This year, I've been focused on how anti-poverty activists can move from a defensive battle defined by trying to save what needs to be saved during these budget debates, to an offensive one, laying out a vision that inspires ongoing, unified action and builds a vibrant movement that connects with people in their communities.

I offered one modest proposal for an "anti-poverty contract"--five issues that impact both low-income and middle class people--around which activists and groups could organize. The Western Center on Law & Poverty and a handful of other national and local groups are trying to build an effort around that idea.

However, when you consider the scale of the problems we face--and what inspires people to take action--clearly much, much more is needed. As I wrote previously, to build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement.

Enter Stephen Lerner.

Lerner is a labor and community organizer who has spent more than three decades organizing hundreds of thousands of janitors, farm workers, garment workers, and other low-wage workers into unions. These efforts resulted in increased wages, first-time health benefits, paid sick days, and other improvements on the job. The architect of the historic Justice for Janitors campaign, he is currently working with unions and community groups across the country to break Wall Street's anti-democratic grip on our politics and our economy.

'To build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement,' writes Kaufmann.Lerner lays out a powerful case about the intersection between poverty and Wall Street accountability--and how a Wall Street accountability movement can transform an economy that offers so few pathways out of poverty, and so many ways to keep people impoverished.

Here is our conversation:

Greg Kaufmann: Why is the Wall Street Accountability movement now the focus of your work and what is the potential you see there?

Stephen Lerner: One of the challenges is that there are so many things wrong right now--that you can be involved in any of a thousand causes. The problem is if they are disconnected it doesn't add up to anything. So, people who are opposed to poverty have a dozen different things they'd like to move on the Hill, none of which are likely to pass at this time.

So the focus on Wall Street is: how do you connect all of these different battles? And, in fact, are there core things in common that drive them together?

If you look at some of the biggest issues of the day--whether it's the loss of wealth in communities of color, the housing crisis, the student debt crisis, local and state governments cutting jobs and services because of debt--you can connect all of these issues to the original economic crisis of 2008, and the growing and continued dominance of the Wall Street big banks.

The majority of people in this country are either impacted by student debt, the ongoing housing crisis, or the crisis of the public sector. And you can trace so much of it to Wall Street. This means instead of having 20 separate campaigns, you can have one campaign, that says how do we rebalance and reorganize the economy so that it benefits everybody--not just a teeny elite at the top.

GK: How does the effort to address these three issues intersect with the fight against poverty in particular?

SL: Let's start with housing. In this country, for many workers and people of color, wealth isn't in the stock market, or the Cayman Islands--it's in a home. And the banks first preyed on folks through subprime loans pre-crisis, making enormous profits while putting people in danger. Then when the bubble burst, millions of people lost their homes, and those who didn't have had outrageous payments because the subprime loans exploded. Now you still have 13 million families that are underwater--owing more on their loans than their homes are worth.

In Latino communities, 66 percent of their wealth was lost, half as a result of housing. In the African-American community it was 53 percent. 50 years of the gains of the civil rights movement and the expansion of the economy were wiped out overnight, pushing millions into poverty. If you add to that the people who are unemployed as a result of the crashed economy--we just have this strange thing that happened: the banks created a disaster, and economists and politicians said, 'That's terrible for the economy, let's give them trillions.' And then the folks who were actually hit the hardest were forced into poverty.

On student debt: funding to public education was dramatically cut, which obviously hurts poor people and workers the most. As it was cut, people had to take out loans. So 37 million people have now run up a trillion dollars in student debt. It's a burden no matter what, but if you come from a family that doesn't have means, you now graduate from school with a crushing debt burden, and then there aren't jobs available. And there's a vicious cycle: you cut the budget of public universities, to give tax breaks to banks and big companies, who respond by creating toxic loan packages for students that they make a profit on. And because public funding of universities has been cut--the schools need to borrow more money in order to operate and build, so the banks get a piece of that action too. And now university endowments are investing in Sallie Mae--the largest private student loan lender--so students have to take out loans to go to school, and the university endowment profits off those loans.

There are much better ways to fund education--like by [publicly] funding education so people can actually afford it, instead of creating these twenty layers that let Wall Street suck money out at every step.

GK: So individuals and families are getting crushed by housing and education debt, and then you say public debt completes a sort of perfect storm?

SL: That's right, what we call predatory public loans. So three things have happened: Wall Street has taken advantage of the desperation of cities and municipalities since the crisis; the deals are so complex that public entities don't know what they are getting into; and third is that Wall Street gets its money at a subsidized, Too Big to Fail rate, and in the case of the discount window, almost for free. Banks get money at .075 percent interest from the Federal Reserve, and they then create all sorts of ways to make more and more money off the spread, from the public sector.

Take interest rate swaps, for example. On the surface it sounds like not a bad idea--a bank says they will protect a city from a fluctuating interest rate by locking it in at, say, 4 percent. If it goes higher, they eat it. And if it goes lower, they make money. But they then add so many different formulas and traps, that all of a sudden when the whole thing blew up during the crisis and a city is hemorrhaging money, and they want to get out of it, it turns out that they have an exit fee that's extraordinary and they can't afford it. In Detroit, the city had to pay around $470 million on a series of bond and interrelated swap deals gone bad at the same time they were laying off police and firemen. So then you end up in fights like, 'Do we help the poor, or do we take workers that are middle class and cut their wages so they'll be poor?'

GK: Describe what this movement looks like--what are some of the asks and how do you see it potentially playing out?

SL: There are multiple levels of how Wall Street is impoverishing the country, and so different people can engage in different ways.

