Musk immediately fired almost 4,000 employees as soon as he took over Twitter, Apple and Amazon have announced a halt in corporate hiring, and Lyft and Stripe are laying off close to 15% of their employees.

Morgan Stanley is also cutting jobs in their "global markets" department, not a very inspiring development, following Goldman Sachs' announcement of their "annual employee culls." Average monthly employment gains this year are 30% less than their 2021 levels. The hardest hit industry remains leisure and hospitality reflecting the impact of Covid-19 continuing to make itself felt through travel in particular.

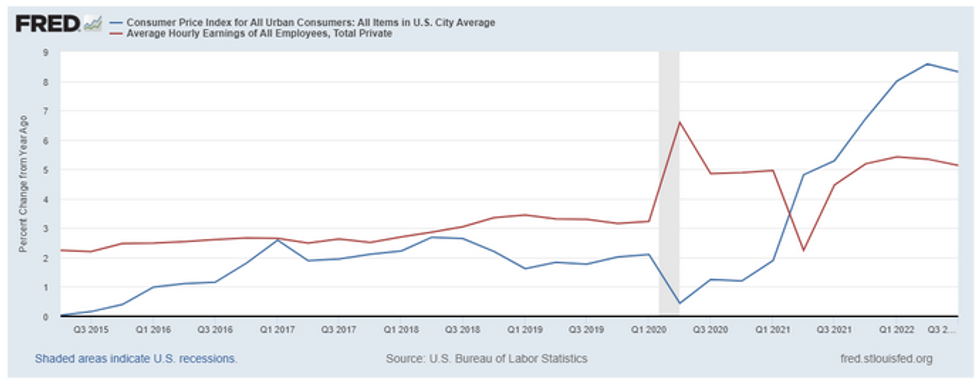

Inflation (measured by the CPI-U) increased by 8.3% in September from the year prior while wages only grew 4.7%, netting a real decrease in purchasing power of 3.6%. The idea that it is wage increases that are driving inflation is thoroughly dispelled when looking at the record corporate profits that have been posted over the last year. Labor costs are the usual culprit for rising corporate expenses historically speaking. However, since Covid over half of the increase in prices can be attributed to markups over the cost of production, and only 8% to unit labor costs.

Average Hourly Earnings vs CPI-U: % Change from Year Ago, 2015-Present

The gap represents the difference between rising costs and rising compensation. Clearly, workers are losing.

This is in the context of a Federal minimum wage that is 27% less in real terms than just 13 years ago, when it was last increased, and 40% less than it was in 1968, when it peaked in inflation-adjusted terms. On the other hand, since Trump took office in January 2017, the "middle-class", or those that are in the 40th-90th percentiles in terms of income, averaged an increase of $120,000. Meanwhile, over the last year alone, the top 1% (average income $1.7 million) saw their wealth grow by 11.5%, or $170k. And considering over the long term, since January of 1976 the top one percent's wealth grew by 283.4%, while the bottom half's wealth grew by a meager 29.9%, or $4.6 thousand. One does not need to have a degree in economics to see the yawning gap that has been growing wider every decade since the early 1970s.

Most workers are also vulnerable debtors. The Fed's sixth rate hike, this time by 75bsp, will be felt by working people and manifest in more income being siphoned off to pay financial obligations and less going into the real economy. If the Fed expects prices to cool, the mechanism is familiar: punishing workers and new and potential homeowners and making it harder for businesses to borrow to expand or roll over existing debt.

Rising rates tend to depress retirement portfolios generally, as stocks lose value in the face of future uncertainty and older bonds depreciate in value in order to compete with newly issued higher-yield bonds. This hits the working people at precisely the time they need financial relief. Families hoping to become homeowners are seeing their dreams put on hold for the foreseeable future. Again, if inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future. With the FOMC being explicitly committed to raising rates no matter the consequences, and the weak position of workers vis-a-vis their employers, economic relief for the working class doesn't seem like it's going to come from above. Workers need to pressure their bosses and policymakers especially to act on behalf of their interests.

