SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

On Friday at midnight, the sequester kicked in, triggering $85 billion in deep, dumb budget cuts that sent "nonessential personnel"-- such as air traffic controllers -- packing.

Not to worry, though: Wall Street's day was pretty much like any other. Billions of dollars in profits were made off of trillions of dollars in financial transactions. And the vast majority of those transactions were conducted tax-free.

Moral of the story: What else is new?

Crash the economy? Free pass. Prevent planes from crashing? Pink slip.

We don't need a team of policymakers to tell us this isn't good policy, or that it needs changing. But on Thursday, we heard policymakers propose exactly that: a change.

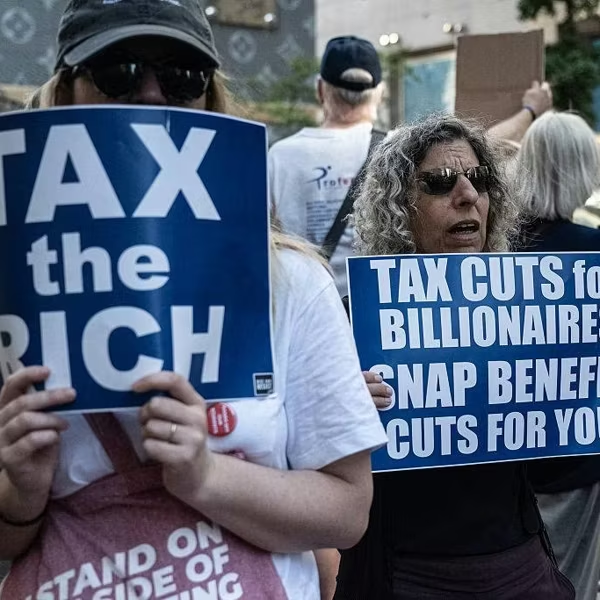

Sens. Tom Harkin (D-Iowa) and Sheldon Whitehouse (D-R.I.), along with Rep. Pete DeFazio (D-Ore.), unveiled a bill that would place a light tax on all financial transactions -- three pennies on every $100 traded.

The good news is that it's a tax so small it could be mistaken for a rounding error. It's so small, Wall Street could easily afford it and the average E-Trade investor would barely notice it. If this were a tax on coffee, it would cost you $1 for every 800 cups you bought at Starbucks.

But there's even better news. This insignificant tax raises a significant amount of revenue -- $352 billion over the next 10 years, or enough to refund about one-third of what the sequester will slash from the federal budget. It's also enough to put many air traffic controllers back to work, Head Start teachers back in preschools, and crucial government programs back in business.

As the saying goes, "Nothing can resist an idea whose time has come."

And after years of Wall Street excess, and at a moment when new revenues are badly needed, the time has surely come for a financial transaction tax .

Indeed, support for such a tax has never been stronger -- or broader. Many on the progressive left have long favored it . Now, though, another group of bleeding-heart liberals, otherwise known as the American people, is on board. When it comes to cutting the deficit, 6 in 10 Americans prefer taxing the financial industry to cutting social spending.

But this idea doesn't just have the masses on its side; it has the elites, and even some Republican elites. Once championed by the granddaddy of liberal economics, John Maynard Keynes, the banner of a financial transactions tax has been picked up by conservative economists including Sheila Bair, George W. Bush's appointee to the Federal Deposit Insurance Corp.

After all, the tax isn't just a good revenue raiser. It's smart regulatory reform.

The high-frequency traders that now dominate our markets would be hardest-hit by the tax. A top economist recently concluded that their lightning speed, algorithm-driven trading drains profits from traditional investors. And analysts fear that such mass trading strategies could lead to disaster if markets behave unexpectedly.

The new tax would discourage these kinds of trades, which would be a good thing.

Europe, at least, seems to agree. Eleven nations, led by the conservative German government, are on track to start collecting the tax by January 2014. Expected revenues: $50 billion per year.

Of course, we're talking about a tax on Wall Street.

It's no wonder that, over the past few weeks, K Street appears to have upped the financial sector's retainer. Their lobbying effort against the tax -- here and in Europe -- is in full swing.

Even the Obama administration has been convinced to come out against the tax in the United States. And they're pressuring Europeans to water down their version by insulating American banks. What's the logic driving this opposition?

Some have argued that, historically, these taxes have been ineffective because of widespread evasion. But they're cherry-picking a few badly designed examples, such as Sweden's lemon of a tax from nearly 30 years ago. This is like saying cars don't work because you bought a Datsun in the '70s.

Many countries have implemented such taxes effectively. The United Kingdom, for example, manages to raise more than $5 billion per year on a 0.5 percent tax on stock trades alone.

Another common argument is that the tax will be passed on to mom-and-pop investors. The just-introduced U.S. legislation addresses these concerns by providing tax credits for contributions to typical middle-class investment accounts, including 401(k)s. Investment funds would still be taxed on their trades, but this could encourage longer-term productive investment instead of the short-term speculation that adds little to no value to the real economy.