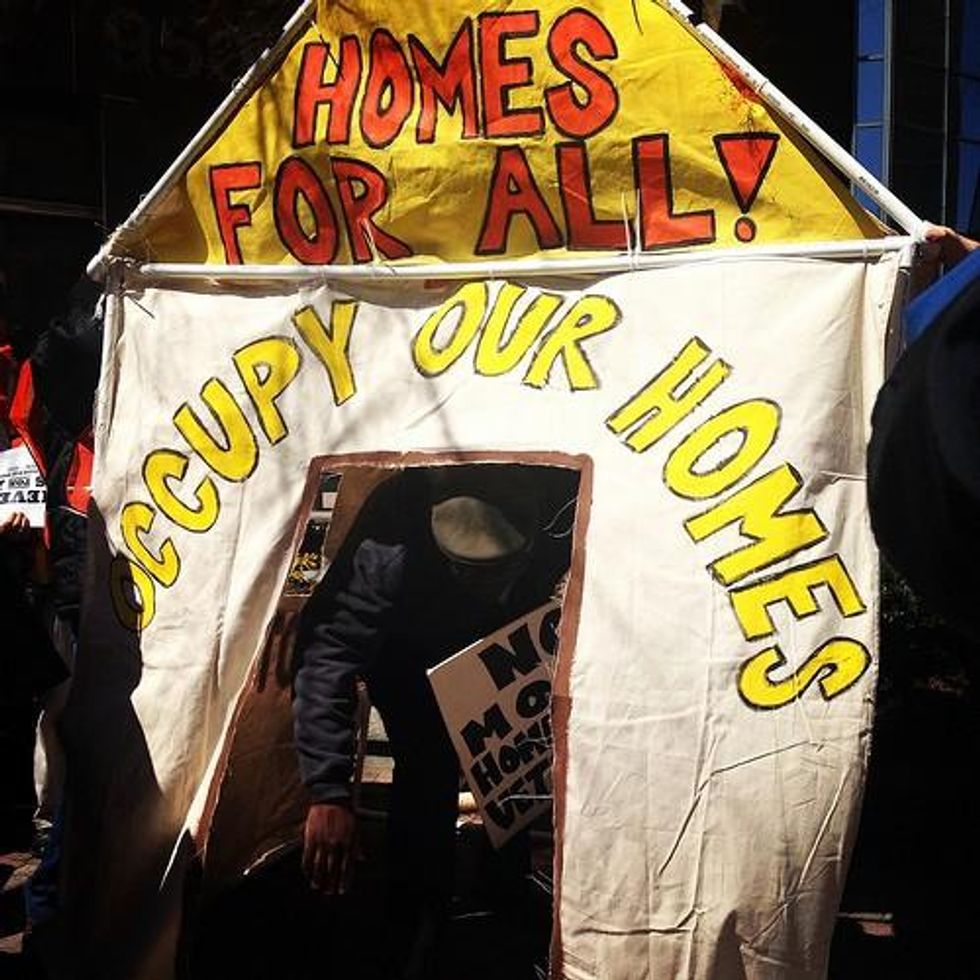

On housing, in Atlanta, Minneapolis, all over California--one piece is the Home Defenders League and Occupy Our Homes. This involves physical encampments, blockading the police, and saying you're not going to take my home, or my neighbor's home. It's incredibly vibrant, street-level resistance--and it's often successful. And as folks are successful, it grows. This is all non-violent, and involves people who are willing to go to jail.

If you take it up a level, there is a simple policy demand, which is that banks should reduce principal on homes to current market value. That means if you're paying a $300,000 mortgage on a home that's worth $200,000, the bank should rewrite it to that value. If we did that, it would save $700 billion to $1 trillion--that's how much people are underwater--and generate $101 billion in economic activity, create 1.5 million jobs, and the average underwater homeowner would save $7,700 a year.

There are cities all over the country that are now exploring using eminent domain to seize these underwater mortgages and rewrite them with principal reductions. For years eminent domain was the tool to take advantage of poor people--tear up a neighborhood, build a highway, build a stadium and tell people they will be paid what their homes are worth on the open market. They said it was for the public good even as it devastated once stable neighborhoods. We're saying let's flip that on it's head--for the public good, let's seize these mortgages and rewrite them at current market value so people can stay in their homes.

On student debt, there is a gamut of activity ranging from student activism on campuses, to state and local legislation, to sit-ins at the Sallie Mae shareholders meeting, to challenging the Education Department on why they have as contractors like Sallie Mae that are profiting off this disaster. The movement includes Senator Elizabeth Warren's brilliant bill to give students loans at the same rate we give to banks. Why should banks get money cheap and student loans be more expensive? And it includes people on their college campuses--a movement around Big Banks Off Campus--because the banks shouldn't be allowed to come on campus and sell their credit cards and figure out new ways to indebt students.

'You never know what triggers something to go from dedicated souls to a mass movement.'

- Stephen LernerFinally, on public debt, people are fighting back. In the case of Oregon, SEIU Local 503 calculated that the state lost $110 million because of the LIBOR manipulations. So here's what happens, the SEIU public sector union goes in to negotiate with the state representing public employees, and the state says we want to cut all of these services for poor people. And the workers themselves are often poor--homecare workers who haven't had a raise in six years. The state says there is no money. And how do you argue if there's no money? Except that the money was stolen! And so the movement is changing the debate: this is not about are public employees overpaid? Are their too many benefits for poor people? Should we have pre-K or not? There are incredible sums of money out there but we've devised a system that drains it from the bottom to the top. Why don't we cut out the middleman? Like let's have an infrastructure bank and loan the money at cost. Let's figure out a way so banks can't make more than a certain amount of money on the spread. And I know that gives the free-market people heart attacks, because this is intervening in the market, but there is no market. Because five banks control it, and where they get their money is from taxpayers. It's our money.

GK: To what extent are these three threads--on student debt, housing debt, and public debt--coalescing into a movement so they aren't the kind of independent, divided struggles that you suggest hold us back from big victories?

SL: As the campaigns develop, the overlap happens more and more. For example, people are seeing the relationship between housing debt and student debt--needing to take out student loans because your family's house isn't worth anything anymore so you can't help finance an education through a second mortgage like you might have in the past. At the Wells Fargo meeting at Salt Lake City, folks campaigning about student debt showed up, and so did people campaigning on housing, and so did people about the environment. So, on an organic level on the street, people are seeing it more and more.

GK: After I covered the actions at the Wells Fargo shareholders meeting, a progressive friend and writer told me, 'The activists seem to think banks can't ignore their message, that being heard is equivalent to making change." How do you think a movement like this actually could make principal reduction a reality, for example?

SL: First, the enemy of change is the notion that if you are not winning at that moment then you are losing. These things never have an even flow. It's not like you start one day, you have steady escalation--they go up and down. In Taylor Branch's book, At Canaan's Edge, you read these transcripts of FBI wiretaps on civil rights leaders and it's them saying, 'We're losing'...or 'so and so was killed'... or 'we have in-fighting, how will we win?' But when we look back at that period now we see that the Civil Rights bill was going to pass, it was all going to happen. I think when you are in the middle of the battle, under siege, you can't see the forest for the trees.