Finally, given the enormous importance of the US economy and the dollar to the rest of the world, those countries that borrowed in dollars are also going to suffer from rate increases. An appreciating dollar also makes it harder to pay off existing debt. Most foreign-denominated debt is in US dollars, making the Fed the de facto central bank of the world, in much the same way as the Bank of England (BoE) once acted before the First World War. Across the global south Fed rate hikes are already shaking out as incipient sovereign debt crises in countries such as Ethiopia, Zambia, and El Salvador, to name only three.

The Fed's moves will inexorably provoke other central banks to follow suit. The BoE enacted its largest rate increase in 30 years making interest rates the highest they've been since 2008. Bank officials declared that they believe forthcoming data will show the UK economy already in a recession over the last three months. And the UK government is acting like it: announcing it is cutting 200,000 jobs in the coming years to reduce government debt.

The political volatility that is the backdrop to all of this demonstrates the costs of investor uncertainty. Don't rile the hand that feeds, so they say. Unfortunately, this hand is selective about where it extends itself.

Winter is coming and with it a very likely economic contraction in 2023. Its roots lie beyond just the pandemic's effects on the economy. To be sure, Covid acted as a catalyst exposing much deeper structural deficiencies related to a highly unequal distribution of wealth along class lines, state capture by huge MNCs and financial interests, and the waning influence of organized labor over the last 40 or more years. The weaknesses in the globalization of supply chains and "just in time" production were on full display as soon as supply bottlenecks manifested during the shutdowns. Compounding this is the war in Ukraine that is making itself felt in both energy and food markets. Finally, climate change is disrupting global food markets in every country on earth in the form of droughts, hurricanes, and other extreme weather events.

If inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future.

The losers are a familiar lot: workers and the Global South. The tools through which the punishments are doled out should also be familiar to students of economic history. The dictums of "central bank independence" and of balanced budgets summarize well both the monetary and fiscal approaches acolytes of the Washington Consensus adhere to in times of economic crisis. But, as the most basic student of history can point out, these two policy precepts are responsible for more suffering than relief. The so-called "independence" of central banks is much more about its freedom from democratic rule than its neutrality between capital and labor. And just a cursory review of different international balance of payment crises reveals the true costs of balanced budgets.

When focusing on the current state of both the domestic and global economy, signs of a looming crisis abound. Layoffs are coming amidst business leaders' concerns over weak growth in the next year. Tech employees are being hit particularly hard: Musk immediately fired almost 4,000 employees as soon as he took over Twitter, Apple and Amazon have announced a halt in corporate hiring, and Lyft and Stripe are laying off close to 15% of their employees.

Morgan Stanley is also cutting jobs in their "global markets" department, not a very inspiring development, following Goldman Sachs' announcement of their "annual employee culls." Average monthly employment gains this year are 30% less than their 2021 levels. The hardest hit industry remains leisure and hospitality reflecting the impact of Covid-19 continuing to make itself felt through travel in particular.

Inflation (measured by the CPI-U) increased by 8.3% in September from the year prior while wages only grew 4.7%, netting a real decrease in purchasing power of 3.6%. The idea that it is wage increases that are driving inflation is thoroughly dispelled when looking at the record corporate profits that have been posted over the last year. Labor costs are the usual culprit for rising corporate expenses historically speaking. However, since Covid over half of the increase in prices can be attributed to markups over the cost of production, and only 8% to unit labor costs.

Average Hourly Earnings vs CPI-U: % Change from Year Ago, 2015-Present

The gap represents the difference between rising costs and rising compensation. Clearly, workers are losing.

