SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

As Russia continues to inflict untold suffering and devastation in Ukraine, many around the world are profiting amid the horrific bloodshed.

Depressingly, given the spiraling climate crisis, fossil fuel firms - and their investors - are the biggest winners of the war, reaping the benefits of surging energy prices and new governmental measures to expand oil production.

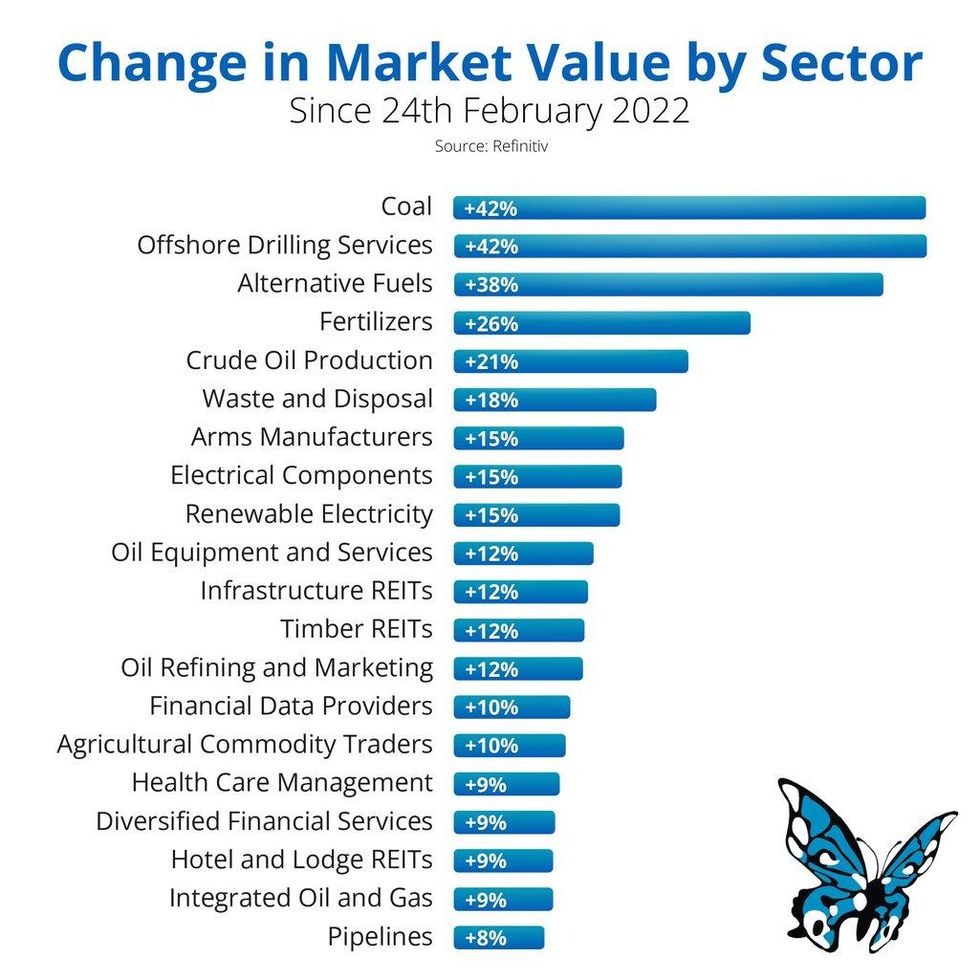

Coal companies and offshore drilling services have done the best out of the geopolitical crisis, both registering an astonishing 42% increase in their market value.

But who else is cashing in on the emerging war economy? To determine this, we must look closer at the market capitalization data, which reveals investors' expectations about different firms' earnings capacities.

The more the market value of a firm rises, the higher it ascends in the overall corporate hierarchy. With this in mind, the graph below shows the 20 corporate sectors that have enjoyed the largest increase in company market value - outperforming 153 others - since the Russian invasion began on 24 February.

Aside from those involved in the extraction, processing, and distribution of fossil fuels - which, remarkably, directly relate to seven of the 20 highest performing sectors - arms manufacturers are, predictably, the other major beneficiaries.