But your friend's critique is fair in that we've been screaming about the banks for years and they are more powerful than ever--the top six banks now control 73 percent of the total assets in the US banking sector. However, we've started to identify some levers that we think begin to level the playingfield. Eminent domain is one example--if you're not willing to reduce principal, then we'll use the power of the city to force you to do it. On LIBOR, city after city is investigating whether they can sue to get their money back. Many are exploring, and some have passed, bills that say if banks don't meet certain standards the cities won't deal with them anymore. Los Angeles, Oakland, New York, Philadelphia, and Pittsburgh have all passed responsible banking ordinances recently.

Also, the banks greed and hubris is so great that [there are] new avenues to go after them. So if you look at the litigation that California Attorney General Kamala Harris filed: this is where the banks essentially did the same thing with credit card loans that they did with mortgages--they moved to litigation without accurate documentation to even show that people owed them money. We are seeing more opportunities for growing protest, more litigation, and more public policy changes. You even now have Ohio Democratic Senator Sherrod Brown and Louisiana Republican Senator David Vitter working together on a bill to break up the big banks.

GK: Is there a role in this movement for people and organizations that are focused on the Hill?

SL: Petitions can raise important issues and get people involved. Lobbying can be important--but I think what we need to do is connect all of this to an analysis of who the villains are and why the economy is unbalanced. This is not a problem of lack of policy--we have unlimited great policy ideas. This is not a problem of lack of money to fund anti-poverty programs. This is a problem of power. I think people need to accept that there is no real significant economic and political change as long as the finance sector is so dominant. The DC-centric stuff will be far more effective if there is something out there in the rest of the country brewing. If this is just an intellectual policy debate about who has the best idea and who has the best statistics, we're doomed.

GK: To win--to really make the kinds of structural changes you are talking about--does the public protest need to be as constant and visible, engaging and creative, as Occupy Wall Street?

SL: Yes, we need to get to that. And there is an interesting myth about Occupy that somehow it just emerged out of nowhere. But many of the people who were engaged in it were part of other battles before Occupy Wall Street. The month before Occupy community groups were doing rallies and sit-ins at banks all over the country. So you never know when things are going to take off. Why did the Vietnam protests take off when they did? Or the civil rights protests? You never know what triggers something to go from dedicated souls to a mass movement.

But your key point is right--the system is currently working for the banks and super-rich. And as long as they feel it's working we won't really achieve change. And so some combination of mass disruptive protest--non-violent--of all sorts of local legislative activity; of a growing change in the narrative. Some mix and match of that has to put the kind of heat on them that makes them feel they have to negotiate over these issues--that they need, for example, to fix mortgages because the alternative is worse. We need to have a better system on student loans, because the alternative is worse. I think that's really our challenge.

GK: In a recent piece, you suggest that anger is insufficient to sustain a movement--that what keeps people going is love. Can you describe what you mean by that?

SL: There are four things currently that are self-defeating for progressives and labor folks: one, the mantra of progressives is built on 'we're losing, there's no hope, we're getting clobbered.' That leads to the slogan of much of the progressive movement which is 'Let's fight for small, incremental, not particularly important change now.' So what we largely talk about isn't very inspiring. We talk about stopping cuts--stopping bad--not how we win good things.

The great movements--take the story of Exodus--they didn't say, 'Can the Egyptians whip us less often?' They said, 'We're leaving. We're outta here. We're gonna form a new country, a place where we can be free.' Ghandi, South Africa, the civil rights movement--all of these movements were based on this idea that there is something profoundly better that we can fight for. And I think for many of us in America we've lost that ability to say we're engaged in this--not just because we care about principal reduction--but because we believe in the richest country on earth we can transform society and redistribute wealth and power. So, we need to have a vision that's inspiring and not be afraid to be called a little utopian.

Second, we need an analysis, a narrative, of who the bad guys are that are concentrating wealth and power. All of the organizing I was involved with--with the garment workers, the farmworkers, and the janitors--they all had an analysis of who really had the power and could fix things, and I think we've forgotten how to do that.

Third, we need to think about the strategy and tactics that give us leverage, so this is not simply yelling and screaming. And fourth is about love--which is that people are involved both out of self-interest because they want to make their lives better; but also because they realize their life is better if they help make other lives better.

If you look at the great movements that's what happens--some combination of vision, analysis, strategy, and this deep, deep feeling that by supporting and sacrificing for others--in the labor movement we call it solidarity--you not only transform your own life, but you transform the lives of people around you and in doing that transform how society operates. That's the roots of how we build what we have to build.

End 'Too Big to Jail': May 18-23, Washington, DC

If you think what Lerner has to say makes sense, here's an immediate opportunity to get involved. Next week, families on the front lines of the foreclosure crisis are traveling from across the country to the nation's capital to make their voices heard.

Their message is simple: five years into the financial crisis, Wall Street has still not been held accountable and communities are still suffering. In fact, a new report from Alliance for a Just Society, the New Bottom Line, and Home Defenders League shows that $192.6 billion in wealth was lost due to the foreclosure crisis in 2012, and this year another 13 million homes are at risk of foreclosure with $221 billion in wealth on the line. (See "Studies/Briefs" below for more information on this report.)

It's long past time for the Administrations to prosecute those who violated the law and for the banks to repay individuals, families and communities that continue to suffer losses--beginning with reducing their mortgages to fair market value.

"We can't have two systems of justice in this country: one for the rich and powerful, where Wall Street criminals are actually rewarded with bailouts and huge bonuses, and another for the rest of us," said Vivian Richardson, who will be in DC next week after successfully defending her home from foreclosure with the help of members of the Alliance of Californians for Community Empowerment. "These Wall Street banksters stole many homes, and are still committing crimes. It is time for them to be held accountable."

There will be home-defense and non-violent, civil disobedience trainings on May 18-19, and a rally and march to the Department of Justice on Monday, May 20. The activists will attempt to meet with Attorney General Eric Holder and are prepared to take direct action if that doesn't happen--blocking entrances, setting up an Occupy-style encampment, getting arrested and staying in jail.

To participate in the Week of Action, you can RSVP here. To take part in the direct action on May 20 fill out this form.