This is in the context of a Federal minimum wage that is 27% less in real terms than just 13 years ago, when it was last increased, and 40% less than it was in 1968, when it peaked in inflation-adjusted terms. On the other hand, since Trump took office in January 2017, the "middle-class", or those that are in the 40th-90th percentiles in terms of income, averaged an increase of $120,000. Meanwhile, over the last year alone, the top 1% (average income $1.7 million) saw their wealth grow by 11.5%, or $170k. And considering over the long term, since January of 1976 the top one percent's wealth grew by 283.4%, while the bottom half's wealth grew by a meager 29.9%, or $4.6 thousand. One does not need to have a degree in economics to see the yawning gap that has been growing wider every decade since the early 1970s.

Most workers are also vulnerable debtors. The Fed's sixth rate hike, this time by 75bsp, will be felt by working people and manifest in more income being siphoned off to pay financial obligations and less going into the real economy. If the Fed expects prices to cool, the mechanism is familiar: punishing workers and new and potential homeowners and making it harder for businesses to borrow to expand or roll over existing debt.

Rising rates tend to depress retirement portfolios generally, as stocks lose value in the face of future uncertainty and older bonds depreciate in value in order to compete with newly issued higher-yield bonds. This hits the working people at precisely the time they need financial relief. Families hoping to become homeowners are seeing their dreams put on hold for the foreseeable future. Again, if inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future. With the FOMC being explicitly committed to raising rates no matter the consequences, and the weak position of workers vis-a-vis their employers, economic relief for the working class doesn't seem like it's going to come from above. Workers need to pressure their bosses and policymakers especially to act on behalf of their interests.

Finally, given the enormous importance of the US economy and the dollar to the rest of the world, those countries that borrowed in dollars are also going to suffer from rate increases. An appreciating dollar also makes it harder to pay off existing debt. Most foreign-denominated debt is in US dollars, making the Fed the de facto central bank of the world, in much the same way as the Bank of England (BoE) once acted before the First World War. Across the global south Fed rate hikes are already shaking out as incipient sovereign debt crises in countries such as Ethiopia, Zambia, and El Salvador, to name only three.

The Fed's moves will inexorably provoke other central banks to follow suit. The BoE enacted its largest rate increase in 30 years making interest rates the highest they've been since 2008. Bank officials declared that they believe forthcoming data will show the UK economy already in a recession over the last three months. And the UK government is acting like it: announcing it is cutting 200,000 jobs in the coming years to reduce government debt.

The political volatility that is the backdrop to all of this demonstrates the costs of investor uncertainty. Don't rile the hand that feeds, so they say. Unfortunately, this hand is selective about where it extends itself.

Winter is coming and with it a very likely economic contraction in 2023. Its roots lie beyond just the pandemic's effects on the economy. To be sure, Covid acted as a catalyst exposing much deeper structural deficiencies related to a highly unequal distribution of wealth along class lines, state capture by huge MNCs and financial interests, and the waning influence of organized labor over the last 40 or more years. The weaknesses in the globalization of supply chains and "just in time" production were on full display as soon as supply bottlenecks manifested during the shutdowns. Compounding this is the war in Ukraine that is making itself felt in both energy and food markets. Finally, climate change is disrupting global food markets in every country on earth in the form of droughts, hurricanes, and other extreme weather events.

If inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future.

The losers are a familiar lot: workers and the Global South. The tools through which the punishments are doled out should also be familiar to students of economic history. The dictums of "central bank independence" and of balanced budgets summarize well both the monetary and fiscal approaches acolytes of the Washington Consensus adhere to in times of economic crisis. But, as the most basic student of history can point out, these two policy precepts are responsible for more suffering than relief. The so-called "independence" of central banks is much more about its freedom from democratic rule than its neutrality between capital and labor. And just a cursory review of different international balance of payment crises reveals the true costs of balanced budgets.

When focusing on the current state of both the domestic and global economy, signs of a looming crisis abound. Layoffs are coming amidst business leaders' concerns over weak growth in the next year. Tech employees are being hit particularly hard: Musk immediately fired almost 4,000 employees as soon as he took over Twitter, Apple and Amazon have announced a halt in corporate hiring, and Lyft and Stripe are laying off close to 15% of their employees.

