SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

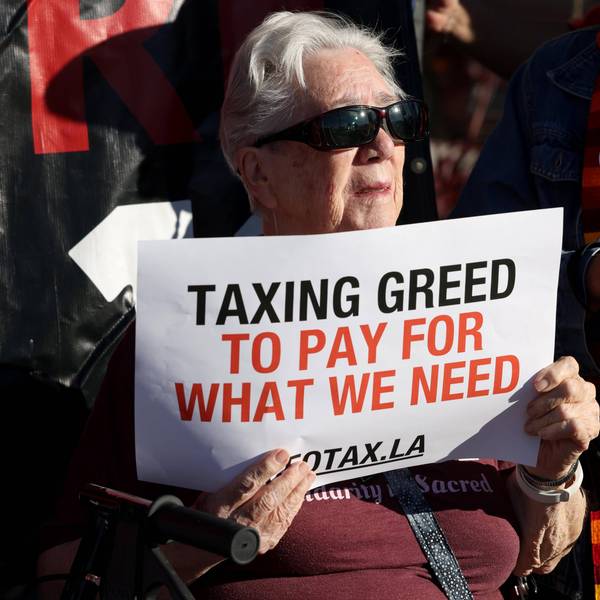

Hours before the Federal Reserve was to announce whether it would increase interest rates, several dozen protesters gathered outside Federal Reserve offices in downtown Washington to demand that the Fed keep interest rates where they are, arguing that the economy as they experience it has yet to recover.

It was not clear whether any of the Federal Reserve members heard the demonstrators, organized by the Center for Popular Democracy's Fed Up coalition, but the demonstrators got their victory nonetheless: After the protesters left, the Fed announced that it would keep its zero-interest-rate policy in effect for a while longer.

That takes off the table the immediate fear that a rate hike would set in motion a slowing down of economic growth before that growth could lift the fortunes of millions of people still looking for work or whose wages have stagnated because the labor market is not tight enough.

"The case for raising short-term interest rates is extraordinarily weak," said Josh Bivens, economist with the Economic Policy Institute. That case would be a tight labor market that forces employers to pay more to find good workers, and an inflation rate that is accelerating. "That is not the economy we have today."

The Fed agreed, saying in a statement that it would wait for "some further improvement in the labor market" and noting that " inflation is anticipated to remain near its recent low level in the near term."

There still remains the longer-term issue of reclaiming the definition of "full employment" in a way that makes sense for workers and the Main Street economy.

Many economic experts and commentators have been declaring that at an unemployment rate of 5.1 percent overall the U.S. economy has already just about reached full employment - hence the pressure on the Fed to increase interest rates and focus on taming inflation, even though inflation rates are far from being in a position to need to be tamed.

Rep. John Conyers (D-Mich.) introduced a bill in Congress today that says what most people on Main Street know is the reality - we are nowhere near full employment yet.

That bill would explicitly define unemployment at "rate of not more than 4 percent" and would call on the Federal Reserve to work toward that goal and "a stable rate of inflation."

"Now the swappers and the investors and the funders on Wall Street gave us the recession and threw millions of Americans out of work and caused a lot of pain and suffering. What we're doing now is taking action," Conyers said. "We want jobs, and the only we can get it is to follow the plans of progressive economists" to encourage more investment in the Main Street economy and create more jobs.

That bill is unlikely to get a serious hearing in a Republican-controlled Congress, but it is a way to change an economic discussion that is often too preoccupied with the ghost of inflation and not concerned enough about the reality of people who are out of work or stranded in low-paying jobs.

"Let's test how low unemployment can go," Bivens said. "That's what they stakes are about today."

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

Hours before the Federal Reserve was to announce whether it would increase interest rates, several dozen protesters gathered outside Federal Reserve offices in downtown Washington to demand that the Fed keep interest rates where they are, arguing that the economy as they experience it has yet to recover.

It was not clear whether any of the Federal Reserve members heard the demonstrators, organized by the Center for Popular Democracy's Fed Up coalition, but the demonstrators got their victory nonetheless: After the protesters left, the Fed announced that it would keep its zero-interest-rate policy in effect for a while longer.