This year, I've been focused on how anti-poverty activists can move from a defensive battle defined by trying to save what needs to be saved during these budget debates, to an offensive one, laying out a vision that inspires ongoing, unified action and builds a vibrant movement that connects with people in their communities.

I offered one modest proposal for an "anti-poverty contract"--five issues that impact both low-income and middle class people--around which activists and groups could organize. The Western Center on Law & Poverty and a handful of other national and local groups are trying to build an effort around that idea.

However, when you consider the scale of the problems we face--and what inspires people to take action--clearly much, much more is needed. As I wrote previously, to build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement.

Enter Stephen Lerner.

Lerner is a labor and community organizer who has spent more than three decades organizing hundreds of thousands of janitors, farm workers, garment workers, and other low-wage workers into unions. These efforts resulted in increased wages, first-time health benefits, paid sick days, and other improvements on the job. The architect of the historic Justice for Janitors campaign, he is currently working with unions and community groups across the country to break Wall Street's anti-democratic grip on our politics and our economy.

'To build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement,' writes Kaufmann.Lerner lays out a powerful case about the intersection between poverty and Wall Street accountability--and how a Wall Street accountability movement can transform an economy that offers so few pathways out of poverty, and so many ways to keep people impoverished.

Here is our conversation:

Greg Kaufmann: Why is the Wall Street Accountability movement now the focus of your work and what is the potential you see there?

Stephen Lerner: One of the challenges is that there are so many things wrong right now--that you can be involved in any of a thousand causes. The problem is if they are disconnected it doesn't add up to anything. So, people who are opposed to poverty have a dozen different things they'd like to move on the Hill, none of which are likely to pass at this time.

So the focus on Wall Street is: how do you connect all of these different battles? And, in fact, are there core things in common that drive them together?

If you look at some of the biggest issues of the day--whether it's the loss of wealth in communities of color, the housing crisis, the student debt crisis, local and state governments cutting jobs and services because of debt--you can connect all of these issues to the original economic crisis of 2008, and the growing and continued dominance of the Wall Street big banks.

The majority of people in this country are either impacted by student debt, the ongoing housing crisis, or the crisis of the public sector. And you can trace so much of it to Wall Street. This means instead of having 20 separate campaigns, you can have one campaign, that says how do we rebalance and reorganize the economy so that it benefits everybody--not just a teeny elite at the top.

GK: How does the effort to address these three issues intersect with the fight against poverty in particular?

SL: Let's start with housing. In this country, for many workers and people of color, wealth isn't in the stock market, or the Cayman Islands--it's in a home. And the banks first preyed on folks through subprime loans pre-crisis, making enormous profits while putting people in danger. Then when the bubble burst, millions of people lost their homes, and those who didn't have had outrageous payments because the subprime loans exploded. Now you still have 13 million families that are underwater--owing more on their loans than their homes are worth.

In Latino communities, 66 percent of their wealth was lost, half as a result of housing. In the African-American community it was 53 percent. 50 years of the gains of the civil rights movement and the expansion of the economy were wiped out overnight, pushing millions into poverty. If you add to that the people who are unemployed as a result of the crashed economy--we just have this strange thing that happened: the banks created a disaster, and economists and politicians said, 'That's terrible for the economy, let's give them trillions.' And then the folks who were actually hit the hardest were forced into poverty.

On student debt: funding to public education was dramatically cut, which obviously hurts poor people and workers the most. As it was cut, people had to take out loans. So 37 million people have now run up a trillion dollars in student debt. It's a burden no matter what, but if you come from a family that doesn't have means, you now graduate from school with a crushing debt burden, and then there aren't jobs available. And there's a vicious cycle: you cut the budget of public universities, to give tax breaks to banks and big companies, who respond by creating toxic loan packages for students that they make a profit on. And because public funding of universities has been cut--the schools need to borrow more money in order to operate and build, so the banks get a piece of that action too. And now university endowments are investing in Sallie Mae--the largest private student loan lender--so students have to take out loans to go to school, and the university endowment profits off those loans.

There are much better ways to fund education--like by [publicly] funding education so people can actually afford it, instead of creating these twenty layers that let Wall Street suck money out at every step.

GK: So individuals and families are getting crushed by housing and education debt, and then you say public debt completes a sort of perfect storm?

SL: That's right, what we call predatory public loans. So three things have happened: Wall Street has taken advantage of the desperation of cities and municipalities since the crisis; the deals are so complex that public entities don't know what they are getting into; and third is that Wall Street gets its money at a subsidized, Too Big to Fail rate, and in the case of the discount window, almost for free. Banks get money at .075 percent interest from the Federal Reserve, and they then create all sorts of ways to make more and more money off the spread, from the public sector.

Take interest rate swaps, for example. On the surface it sounds like not a bad idea--a bank says they will protect a city from a fluctuating interest rate by locking it in at, say, 4 percent. If it goes higher, they eat it. And if it goes lower, they make money. But they then add so many different formulas and traps, that all of a sudden when the whole thing blew up during the crisis and a city is hemorrhaging money, and they want to get out of it, it turns out that they have an exit fee that's extraordinary and they can't afford it. In Detroit, the city had to pay around $470 million on a series of bond and interrelated swap deals gone bad at the same time they were laying off police and firemen. So then you end up in fights like, 'Do we help the poor, or do we take workers that are middle class and cut their wages so they'll be poor?'

GK: Describe what this movement looks like--what are some of the asks and how do you see it potentially playing out?

SL: There are multiple levels of how Wall Street is impoverishing the country, and so different people can engage in different ways.

On housing, in Atlanta, Minneapolis, all over California--one piece is the Home Defenders League and Occupy Our Homes. This involves physical encampments, blockading the police, and saying you're not going to take my home, or my neighbor's home. It's incredibly vibrant, street-level resistance--and it's often successful. And as folks are successful, it grows. This is all non-violent, and involves people who are willing to go to jail.

If you take it up a level, there is a simple policy demand, which is that banks should reduce principal on homes to current market value. That means if you're paying a $300,000 mortgage on a home that's worth $200,000, the bank should rewrite it to that value. If we did that, it would save $700 billion to $1 trillion--that's how much people are underwater--and generate $101 billion in economic activity, create 1.5 million jobs, and the average underwater homeowner would save $7,700 a year.