Morgan Stanley is also cutting jobs in their "global markets" department, not a very inspiring development, following Goldman Sachs' announcement of their "annual employee culls." Average monthly employment gains this year are 30% less than their 2021 levels. The hardest hit industry remains leisure and hospitality reflecting the impact of Covid-19 continuing to make itself felt through travel in particular.

Inflation (measured by the CPI-U) increased by 8.3% in September from the year prior while wages only grew 4.7%, netting a real decrease in purchasing power of 3.6%. The idea that it is wage increases that are driving inflation is thoroughly dispelled when looking at the record corporate profits that have been posted over the last year. Labor costs are the usual culprit for rising corporate expenses historically speaking. However, since Covid over half of the increase in prices can be attributed to markups over the cost of production, and only 8% to unit labor costs.

Average Hourly Earnings vs CPI-U: % Change from Year Ago, 2015-Present

The gap represents the difference between rising costs and rising compensation. Clearly, workers are losing.

This is in the context of a Federal minimum wage that is 27% less in real terms than just 13 years ago, when it was last increased, and 40% less than it was in 1968, when it peaked in inflation-adjusted terms. On the other hand, since Trump took office in January 2017, the "middle-class", or those that are in the 40th-90th percentiles in terms of income, averaged an increase of $120,000. Meanwhile, over the last year alone, the top 1% (average income $1.7 million) saw their wealth grow by 11.5%, or $170k. And considering over the long term, since January of 1976 the top one percent's wealth grew by 283.4%, while the bottom half's wealth grew by a meager 29.9%, or $4.6 thousand. One does not need to have a degree in economics to see the yawning gap that has been growing wider every decade since the early 1970s.

Most workers are also vulnerable debtors. The Fed's sixth rate hike, this time by 75bsp, will be felt by working people and manifest in more income being siphoned off to pay financial obligations and less going into the real economy. If the Fed expects prices to cool, the mechanism is familiar: punishing workers and new and potential homeowners and making it harder for businesses to borrow to expand or roll over existing debt.

Rising rates tend to depress retirement portfolios generally, as stocks lose value in the face of future uncertainty and older bonds depreciate in value in order to compete with newly issued higher-yield bonds. This hits the working people at precisely the time they need financial relief. Families hoping to become homeowners are seeing their dreams put on hold for the foreseeable future. Again, if inflation is tamed in this manner, it will be at the expense of workers' paychecks today, and their wealth and prosperity in the future. With the FOMC being explicitly committed to raising rates no matter the consequences, and the weak position of workers vis-a-vis their employers, economic relief for the working class doesn't seem like it's going to come from above. Workers need to pressure their bosses and policymakers especially to act on behalf of their interests.

Finally, given the enormous importance of the US economy and the dollar to the rest of the world, those countries that borrowed in dollars are also going to suffer from rate increases. An appreciating dollar also makes it harder to pay off existing debt. Most foreign-denominated debt is in US dollars, making the Fed the de facto central bank of the world, in much the same way as the Bank of England (BoE) once acted before the First World War. Across the global south Fed rate hikes are already shaking out as incipient sovereign debt crises in countries such as Ethiopia, Zambia, and El Salvador, to name only three.

The Fed's moves will inexorably provoke other central banks to follow suit. The BoE enacted its largest rate increase in 30 years making interest rates the highest they've been since 2008. Bank officials declared that they believe forthcoming data will show the UK economy already in a recession over the last three months. And the UK government is acting like it: announcing it is cutting 200,000 jobs in the coming years to reduce government debt.

The political volatility that is the backdrop to all of this demonstrates the costs of investor uncertainty. Don't rile the hand that feeds, so they say. Unfortunately, this hand is selective about where it extends itself.