As American families rush to complete their annual tax returns, many will have paid more in federal income taxes than some of America's largest and most profitable corporations. AT&T, Boeing, Citigroup, Duke Energy and Ford collectively reported more than $20 billion of US pre-tax income last year, yet none of them paid a dime in federal income taxes. Instead, they claimed refunds of more than $1.3 billion from the IRS.

These corporations are not alone in turning tax dodging into a competitive sport. Last year, US corporations paid an effective tax rate of just 12.1 percent, the lowest level in the last forty years, according to the Congressional Budget Office. Sixty years ago, when Republican President Dwight Eisenhower lived in the White House, corporations paid 32 percent of federal government's tax receipts; last year they paid 9 percent.

Below are six examples of how large corporations have rigged the tax rules to ensure that those who have the most get to amass even more, at the expense of everyone else. Figuring out how to unrig them is not rocket science, but it will require strong public pressure on lawmakers to ensure that America's most prosperous corporations pay their fair share.

Boeing's Double Dip

In each of the past nine years, Boeing has reported at least $1 billion in pre-tax profits, yet in only one did it pay any US corporate income taxes. In fact, the aerospace giant got so much money in tax subsidies that it had an effective tax rate of -7.8 percent during this period.

One of the main reasons Boeing has avoided the taxman is that the rest of us subsidize their research and development spending. Last year this amounted to $137 million. Congress first passed the research and experimentation tax credit during the 1981 recession, intending to provide a temporary boost to America's sagging economy. Though it has expired for short periods over the years, it has been renewed thirteen times, and Congress is presently considering making the tax credit permanent.

Government investment in basic research and development can be valuable, but the way the current tax credit is structured, much of the support goes to large well-resourced high-tech firms like Boeing that would have conducted the research anyway as a part of maintaining a vibrant business.

What's particularly disturbing about the Boeing subsidies, however, is that the company already bills the Pentagon for research costs. The third largest defense contractor, Boeing has landed more than $54 billion in government contracts in the past nine years. So essentially, taxpayers are paying for the company's research--twice.

GE's Tax-Free Offshore Profits

General Electric employs 975 people to mine the tax code for every possible deduction. One of their IRS returns ran an awe-inspiring 57,000 pages. As a result, GE paid an effective tax rate of just 2.3 percent on more than $81 billion of US income over the last decade.

One of GE's most lucrative tax breaks is dubbed "the active financing exception." Under US tax law income earned from interest anywhere in the world is taxable in the United States. That is because interest is consider a "passive business activity" that is easily transferred from country to country. The active financing exception allows corporation that establish captive foreign finance subsidiaries to exclude interest they earn offshore from their US taxes. The 1997 subsidy was meant as a temporary measure to help US banks and manufacturers compete internationally.

General Electric's lobbyists, who led the fight to create the subsidy, have made sure the "temporary" part was just a joke. Congress has renewed the exemption multiple times over the last fifteen years. And in the meantime, active financing has allowed GE to legally shift much of its US profits to overseas jurisdictions with lower taxes.

The active financing exception is one of sixty tax breaks, known as "tax extenders," that expired last year. Congress is actively considering reauthorizing them, even while they also consider dramatic cuts to social programs.

AIG's Stealth Bailout

In 2008, American International Group's reckless uncovered bets helped lead the global economy to the brink of collapse. Taxpayers bailed out the rogue insurer to the tune of $182 billion.

Less well-known is a perk the US Treasury made available to AIG that allowed the company to retain its losses to offset against future profits. Tapping these tax losses allowed AIG to report more than $17 billion in tax-free profits in 2011, a move Elizabeth Warren, who chaired the TARP oversight panel, labeled a "stealth bailout." "When the government bailed out AIG, it should not have allowed the failed insurance giant to duck taxes for years to come," wrote Warren in a statement co-signed by three other panel members.

"This corporate tax break transfers public money to AIG's private shareholders and inflates executive pay at AIG--both at the public's expense," added Damon Silvers, another member of the oversight panel. At least four of the executives who stand to benefit financially from the tax break were leading the company at the time of the massive failure.

