Writing in the Guardian newspaper on Saturday, journalist Dan Roberts details how newly released documents from inside the Clinton administration reveal how the president's economic advisors at the time downplayed the possible negative impacts of deregulating Wall Street as they pushed for measures that many critics say ultimately led to the financial crash of 2008.

An additional and troubling aspect of what the documents show is that many of the key players involved with championing the repeal of important laws like the Glass-Steagall Act--passed in the wake of the Great Depression to separate investment services from commercial banking--continue to hold sway and influence inside the Obama White House.

Released by the Clinton Library on Friday as part of a large declassification of presidential documents, Roberts' reporting shows how these specific internal memos reveal how top-level advisers tried to pressure Clinton to follow their advice on Wall Street deregulation. In addition, read carefully, portions of the hand-written notes show the pro-active manner by which the Clinton team kept aspects of their motivations--which included providing preferential treatment to large financial firms like Citigroup--out of the public record.

As Roberts reports:

A Financial Services Modernization Act was passed by Congress in 1999, giving retrospective clearance to the 1998 merger of Citigroup and Travelers Group and unleashing a wave of Wall Street consolidation that was later blamed for forcing taxpayers to spend billions bailing out the enlarged banks after the sub-prime mortgage crisis.

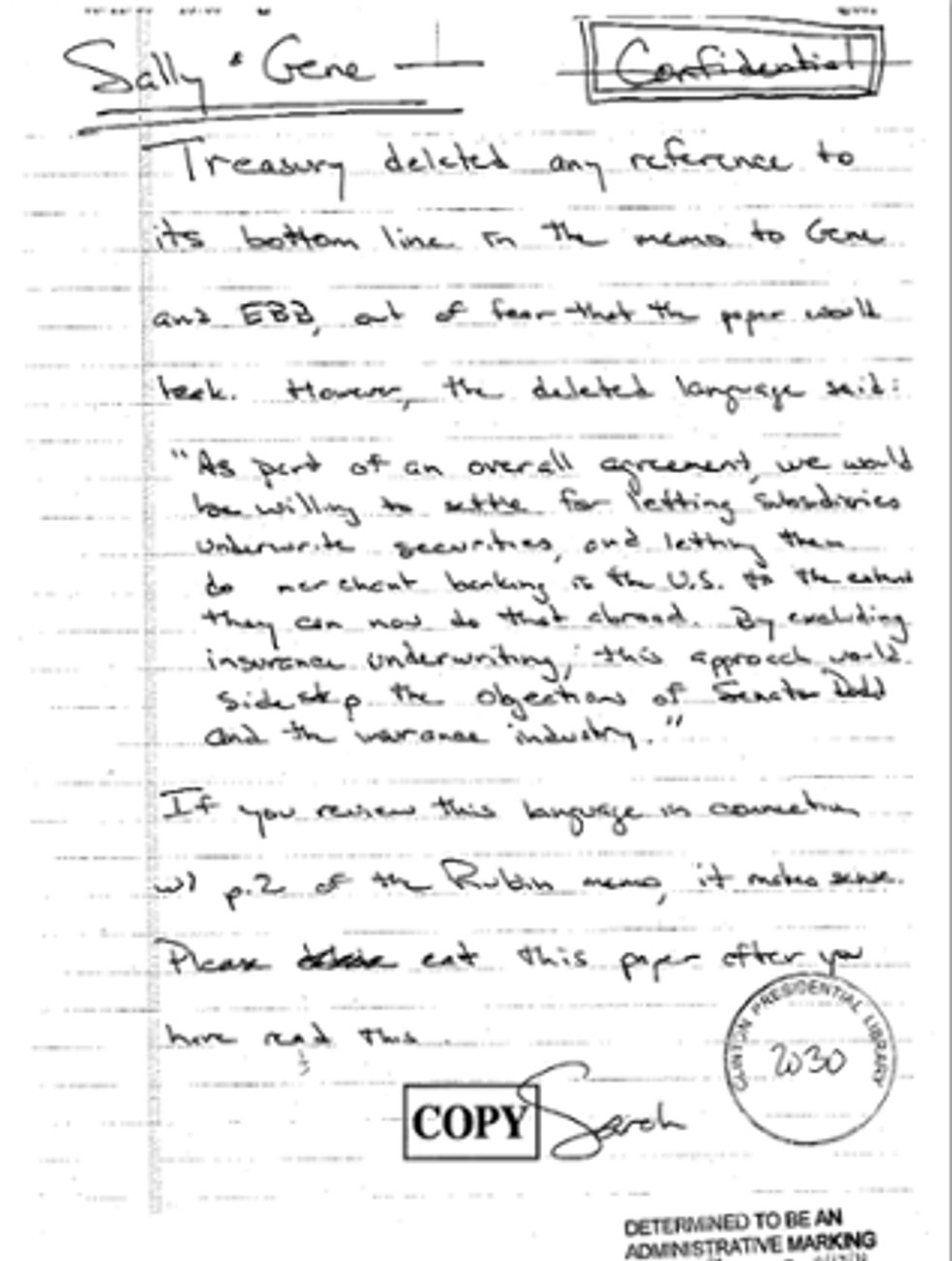

The White House papers show only limited discussion of the risks of such deregulation, but include a private note which reveals that details of a deal with Citigroup to clear its merger in advance of the legislation were deleted from official documents, for fear of it leaking out.

"Please eat this paper after you have read this," jokes the hand-written 1998 note addressed to Gene Sperling, then director of Clinton's National Economic Council.

Earlier, in February 1995, newly-appointed Treasury secretary Robert Rubin, his deputy Bo Cutter and senior advisers including John Podesta gave the president three days to decide whether to back a repeal of Glass-Steagall.

The reporting goes on to point out the prominent role these Clinton advisers--Rubin, Sperling, and Podesta--played and continue to play in the Obama administration.

"The closeness of Obama's team to the deregulation policies of the late 1990s is well known and has been criticized by campaigners as a reason for the current administration's reluctance to institute more aggressive Wall Street reforms after the banking crash," writes Roberts. "But the new documents cast fresh light on the way the White House was first ushered toward deregulation by the tight group of Rubin allies."