There are cities all over the country that are now exploring using eminent domain to seize these underwater mortgages and rewrite them with principal reductions. For years eminent domain was the tool to take advantage of poor people--tear up a neighborhood, build a highway, build a stadium and tell people they will be paid what their homes are worth on the open market. They said it was for the public good even as it devastated once stable neighborhoods. We're saying let's flip that on it's head--for the public good, let's seize these mortgages and rewrite them at current market value so people can stay in their homes.

On student debt, there is a gamut of activity ranging from student activism on campuses, to state and local legislation, to sit-ins at the Sallie Mae shareholders meeting, to challenging the Education Department on why they have as contractors like Sallie Mae that are profiting off this disaster. The movement includes Senator Elizabeth Warren's brilliant bill to give students loans at the same rate we give to banks. Why should banks get money cheap and student loans be more expensive? And it includes people on their college campuses--a movement around Big Banks Off Campus--because the banks shouldn't be allowed to come on campus and sell their credit cards and figure out new ways to indebt students.

'You never know what triggers something to go from dedicated souls to a mass movement.'

- Stephen LernerFinally, on public debt, people are fighting back. In the case of Oregon, SEIU Local 503 calculated that the state lost $110 million because of the LIBOR manipulations. So here's what happens, the SEIU public sector union goes in to negotiate with the state representing public employees, and the state says we want to cut all of these services for poor people. And the workers themselves are often poor--homecare workers who haven't had a raise in six years. The state says there is no money. And how do you argue if there's no money? Except that the money was stolen! And so the movement is changing the debate: this is not about are public employees overpaid? Are their too many benefits for poor people? Should we have pre-K or not? There are incredible sums of money out there but we've devised a system that drains it from the bottom to the top. Why don't we cut out the middleman? Like let's have an infrastructure bank and loan the money at cost. Let's figure out a way so banks can't make more than a certain amount of money on the spread. And I know that gives the free-market people heart attacks, because this is intervening in the market, but there is no market. Because five banks control it, and where they get their money is from taxpayers. It's our money.

GK: To what extent are these three threads--on student debt, housing debt, and public debt--coalescing into a movement so they aren't the kind of independent, divided struggles that you suggest hold us back from big victories?

SL: As the campaigns develop, the overlap happens more and more. For example, people are seeing the relationship between housing debt and student debt--needing to take out student loans because your family's house isn't worth anything anymore so you can't help finance an education through a second mortgage like you might have in the past. At the Wells Fargo meeting at Salt Lake City, folks campaigning about student debt showed up, and so did people campaigning on housing, and so did people about the environment. So, on an organic level on the street, people are seeing it more and more.

GK: After I covered the actions at the Wells Fargo shareholders meeting, a progressive friend and writer told me, 'The activists seem to think banks can't ignore their message, that being heard is equivalent to making change." How do you think a movement like this actually could make principal reduction a reality, for example?

SL: First, the enemy of change is the notion that if you are not winning at that moment then you are losing. These things never have an even flow. It's not like you start one day, you have steady escalation--they go up and down. In Taylor Branch's book, At Canaan's Edge, you read these transcripts of FBI wiretaps on civil rights leaders and it's them saying, 'We're losing'...or 'so and so was killed'... or 'we have in-fighting, how will we win?' But when we look back at that period now we see that the Civil Rights bill was going to pass, it was all going to happen. I think when you are in the middle of the battle, under siege, you can't see the forest for the trees.

But your friend's critique is fair in that we've been screaming about the banks for years and they are more powerful than ever--the top six banks now control 73 percent of the total assets in the US banking sector. However, we've started to identify some levers that we think begin to level the playingfield. Eminent domain is one example--if you're not willing to reduce principal, then we'll use the power of the city to force you to do it. On LIBOR, city after city is investigating whether they can sue to get their money back. Many are exploring, and some have passed, bills that say if banks don't meet certain standards the cities won't deal with them anymore. Los Angeles, Oakland, New York, Philadelphia, and Pittsburgh have all passed responsible banking ordinances recently.

Also, the banks greed and hubris is so great that [there are] new avenues to go after them. So if you look at the litigation that California Attorney General Kamala Harris filed: this is where the banks essentially did the same thing with credit card loans that they did with mortgages--they moved to litigation without accurate documentation to even show that people owed them money. We are seeing more opportunities for growing protest, more litigation, and more public policy changes. You even now have Ohio Democratic Senator Sherrod Brown and Louisiana Republican Senator David Vitter working together on a bill to break up the big banks.

GK: Is there a role in this movement for people and organizations that are focused on the Hill?

SL: Petitions can raise important issues and get people involved. Lobbying can be important--but I think what we need to do is connect all of this to an analysis of who the villains are and why the economy is unbalanced. This is not a problem of lack of policy--we have unlimited great policy ideas. This is not a problem of lack of money to fund anti-poverty programs. This is a problem of power. I think people need to accept that there is no real significant economic and political change as long as the finance sector is so dominant. The DC-centric stuff will be far more effective if there is something out there in the rest of the country brewing. If this is just an intellectual policy debate about who has the best idea and who has the best statistics, we're doomed.

GK: To win--to really make the kinds of structural changes you are talking about--does the public protest need to be as constant and visible, engaging and creative, as Occupy Wall Street?

SL: Yes, we need to get to that. And there is an interesting myth about Occupy that somehow it just emerged out of nowhere. But many of the people who were engaged in it were part of other battles before Occupy Wall Street. The month before Occupy community groups were doing rallies and sit-ins at banks all over the country. So you never know when things are going to take off. Why did the Vietnam protests take off when they did? Or the civil rights protests? You never know what triggers something to go from dedicated souls to a mass movement.

But your key point is right--the system is currently working for the banks and super-rich. And as long as they feel it's working we won't really achieve change. And so some combination of mass disruptive protest--non-violent--of all sorts of local legislative activity; of a growing change in the narrative. Some mix and match of that has to put the kind of heat on them that makes them feel they have to negotiate over these issues--that they need, for example, to fix mortgages because the alternative is worse. We need to have a better system on student loans, because the alternative is worse. I think that's really our challenge.

GK: In a recent piece, you suggest that anger is insufficient to sustain a movement--that what keeps people going is love. Can you describe what you mean by that?

SL: There are four things currently that are self-defeating for progressives and labor folks: one, the mantra of progressives is built on 'we're losing, there's no hope, we're getting clobbered.' That leads to the slogan of much of the progressive movement which is 'Let's fight for small, incremental, not particularly important change now.' So what we largely talk about isn't very inspiring. We talk about stopping cuts--stopping bad--not how we win good things.

