SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

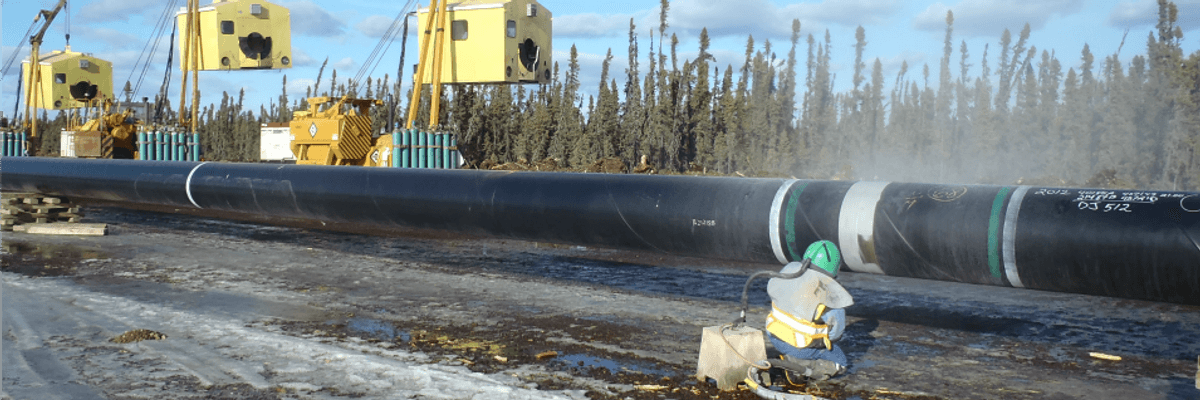

Roads, bridges, and pipelines will be constructed without the necessary protections for clean air, clean water, and the environment. (Photo: jasonwoodhead23/Flickr/cc)

In his January State of the Union address, President Trump called for $1.5 trillion in infrastructure spending over the next decade. If that amount materialized, it could go a long way toward meeting the nation's infrastructure needs. But the release on February 12 of his detailed plan for raising and allocating those funds dashed any hope that this administration would address the nation's acute need for infrastructure investment.

The meagerness of the federal contribution -- just $200 billion over ten years, or less than 0.1 percent of GDP over that period -- was already clear from the State of the Union. Half of those funds are allocated to an Incentive Program intended to support surface transportation and airports, passenger rail, ports and waterways, flood control, water supply, hydropower, water resources, drinking water facilities, wastewater facilities, storm water facilities, and brownfield and Superfund sites. Just listing everything the President's plan claims to address for a federal expenditure of just $100 billion makes the inadequacy of the plan obvious. But there's more.

The Incentive Program requires states and localities to put up 80 percent of the cost of any project in order to get a federal match of 20 percent. This turns the traditional approach to infrastructure investment on its head. The federal government typically provides 80 percent of the funding for such projects. It is wishful thinking to imagine how cash-strapped states and cities -- already on the hook for extensive local infrastructure spending -- will be able to find new public sources of financing, especially now that the recent Republican-passed tax law has severely limited their ability to raise taxes to pay for such undertakings.

Trump's plan turns infrastructure investment on its head in another way as well. Traditionally, the selection of projects to be funded by the federal government emphasized benefits to the public. The administration's plan weighs the ability to attract sources of funding outside the federal government at 70 percent when considering whether to support it; economic and social returns from the project count for just 5 percent. Federal funding will go to projects that are most attractive to private investors, rather than to those, like clean water, that meet the needs of communities.

President Trump's plans for the nation's infrastructure are, unbelievably, even worse than they appear. In the President's budget, released on the same day as the infrastructure plan, Democrats in Congress identified more than $240 billion over the next decade in proposed cuts to ongoing infrastructure. This includes a cut of $122 billion to the Highway Trust Fund as well as reductions in programs that fund rail, aviation, and wastewater projects. Net federal spending on infrastructure may actually fall over the next decade if the President's plans are approved by Congress, potentially leaving the nation's infrastructure in a more dire condition than when he took office.

Public-Private Partnerships and the Role of Private Equity

With states and localities sidelined by budget realities, the administration appears to be counting on private investors to step-up and propose public-private partnerships. No doubt some projects will attract private financing. The infrastructure plan sweetens such deals by:

Increased tolls and fees paid by the public would go to private investors that engage in partnerships with public agencies.