Apple and Facebook's Double Books

Under current rules, companies can show shareholders and the IRS two different sets of books. In financial statements to shareholders, they're allowed to estimate the value for their executives' stock options at the time they're granted. But when it comes to paying their taxes, they can lower their bill by deducting the full value of the options on the day executives cash them in, which is often a much higher figure. This loophole saved Apple $1.5 billion on its taxes between 2008-10, according to Citizens for Tax Justice, boosting its bottom line and its executive bonuses.

When Facebook becomes a public company later this year, the stock option deduction will save it an estimated $3 billion on taxes, including an immediate $500 million IRS refund of the taxes it has paid during the last two years.

The Ending Excessive Corporate Deductions for Stock Options Act (S. 1375) and the Cut Unjustified Tax Loopholes Act (S. 2075), both introduced by Senator Carl Levin (D-MI) would close this loophole and limit companies to a tax deduction no greater than the expense they report to shareholders.

Pfizer Heaves Domestic Profits Overseas

Pfizer is the largest drug company in the world. It generates 40 percent of its sales in the largest and most lucrative drug market--the United States. And yet Pfizer has reported losses in the US in each of the last four years.

Pfizer's tax disclosures offer some clues to how the company achieves this puzzling result. First, it operates eighty subsidiaries in offshore tax havens. Second, Pfizer's 2011 non-US tax rate was a low 14.7 percent, suggesting that they booked a significant portion of overseas profits in tax havens like Luxembourg, Ireland and Jersey, places where Pfizer has at least ten subsidiaries each.

Here's how these strategies work. A company like Pfizer conducts the bulk of its product and research development in the United States. This work is done by scientists, many of whom were educated in US schools, often using basic research that was funded by US taxpayers. The corporation then takes the patents earned by its US labs and registers them in nations that impose little or no taxes on income from patent royalties. When Pfizer sells a pill, it charges a lot for the use of the patent, telling the IRS that without the intellectual property, the product would be virtually worthless. By doing this, Pfizer transfers much of their profits to the tax haven, while retaining much of the costs of research, advertising and management in the United States. Such shenanigans cost the US Treasury an estimated $100 billion a year.

A pending bill, the Stop Tax Haven Abuse Act, would require that offshore subsidiaries managed from the United States and often little more than a post office box and a brass nameplate be treated as US entities for tax purposes.

Bechtel's "Mini" Masquerade

Though Bechtel is the world's largest telecommunications, engineering and construction firm (with $32.9 billion in revenue and 52,700 employees), in terms of corporate structure it is one of America's largest "small businesses." That's because the giant corporation takes advantage of a 1958 law intended to extend limited liability protection to owners of small, family-owned businesses. Companies that qualify for this law's "S Corporation" status do not have to pay federal corporate income taxes. Instead the company's profits are reported as personal income by individual owners. While the Bechtel empire was hardly the intended beneficiary, their firm technically qualifies for the S Corporation status because it is family run and has less than 100 shareholders.

At the time the law was enacted, the wide differential between top corporate tax rates (52 percent) and top individual rates (91 percent) was a disincentive for gaming the system to dodge taxes. Fast forward half a century and top tax rates have collapsed to only 35 percent for corporations and individuals, erasing the previous disincentive for big corporations to change their business status. By incorporating as an S Corporation, enormous businesses like Bechtel pay just individual taxes, rather than having their corporation pay taxes on corporate profits and shareholders pay taxes on their dividends.

S Corporations, and other businesses where income is taxed only at the individual level, have become the new tax haven, where large businesses have fled to avoid US corporate income taxes. In 2008, more than 14,000 S Corporation tax returns were filed by firms with more than $50 million in revenue, according to the IRS. These 14,000 firms, with an average profit of $6.4 million each, collectively reported 29 percent of the total profit on nearly 4 million S Corporation tax returns. Preserving S Corporation status for real small businesses can help level the playing field, but closing the loophole that allows giant multinational corporations to avoid the corporate taxes that their peers have to pay is key to bringing more fairness to the tax code and more funds into public coffers.