The great movements--take the story of Exodus--they didn't say, 'Can the Egyptians whip us less often?' They said, 'We're leaving. We're outta here. We're gonna form a new country, a place where we can be free.' Ghandi, South Africa, the civil rights movement--all of these movements were based on this idea that there is something profoundly better that we can fight for. And I think for many of us in America we've lost that ability to say we're engaged in this--not just because we care about principal reduction--but because we believe in the richest country on earth we can transform society and redistribute wealth and power. So, we need to have a vision that's inspiring and not be afraid to be called a little utopian.

Second, we need an analysis, a narrative, of who the bad guys are that are concentrating wealth and power. All of the organizing I was involved with--with the garment workers, the farmworkers, and the janitors--they all had an analysis of who really had the power and could fix things, and I think we've forgotten how to do that.

Third, we need to think about the strategy and tactics that give us leverage, so this is not simply yelling and screaming. And fourth is about love--which is that people are involved both out of self-interest because they want to make their lives better; but also because they realize their life is better if they help make other lives better.

If you look at the great movements that's what happens--some combination of vision, analysis, strategy, and this deep, deep feeling that by supporting and sacrificing for others--in the labor movement we call it solidarity--you not only transform your own life, but you transform the lives of people around you and in doing that transform how society operates. That's the roots of how we build what we have to build.

End 'Too Big to Jail': May 18-23, Washington, DC

If you think what Lerner has to say makes sense, here's an immediate opportunity to get involved. Next week, families on the front lines of the foreclosure crisis are traveling from across the country to the nation's capital to make their voices heard.

Their message is simple: five years into the financial crisis, Wall Street has still not been held accountable and communities are still suffering. In fact, a new report from Alliance for a Just Society, the New Bottom Line, and Home Defenders League shows that $192.6 billion in wealth was lost due to the foreclosure crisis in 2012, and this year another 13 million homes are at risk of foreclosure with $221 billion in wealth on the line. (See "Studies/Briefs" below for more information on this report.)

It's long past time for the Administrations to prosecute those who violated the law and for the banks to repay individuals, families and communities that continue to suffer losses--beginning with reducing their mortgages to fair market value.

"We can't have two systems of justice in this country: one for the rich and powerful, where Wall Street criminals are actually rewarded with bailouts and huge bonuses, and another for the rest of us," said Vivian Richardson, who will be in DC next week after successfully defending her home from foreclosure with the help of members of the Alliance of Californians for Community Empowerment. "These Wall Street banksters stole many homes, and are still committing crimes. It is time for them to be held accountable."

There will be home-defense and non-violent, civil disobedience trainings on May 18-19, and a rally and march to the Department of Justice on Monday, May 20. The activists will attempt to meet with Attorney General Eric Holder and are prepared to take direct action if that doesn't happen--blocking entrances, setting up an Occupy-style encampment, getting arrested and staying in jail.

To participate in the Week of Action, you can RSVP here. To take part in the direct action on May 20 fill out this form.

This year, I've been focused on how anti-poverty activists can move from a defensive battle defined by trying to save what needs to be saved during these budget debates, to an offensive one, laying out a vision that inspires ongoing, unified action and builds a vibrant movement that connects with people in their communities.

I offered one modest proposal for an "anti-poverty contract"--five issues that impact both low-income and middle class people--around which activists and groups could organize. The Western Center on Law & Poverty and a handful of other national and local groups are trying to build an effort around that idea.

However, when you consider the scale of the problems we face--and what inspires people to take action--clearly much, much more is needed. As I wrote previously, to build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement.

Enter Stephen Lerner.

Lerner is a labor and community organizer who has spent more than three decades organizing hundreds of thousands of janitors, farm workers, garment workers, and other low-wage workers into unions. These efforts resulted in increased wages, first-time health benefits, paid sick days, and other improvements on the job. The architect of the historic Justice for Janitors campaign, he is currently working with unions and community groups across the country to break Wall Street's anti-democratic grip on our politics and our economy.

'To build a new anti-poverty movement will require the kind of organizing and actions that are as creative, visible, and gripping as the Occupy Wall Street movement,' writes Kaufmann.Lerner lays out a powerful case about the intersection between poverty and Wall Street accountability--and how a Wall Street accountability movement can transform an economy that offers so few pathways out of poverty, and so many ways to keep people impoverished.

Here is our conversation:

Greg Kaufmann: Why is the Wall Street Accountability movement now the focus of your work and what is the potential you see there?

Stephen Lerner: One of the challenges is that there are so many things wrong right now--that you can be involved in any of a thousand causes. The problem is if they are disconnected it doesn't add up to anything. So, people who are opposed to poverty have a dozen different things they'd like to move on the Hill, none of which are likely to pass at this time.

So the focus on Wall Street is: how do you connect all of these different battles? And, in fact, are there core things in common that drive them together?

If you look at some of the biggest issues of the day--whether it's the loss of wealth in communities of color, the housing crisis, the student debt crisis, local and state governments cutting jobs and services because of debt--you can connect all of these issues to the original economic crisis of 2008, and the growing and continued dominance of the Wall Street big banks.

The majority of people in this country are either impacted by student debt, the ongoing housing crisis, or the crisis of the public sector. And you can trace so much of it to Wall Street. This means instead of having 20 separate campaigns, you can have one campaign, that says how do we rebalance and reorganize the economy so that it benefits everybody--not just a teeny elite at the top.

GK: How does the effort to address these three issues intersect with the fight against poverty in particular?

SL: Let's start with housing. In this country, for many workers and people of color, wealth isn't in the stock market, or the Cayman Islands--it's in a home. And the banks first preyed on folks through subprime loans pre-crisis, making enormous profits while putting people in danger. Then when the bubble burst, millions of people lost their homes, and those who didn't have had outrageous payments because the subprime loans exploded. Now you still have 13 million families that are underwater--owing more on their loans than their homes are worth.

In Latino communities, 66 percent of their wealth was lost, half as a result of housing. In the African-American community it was 53 percent. 50 years of the gains of the civil rights movement and the expansion of the economy were wiped out overnight, pushing millions into poverty. If you add to that the people who are unemployed as a result of the crashed economy--we just have this strange thing that happened: the banks created a disaster, and economists and politicians said, 'That's terrible for the economy, let's give them trillions.' And then the folks who were actually hit the hardest were forced into poverty.