Such firms have seen a 15% increase in their market value due to the heightened demand for military hardware and the commitment by NATO governments to expand military spending.

Agricultural commodity traders have also seen 10% growth in market capitalization in the past two months, profiting hugely from the market instability and rising commodity prices brought about by the conflict.

This has led critics to argue that, in many ways, these traders actually promote the disruption in food systems that they then benefit from.

The situation is decidedly gloomy. Amid continuing war in Ukraine, escalating tensions between Russia and the West, a cost-of-living crisis in Europe and the wider world, and ongoing global warming, investors are backing those firms that directly benefit from geopolitical conflict, commodity market instability, and our continued dependency on fossil fuels.

There are, however, some glimmers of hope. Alternative fuels companies - which operate in areas ranging from the installation of charging points for electric vehicles to the production of bioenergy and the manufacture of hydrogen fuel cells - have seen their market value grow by 38%.

Companies engaged in generating electricity from renewable sources, such as wind and solar power, have also enjoyed a 15% rise.

This indicates that investors are generally willing to back renewable energy in the context of its increasing share of the overall energy mix, even as they persist in supporting fossil fuel firms profiting from the continued growth in the volume of hydrocarbons consumed worldwide.

But even if the green energy firms had been the big winners of the past two months, this would not be an unalloyed good.

The firms have environmental and social costs, such as the heavy deforestation in South East Asia to meet the increased demand for palm oil from the biodiesel sector. Or the vast quantities of cobalt - a key component of the batteries that store renewable energy and power electric cars - that are mined in highly exploitative and ecologically destructive conditions in the Democratic Republic of Congo.

Given these concerns, governments must play a larger role in directly investing in renewables, rather than relying on equity markets that prioritize short-term profits above all else. In doing so, they must also enforce standards on materials procurement and labor conditions in renewable energy supply chains. Equally, they should focus on curtailing fossil fuel extraction rather than enabling its expansion.

Overall, while the current actions of equity investors offer a grim augury for the future, it is ultimately governmental action that will determine whether we move on a path towards justice and ecological restoration.

As Russia continues to inflict untold suffering and devastation in Ukraine, many around the world are profiting amid the horrific bloodshed.

Depressingly, given the spiraling climate crisis, fossil fuel firms - and their investors - are the biggest winners of the war, reaping the benefits of surging energy prices and new governmental measures to expand oil production.

Coal companies and offshore drilling services have done the best out of the geopolitical crisis, both registering an astonishing 42% increase in their market value.

But who else is cashing in on the emerging war economy? To determine this, we must look closer at the market capitalization data, which reveals investors' expectations about different firms' earnings capacities.

The more the market value of a firm rises, the higher it ascends in the overall corporate hierarchy. With this in mind, the graph below shows the 20 corporate sectors that have enjoyed the largest increase in company market value - outperforming 153 others - since the Russian invasion began on 24 February.

Aside from those involved in the extraction, processing, and distribution of fossil fuels - which, remarkably, directly relate to seven of the 20 highest performing sectors - arms manufacturers are, predictably, the other major beneficiaries.

Such firms have seen a 15% increase in their market value due to the heightened demand for military hardware and the commitment by NATO governments to expand military spending.

Agricultural commodity traders have also seen 10% growth in market capitalization in the past two months, profiting hugely from the market instability and rising commodity prices brought about by the conflict.

This has led critics to argue that, in many ways, these traders actually promote the disruption in food systems that they then benefit from.

The situation is decidedly gloomy. Amid continuing war in Ukraine, escalating tensions between Russia and the West, a cost-of-living crisis in Europe and the wider world, and ongoing global warming, investors are backing those firms that directly benefit from geopolitical conflict, commodity market instability, and our continued dependency on fossil fuels.

There are, however, some glimmers of hope. Alternative fuels companies - which operate in areas ranging from the installation of charging points for electric vehicles to the production of bioenergy and the manufacture of hydrogen fuel cells - have seen their market value grow by 38%.

Companies engaged in generating electricity from renewable sources, such as wind and solar power, have also enjoyed a 15% rise.