As the 99% Spring unfolds, restoring fairness to our tax code must be at the center of the debate. As it stands, our tax system rewards those at the top, robbing the rest of us of the public money we need to transform the economy from one that works for the 1 percent to one that works for the 100 percent.

A note on the chart. Corporate tax rates were calculated using current federal corporate income taxes paid in 2011 divided by 2011 US pretax income, as reported in company 10-K annual reported filed with the Securities and Exchange Commission. Deferred taxes, which might be paid some day in the future, were excluded, as were income taxes paid to state or local governments. Individual tax rates were taken from a recent Citizens for Tax Justice report.

As American families rush to complete their annual tax returns, many will have paid more in federal income taxes than some of America's largest and most profitable corporations. AT&T, Boeing, Citigroup, Duke Energy and Ford collectively reported more than $20 billion of US pre-tax income last year, yet none of them paid a dime in federal income taxes. Instead, they claimed refunds of more than $1.3 billion from the IRS.

These corporations are not alone in turning tax dodging into a competitive sport. Last year, US corporations paid an effective tax rate of just 12.1 percent, the lowest level in the last forty years, according to the Congressional Budget Office. Sixty years ago, when Republican President Dwight Eisenhower lived in the White House, corporations paid 32 percent of federal government's tax receipts; last year they paid 9 percent.

Below are six examples of how large corporations have rigged the tax rules to ensure that those who have the most get to amass even more, at the expense of everyone else. Figuring out how to unrig them is not rocket science, but it will require strong public pressure on lawmakers to ensure that America's most prosperous corporations pay their fair share.

Boeing's Double Dip

In each of the past nine years, Boeing has reported at least $1 billion in pre-tax profits, yet in only one did it pay any US corporate income taxes. In fact, the aerospace giant got so much money in tax subsidies that it had an effective tax rate of -7.8 percent during this period.

One of the main reasons Boeing has avoided the taxman is that the rest of us subsidize their research and development spending. Last year this amounted to $137 million. Congress first passed the research and experimentation tax credit during the 1981 recession, intending to provide a temporary boost to America's sagging economy. Though it has expired for short periods over the years, it has been renewed thirteen times, and Congress is presently considering making the tax credit permanent.

Government investment in basic research and development can be valuable, but the way the current tax credit is structured, much of the support goes to large well-resourced high-tech firms like Boeing that would have conducted the research anyway as a part of maintaining a vibrant business.

What's particularly disturbing about the Boeing subsidies, however, is that the company already bills the Pentagon for research costs. The third largest defense contractor, Boeing has landed more than $54 billion in government contracts in the past nine years. So essentially, taxpayers are paying for the company's research--twice.

GE's Tax-Free Offshore Profits

General Electric employs 975 people to mine the tax code for every possible deduction. One of their IRS returns ran an awe-inspiring 57,000 pages. As a result, GE paid an effective tax rate of just 2.3 percent on more than $81 billion of US income over the last decade.

One of GE's most lucrative tax breaks is dubbed "the active financing exception." Under US tax law income earned from interest anywhere in the world is taxable in the United States. That is because interest is consider a "passive business activity" that is easily transferred from country to country. The active financing exception allows corporation that establish captive foreign finance subsidiaries to exclude interest they earn offshore from their US taxes. The 1997 subsidy was meant as a temporary measure to help US banks and manufacturers compete internationally.

General Electric's lobbyists, who led the fight to create the subsidy, have made sure the "temporary" part was just a joke. Congress has renewed the exemption multiple times over the last fifteen years. And in the meantime, active financing has allowed GE to legally shift much of its US profits to overseas jurisdictions with lower taxes.

The active financing exception is one of sixty tax breaks, known as "tax extenders," that expired last year. Congress is actively considering reauthorizing them, even while they also consider dramatic cuts to social programs.