On student debt: funding to public education was dramatically cut, which obviously hurts poor people and workers the most. As it was cut, people had to take out loans. So 37 million people have now run up a trillion dollars in student debt. It's a burden no matter what, but if you come from a family that doesn't have means, you now graduate from school with a crushing debt burden, and then there aren't jobs available. And there's a vicious cycle: you cut the budget of public universities, to give tax breaks to banks and big companies, who respond by creating toxic loan packages for students that they make a profit on. And because public funding of universities has been cut--the schools need to borrow more money in order to operate and build, so the banks get a piece of that action too. And now university endowments are investing in Sallie Mae--the largest private student loan lender--so students have to take out loans to go to school, and the university endowment profits off those loans.

There are much better ways to fund education--like by [publicly] funding education so people can actually afford it, instead of creating these twenty layers that let Wall Street suck money out at every step.

GK: So individuals and families are getting crushed by housing and education debt, and then you say public debt completes a sort of perfect storm?

SL: That's right, what we call predatory public loans. So three things have happened: Wall Street has taken advantage of the desperation of cities and municipalities since the crisis; the deals are so complex that public entities don't know what they are getting into; and third is that Wall Street gets its money at a subsidized, Too Big to Fail rate, and in the case of the discount window, almost for free. Banks get money at .075 percent interest from the Federal Reserve, and they then create all sorts of ways to make more and more money off the spread, from the public sector.

Take interest rate swaps, for example. On the surface it sounds like not a bad idea--a bank says they will protect a city from a fluctuating interest rate by locking it in at, say, 4 percent. If it goes higher, they eat it. And if it goes lower, they make money. But they then add so many different formulas and traps, that all of a sudden when the whole thing blew up during the crisis and a city is hemorrhaging money, and they want to get out of it, it turns out that they have an exit fee that's extraordinary and they can't afford it. In Detroit, the city had to pay around $470 million on a series of bond and interrelated swap deals gone bad at the same time they were laying off police and firemen. So then you end up in fights like, 'Do we help the poor, or do we take workers that are middle class and cut their wages so they'll be poor?'

GK: Describe what this movement looks like--what are some of the asks and how do you see it potentially playing out?

SL: There are multiple levels of how Wall Street is impoverishing the country, and so different people can engage in different ways.

On housing, in Atlanta, Minneapolis, all over California--one piece is the Home Defenders League and Occupy Our Homes. This involves physical encampments, blockading the police, and saying you're not going to take my home, or my neighbor's home. It's incredibly vibrant, street-level resistance--and it's often successful. And as folks are successful, it grows. This is all non-violent, and involves people who are willing to go to jail.

If you take it up a level, there is a simple policy demand, which is that banks should reduce principal on homes to current market value. That means if you're paying a $300,000 mortgage on a home that's worth $200,000, the bank should rewrite it to that value. If we did that, it would save $700 billion to $1 trillion--that's how much people are underwater--and generate $101 billion in economic activity, create 1.5 million jobs, and the average underwater homeowner would save $7,700 a year.

There are cities all over the country that are now exploring using eminent domain to seize these underwater mortgages and rewrite them with principal reductions. For years eminent domain was the tool to take advantage of poor people--tear up a neighborhood, build a highway, build a stadium and tell people they will be paid what their homes are worth on the open market. They said it was for the public good even as it devastated once stable neighborhoods. We're saying let's flip that on it's head--for the public good, let's seize these mortgages and rewrite them at current market value so people can stay in their homes.

On student debt, there is a gamut of activity ranging from student activism on campuses, to state and local legislation, to sit-ins at the Sallie Mae shareholders meeting, to challenging the Education Department on why they have as contractors like Sallie Mae that are profiting off this disaster. The movement includes Senator Elizabeth Warren's brilliant bill to give students loans at the same rate we give to banks. Why should banks get money cheap and student loans be more expensive? And it includes people on their college campuses--a movement around Big Banks Off Campus--because the banks shouldn't be allowed to come on campus and sell their credit cards and figure out new ways to indebt students.

'You never know what triggers something to go from dedicated souls to a mass movement.'

- Stephen LernerFinally, on public debt, people are fighting back. In the case of Oregon, SEIU Local 503 calculated that the state lost $110 million because of the LIBOR manipulations. So here's what happens, the SEIU public sector union goes in to negotiate with the state representing public employees, and the state says we want to cut all of these services for poor people. And the workers themselves are often poor--homecare workers who haven't had a raise in six years. The state says there is no money. And how do you argue if there's no money? Except that the money was stolen! And so the movement is changing the debate: this is not about are public employees overpaid? Are their too many benefits for poor people? Should we have pre-K or not? There are incredible sums of money out there but we've devised a system that drains it from the bottom to the top. Why don't we cut out the middleman? Like let's have an infrastructure bank and loan the money at cost. Let's figure out a way so banks can't make more than a certain amount of money on the spread. And I know that gives the free-market people heart attacks, because this is intervening in the market, but there is no market. Because five banks control it, and where they get their money is from taxpayers. It's our money.

GK: To what extent are these three threads--on student debt, housing debt, and public debt--coalescing into a movement so they aren't the kind of independent, divided struggles that you suggest hold us back from big victories?

SL: As the campaigns develop, the overlap happens more and more. For example, people are seeing the relationship between housing debt and student debt--needing to take out student loans because your family's house isn't worth anything anymore so you can't help finance an education through a second mortgage like you might have in the past. At the Wells Fargo meeting at Salt Lake City, folks campaigning about student debt showed up, and so did people campaigning on housing, and so did people about the environment. So, on an organic level on the street, people are seeing it more and more.

GK: After I covered the actions at the Wells Fargo shareholders meeting, a progressive friend and writer told me, 'The activists seem to think banks can't ignore their message, that being heard is equivalent to making change." How do you think a movement like this actually could make principal reduction a reality, for example?

SL: First, the enemy of change is the notion that if you are not winning at that moment then you are losing. These things never have an even flow. It's not like you start one day, you have steady escalation--they go up and down. In Taylor Branch's book, At Canaan's Edge, you read these transcripts of FBI wiretaps on civil rights leaders and it's them saying, 'We're losing'...or 'so and so was killed'... or 'we have in-fighting, how will we win?' But when we look back at that period now we see that the Civil Rights bill was going to pass, it was all going to happen. I think when you are in the middle of the battle, under siege, you can't see the forest for the trees.