Whether it reflects poorly or favorably on the legacy of Bill Clinton, the nature of some of Rubin's advice on the issue makes it appear that the president was urged to stand aside so that the Treasury Secretary himself could take the lead on the reforms.

"Should you approve our recommendation to move forward, the proposal would be a Treasury initiative, and would not require a significant time commitment from the White House," writes the Treasury secretary in one memo.

"I and my staff will manage the process of advancing the proposal," Rubin wrote.

After leaving the White House, Rubin went on to work for Citigroup as adviser and then chairman for which, according to records, he was compensated more than $120 million in cash and stock for his services.

________________________________

Writing in the Guardian newspaper on Saturday, journalist Dan Roberts details how newly released documents from inside the Clinton administration reveal how the president's economic advisors at the time downplayed the possible negative impacts of deregulating Wall Street as they pushed for measures that many critics say ultimately led to the financial crash of 2008.

An additional and troubling aspect of what the documents show is that many of the key players involved with championing the repeal of important laws like the Glass-Steagall Act--passed in the wake of the Great Depression to separate investment services from commercial banking--continue to hold sway and influence inside the Obama White House.

Released by the Clinton Library on Friday as part of a large declassification of presidential documents, Roberts' reporting shows how these specific internal memos reveal how top-level advisers tried to pressure Clinton to follow their advice on Wall Street deregulation. In addition, read carefully, portions of the hand-written notes show the pro-active manner by which the Clinton team kept aspects of their motivations--which included providing preferential treatment to large financial firms like Citigroup--out of the public record.

As Roberts reports:

A Financial Services Modernization Act was passed by Congress in 1999, giving retrospective clearance to the 1998 merger of Citigroup and Travelers Group and unleashing a wave of Wall Street consolidation that was later blamed for forcing taxpayers to spend billions bailing out the enlarged banks after the sub-prime mortgage crisis.

The White House papers show only limited discussion of the risks of such deregulation, but include a private note which reveals that details of a deal with Citigroup to clear its merger in advance of the legislation were deleted from official documents, for fear of it leaking out.

"Please eat this paper after you have read this," jokes the hand-written 1998 note addressed to Gene Sperling, then director of Clinton's National Economic Council.

