Since July 4, we have been reading in major world newspapers and in statements by legislators, central banks, and judicial authorities, that there is a "scandal" about something called LIBOR. Before that time, few persons outside the group concerned with banking had even heard of LIBOR. Suddenly, we were being told that major banks in Great Britain, the United States, Switzerland, Germany, France, and probably a number of other countries had engaged in actions that were allegedly "fraudulent."

Furthermore, we were being told that this was not a matter of pennies. Financial derivatives of hundreds of trillions of dollars are based on the LIBOR rates. The charge was that banks "manipulated" the LIBOR rate, with the consequence not only that they made incredible profits, but that persons who were paying for mortgages on their loans or students who were repaying loans were paying far more than they would have otherwise. In short, the banks were in effect gaining enormously at the expense of others who were losing enormously.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system.

This has led to many questions. (1) How was this possible? (2) Why didn't regulatory authorities stop a practice that is now said to be fraudulent, or who knew what when? And (3) can anything now be done to make sure that this doesn't happen again?

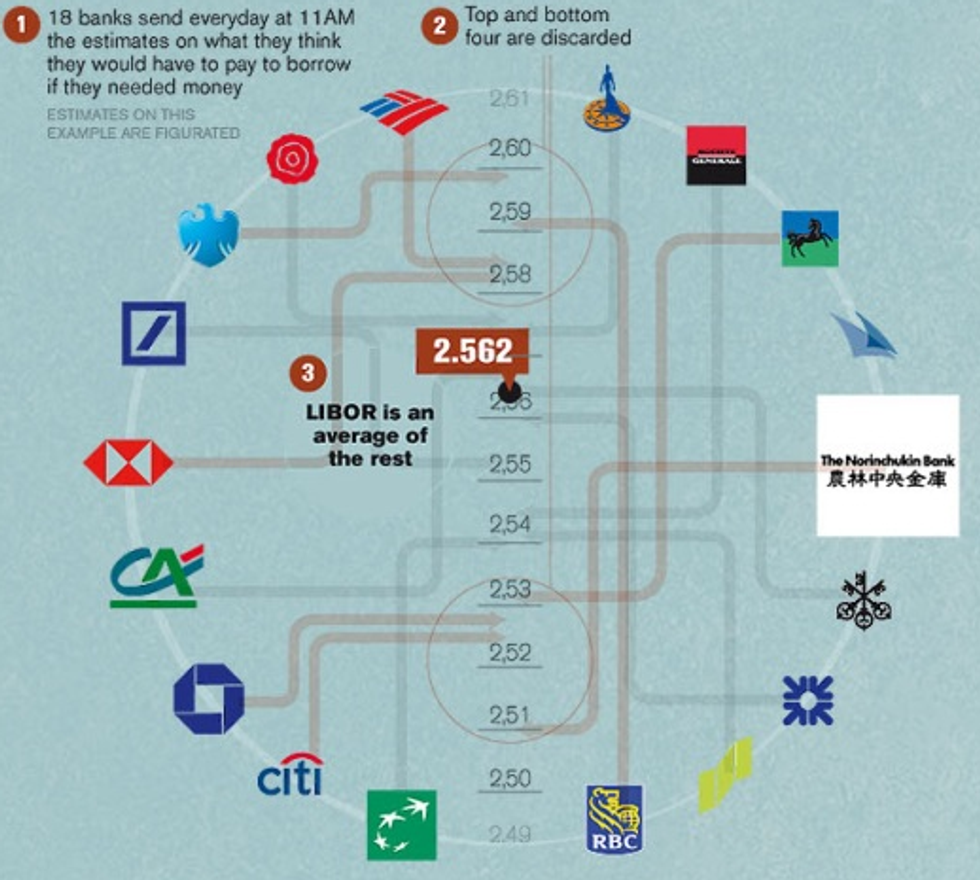

Let's start with what the LIBOR rate is. It stands for London Interbank Offered Rate. It is not that old. Its definitive version dates only to 1986. The British Bankers Association at that time required that "leading banks" share information each weekday on the interest rate they would be charged if borrowing from other banks. After eliminating outliers, an average rate was determined, and changed daily. The idea was that if banks felt confident about the state of the economy, the rate would be lower, and if they were less confident, the rate would be higher.

Once the world press used the word "scandal" to talk about the LIBOR rate, it came out that there had been much earlier public discussion in less observed places. It seems that the Wall Street Journal had released a study on May 29, 2008 (yes 2008) suggesting that some banks had been understating borrowing costs. Of course there were immediately others who said this was inaccurate or, if accurate, inadvertent. There were subsequent scholarly analyses that suggested however that the charge of understatement of costs was in fact true.

The point was that when a bank is dealing with $50 trillion of so-called notional values, a slight underreporting of rates generates a significant increase in profit immediately. So temptation was obvious. It turns out that, as early as 2007, both the Federal Reserve Bank and the Bank of England suspected the underreporting. Neither did very much about it.