Private equity (PE) firms increased fundraising for infrastructure investment following Trump's election. As an advisor to the Trump campaign, private equity mogul (now Commerce Secretary) Wilbur Ross promulgated a no-lose, high-return plan for private equity investment in infrastructure. Shortly after Trump's inauguration, Joe Baratta, global head of private equity at Blackstone Group, the largest private equity firm in the world, announced plans to raise an infrastructure fund of as much as $40 billion in equity. This would be Blackstone's largest fund ever. Global Infrastructure Partners did raise $15.8 billion for what is currently the largest infrastructure fund. Brookfield Asset Management Inc. raised $14 billion for its third infrastructure fund. In 2017, PE firms raised a record amount of money -- nearly $40 billion, not counting the Blackstone fund that is still in process -- for infrastructure investment; PE funds now hold $70 billion for this purpose.

Little of Ross' proposal, that would have secured high returns for private equity investors, has survived in the plan put forward by President Trump. In spite of two years of fundraising, it's unclear how much PE will contribute to the 80 percent mix of state, local and private funds needed to qualify for federal funds. Adding to the murky role PE will play in infrastructure investment, the return expectations for infrastructure investment have actually come down, and experienced PE investors generally expect a 10 to 11 percent return on investment for core infrastructure strategies.

Moreover, absent strong guarantees of outsized earnings, PE infrastructure funds prefer to buy existing public assets, rather than invest in developing new infrastructure. This may explain the bizarre and unexpected proposals in President Trump's budget to sell Dulles and Reagan National airports, the Baltimore-Washington and George Washington Parkways, the Tennessee Valley electric power assets, and so much more government-owned infrastructure.

What is clear is that the public will pay for local infrastructure projects carried out under the $100 billion Incentive Program, whether financed by state and local governments alone, or via public-private partnerships, through fees, tolls, and possibly higher gasoline taxes. The needs of poorer communities unable to raise much money will largely go unmet.

Other Provisions in the Infrastructure Plan

In addition to the $100 billion Incentive Program, another $50 billion would be allocated to the Rural Infrastructure Program, 80 percent of it in the form of block grants to states to be used in rural areas with populations of less than 50,000 and for Tribal and territorial infrastructure. This is just $5 billion a year spread across the entire United States. Another $20 billion would be made available for Transformative Projects. These grants would be administered by Ross' Department of Commerce and would cover 30 to 80 percent of the costs of these projects, depending on whether the funds were requested for a demonstration project, project planning, or capital construction.

One element of the infrastructure plan has survived since it was first proposed during Trump's presidential campaign: the plan will gut environmental protection requirements that date back to the 1970s. Under rubrics such as "streamlining the application process" or "getting projects completed more quickly," roads, bridges, and pipelines will be constructed without the necessary protections for clean air, clean water, and the environment. Some projects would be allowed to proceed before completion of a review by the National Environmental Protection Act. Local communities would not know the environmental impacts they will face and will have little opportunity for input during project planning.

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

In his January State of the Union address, President Trump called for $1.5 trillion in infrastructure spending over the next decade. If that amount materialized, it could go a long way toward meeting the nation's infrastructure needs. But the release on February 12 of his detailed plan for raising and allocating those funds dashed any hope that this administration would address the nation's acute need for infrastructure investment.

The meagerness of the federal contribution -- just $200 billion over ten years, or less than 0.1 percent of GDP over that period -- was already clear from the State of the Union. Half of those funds are allocated to an Incentive Program intended to support surface transportation and airports, passenger rail, ports and waterways, flood control, water supply, hydropower, water resources, drinking water facilities, wastewater facilities, storm water facilities, and brownfield and Superfund sites. Just listing everything the President's plan claims to address for a federal expenditure of just $100 billion makes the inadequacy of the plan obvious. But there's more.

The Incentive Program requires states and localities to put up 80 percent of the cost of any project in order to get a federal match of 20 percent. This turns the traditional approach to infrastructure investment on its head. The federal government typically provides 80 percent of the funding for such projects. It is wishful thinking to imagine how cash-strapped states and cities -- already on the hook for extensive local infrastructure spending -- will be able to find new public sources of financing, especially now that the recent Republican-passed tax law has severely limited their ability to raise taxes to pay for such undertakings.

Trump's plan turns infrastructure investment on its head in another way as well. Traditionally, the selection of projects to be funded by the federal government emphasized benefits to the public. The administration's plan weighs the ability to attract sources of funding outside the federal government at 70 percent when considering whether to support it; economic and social returns from the project count for just 5 percent. Federal funding will go to projects that are most attractive to private investors, rather than to those, like clean water, that meet the needs of communities.