AIG's Stealth Bailout

In 2008, American International Group's reckless uncovered bets helped lead the global economy to the brink of collapse. Taxpayers bailed out the rogue insurer to the tune of $182 billion.

Less well-known is a perk the US Treasury made available to AIG that allowed the company to retain its losses to offset against future profits. Tapping these tax losses allowed AIG to report more than $17 billion in tax-free profits in 2011, a move Elizabeth Warren, who chaired the TARP oversight panel, labeled a "stealth bailout." "When the government bailed out AIG, it should not have allowed the failed insurance giant to duck taxes for years to come," wrote Warren in a statement co-signed by three other panel members.

"This corporate tax break transfers public money to AIG's private shareholders and inflates executive pay at AIG--both at the public's expense," added Damon Silvers, another member of the oversight panel. At least four of the executives who stand to benefit financially from the tax break were leading the company at the time of the massive failure.

Apple and Facebook's Double Books

Under current rules, companies can show shareholders and the IRS two different sets of books. In financial statements to shareholders, they're allowed to estimate the value for their executives' stock options at the time they're granted. But when it comes to paying their taxes, they can lower their bill by deducting the full value of the options on the day executives cash them in, which is often a much higher figure. This loophole saved Apple $1.5 billion on its taxes between 2008-10, according to Citizens for Tax Justice, boosting its bottom line and its executive bonuses.

When Facebook becomes a public company later this year, the stock option deduction will save it an estimated $3 billion on taxes, including an immediate $500 million IRS refund of the taxes it has paid during the last two years.

The Ending Excessive Corporate Deductions for Stock Options Act (S. 1375) and the Cut Unjustified Tax Loopholes Act (S. 2075), both introduced by Senator Carl Levin (D-MI) would close this loophole and limit companies to a tax deduction no greater than the expense they report to shareholders.

Pfizer Heaves Domestic Profits Overseas

Pfizer is the largest drug company in the world. It generates 40 percent of its sales in the largest and most lucrative drug market--the United States. And yet Pfizer has reported losses in the US in each of the last four years.

Pfizer's tax disclosures offer some clues to how the company achieves this puzzling result. First, it operates eighty subsidiaries in offshore tax havens. Second, Pfizer's 2011 non-US tax rate was a low 14.7 percent, suggesting that they booked a significant portion of overseas profits in tax havens like Luxembourg, Ireland and Jersey, places where Pfizer has at least ten subsidiaries each.

Here's how these strategies work. A company like Pfizer conducts the bulk of its product and research development in the United States. This work is done by scientists, many of whom were educated in US schools, often using basic research that was funded by US taxpayers. The corporation then takes the patents earned by its US labs and registers them in nations that impose little or no taxes on income from patent royalties. When Pfizer sells a pill, it charges a lot for the use of the patent, telling the IRS that without the intellectual property, the product would be virtually worthless. By doing this, Pfizer transfers much of their profits to the tax haven, while retaining much of the costs of research, advertising and management in the United States. Such shenanigans cost the US Treasury an estimated $100 billion a year.

A pending bill, the Stop Tax Haven Abuse Act, would require that offshore subsidiaries managed from the United States and often little more than a post office box and a brass nameplate be treated as US entities for tax purposes.

Bechtel's "Mini" Masquerade

Though Bechtel is the world's largest telecommunications, engineering and construction firm (with $32.9 billion in revenue and 52,700 employees), in terms of corporate structure it is one of America's largest "small businesses." That's because the giant corporation takes advantage of a 1958 law intended to extend limited liability protection to owners of small, family-owned businesses. Companies that qualify for this law's "S Corporation" status do not have to pay federal corporate income taxes. Instead the company's profits are reported as personal income by individual owners. While the Bechtel empire was hardly the intended beneficiary, their firm technically qualifies for the S Corporation status because it is family run and has less than 100 shareholders.