If the Obama administration is serious about fair taxation and a smart approach to the deficit, it should change its position. Rather than trying to derail Europe's efforts, it should cooperate with Europe to ensure that the tax there is effectively enforced. And the administration should build support in Congress, including among Republicans.

Yes, we've all heard House Speaker John Boehner's line that the debate over revenue raising is over. We also remember former President George H.W. Bush's line, "Read my lips, no new taxes," and how quickly his lips starting saying something else.

For tea partyers, wouldn't a tax on Wall Street, the beneficiaries of the bailout they so reviled, be less objectionable than most other revenue options?

Sequestration is a septic wound, self-inflicted by lawmakers who can't agree on anything. Here, at last, we have a smart idea with widespread support -- Americans and Europeans, populists and economists, progressives and conservatives.

After Friday's dumb budget cuts, a little smart policymaking would be nice for a change.

On Friday at midnight, the sequester kicked in, triggering $85 billion in deep, dumb budget cuts that sent "nonessential personnel"-- such as air traffic controllers -- packing.

Not to worry, though: Wall Street's day was pretty much like any other. Billions of dollars in profits were made off of trillions of dollars in financial transactions. And the vast majority of those transactions were conducted tax-free.

Moral of the story: What else is new?

Crash the economy? Free pass. Prevent planes from crashing? Pink slip.

We don't need a team of policymakers to tell us this isn't good policy, or that it needs changing. But on Thursday, we heard policymakers propose exactly that: a change.

Sens. Tom Harkin (D-Iowa) and Sheldon Whitehouse (D-R.I.), along with Rep. Pete DeFazio (D-Ore.), unveiled a bill that would place a light tax on all financial transactions -- three pennies on every $100 traded.

The good news is that it's a tax so small it could be mistaken for a rounding error. It's so small, Wall Street could easily afford it and the average E-Trade investor would barely notice it. If this were a tax on coffee, it would cost you $1 for every 800 cups you bought at Starbucks.

But there's even better news. This insignificant tax raises a significant amount of revenue -- $352 billion over the next 10 years, or enough to refund about one-third of what the sequester will slash from the federal budget. It's also enough to put many air traffic controllers back to work, Head Start teachers back in preschools, and crucial government programs back in business.

As the saying goes, "Nothing can resist an idea whose time has come."

And after years of Wall Street excess, and at a moment when new revenues are badly needed, the time has surely come for a financial transaction tax .

Indeed, support for such a tax has never been stronger -- or broader. Many on the progressive left have long favored it . Now, though, another group of bleeding-heart liberals, otherwise known as the American people, is on board. When it comes to cutting the deficit, 6 in 10 Americans prefer taxing the financial industry to cutting social spending.

But this idea doesn't just have the masses on its side; it has the elites, and even some Republican elites. Once championed by the granddaddy of liberal economics, John Maynard Keynes, the banner of a financial transactions tax has been picked up by conservative economists including Sheila Bair, George W. Bush's appointee to the Federal Deposit Insurance Corp.

After all, the tax isn't just a good revenue raiser. It's smart regulatory reform.

The high-frequency traders that now dominate our markets would be hardest-hit by the tax. A top economist recently concluded that their lightning speed, algorithm-driven trading drains profits from traditional investors. And analysts fear that such mass trading strategies could lead to disaster if markets behave unexpectedly.

The new tax would discourage these kinds of trades, which would be a good thing.

Europe, at least, seems to agree. Eleven nations, led by the conservative German government, are on track to start collecting the tax by January 2014. Expected revenues: $50 billion per year.

Of course, we're talking about a tax on Wall Street.

It's no wonder that, over the past few weeks, K Street appears to have upped the financial sector's retainer. Their lobbying effort against the tax -- here and in Europe -- is in full swing.

Even the Obama administration has been convinced to come out against the tax in the United States. And they're pressuring Europeans to water down their version by insulating American banks. What's the logic driving this opposition?

Some have argued that, historically, these taxes have been ineffective because of widespread evasion. But they're cherry-picking a few badly designed examples, such as Sweden's lemon of a tax from nearly 30 years ago. This is like saying cars don't work because you bought a Datsun in the '70s.

Many countries have implemented such taxes effectively. The United Kingdom, for example, manages to raise more than $5 billion per year on a 0.5 percent tax on stock trades alone.

Another common argument is that the tax will be passed on to mom-and-pop investors. The just-introduced U.S. legislation addresses these concerns by providing tax credits for contributions to typical middle-class investment accounts, including 401(k)s. Investment funds would still be taxed on their trades, but this could encourage longer-term productive investment instead of the short-term speculation that adds little to no value to the real economy.

If the Obama administration is serious about fair taxation and a smart approach to the deficit, it should change its position. Rather than trying to derail Europe's efforts, it should cooperate with Europe to ensure that the tax there is effectively enforced. And the administration should build support in Congress, including among Republicans.

Yes, we've all heard House Speaker John Boehner's line that the debate over revenue raising is over. We also remember former President George H.W. Bush's line, "Read my lips, no new taxes," and how quickly his lips starting saying something else.