We are now being told that these rates, far from being reliable or stable, are really "guesswork." Once Lehman Brothers collapsed, banks throughout the world largely stopped lending to each other. So, as the New York Times put it in its story of July 19, 2012, "the precise rates have little basis in reality." In 2011, the U.S. Justice Department began a criminal investigation. As a result of leaks, we now know there were email exchanges between the bankers gleefully talking about, and encouraging, the underreporting of the rates. Why not? They were making a lot of money.

In the middle of all this, the Independent ran a two-page spread on tax havens, and the incredible amounts of money that are shipped out of countries of the global South to these tax havens, thereby depriving these countries of probably more than enough to finance much of the kind of economic transformation and social redistribution they say they want to do. Unlike fraudulently setting LIBOR rates, the tax havens are actually legal.

So, where is the scandal? Both practices - manipulating LIBOR rates and transferring money to tax havens - are absolutely normal practices in a capitalist world-economy. The object of capitalism is after all the accumulation of capital - the more the better. A capitalist who doesn't maximize revenue, one way or the other, will sooner or later be eliminated from the game.

The role of the states has never been to control or limit these practices, but to wink at them for as long as they can. Every once in a while, the practices - of the capitalists and of the states - gets momentarily exposed. A few people go to jail, or are forced to return the technically illegal profits. And politicians talk of reform - seeking to adopt with great fanfare the lowest level of "reform" they can get away with.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system. Will this ever change? Yes, of course. One day the system will be no more. Of course that opens another question. Will the successor system be better? It's possible, but far from certain.

In the meantime, to call the LIBOR manipulations a scandal is to draw our attention away from the fact that it is simply one more normal way of accumulating capital. In 1992, James Carville, campaign strategist for Bill Clinton, then running for U.S. president, famously said, "It's the economy, stupid." Faced with the so-called scandals, we ought to be saying, "It's the system, stupid."

Since July 4, we have been reading in major world newspapers and in statements by legislators, central banks, and judicial authorities, that there is a "scandal" about something called LIBOR. Before that time, few persons outside the group concerned with banking had even heard of LIBOR. Suddenly, we were being told that major banks in Great Britain, the United States, Switzerland, Germany, France, and probably a number of other countries had engaged in actions that were allegedly "fraudulent."

Furthermore, we were being told that this was not a matter of pennies. Financial derivatives of hundreds of trillions of dollars are based on the LIBOR rates. The charge was that banks "manipulated" the LIBOR rate, with the consequence not only that they made incredible profits, but that persons who were paying for mortgages on their loans or students who were repaying loans were paying far more than they would have otherwise. In short, the banks were in effect gaining enormously at the expense of others who were losing enormously.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system.

This has led to many questions. (1) How was this possible? (2) Why didn't regulatory authorities stop a practice that is now said to be fraudulent, or who knew what when? And (3) can anything now be done to make sure that this doesn't happen again?

Let's start with what the LIBOR rate is. It stands for London Interbank Offered Rate. It is not that old. Its definitive version dates only to 1986. The British Bankers Association at that time required that "leading banks" share information each weekday on the interest rate they would be charged if borrowing from other banks. After eliminating outliers, an average rate was determined, and changed daily. The idea was that if banks felt confident about the state of the economy, the rate would be lower, and if they were less confident, the rate would be higher.

Once the world press used the word "scandal" to talk about the LIBOR rate, it came out that there had been much earlier public discussion in less observed places. It seems that the Wall Street Journal had released a study on May 29, 2008 (yes 2008) suggesting that some banks had been understating borrowing costs. Of course there were immediately others who said this was inaccurate or, if accurate, inadvertent. There were subsequent scholarly analyses that suggested however that the charge of understatement of costs was in fact true.

The point was that when a bank is dealing with $50 trillion of so-called notional values, a slight underreporting of rates generates a significant increase in profit immediately. So temptation was obvious. It turns out that, as early as 2007, both the Federal Reserve Bank and the Bank of England suspected the underreporting. Neither did very much about it.

We are now being told that these rates, far from being reliable or stable, are really "guesswork." Once Lehman Brothers collapsed, banks throughout the world largely stopped lending to each other. So, as the New York Times put it in its story of July 19, 2012, "the precise rates have little basis in reality." In 2011, the U.S. Justice Department began a criminal investigation. As a result of leaks, we now know there were email exchanges between the bankers gleefully talking about, and encouraging, the underreporting of the rates. Why not? They were making a lot of money.

In the middle of all this, the Independent ran a two-page spread on tax havens, and the incredible amounts of money that are shipped out of countries of the global South to these tax havens, thereby depriving these countries of probably more than enough to finance much of the kind of economic transformation and social redistribution they say they want to do. Unlike fraudulently setting LIBOR rates, the tax havens are actually legal.

So, where is the scandal? Both practices - manipulating LIBOR rates and transferring money to tax havens - are absolutely normal practices in a capitalist world-economy. The object of capitalism is after all the accumulation of capital - the more the better. A capitalist who doesn't maximize revenue, one way or the other, will sooner or later be eliminated from the game.