At the time the law was enacted, the wide differential between top corporate tax rates (52 percent) and top individual rates (91 percent) was a disincentive for gaming the system to dodge taxes. Fast forward half a century and top tax rates have collapsed to only 35 percent for corporations and individuals, erasing the previous disincentive for big corporations to change their business status. By incorporating as an S Corporation, enormous businesses like Bechtel pay just individual taxes, rather than having their corporation pay taxes on corporate profits and shareholders pay taxes on their dividends.

S Corporations, and other businesses where income is taxed only at the individual level, have become the new tax haven, where large businesses have fled to avoid US corporate income taxes. In 2008, more than 14,000 S Corporation tax returns were filed by firms with more than $50 million in revenue, according to the IRS. These 14,000 firms, with an average profit of $6.4 million each, collectively reported 29 percent of the total profit on nearly 4 million S Corporation tax returns. Preserving S Corporation status for real small businesses can help level the playing field, but closing the loophole that allows giant multinational corporations to avoid the corporate taxes that their peers have to pay is key to bringing more fairness to the tax code and more funds into public coffers.

As the 99% Spring unfolds, restoring fairness to our tax code must be at the center of the debate. As it stands, our tax system rewards those at the top, robbing the rest of us of the public money we need to transform the economy from one that works for the 1 percent to one that works for the 100 percent.

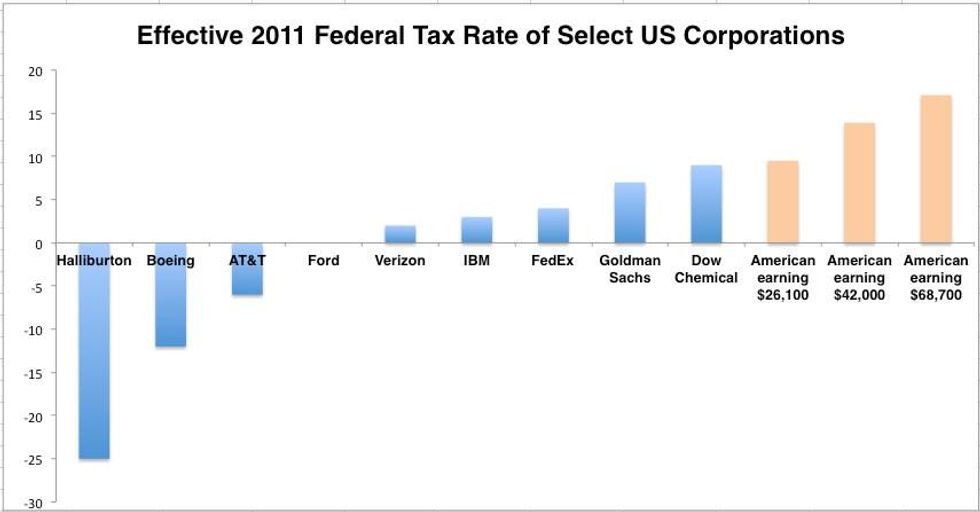

A note on the chart. Corporate tax rates were calculated using current federal corporate income taxes paid in 2011 divided by 2011 US pretax income, as reported in company 10-K annual reported filed with the Securities and Exchange Commission. Deferred taxes, which might be paid some day in the future, were excluded, as were income taxes paid to state or local governments. Individual tax rates were taken from a recent Citizens for Tax Justice report.

As American families rush to complete their annual tax returns, many will have paid more in federal income taxes than some of America's largest and most profitable corporations. AT&T, Boeing, Citigroup, Duke Energy and Ford collectively reported more than $20 billion of US pre-tax income last year, yet none of them paid a dime in federal income taxes. Instead, they claimed refunds of more than $1.3 billion from the IRS.

These corporations are not alone in turning tax dodging into a competitive sport. Last year, US corporations paid an effective tax rate of just 12.1 percent, the lowest level in the last forty years, according to the Congressional Budget Office. Sixty years ago, when Republican President Dwight Eisenhower lived in the White House, corporations paid 32 percent of federal government's tax receipts; last year they paid 9 percent.