President Trump's plans for the nation's infrastructure are, unbelievably, even worse than they appear. In the President's budget, released on the same day as the infrastructure plan, Democrats in Congress identified more than $240 billion over the next decade in proposed cuts to ongoing infrastructure. This includes a cut of $122 billion to the Highway Trust Fund as well as reductions in programs that fund rail, aviation, and wastewater projects. Net federal spending on infrastructure may actually fall over the next decade if the President's plans are approved by Congress, potentially leaving the nation's infrastructure in a more dire condition than when he took office.

Public-Private Partnerships and the Role of Private Equity

With states and localities sidelined by budget realities, the administration appears to be counting on private investors to step-up and propose public-private partnerships. No doubt some projects will attract private financing. The infrastructure plan sweetens such deals by:

Increased tolls and fees paid by the public would go to private investors that engage in partnerships with public agencies.

Private equity (PE) firms increased fundraising for infrastructure investment following Trump's election. As an advisor to the Trump campaign, private equity mogul (now Commerce Secretary) Wilbur Ross promulgated a no-lose, high-return plan for private equity investment in infrastructure. Shortly after Trump's inauguration, Joe Baratta, global head of private equity at Blackstone Group, the largest private equity firm in the world, announced plans to raise an infrastructure fund of as much as $40 billion in equity. This would be Blackstone's largest fund ever. Global Infrastructure Partners did raise $15.8 billion for what is currently the largest infrastructure fund. Brookfield Asset Management Inc. raised $14 billion for its third infrastructure fund. In 2017, PE firms raised a record amount of money -- nearly $40 billion, not counting the Blackstone fund that is still in process -- for infrastructure investment; PE funds now hold $70 billion for this purpose.

Little of Ross' proposal, that would have secured high returns for private equity investors, has survived in the plan put forward by President Trump. In spite of two years of fundraising, it's unclear how much PE will contribute to the 80 percent mix of state, local and private funds needed to qualify for federal funds. Adding to the murky role PE will play in infrastructure investment, the return expectations for infrastructure investment have actually come down, and experienced PE investors generally expect a 10 to 11 percent return on investment for core infrastructure strategies.

Moreover, absent strong guarantees of outsized earnings, PE infrastructure funds prefer to buy existing public assets, rather than invest in developing new infrastructure. This may explain the bizarre and unexpected proposals in President Trump's budget to sell Dulles and Reagan National airports, the Baltimore-Washington and George Washington Parkways, the Tennessee Valley electric power assets, and so much more government-owned infrastructure.

What is clear is that the public will pay for local infrastructure projects carried out under the $100 billion Incentive Program, whether financed by state and local governments alone, or via public-private partnerships, through fees, tolls, and possibly higher gasoline taxes. The needs of poorer communities unable to raise much money will largely go unmet.

Other Provisions in the Infrastructure Plan

In addition to the $100 billion Incentive Program, another $50 billion would be allocated to the Rural Infrastructure Program, 80 percent of it in the form of block grants to states to be used in rural areas with populations of less than 50,000 and for Tribal and territorial infrastructure. This is just $5 billion a year spread across the entire United States. Another $20 billion would be made available for Transformative Projects. These grants would be administered by Ross' Department of Commerce and would cover 30 to 80 percent of the costs of these projects, depending on whether the funds were requested for a demonstration project, project planning, or capital construction.

One element of the infrastructure plan has survived since it was first proposed during Trump's presidential campaign: the plan will gut environmental protection requirements that date back to the 1970s. Under rubrics such as "streamlining the application process" or "getting projects completed more quickly," roads, bridges, and pipelines will be constructed without the necessary protections for clean air, clean water, and the environment. Some projects would be allowed to proceed before completion of a review by the National Environmental Protection Act. Local communities would not know the environmental impacts they will face and will have little opportunity for input during project planning.

In his January State of the Union address, President Trump called for $1.5 trillion in infrastructure spending over the next decade. If that amount materialized, it could go a long way toward meeting the nation's infrastructure needs. But the release on February 12 of his detailed plan for raising and allocating those funds dashed any hope that this administration would address the nation's acute need for infrastructure investment.

The meagerness of the federal contribution -- just $200 billion over ten years, or less than 0.1 percent of GDP over that period -- was already clear from the State of the Union. Half of those funds are allocated to an Incentive Program intended to support surface transportation and airports, passenger rail, ports and waterways, flood control, water supply, hydropower, water resources, drinking water facilities, wastewater facilities, storm water facilities, and brownfield and Superfund sites. Just listing everything the President's plan claims to address for a federal expenditure of just $100 billion makes the inadequacy of the plan obvious. But there's more.