Earlier, in February 1995, newly-appointed Treasury secretary Robert Rubin, his deputy Bo Cutter and senior advisers including John Podesta gave the president three days to decide whether to back a repeal of Glass-Steagall.

The reporting goes on to point out the prominent role these Clinton advisers--Rubin, Sperling, and Podesta--played and continue to play in the Obama administration.

"The closeness of Obama's team to the deregulation policies of the late 1990s is well known and has been criticized by campaigners as a reason for the current administration's reluctance to institute more aggressive Wall Street reforms after the banking crash," writes Roberts. "But the new documents cast fresh light on the way the White House was first ushered toward deregulation by the tight group of Rubin allies."

Whether it reflects poorly or favorably on the legacy of Bill Clinton, the nature of some of Rubin's advice on the issue makes it appear that the president was urged to stand aside so that the Treasury Secretary himself could take the lead on the reforms.

"Should you approve our recommendation to move forward, the proposal would be a Treasury initiative, and would not require a significant time commitment from the White House," writes the Treasury secretary in one memo.

"I and my staff will manage the process of advancing the proposal," Rubin wrote.

After leaving the White House, Rubin went on to work for Citigroup as adviser and then chairman for which, according to records, he was compensated more than $120 million in cash and stock for his services.

________________________________

Writing in the Guardian newspaper on Saturday, journalist Dan Roberts details how newly released documents from inside the Clinton administration reveal how the president's economic advisors at the time downplayed the possible negative impacts of deregulating Wall Street as they pushed for measures that many critics say ultimately led to the financial crash of 2008.

An additional and troubling aspect of what the documents show is that many of the key players involved with championing the repeal of important laws like the Glass-Steagall Act--passed in the wake of the Great Depression to separate investment services from commercial banking--continue to hold sway and influence inside the Obama White House.

Released by the Clinton Library on Friday as part of a large declassification of presidential documents, Roberts' reporting shows how these specific internal memos reveal how top-level advisers tried to pressure Clinton to follow their advice on Wall Street deregulation. In addition, read carefully, portions of the hand-written notes show the pro-active manner by which the Clinton team kept aspects of their motivations--which included providing preferential treatment to large financial firms like Citigroup--out of the public record.

As Roberts reports:

A Financial Services Modernization Act was passed by Congress in 1999, giving retrospective clearance to the 1998 merger of Citigroup and Travelers Group and unleashing a wave of Wall Street consolidation that was later blamed for forcing taxpayers to spend billions bailing out the enlarged banks after the sub-prime mortgage crisis.

The White House papers show only limited discussion of the risks of such deregulation, but include a private note which reveals that details of a deal with Citigroup to clear its merger in advance of the legislation were deleted from official documents, for fear of it leaking out.

"Please eat this paper after you have read this," jokes the hand-written 1998 note addressed to Gene Sperling, then director of Clinton's National Economic Council.

Earlier, in February 1995, newly-appointed Treasury secretary Robert Rubin, his deputy Bo Cutter and senior advisers including John Podesta gave the president three days to decide whether to back a repeal of Glass-Steagall.

The reporting goes on to point out the prominent role these Clinton advisers--Rubin, Sperling, and Podesta--played and continue to play in the Obama administration.

"The closeness of Obama's team to the deregulation policies of the late 1990s is well known and has been criticized by campaigners as a reason for the current administration's reluctance to institute more aggressive Wall Street reforms after the banking crash," writes Roberts. "But the new documents cast fresh light on the way the White House was first ushered toward deregulation by the tight group of Rubin allies."

Whether it reflects poorly or favorably on the legacy of Bill Clinton, the nature of some of Rubin's advice on the issue makes it appear that the president was urged to stand aside so that the Treasury Secretary himself could take the lead on the reforms.

"Should you approve our recommendation to move forward, the proposal would be a Treasury initiative, and would not require a significant time commitment from the White House," writes the Treasury secretary in one memo.

"I and my staff will manage the process of advancing the proposal," Rubin wrote.

After leaving the White House, Rubin went on to work for Citigroup as adviser and then chairman for which, according to records, he was compensated more than $120 million in cash and stock for his services.

________________________________