Below are six examples of how large corporations have rigged the tax rules to ensure that those who have the most get to amass even more, at the expense of everyone else. Figuring out how to unrig them is not rocket science, but it will require strong public pressure on lawmakers to ensure that America's most prosperous corporations pay their fair share.

Boeing's Double Dip

In each of the past nine years, Boeing has reported at least $1 billion in pre-tax profits, yet in only one did it pay any US corporate income taxes. In fact, the aerospace giant got so much money in tax subsidies that it had an effective tax rate of -7.8 percent during this period.

One of the main reasons Boeing has avoided the taxman is that the rest of us subsidize their research and development spending. Last year this amounted to $137 million. Congress first passed the research and experimentation tax credit during the 1981 recession, intending to provide a temporary boost to America's sagging economy. Though it has expired for short periods over the years, it has been renewed thirteen times, and Congress is presently considering making the tax credit permanent.

Government investment in basic research and development can be valuable, but the way the current tax credit is structured, much of the support goes to large well-resourced high-tech firms like Boeing that would have conducted the research anyway as a part of maintaining a vibrant business.

What's particularly disturbing about the Boeing subsidies, however, is that the company already bills the Pentagon for research costs. The third largest defense contractor, Boeing has landed more than $54 billion in government contracts in the past nine years. So essentially, taxpayers are paying for the company's research--twice.

GE's Tax-Free Offshore Profits

General Electric employs 975 people to mine the tax code for every possible deduction. One of their IRS returns ran an awe-inspiring 57,000 pages. As a result, GE paid an effective tax rate of just 2.3 percent on more than $81 billion of US income over the last decade.

One of GE's most lucrative tax breaks is dubbed "the active financing exception." Under US tax law income earned from interest anywhere in the world is taxable in the United States. That is because interest is consider a "passive business activity" that is easily transferred from country to country. The active financing exception allows corporation that establish captive foreign finance subsidiaries to exclude interest they earn offshore from their US taxes. The 1997 subsidy was meant as a temporary measure to help US banks and manufacturers compete internationally.

General Electric's lobbyists, who led the fight to create the subsidy, have made sure the "temporary" part was just a joke. Congress has renewed the exemption multiple times over the last fifteen years. And in the meantime, active financing has allowed GE to legally shift much of its US profits to overseas jurisdictions with lower taxes.

The active financing exception is one of sixty tax breaks, known as "tax extenders," that expired last year. Congress is actively considering reauthorizing them, even while they also consider dramatic cuts to social programs.

AIG's Stealth Bailout

In 2008, American International Group's reckless uncovered bets helped lead the global economy to the brink of collapse. Taxpayers bailed out the rogue insurer to the tune of $182 billion.

Less well-known is a perk the US Treasury made available to AIG that allowed the company to retain its losses to offset against future profits. Tapping these tax losses allowed AIG to report more than $17 billion in tax-free profits in 2011, a move Elizabeth Warren, who chaired the TARP oversight panel, labeled a "stealth bailout." "When the government bailed out AIG, it should not have allowed the failed insurance giant to duck taxes for years to come," wrote Warren in a statement co-signed by three other panel members.

"This corporate tax break transfers public money to AIG's private shareholders and inflates executive pay at AIG--both at the public's expense," added Damon Silvers, another member of the oversight panel. At least four of the executives who stand to benefit financially from the tax break were leading the company at the time of the massive failure.

Apple and Facebook's Double Books

Under current rules, companies can show shareholders and the IRS two different sets of books. In financial statements to shareholders, they're allowed to estimate the value for their executives' stock options at the time they're granted. But when it comes to paying their taxes, they can lower their bill by deducting the full value of the options on the day executives cash them in, which is often a much higher figure. This loophole saved Apple $1.5 billion on its taxes between 2008-10, according to Citizens for Tax Justice, boosting its bottom line and its executive bonuses.

When Facebook becomes a public company later this year, the stock option deduction will save it an estimated $3 billion on taxes, including an immediate $500 million IRS refund of the taxes it has paid during the last two years.