That takes off the table the immediate fear that a rate hike would set in motion a slowing down of economic growth before that growth could lift the fortunes of millions of people still looking for work or whose wages have stagnated because the labor market is not tight enough.

"The case for raising short-term interest rates is extraordinarily weak," said Josh Bivens, economist with the Economic Policy Institute. That case would be a tight labor market that forces employers to pay more to find good workers, and an inflation rate that is accelerating. "That is not the economy we have today."

The Fed agreed, saying in a statement that it would wait for "some further improvement in the labor market" and noting that " inflation is anticipated to remain near its recent low level in the near term."

There still remains the longer-term issue of reclaiming the definition of "full employment" in a way that makes sense for workers and the Main Street economy.

Many economic experts and commentators have been declaring that at an unemployment rate of 5.1 percent overall the U.S. economy has already just about reached full employment - hence the pressure on the Fed to increase interest rates and focus on taming inflation, even though inflation rates are far from being in a position to need to be tamed.

Rep. John Conyers (D-Mich.) introduced a bill in Congress today that says what most people on Main Street know is the reality - we are nowhere near full employment yet.

That bill would explicitly define unemployment at "rate of not more than 4 percent" and would call on the Federal Reserve to work toward that goal and "a stable rate of inflation."

"Now the swappers and the investors and the funders on Wall Street gave us the recession and threw millions of Americans out of work and caused a lot of pain and suffering. What we're doing now is taking action," Conyers said. "We want jobs, and the only we can get it is to follow the plans of progressive economists" to encourage more investment in the Main Street economy and create more jobs.

That bill is unlikely to get a serious hearing in a Republican-controlled Congress, but it is a way to change an economic discussion that is often too preoccupied with the ghost of inflation and not concerned enough about the reality of people who are out of work or stranded in low-paying jobs.

"Let's test how low unemployment can go," Bivens said. "That's what they stakes are about today."

Hours before the Federal Reserve was to announce whether it would increase interest rates, several dozen protesters gathered outside Federal Reserve offices in downtown Washington to demand that the Fed keep interest rates where they are, arguing that the economy as they experience it has yet to recover.

It was not clear whether any of the Federal Reserve members heard the demonstrators, organized by the Center for Popular Democracy's Fed Up coalition, but the demonstrators got their victory nonetheless: After the protesters left, the Fed announced that it would keep its zero-interest-rate policy in effect for a while longer.

That takes off the table the immediate fear that a rate hike would set in motion a slowing down of economic growth before that growth could lift the fortunes of millions of people still looking for work or whose wages have stagnated because the labor market is not tight enough.

"The case for raising short-term interest rates is extraordinarily weak," said Josh Bivens, economist with the Economic Policy Institute. That case would be a tight labor market that forces employers to pay more to find good workers, and an inflation rate that is accelerating. "That is not the economy we have today."

The Fed agreed, saying in a statement that it would wait for "some further improvement in the labor market" and noting that " inflation is anticipated to remain near its recent low level in the near term."

There still remains the longer-term issue of reclaiming the definition of "full employment" in a way that makes sense for workers and the Main Street economy.

Many economic experts and commentators have been declaring that at an unemployment rate of 5.1 percent overall the U.S. economy has already just about reached full employment - hence the pressure on the Fed to increase interest rates and focus on taming inflation, even though inflation rates are far from being in a position to need to be tamed.

Rep. John Conyers (D-Mich.) introduced a bill in Congress today that says what most people on Main Street know is the reality - we are nowhere near full employment yet.

That bill would explicitly define unemployment at "rate of not more than 4 percent" and would call on the Federal Reserve to work toward that goal and "a stable rate of inflation."

"Now the swappers and the investors and the funders on Wall Street gave us the recession and threw millions of Americans out of work and caused a lot of pain and suffering. What we're doing now is taking action," Conyers said. "We want jobs, and the only we can get it is to follow the plans of progressive economists" to encourage more investment in the Main Street economy and create more jobs.

That bill is unlikely to get a serious hearing in a Republican-controlled Congress, but it is a way to change an economic discussion that is often too preoccupied with the ghost of inflation and not concerned enough about the reality of people who are out of work or stranded in low-paying jobs.

"Let's test how low unemployment can go," Bivens said. "That's what they stakes are about today."