This indicates that investors are generally willing to back renewable energy in the context of its increasing share of the overall energy mix, even as they persist in supporting fossil fuel firms profiting from the continued growth in the volume of hydrocarbons consumed worldwide.

But even if the green energy firms had been the big winners of the past two months, this would not be an unalloyed good.

The firms have environmental and social costs, such as the heavy deforestation in South East Asia to meet the increased demand for palm oil from the biodiesel sector. Or the vast quantities of cobalt - a key component of the batteries that store renewable energy and power electric cars - that are mined in highly exploitative and ecologically destructive conditions in the Democratic Republic of Congo.

Given these concerns, governments must play a larger role in directly investing in renewables, rather than relying on equity markets that prioritize short-term profits above all else. In doing so, they must also enforce standards on materials procurement and labor conditions in renewable energy supply chains. Equally, they should focus on curtailing fossil fuel extraction rather than enabling its expansion.

Overall, while the current actions of equity investors offer a grim augury for the future, it is ultimately governmental action that will determine whether we move on a path towards justice and ecological restoration.

As Russia continues to inflict untold suffering and devastation in Ukraine, many around the world are profiting amid the horrific bloodshed.

Depressingly, given the spiraling climate crisis, fossil fuel firms - and their investors - are the biggest winners of the war, reaping the benefits of surging energy prices and new governmental measures to expand oil production.

Coal companies and offshore drilling services have done the best out of the geopolitical crisis, both registering an astonishing 42% increase in their market value.

But who else is cashing in on the emerging war economy? To determine this, we must look closer at the market capitalization data, which reveals investors' expectations about different firms' earnings capacities.

The more the market value of a firm rises, the higher it ascends in the overall corporate hierarchy. With this in mind, the graph below shows the 20 corporate sectors that have enjoyed the largest increase in company market value - outperforming 153 others - since the Russian invasion began on 24 February.

Aside from those involved in the extraction, processing, and distribution of fossil fuels - which, remarkably, directly relate to seven of the 20 highest performing sectors - arms manufacturers are, predictably, the other major beneficiaries.

Such firms have seen a 15% increase in their market value due to the heightened demand for military hardware and the commitment by NATO governments to expand military spending.

Agricultural commodity traders have also seen 10% growth in market capitalization in the past two months, profiting hugely from the market instability and rising commodity prices brought about by the conflict.

This has led critics to argue that, in many ways, these traders actually promote the disruption in food systems that they then benefit from.

The situation is decidedly gloomy. Amid continuing war in Ukraine, escalating tensions between Russia and the West, a cost-of-living crisis in Europe and the wider world, and ongoing global warming, investors are backing those firms that directly benefit from geopolitical conflict, commodity market instability, and our continued dependency on fossil fuels.

There are, however, some glimmers of hope. Alternative fuels companies - which operate in areas ranging from the installation of charging points for electric vehicles to the production of bioenergy and the manufacture of hydrogen fuel cells - have seen their market value grow by 38%.

Companies engaged in generating electricity from renewable sources, such as wind and solar power, have also enjoyed a 15% rise.

This indicates that investors are generally willing to back renewable energy in the context of its increasing share of the overall energy mix, even as they persist in supporting fossil fuel firms profiting from the continued growth in the volume of hydrocarbons consumed worldwide.

But even if the green energy firms had been the big winners of the past two months, this would not be an unalloyed good.

The firms have environmental and social costs, such as the heavy deforestation in South East Asia to meet the increased demand for palm oil from the biodiesel sector. Or the vast quantities of cobalt - a key component of the batteries that store renewable energy and power electric cars - that are mined in highly exploitative and ecologically destructive conditions in the Democratic Republic of Congo.

Given these concerns, governments must play a larger role in directly investing in renewables, rather than relying on equity markets that prioritize short-term profits above all else. In doing so, they must also enforce standards on materials procurement and labor conditions in renewable energy supply chains. Equally, they should focus on curtailing fossil fuel extraction rather than enabling its expansion.

Overall, while the current actions of equity investors offer a grim augury for the future, it is ultimately governmental action that will determine whether we move on a path towards justice and ecological restoration.