But your friend's critique is fair in that we've been screaming about the banks for years and they are more powerful than ever--the top six banks now control 73 percent of the total assets in the US banking sector. However, we've started to identify some levers that we think begin to level the playingfield. Eminent domain is one example--if you're not willing to reduce principal, then we'll use the power of the city to force you to do it. On LIBOR, city after city is investigating whether they can sue to get their money back. Many are exploring, and some have passed, bills that say if banks don't meet certain standards the cities won't deal with them anymore. Los Angeles, Oakland, New York, Philadelphia, and Pittsburgh have all passed responsible banking ordinances recently.

Also, the banks greed and hubris is so great that [there are] new avenues to go after them. So if you look at the litigation that California Attorney General Kamala Harris filed: this is where the banks essentially did the same thing with credit card loans that they did with mortgages--they moved to litigation without accurate documentation to even show that people owed them money. We are seeing more opportunities for growing protest, more litigation, and more public policy changes. You even now have Ohio Democratic Senator Sherrod Brown and Louisiana Republican Senator David Vitter working together on a bill to break up the big banks.

GK: Is there a role in this movement for people and organizations that are focused on the Hill?

SL: Petitions can raise important issues and get people involved. Lobbying can be important--but I think what we need to do is connect all of this to an analysis of who the villains are and why the economy is unbalanced. This is not a problem of lack of policy--we have unlimited great policy ideas. This is not a problem of lack of money to fund anti-poverty programs. This is a problem of power. I think people need to accept that there is no real significant economic and political change as long as the finance sector is so dominant. The DC-centric stuff will be far more effective if there is something out there in the rest of the country brewing. If this is just an intellectual policy debate about who has the best idea and who has the best statistics, we're doomed.

GK: To win--to really make the kinds of structural changes you are talking about--does the public protest need to be as constant and visible, engaging and creative, as Occupy Wall Street?

SL: Yes, we need to get to that. And there is an interesting myth about Occupy that somehow it just emerged out of nowhere. But many of the people who were engaged in it were part of other battles before Occupy Wall Street. The month before Occupy community groups were doing rallies and sit-ins at banks all over the country. So you never know when things are going to take off. Why did the Vietnam protests take off when they did? Or the civil rights protests? You never know what triggers something to go from dedicated souls to a mass movement.

But your key point is right--the system is currently working for the banks and super-rich. And as long as they feel it's working we won't really achieve change. And so some combination of mass disruptive protest--non-violent--of all sorts of local legislative activity; of a growing change in the narrative. Some mix and match of that has to put the kind of heat on them that makes them feel they have to negotiate over these issues--that they need, for example, to fix mortgages because the alternative is worse. We need to have a better system on student loans, because the alternative is worse. I think that's really our challenge.

GK: In a recent piece, you suggest that anger is insufficient to sustain a movement--that what keeps people going is love. Can you describe what you mean by that?

SL: There are four things currently that are self-defeating for progressives and labor folks: one, the mantra of progressives is built on 'we're losing, there's no hope, we're getting clobbered.' That leads to the slogan of much of the progressive movement which is 'Let's fight for small, incremental, not particularly important change now.' So what we largely talk about isn't very inspiring. We talk about stopping cuts--stopping bad--not how we win good things.

The great movements--take the story of Exodus--they didn't say, 'Can the Egyptians whip us less often?' They said, 'We're leaving. We're outta here. We're gonna form a new country, a place where we can be free.' Ghandi, South Africa, the civil rights movement--all of these movements were based on this idea that there is something profoundly better that we can fight for. And I think for many of us in America we've lost that ability to say we're engaged in this--not just because we care about principal reduction--but because we believe in the richest country on earth we can transform society and redistribute wealth and power. So, we need to have a vision that's inspiring and not be afraid to be called a little utopian.

Second, we need an analysis, a narrative, of who the bad guys are that are concentrating wealth and power. All of the organizing I was involved with--with the garment workers, the farmworkers, and the janitors--they all had an analysis of who really had the power and could fix things, and I think we've forgotten how to do that.

Third, we need to think about the strategy and tactics that give us leverage, so this is not simply yelling and screaming. And fourth is about love--which is that people are involved both out of self-interest because they want to make their lives better; but also because they realize their life is better if they help make other lives better.

If you look at the great movements that's what happens--some combination of vision, analysis, strategy, and this deep, deep feeling that by supporting and sacrificing for others--in the labor movement we call it solidarity--you not only transform your own life, but you transform the lives of people around you and in doing that transform how society operates. That's the roots of how we build what we have to build.

End 'Too Big to Jail': May 18-23, Washington, DC

If you think what Lerner has to say makes sense, here's an immediate opportunity to get involved. Next week, families on the front lines of the foreclosure crisis are traveling from across the country to the nation's capital to make their voices heard.

Their message is simple: five years into the financial crisis, Wall Street has still not been held accountable and communities are still suffering. In fact, a new report from Alliance for a Just Society, the New Bottom Line, and Home Defenders League shows that $192.6 billion in wealth was lost due to the foreclosure crisis in 2012, and this year another 13 million homes are at risk of foreclosure with $221 billion in wealth on the line. (See "Studies/Briefs" below for more information on this report.)

It's long past time for the Administrations to prosecute those who violated the law and for the banks to repay individuals, families and communities that continue to suffer losses--beginning with reducing their mortgages to fair market value.

"We can't have two systems of justice in this country: one for the rich and powerful, where Wall Street criminals are actually rewarded with bailouts and huge bonuses, and another for the rest of us," said Vivian Richardson, who will be in DC next week after successfully defending her home from foreclosure with the help of members of the Alliance of Californians for Community Empowerment. "These Wall Street banksters stole many homes, and are still committing crimes. It is time for them to be held accountable."

There will be home-defense and non-violent, civil disobedience trainings on May 18-19, and a rally and march to the Department of Justice on Monday, May 20. The activists will attempt to meet with Attorney General Eric Holder and are prepared to take direct action if that doesn't happen--blocking entrances, setting up an Occupy-style encampment, getting arrested and staying in jail.

To participate in the Week of Action, you can RSVP here. To take part in the direct action on May 20 fill out this form.