The role of the states has never been to control or limit these practices, but to wink at them for as long as they can. Every once in a while, the practices - of the capitalists and of the states - gets momentarily exposed. A few people go to jail, or are forced to return the technically illegal profits. And politicians talk of reform - seeking to adopt with great fanfare the lowest level of "reform" they can get away with.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system. Will this ever change? Yes, of course. One day the system will be no more. Of course that opens another question. Will the successor system be better? It's possible, but far from certain.

In the meantime, to call the LIBOR manipulations a scandal is to draw our attention away from the fact that it is simply one more normal way of accumulating capital. In 1992, James Carville, campaign strategist for Bill Clinton, then running for U.S. president, famously said, "It's the economy, stupid." Faced with the so-called scandals, we ought to be saying, "It's the system, stupid."

Since July 4, we have been reading in major world newspapers and in statements by legislators, central banks, and judicial authorities, that there is a "scandal" about something called LIBOR. Before that time, few persons outside the group concerned with banking had even heard of LIBOR. Suddenly, we were being told that major banks in Great Britain, the United States, Switzerland, Germany, France, and probably a number of other countries had engaged in actions that were allegedly "fraudulent."

Furthermore, we were being told that this was not a matter of pennies. Financial derivatives of hundreds of trillions of dollars are based on the LIBOR rates. The charge was that banks "manipulated" the LIBOR rate, with the consequence not only that they made incredible profits, but that persons who were paying for mortgages on their loans or students who were repaying loans were paying far more than they would have otherwise. In short, the banks were in effect gaining enormously at the expense of others who were losing enormously.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system.

This has led to many questions. (1) How was this possible? (2) Why didn't regulatory authorities stop a practice that is now said to be fraudulent, or who knew what when? And (3) can anything now be done to make sure that this doesn't happen again?

Let's start with what the LIBOR rate is. It stands for London Interbank Offered Rate. It is not that old. Its definitive version dates only to 1986. The British Bankers Association at that time required that "leading banks" share information each weekday on the interest rate they would be charged if borrowing from other banks. After eliminating outliers, an average rate was determined, and changed daily. The idea was that if banks felt confident about the state of the economy, the rate would be lower, and if they were less confident, the rate would be higher.

Once the world press used the word "scandal" to talk about the LIBOR rate, it came out that there had been much earlier public discussion in less observed places. It seems that the Wall Street Journal had released a study on May 29, 2008 (yes 2008) suggesting that some banks had been understating borrowing costs. Of course there were immediately others who said this was inaccurate or, if accurate, inadvertent. There were subsequent scholarly analyses that suggested however that the charge of understatement of costs was in fact true.

The point was that when a bank is dealing with $50 trillion of so-called notional values, a slight underreporting of rates generates a significant increase in profit immediately. So temptation was obvious. It turns out that, as early as 2007, both the Federal Reserve Bank and the Bank of England suspected the underreporting. Neither did very much about it.

We are now being told that these rates, far from being reliable or stable, are really "guesswork." Once Lehman Brothers collapsed, banks throughout the world largely stopped lending to each other. So, as the New York Times put it in its story of July 19, 2012, "the precise rates have little basis in reality." In 2011, the U.S. Justice Department began a criminal investigation. As a result of leaks, we now know there were email exchanges between the bankers gleefully talking about, and encouraging, the underreporting of the rates. Why not? They were making a lot of money.

In the middle of all this, the Independent ran a two-page spread on tax havens, and the incredible amounts of money that are shipped out of countries of the global South to these tax havens, thereby depriving these countries of probably more than enough to finance much of the kind of economic transformation and social redistribution they say they want to do. Unlike fraudulently setting LIBOR rates, the tax havens are actually legal.

So, where is the scandal? Both practices - manipulating LIBOR rates and transferring money to tax havens - are absolutely normal practices in a capitalist world-economy. The object of capitalism is after all the accumulation of capital - the more the better. A capitalist who doesn't maximize revenue, one way or the other, will sooner or later be eliminated from the game.

The role of the states has never been to control or limit these practices, but to wink at them for as long as they can. Every once in a while, the practices - of the capitalists and of the states - gets momentarily exposed. A few people go to jail, or are forced to return the technically illegal profits. And politicians talk of reform - seeking to adopt with great fanfare the lowest level of "reform" they can get away with.

But this is not a scandal, because what is called "scandal" is in fact the heart of the system. Will this ever change? Yes, of course. One day the system will be no more. Of course that opens another question. Will the successor system be better? It's possible, but far from certain.

In the meantime, to call the LIBOR manipulations a scandal is to draw our attention away from the fact that it is simply one more normal way of accumulating capital. In 1992, James Carville, campaign strategist for Bill Clinton, then running for U.S. president, famously said, "It's the economy, stupid." Faced with the so-called scandals, we ought to be saying, "It's the system, stupid."