For tea partyers, wouldn't a tax on Wall Street, the beneficiaries of the bailout they so reviled, be less objectionable than most other revenue options?

Sequestration is a septic wound, self-inflicted by lawmakers who can't agree on anything. Here, at last, we have a smart idea with widespread support -- Americans and Europeans, populists and economists, progressives and conservatives.

After Friday's dumb budget cuts, a little smart policymaking would be nice for a change.

On Friday at midnight, the sequester kicked in, triggering $85 billion in deep, dumb budget cuts that sent "nonessential personnel"-- such as air traffic controllers -- packing.

Not to worry, though: Wall Street's day was pretty much like any other. Billions of dollars in profits were made off of trillions of dollars in financial transactions. And the vast majority of those transactions were conducted tax-free.

Moral of the story: What else is new?

Crash the economy? Free pass. Prevent planes from crashing? Pink slip.

We don't need a team of policymakers to tell us this isn't good policy, or that it needs changing. But on Thursday, we heard policymakers propose exactly that: a change.

Sens. Tom Harkin (D-Iowa) and Sheldon Whitehouse (D-R.I.), along with Rep. Pete DeFazio (D-Ore.), unveiled a bill that would place a light tax on all financial transactions -- three pennies on every $100 traded.

The good news is that it's a tax so small it could be mistaken for a rounding error. It's so small, Wall Street could easily afford it and the average E-Trade investor would barely notice it. If this were a tax on coffee, it would cost you $1 for every 800 cups you bought at Starbucks.

But there's even better news. This insignificant tax raises a significant amount of revenue -- $352 billion over the next 10 years, or enough to refund about one-third of what the sequester will slash from the federal budget. It's also enough to put many air traffic controllers back to work, Head Start teachers back in preschools, and crucial government programs back in business.

As the saying goes, "Nothing can resist an idea whose time has come."

And after years of Wall Street excess, and at a moment when new revenues are badly needed, the time has surely come for a financial transaction tax .

Indeed, support for such a tax has never been stronger -- or broader. Many on the progressive left have long favored it . Now, though, another group of bleeding-heart liberals, otherwise known as the American people, is on board. When it comes to cutting the deficit, 6 in 10 Americans prefer taxing the financial industry to cutting social spending.

But this idea doesn't just have the masses on its side; it has the elites, and even some Republican elites. Once championed by the granddaddy of liberal economics, John Maynard Keynes, the banner of a financial transactions tax has been picked up by conservative economists including Sheila Bair, George W. Bush's appointee to the Federal Deposit Insurance Corp.

After all, the tax isn't just a good revenue raiser. It's smart regulatory reform.

The high-frequency traders that now dominate our markets would be hardest-hit by the tax. A top economist recently concluded that their lightning speed, algorithm-driven trading drains profits from traditional investors. And analysts fear that such mass trading strategies could lead to disaster if markets behave unexpectedly.

The new tax would discourage these kinds of trades, which would be a good thing.

Europe, at least, seems to agree. Eleven nations, led by the conservative German government, are on track to start collecting the tax by January 2014. Expected revenues: $50 billion per year.

Of course, we're talking about a tax on Wall Street.

It's no wonder that, over the past few weeks, K Street appears to have upped the financial sector's retainer. Their lobbying effort against the tax -- here and in Europe -- is in full swing.

Even the Obama administration has been convinced to come out against the tax in the United States. And they're pressuring Europeans to water down their version by insulating American banks. What's the logic driving this opposition?

Some have argued that, historically, these taxes have been ineffective because of widespread evasion. But they're cherry-picking a few badly designed examples, such as Sweden's lemon of a tax from nearly 30 years ago. This is like saying cars don't work because you bought a Datsun in the '70s.

Many countries have implemented such taxes effectively. The United Kingdom, for example, manages to raise more than $5 billion per year on a 0.5 percent tax on stock trades alone.

Another common argument is that the tax will be passed on to mom-and-pop investors. The just-introduced U.S. legislation addresses these concerns by providing tax credits for contributions to typical middle-class investment accounts, including 401(k)s. Investment funds would still be taxed on their trades, but this could encourage longer-term productive investment instead of the short-term speculation that adds little to no value to the real economy.

If the Obama administration is serious about fair taxation and a smart approach to the deficit, it should change its position. Rather than trying to derail Europe's efforts, it should cooperate with Europe to ensure that the tax there is effectively enforced. And the administration should build support in Congress, including among Republicans.

Yes, we've all heard House Speaker John Boehner's line that the debate over revenue raising is over. We also remember former President George H.W. Bush's line, "Read my lips, no new taxes," and how quickly his lips starting saying something else.

For tea partyers, wouldn't a tax on Wall Street, the beneficiaries of the bailout they so reviled, be less objectionable than most other revenue options?

Sequestration is a septic wound, self-inflicted by lawmakers who can't agree on anything. Here, at last, we have a smart idea with widespread support -- Americans and Europeans, populists and economists, progressives and conservatives.

After Friday's dumb budget cuts, a little smart policymaking would be nice for a change.