The Ending Excessive Corporate Deductions for Stock Options Act (S. 1375) and the Cut Unjustified Tax Loopholes Act (S. 2075), both introduced by Senator Carl Levin (D-MI) would close this loophole and limit companies to a tax deduction no greater than the expense they report to shareholders.

Pfizer Heaves Domestic Profits Overseas

Pfizer is the largest drug company in the world. It generates 40 percent of its sales in the largest and most lucrative drug market--the United States. And yet Pfizer has reported losses in the US in each of the last four years.

Pfizer's tax disclosures offer some clues to how the company achieves this puzzling result. First, it operates eighty subsidiaries in offshore tax havens. Second, Pfizer's 2011 non-US tax rate was a low 14.7 percent, suggesting that they booked a significant portion of overseas profits in tax havens like Luxembourg, Ireland and Jersey, places where Pfizer has at least ten subsidiaries each.

Here's how these strategies work. A company like Pfizer conducts the bulk of its product and research development in the United States. This work is done by scientists, many of whom were educated in US schools, often using basic research that was funded by US taxpayers. The corporation then takes the patents earned by its US labs and registers them in nations that impose little or no taxes on income from patent royalties. When Pfizer sells a pill, it charges a lot for the use of the patent, telling the IRS that without the intellectual property, the product would be virtually worthless. By doing this, Pfizer transfers much of their profits to the tax haven, while retaining much of the costs of research, advertising and management in the United States. Such shenanigans cost the US Treasury an estimated $100 billion a year.

A pending bill, the Stop Tax Haven Abuse Act, would require that offshore subsidiaries managed from the United States and often little more than a post office box and a brass nameplate be treated as US entities for tax purposes.

Bechtel's "Mini" Masquerade

Though Bechtel is the world's largest telecommunications, engineering and construction firm (with $32.9 billion in revenue and 52,700 employees), in terms of corporate structure it is one of America's largest "small businesses." That's because the giant corporation takes advantage of a 1958 law intended to extend limited liability protection to owners of small, family-owned businesses. Companies that qualify for this law's "S Corporation" status do not have to pay federal corporate income taxes. Instead the company's profits are reported as personal income by individual owners. While the Bechtel empire was hardly the intended beneficiary, their firm technically qualifies for the S Corporation status because it is family run and has less than 100 shareholders.

At the time the law was enacted, the wide differential between top corporate tax rates (52 percent) and top individual rates (91 percent) was a disincentive for gaming the system to dodge taxes. Fast forward half a century and top tax rates have collapsed to only 35 percent for corporations and individuals, erasing the previous disincentive for big corporations to change their business status. By incorporating as an S Corporation, enormous businesses like Bechtel pay just individual taxes, rather than having their corporation pay taxes on corporate profits and shareholders pay taxes on their dividends.

S Corporations, and other businesses where income is taxed only at the individual level, have become the new tax haven, where large businesses have fled to avoid US corporate income taxes. In 2008, more than 14,000 S Corporation tax returns were filed by firms with more than $50 million in revenue, according to the IRS. These 14,000 firms, with an average profit of $6.4 million each, collectively reported 29 percent of the total profit on nearly 4 million S Corporation tax returns. Preserving S Corporation status for real small businesses can help level the playing field, but closing the loophole that allows giant multinational corporations to avoid the corporate taxes that their peers have to pay is key to bringing more fairness to the tax code and more funds into public coffers.

As the 99% Spring unfolds, restoring fairness to our tax code must be at the center of the debate. As it stands, our tax system rewards those at the top, robbing the rest of us of the public money we need to transform the economy from one that works for the 1 percent to one that works for the 100 percent.

A note on the chart. Corporate tax rates were calculated using current federal corporate income taxes paid in 2011 divided by 2011 US pretax income, as reported in company 10-K annual reported filed with the Securities and Exchange Commission. Deferred taxes, which might be paid some day in the future, were excluded, as were income taxes paid to state or local governments. Individual tax rates were taken from a recent Citizens for Tax Justice report.