The Incentive Program requires states and localities to put up 80 percent of the cost of any project in order to get a federal match of 20 percent. This turns the traditional approach to infrastructure investment on its head. The federal government typically provides 80 percent of the funding for such projects. It is wishful thinking to imagine how cash-strapped states and cities -- already on the hook for extensive local infrastructure spending -- will be able to find new public sources of financing, especially now that the recent Republican-passed tax law has severely limited their ability to raise taxes to pay for such undertakings.

Trump's plan turns infrastructure investment on its head in another way as well. Traditionally, the selection of projects to be funded by the federal government emphasized benefits to the public. The administration's plan weighs the ability to attract sources of funding outside the federal government at 70 percent when considering whether to support it; economic and social returns from the project count for just 5 percent. Federal funding will go to projects that are most attractive to private investors, rather than to those, like clean water, that meet the needs of communities.

President Trump's plans for the nation's infrastructure are, unbelievably, even worse than they appear. In the President's budget, released on the same day as the infrastructure plan, Democrats in Congress identified more than $240 billion over the next decade in proposed cuts to ongoing infrastructure. This includes a cut of $122 billion to the Highway Trust Fund as well as reductions in programs that fund rail, aviation, and wastewater projects. Net federal spending on infrastructure may actually fall over the next decade if the President's plans are approved by Congress, potentially leaving the nation's infrastructure in a more dire condition than when he took office.

Public-Private Partnerships and the Role of Private Equity

With states and localities sidelined by budget realities, the administration appears to be counting on private investors to step-up and propose public-private partnerships. No doubt some projects will attract private financing. The infrastructure plan sweetens such deals by:

Increased tolls and fees paid by the public would go to private investors that engage in partnerships with public agencies.

Private equity (PE) firms increased fundraising for infrastructure investment following Trump's election. As an advisor to the Trump campaign, private equity mogul (now Commerce Secretary) Wilbur Ross promulgated a no-lose, high-return plan for private equity investment in infrastructure. Shortly after Trump's inauguration, Joe Baratta, global head of private equity at Blackstone Group, the largest private equity firm in the world, announced plans to raise an infrastructure fund of as much as $40 billion in equity. This would be Blackstone's largest fund ever. Global Infrastructure Partners did raise $15.8 billion for what is currently the largest infrastructure fund. Brookfield Asset Management Inc. raised $14 billion for its third infrastructure fund. In 2017, PE firms raised a record amount of money -- nearly $40 billion, not counting the Blackstone fund that is still in process -- for infrastructure investment; PE funds now hold $70 billion for this purpose.

Little of Ross' proposal, that would have secured high returns for private equity investors, has survived in the plan put forward by President Trump. In spite of two years of fundraising, it's unclear how much PE will contribute to the 80 percent mix of state, local and private funds needed to qualify for federal funds. Adding to the murky role PE will play in infrastructure investment, the return expectations for infrastructure investment have actually come down, and experienced PE investors generally expect a 10 to 11 percent return on investment for core infrastructure strategies.

Moreover, absent strong guarantees of outsized earnings, PE infrastructure funds prefer to buy existing public assets, rather than invest in developing new infrastructure. This may explain the bizarre and unexpected proposals in President Trump's budget to sell Dulles and Reagan National airports, the Baltimore-Washington and George Washington Parkways, the Tennessee Valley electric power assets, and so much more government-owned infrastructure.

What is clear is that the public will pay for local infrastructure projects carried out under the $100 billion Incentive Program, whether financed by state and local governments alone, or via public-private partnerships, through fees, tolls, and possibly higher gasoline taxes. The needs of poorer communities unable to raise much money will largely go unmet.

Other Provisions in the Infrastructure Plan

In addition to the $100 billion Incentive Program, another $50 billion would be allocated to the Rural Infrastructure Program, 80 percent of it in the form of block grants to states to be used in rural areas with populations of less than 50,000 and for Tribal and territorial infrastructure. This is just $5 billion a year spread across the entire United States. Another $20 billion would be made available for Transformative Projects. These grants would be administered by Ross' Department of Commerce and would cover 30 to 80 percent of the costs of these projects, depending on whether the funds were requested for a demonstration project, project planning, or capital construction.

One element of the infrastructure plan has survived since it was first proposed during Trump's presidential campaign: the plan will gut environmental protection requirements that date back to the 1970s. Under rubrics such as "streamlining the application process" or "getting projects completed more quickly," roads, bridges, and pipelines will be constructed without the necessary protections for clean air, clean water, and the environment. Some projects would be allowed to proceed before completion of a review by the National Environmental Protection Act. Local communities would not know the environmental impacts they will face and will have little opportunity for input during project planning.